Southwest Florida Flood Insurance: How to Protect Your Home From Unexpected Floods

Southwest Florida sits in one of the nation’s most flood-prone regions, with hurricane season bringing serious risks to homes every year. Standard homeowners insurance won’t cover flood damage, leaving many residents financially exposed when storms hit.

At Responsive Insurance, Inc., we help homeowners understand their Southwest Florida flood insurance options so they can protect their property and finances. This guide walks you through what coverage you need and how to get it.

Why Flood Insurance Matters in Southwest Florida

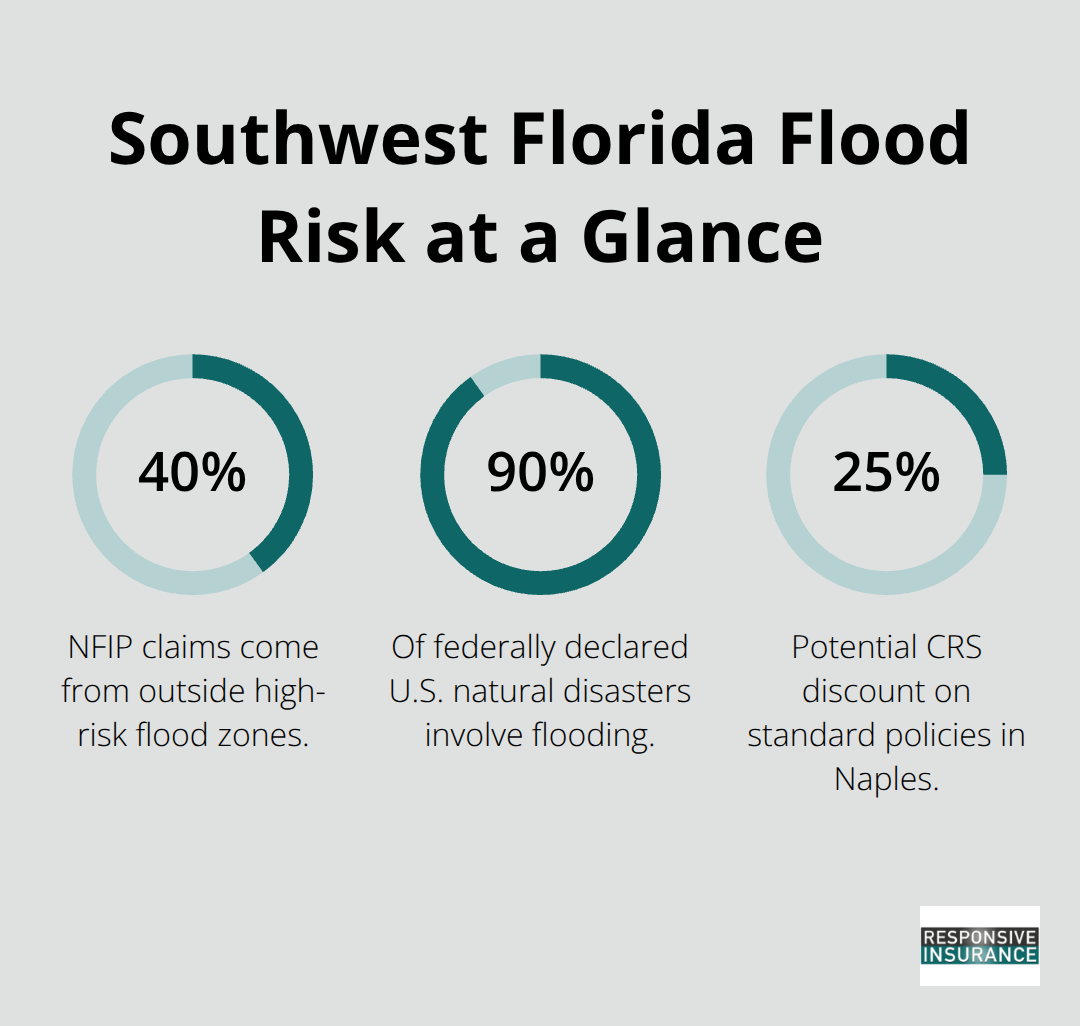

Flood damage costs homeowners in Southwest Florida far more than most realize. The National Flood Insurance Program reports that about 40% of NFIP flood insurance claims come from properties outside high-risk flood zones, meaning your home faces flood risk even if you think you’re safe. Ninety percent of federally declared natural disasters in the U.S. involve flooding, according to FEMA, and Southwest Florida sits directly in the path of hurricane season.

When storms arrive, storm surge combines with heavy rainfall to overwhelm drainage systems and breach levees. Standard homeowners insurance explicitly excludes flood damage, leaving you completely unprotected when water enters your home. Flood losses easily reach $25,000 or more per event, and without insurance, you’ll pay every dollar from your own pocket. Government disaster assistance exists, but it’s not automatic and typically arrives only after an official disaster declaration. Many homeowners who skip flood insurance assume they’ll qualify for federal aid after a flood-this assumption has cost families their life savings.

Your Home Is More Vulnerable Than You Think

Even homes in lower-risk areas flood regularly. In Southwest Florida, Cape Coral residents pay around $1,709 per year for NFIP flood insurance, while those in Charlotte County pay approximately $1,768 annually, reflecting the region’s genuine exposure. The City of Naples has earned a CRS Rating Class 5 with NFIP, which can yield up to a 25% discount on standard policies for residents who take mitigation steps. If your property sits in a Special Flood Hazard Area and you have a federally backed mortgage, flood insurance is mandatory-lenders won’t close without proof of coverage. If you’ve received a federal grant for previous flood losses and want to qualify for future assistance, you must carry flood insurance. This requirement exists because flooding repeats in the same locations. Without coverage, your second flood becomes your financial catastrophe.

What Standard Insurance Actually Covers

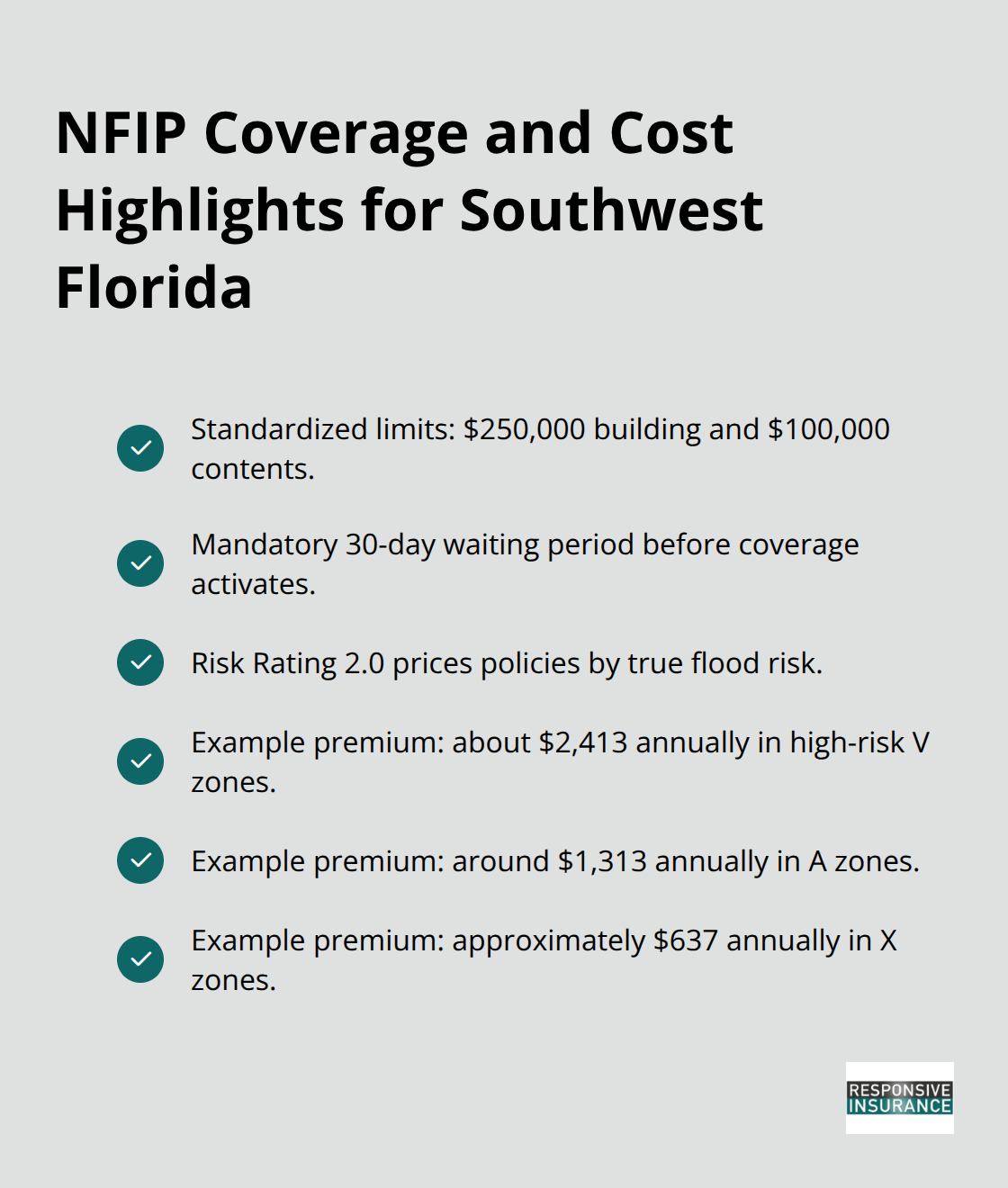

Your homeowners policy covers wind damage from hurricanes, but the moment water enters your home through flooding, your coverage stops. This distinction matters enormously. A hurricane may damage your roof with wind, and homeowners insurance pays for that. But if that same hurricane brings storm surge or heavy rain that floods your basement, homeowners insurance covers nothing. Contents inside your home-furniture, appliances, electronics, clothing-are equally unprotected. Flood insurance fills this gap by covering both structural damage and personal belongings. Building coverage under NFIP protects up to $250,000 for single-family homes, while contents coverage protects up to $100,000. This separation means you control two separate deductibles and can adjust each based on your risk tolerance and budget. Understanding these coverage limits helps you determine whether you need additional protection through private flood insurance or excess policies.

Comparing NFIP and Private Flood Insurance

NFIP Coverage and Costs in Southwest Florida

The National Flood Insurance Program dominates the Southwest Florida market, covering more than 1.7 million policies statewide as of April 2026. NFIP coverage limits of $250,000 for building and $100,000 for contents are standardized, with a mandatory 30-day waiting period before coverage activates. Under Risk Rating 2.0, NFIP premiums now reflect true flood risk rather than zone-based pricing alone. A single-family home in a high-risk V zone costs about $2,413 annually, while homes in lower-risk X zones average $637 per year according to the National Flood Insurance Program.

The program separates building and contents coverage into distinct policies with separate deductibles, which gives you control over how much protection you purchase for your structure versus your belongings.

NFIP policies cover direct physical losses from floodwaters, storm surge, and mudflows but explicitly exclude mold damage and flood-related failures of appliances or burst pipes inside your home. This distinction matters when you file a claim, since water damage from a burst pipe falls under your homeowners policy, not flood insurance.

Private Flood Insurance as an Alternative

Private flood insurers offer an alternative that many Southwest Florida homeowners overlook. These carriers provide higher coverage limits, shorter waiting periods, and potentially lower premiums in lower-risk areas. Some private insurers offer additional living expense coverage or different deductible structures that better match your situation. The trade-off is that private carriers maintain stricter underwriting standards and may decline coverage in the highest-risk zones where NFIP remains available to anyone. Shopping both options matters because a private policy might cost significantly less if your home sits in an X zone or lower-risk area.

Calculating Your Coverage Needs

Determining your coverage amount requires honest assessment of what you own and what replacement would cost. Most Southwest Florida homeowners dramatically underestimate their contents value. Furniture alone in a typical home exceeds $15,000, and adding clothing, electronics, artwork, and appliances easily pushes total contents to $40,000 or more. NFIP contents coverage maxes at $100,000, which sounds generous until you price replacement after a flood.

An elevation certificate documents your home’s lowest floor elevation and can lower your premium substantially (typically costing $400 to $750 through a qualified surveyor). If your home sits in a Special Flood Hazard Area, your mortgage lender already requires flood insurance, so your decision focuses on whether NFIP limits suffice or whether excess coverage makes sense.

Mitigation Steps That Lower Premiums

Many homeowners in Charlotte County, Cape Coral, and Naples reduce their premiums through mitigation steps, including elevating utilities, installing flood vents, or filling basements. Your agent can model how these improvements affect your annual cost and whether the savings justify the upfront investment. Comparing quotes from multiple insurers reveals significant price differences for the same NFIP policy, since each insurer handles your policy differently. The right coverage choice depends on your property’s specific risk profile and your financial situation-factors that shift when you move to a new flood zone or make home improvements that reduce your exposure.

Getting Flood Insurance in Southwest Florida

Know Your Flood Risk Zone

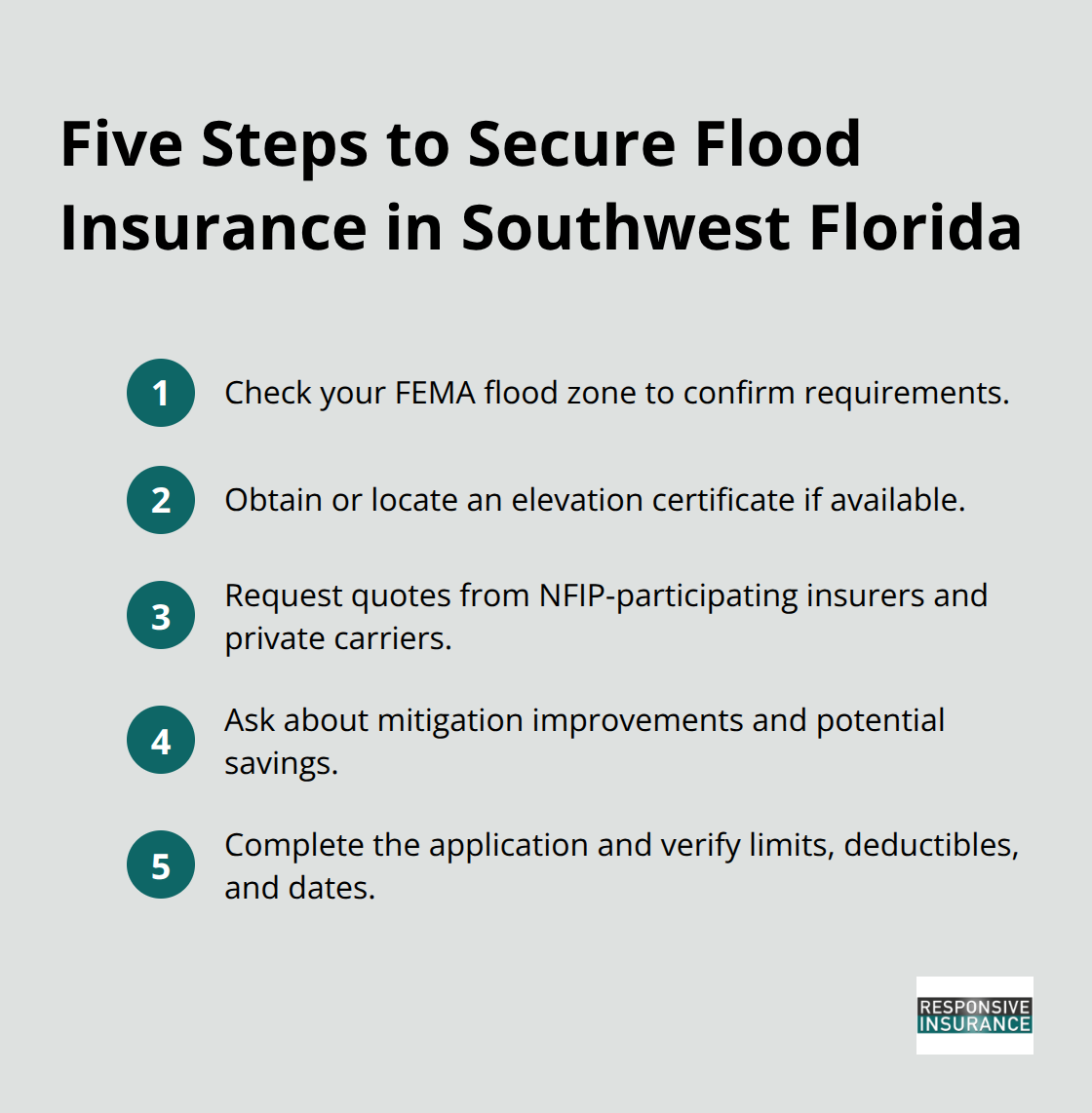

Start with your flood risk zone, since it determines both your insurance requirements and your premium. Visit the FEMA Flood Map Service Center and enter your Naples, Cape Coral, or Charlotte County address to see whether your property falls in a Special Flood Hazard Area, an X zone, or a D zone with unknown risk. This step answers a critical question: is flood insurance mandatory for your mortgage, or optional but prudent? If your lender required flood insurance at closing, your zone designation appears on your mortgage documents. If you’re unsure, call your mortgage servicer or the City of Naples Floodplain Coordinator at 239-213-5039 for clarification.

Your zone determines your baseline premium under Risk Rating 2.0, with V zones averaging $2,413 annually, A zones around $1,313, and X zones approximately $637 according to the National Flood Insurance Program. Knowing this number before you shop prevents sticker shock when quotes arrive.

Strengthen Your Assessment With an Elevation Certificate

An elevation certificate documents your home’s lowest floor elevation relative to the base flood elevation. This document strengthens your risk assessment significantly. Obtaining one costs $400 to $750 through a qualified surveyor but can lower premiums substantially if your home sits above the flood level for your zone. Many properties already have elevation certificates on file with the local floodplain manager, so contact your municipality first before paying for a new survey.

Obtain Quotes From Multiple Providers

Once you understand your risk, obtain quotes from multiple NFIP-participating insurers and private carriers. NFIP policies are standardized in coverage but vary by insurer’s handling and service quality, so the same policy might cost differently depending who sells it. Allstate, Liberty Mutual, USAA, and smaller regional carriers all participate in NFIP, and each calculates premiums slightly differently based on their own loss experience.

Contact three to five providers and request quotes for both NFIP and private flood options if available in your zone. Expect quotes to take one to three business days, since underwriters review your elevation certificate, property age, construction type, and claim history. Private carriers often quote faster and sometimes offer lower rates in lower-risk areas, but they may decline the highest-risk V and AE zones where NFIP guarantees coverage.

Evaluate Mitigation Improvements

During this comparison phase, ask each agent whether mitigation improvements like elevated utilities, flood vents, or basement filling would reduce your premium and by how much. A $3,000 investment in flood vents might save $200 annually, paying for itself in 15 years while protecting your property. These improvements also strengthen your home’s resilience against future floods, making them valuable beyond premium savings alone.

Complete Your Application and Verify Coverage

Once you’ve selected a carrier and policy type, complete your application with accurate information about your property’s age, construction materials, and prior flood losses. The 30-day waiting period begins when NFIP coverage is purchased, so don’t delay this step if hurricane season approaches. Review the policy documents before the waiting period expires to confirm coverage limits match your home’s value and contents inventory, and verify deductibles align with your budget. If you discover gaps in coverage after review, contact your flood insurance agent immediately to adjust limits or add excess coverage while you still have time before storms arrive.

Final Thoughts

Southwest Florida’s flood risk demands action before hurricane season arrives. Ninety percent of federally declared natural disasters involve flooding, and your standard homeowners policy leaves you completely exposed when water enters your home. Flood losses regularly exceed $25,000 per event, and without Southwest Florida flood insurance, you absorb every dollar yourself-government disaster assistance won’t arrive automatically and only comes after official declarations.

Your options are straightforward: the National Flood Insurance Program offers standardized coverage with $250,000 building limits and $100,000 contents limits, while private flood insurers provide alternatives with potentially lower costs in lower-risk areas and higher coverage limits. Start by checking your flood risk zone through the FEMA Flood Map Service Center, then obtain quotes from multiple carriers to compare actual costs for your property. The 30-day waiting period means coverage doesn’t activate immediately, so delaying this decision leaves you exposed when storms approach.

We at Responsive Insurance, Inc. help Southwest Florida homeowners navigate these decisions with confidence and clarity. Contact us today to discuss your flood insurance requirements and receive personalized quotes that match your home’s actual risk profile.