Naples Rental Property Coverage: Protecting Your Investment

Owning rental property in Naples comes with real financial exposure. Between seasonal tenant turnover, hurricane threats, and liability risks from guests, your investment faces challenges that standard homeowners policies simply don’t address.

At Responsive Insurance, Inc., we see rental property owners in Naples underinsured far too often. The right Naples rental property coverage strategy protects your income, your assets, and your peace of mind.

Why Naples Rentals Face Distinct Insurance Challenges

High Tenant Turnover Drives Liability Exposure

Naples rental properties operate in an environment that creates risks standard homeowners policies simply won’t cover. Florida’s population exceeds 22 million and grows faster than the national average, with the state adding roughly 1,000 new residents daily. Many of these newcomers rent before buying, which drives high tenant turnover in Naples. Short-term vacation rentals alone generate more than 8 billion dollars annually across Florida, creating additional complexity for property owners who juggle seasonal guests and extended lease agreements simultaneously. This constant churn of occupants means your liability exposure shifts month to month. A guest injury claim during summer season hits differently than a long-term tenant dispute, and your insurance needs to account for both scenarios.

Hurricane and Windstorm Deductibles Hit Hard

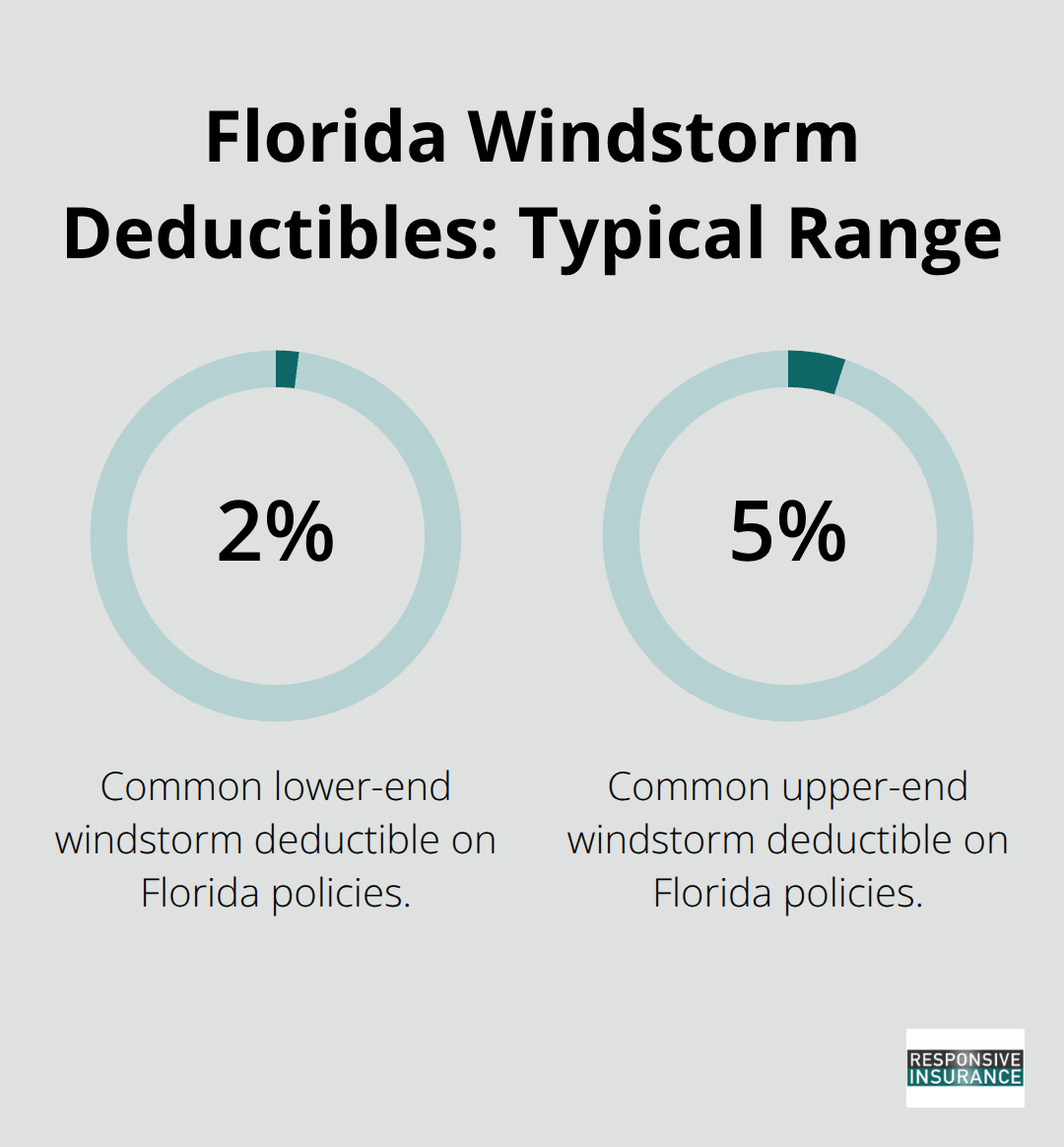

Hurricane season transforms Naples into a high-stakes insurance environment. Windstorm deductibles in Florida policies commonly range from 2 to 5 percent of dwelling coverage, which translates to substantial out-of-pocket costs after a major storm. Coastal properties like those in Naples face elevated premiums because proximity to the coast significantly affects rates.

Florida’s rental stock was built before modern building codes, which influences both insurability and premium calculations for older Naples properties.

Flood Coverage Requires Separate Protection

Flood coverage deserves particular attention because it is not included in standard landlord policies at all. The National Flood Insurance Program and private flood insurers offer separate policies, but many Naples owners overlook this gap entirely. Standard landlord insurance covers sudden events like burst pipes and appliance failures, but flood damage requires its own protection.

Why Standard Homeowners Policies Fall Short

When you combine hurricane exposure with flood risk and seasonal tenant transitions, the liability landscape becomes complex. A guest injured during peak season, a tenant’s dispute over property damage, or hurricane-related loss of rental income each requires specific coverage limits tailored to Naples conditions. Standard homeowners policies deny claims on tenant-occupied properties outright, leaving owners personally liable for damages. This is why landlord insurance exists-and why skipping it or underestimating coverage limits puts your entire investment at risk. Understanding what separates landlord policies from standard homeowners coverage becomes your first step toward adequate protection.

What Coverage Actually Protects Your Naples Rental

Landlord Insurance vs. Standard Homeowners Policies

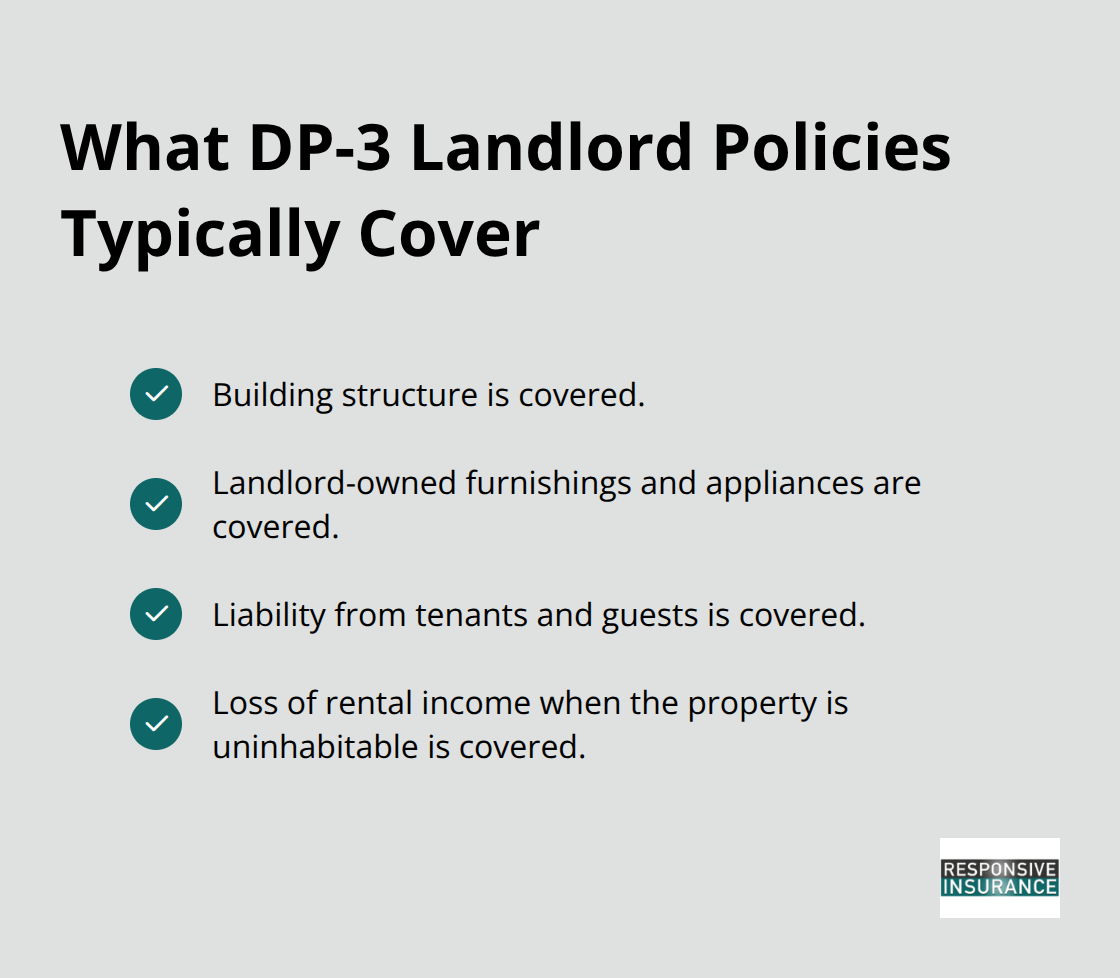

Landlord insurance and standard homeowners policies are fundamentally different products, and this distinction matters enormously for your Naples investment. Standard homeowners insurance explicitly excludes tenant-occupied properties, meaning if a guest is injured or property is damaged while someone else lives there, your claim gets denied. Landlord policies, typically written as DP-3 forms in Florida, cover the building structure, landlord-owned furnishings and appliances, liability exposure from tenants and guests, and loss of rental income when the property becomes uninhabitable.

The median annual premium for Florida landlord insurance runs around $2,404 according to industry data, though Naples properties often cost more due to coastal exposure and flood risk.

Loss of Rents Coverage Protects Your Income

Loss of rents coverage is particularly valuable for Naples owners because it reimburses you when a covered event like a hurricane or fire makes the property unrentable. To calculate your coverage need, multiply your monthly rental income by the estimated months it would take to repair or rebuild the property after a major loss. This protection directly addresses the income vulnerability that makes Naples rental properties distinct from standard residential properties.

Liability Limits Match Your Rental Model

Liability limits typically range from $300,000 to $2 million per occurrence, adding roughly $200 to $400 annually to your premium. Choosing the right liability limit depends on your property type and rental model. Single-family rentals with long-term tenants need different protection than properties hosting weekly vacation guests, where injury exposure increases significantly. Multi-unit properties face compounded liability because multiple tenants and their guests create more claims opportunities. For Naples rental properties with guest exposure from short-term vacation rentals, higher liability limits make financial sense because a single serious injury claim can exceed basic coverage quickly.

Tenant Renters Insurance and Water Damage Protection

Requiring tenants to carry renters insurance protects you by shifting some liability exposure to them and can reduce disputes over personal property damage. Some insurers offer modest premium discounts when landlords mandate tenant renters insurance, typically with a minimum liability threshold of $100,000. Water damage coverage within your landlord policy addresses sudden events like burst pipes and appliance failures, protecting your rental income if tenants must relocate temporarily. However, this coverage excludes flood damage entirely, which requires separate flood insurance through the National Flood Insurance Program or private flood insurers.

Shopping for the Right Policy

Bundling your landlord policy with other coverages through the same insurer often yields premium discounts, and working with an independent agent helps you compare quotes across multiple Florida carriers since the market remains competitive but selective about rental properties. As an independent agency based in Naples, Responsive Insurance, Inc. works with multiple A-rated insurance companies to compare coverage options and find the best fit for your rental property needs. The next step involves understanding which coverage gaps most commonly catch Naples owners off guard-and how to identify them in your own policy before a loss occurs.

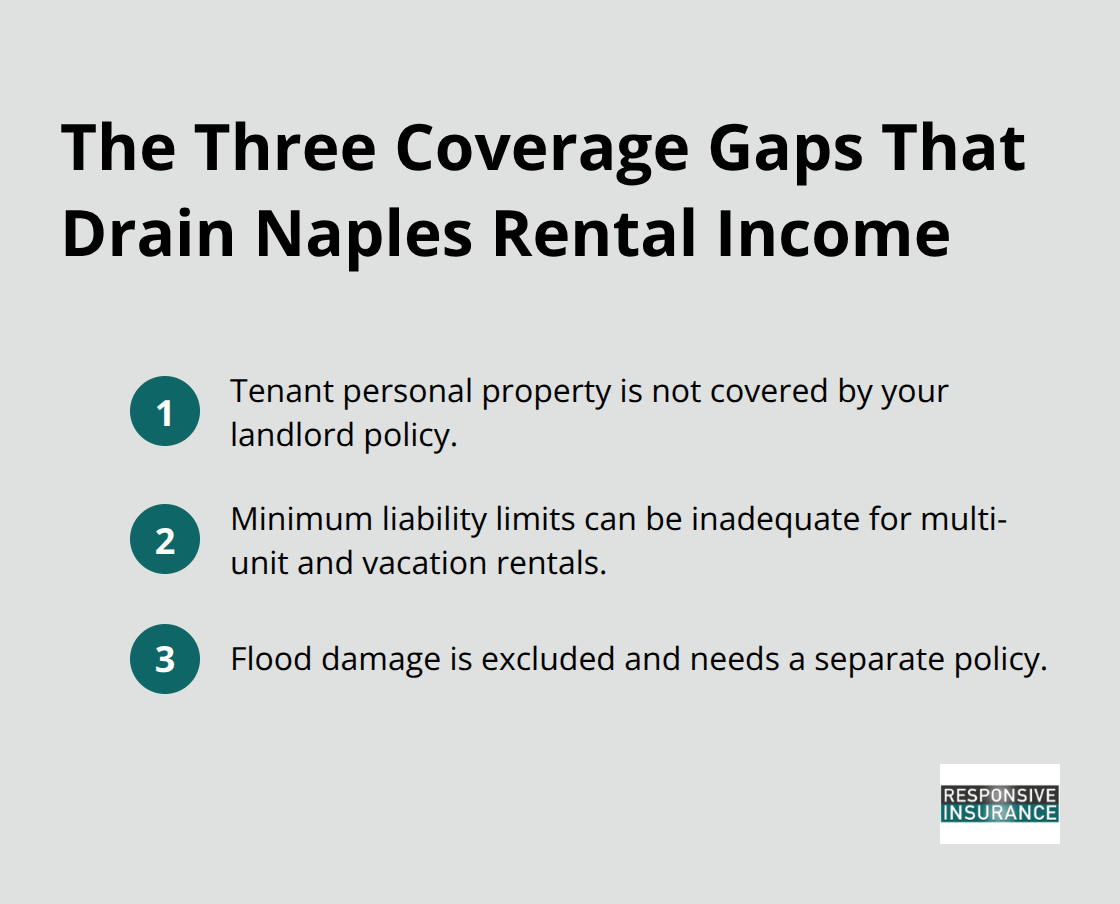

Coverage Gaps That Drain Your Rental Income

Most Naples rental property owners discover their coverage gaps only after a loss occurs, and by then the financial damage is done. The first gap appears when owners assume their landlord policy covers tenant personal property damage. Your policy protects the building structure and your furnishings, but if a tenant’s belongings suffer damage from fire or theft, that loss falls on them-unless they carry renters insurance.

This is why requiring tenants to maintain at least $100,000 in liability coverage matters so much. Without it, disputes over damaged personal property create tension and potential small claims court battles that consume your time and rental income.

Tenant Personal Property Claims Create Costly Disputes

A kitchen fire that destroys a tenant’s furniture and electronics can trigger $15,000 to $25,000 in claims they’ll expect you to cover, even though your policy explicitly excludes their items. The solution is straightforward: include renters insurance requirements in your lease agreement and verify coverage before tenants move in. Some insurers offer small premium discounts when landlords mandate this protection, making it a financial win for both parties. This simple step prevents disputes and protects your relationship with tenants while keeping your policy limits focused on what actually matters-your building and income.

Inadequate Liability Limits for Multi-Unit Properties

The second gap hits harder for multi-unit properties and vacation rentals. Liability limits of $300,000 feel adequate until a guest suffers a serious injury on your property. A slip-and-fall that results in permanent disability, a pool drowning, or a structural failure causing multiple injuries can generate settlements exceeding $500,000 to $1 million. Naples properties with pools, hot tubs, or guest access face compounded exposure because injury claims spike significantly. Industry data shows landlord liability coverage typically ranges from $300,000 to $2 million per occurrence, yet many owners stick with the minimum to save $200 to $400 annually on premiums. This false economy backfires instantly when a serious claim arrives.

Multi-unit buildings amplify this risk exponentially-each additional unit means more tenants, more guests, and more injury opportunities. Owners with multiple units or guest-heavy rentals should carry at least $1 million in liability coverage, with umbrella policies of $2 million to $5 million adding meaningful protection for just a few hundred dollars annually. The cost difference between basic and robust liability coverage proves negligible compared to the financial devastation a major injury claim can inflict on your investment.

Flood Insurance Exclusions Leave Properties Vulnerable

The third gap proves especially costly in Naples: overlooking flood insurance entirely. Standard landlord policies exclude flood damage completely, yet Naples sits in a high-risk environment where heavy rain, storm surge, and poor drainage create frequent flooding. The National Flood Insurance Program charges roughly $400 to $800 annually for basic flood coverage on rental properties, yet many owners skip it to save money. A single flood event that makes the property uninhabitable for three months costs far more than years of premiums-you lose three months of rental income, face water damage repairs to structure and systems, and potentially deal with mold remediation.

Properties in designated flood zones face mandatory flood insurance if financed through a mortgage, but even properties outside formal flood zones experience water intrusion during heavy storms. The practical step involves checking your property’s flood zone designation through FEMA flood maps, then comparing coverage quotes from both the National Flood Insurance Program and private flood insurers. Private flood policies sometimes offer better rates and broader coverage than NFIP, particularly for older Naples properties.

Final Thoughts

Your Naples rental property represents a significant financial commitment, and protecting it requires more than hoping your current coverage is adequate. The gaps we’ve outlined-tenant personal property disputes, insufficient liability limits, and missing flood insurance-drain rental income and expose you to personal liability that can exceed your policy limits. Naples rental property coverage must address three distinct risks: property damage from hurricanes and storms, lost rental income when tenants cannot occupy the unit, and liability claims from guest injuries or property damage.

Working with a local insurance agent matters because they understand Naples conditions in ways national carriers cannot. An agent familiar with coastal exposure, flood zones, and seasonal rental patterns helps you avoid the coverage gaps that catch most owners off guard. They compare quotes across multiple A-rated insurance companies rather than pushing a single carrier’s products, and they identify which optional coverages make financial sense for your specific property type and rental model.

Your next step is straightforward: gather your current policy documents and request a coverage review from an agent who specializes in rental properties. Bring details about your property type, rental model, liability exposure, and flood zone designation, then ask specifically about loss of rents coverage limits, liability limits relative to your guest exposure, and whether flood insurance makes sense for your location. Contact Responsive Insurance, Inc. to schedule a consultation and protect your Naples rental investment properly.