Florida NFIP Policy Guide: Understanding the National Flood Insurance Program

Flooding is the most common natural disaster in Florida, affecting thousands of homeowners every year. At Responsive Insurance, Inc., we’ve created this Florida NFIP policy guide to help you understand your coverage options and protect your home.

Whether you live in a high-risk flood zone or think you’re safe, knowing how the National Flood Insurance Program works could save you thousands in unexpected costs.

What Is the National Flood Insurance Program

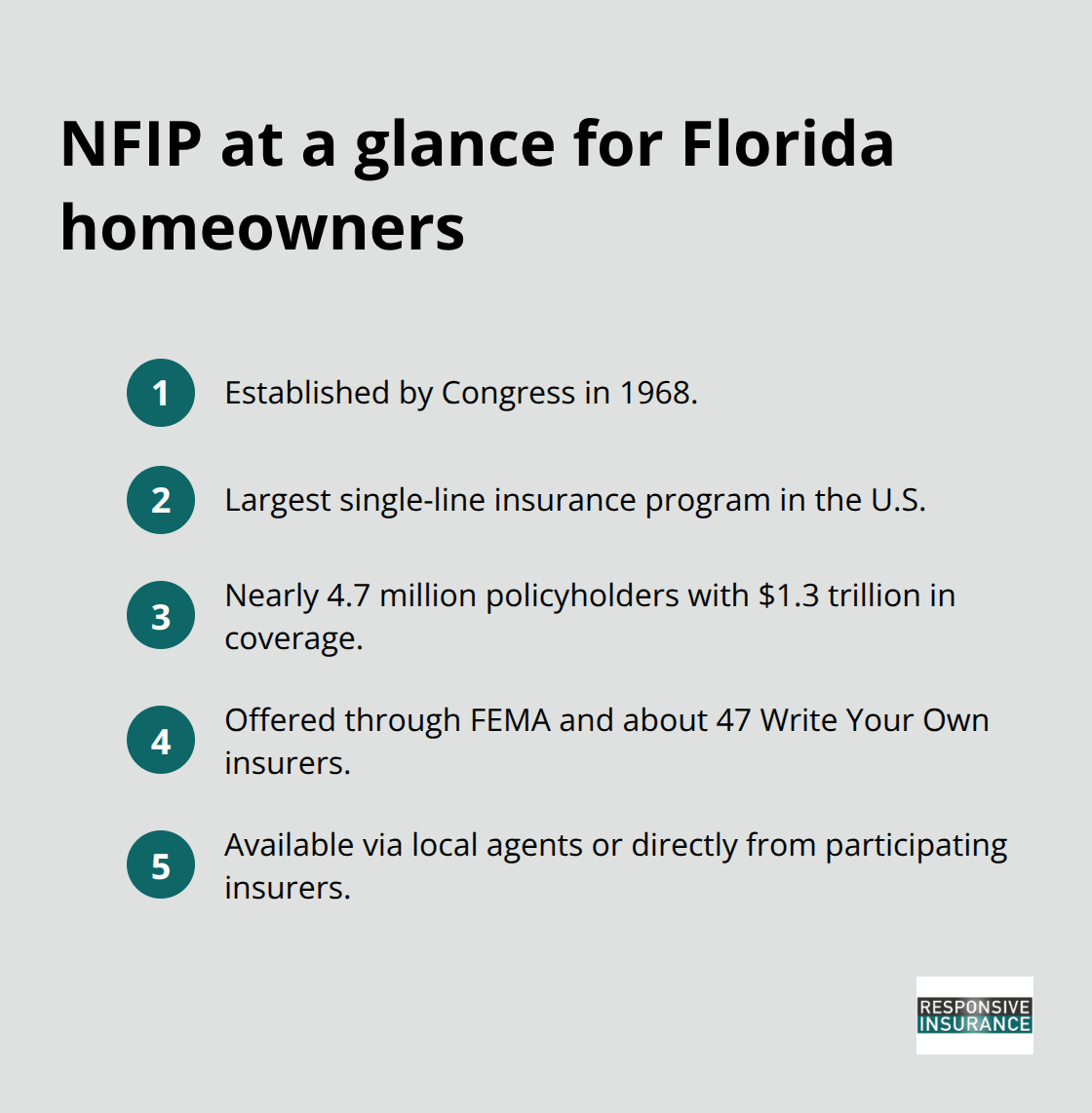

Congress established the National Flood Insurance Program in 1968 after recognizing that standard homeowners insurance policies would not cover flood damage. Today, the NFIP stands as the nation’s largest single-line insurance program, protecting nearly 4.7 million policyholders with over $1.3 trillion in coverage. For Naples residents, this matters because most private homeowners policies exclude water damage from flooding, leaving you exposed to catastrophic losses.

The National Flood Insurance Program was designed to fill this gap and make flood insurance available in areas where private insurers refused to operate. Florida has more NFIP policies than any other state, which tells you something important: flood risk here is real and widespread. Without the NFIP, thousands of Florida home sales would never close each month because lenders require flood insurance in high-risk areas. The program operates through a partnership between FEMA and about 47 private insurance companies that sell and service policies under the Write Your Own Program. This structure means you can purchase NFIP coverage through your local agent or directly from an insurer, giving you flexibility in how you buy protection.

Standard Coverage Limits and What They Mean

Standard NFIP policies establish maximum coverage limits that vary by property type. For a single-family home, building coverage tops out at $250,000 and contents coverage at $100,000. These limits fall significantly short of the replacement cost for many Naples homes, which is why some homeowners layer excess flood insurance on top of their NFIP policy. The NFIP also excludes certain types of damage: it does not cover basements, crawlspaces, or earth movement, and it does not pay for additional living expenses or business interruption. You need to understand these exclusions before assuming you’re fully protected.

How Deductibles and Risk Rating Work

The program offers flexibility through deductible options, typically ranging from $500 to $10,000, and choosing a higher deductible lowers your annual premium. NFIP rates are now based on individual property characteristics through a system called Risk Rating 2.0, which replaced zone-based pricing starting in late 2021. Your specific elevation, distance from water, and construction details affect your rate, not just which flood zone your address falls in. Annual premiums are capped at $10,000 per year, which helps keep coverage affordable even in the highest-risk areas. Understanding these pricing factors allows you to make informed decisions about your coverage level and deductible selection.

Who Needs Flood Insurance in Florida

Mandatory Coverage Requirements for Mortgaged Properties

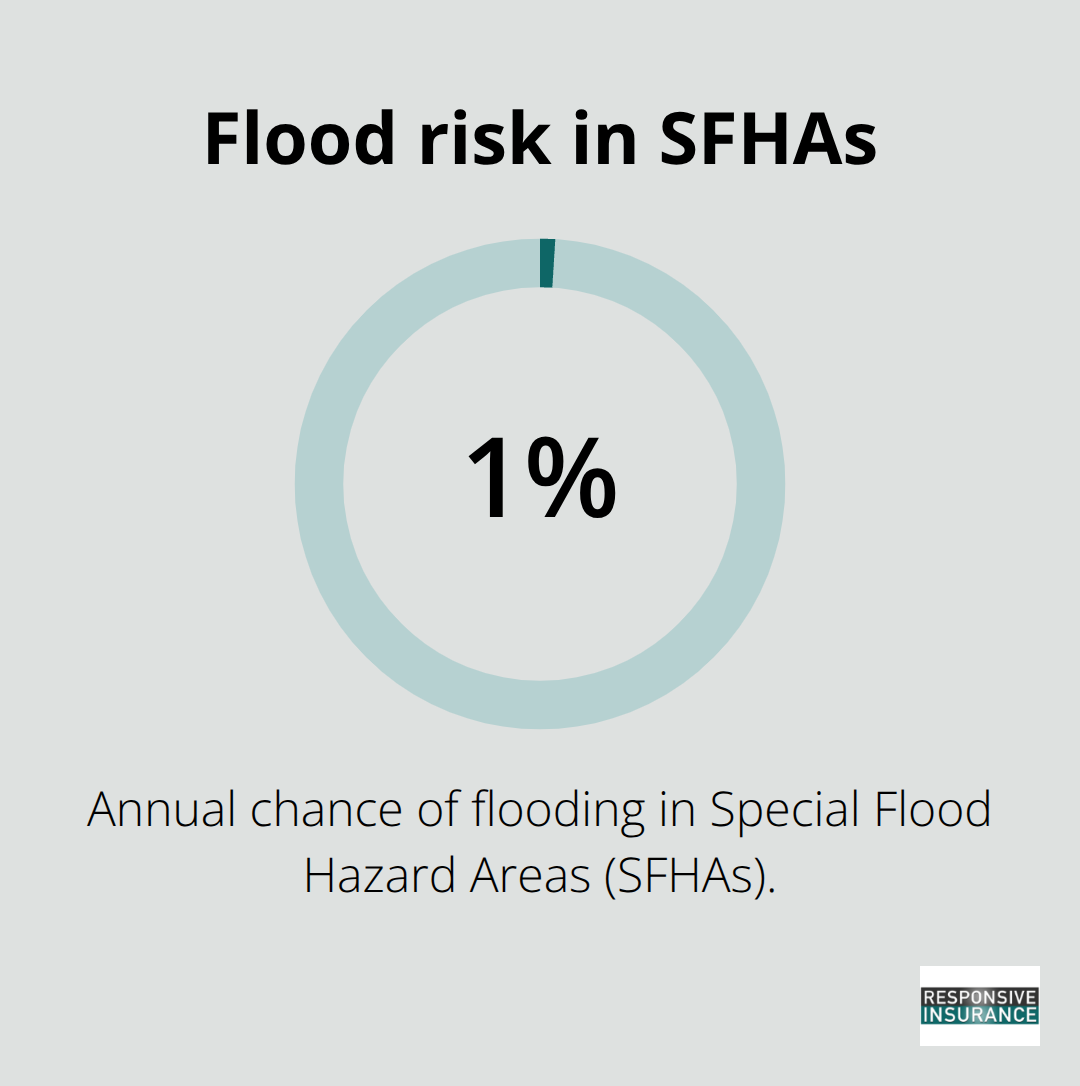

If you have a mortgage in Florida, your lender will require flood insurance when your property sits in a high-risk flood zone, technically called a Special Flood Hazard Area or SFHA. FEMA maintains Flood Insurance Rate Maps that designate these zones, which represent areas with at least a 1% annual chance of flooding. For Naples residents, this requirement is not theoretical-Florida holds more NFIP policies than any other state, and nearly every real estate transaction involves flood risk assessment.

Your lender uses these maps to determine mandatory coverage, which means you cannot close on a mortgaged property in an SFHA without proof of flood insurance.

Why Properties Outside High-Risk Zones Still Need Protection

Even if your property sits outside a designated high-risk zone, you should still consider coverage because standard homeowners policies exclude all flood damage, regardless of zone designation. Flooding does not respect map boundaries, and properties in moderate or low-risk areas experience significant losses during major events. FEMA estimates that floodplain management standards save about $2.4 billion annually in avoided flood losses, yet this protection only works if homeowners carry appropriate coverage.

Evaluating Your Actual Flood Risk

The decision to purchase flood insurance outside a mandatory zone should be practical and data-driven. Talk to your insurance agent about obtaining a detailed flood report for your property, which shows historical flood events in your area and estimated water depths during various storm scenarios. If your home sits within a few blocks of waterways, in an area with poor drainage, or in a neighborhood with a history of localized flooding, the cost of NFIP coverage typically proves far cheaper than the cost of uninsured flood damage.

Comparing Costs Against Potential Losses

Premiums for properties outside high-risk zones cost significantly less than those in SFHAs, making voluntary coverage an affordable option for many homeowners. A single flood event can result in tens of thousands of dollars in damage to flooring, drywall, electrical systems, and personal property. Your homeowners policy will not cover any of this, leaving you personally responsible for recovery costs and temporary housing expenses. The NFIP caps annual premiums at $10,000 even for the highest-risk properties, so the financial calculation often favors obtaining coverage rather than gambling that your property will never flood.

Understanding your flood risk and coverage needs sets the foundation for selecting the right policy. The next section explains exactly what NFIP policies cover and exclude, plus the specific factors that determine your premium amount.

Understanding NFIP Coverage and Costs

NFIP policies cover two distinct categories: building coverage and contents coverage, and understanding the difference matters because your home likely needs both. Building coverage pays for structural damage to your house itself, including the foundation, walls, roof, built-in appliances, and permanently installed equipment like HVAC systems. Contents coverage protects your personal belongings inside the home, from furniture to electronics to clothing. For a single-family home in Naples, the NFIP caps building coverage at $250,000 and contents at $100,000, according to FEMA standards. Many homeowners discover these limits fall far short of their actual replacement costs, especially in Southwest Florida where home values run high.

What NFIP Policies Exclude

The exclusions matter just as much as what the program covers. The NFIP does not cover basements or crawlspaces under any circumstances, even if water damage occurs there. It also excludes earth movement, which means damage from settling, subsidence, or erosion receives no payment. Additional living expenses if you must temporarily relocate after a flood are not covered, nor are losses from business interruption. These gaps explain why some property owners in high-risk areas layer excess flood insurance on top of their standard NFIP policy to close the coverage holes.

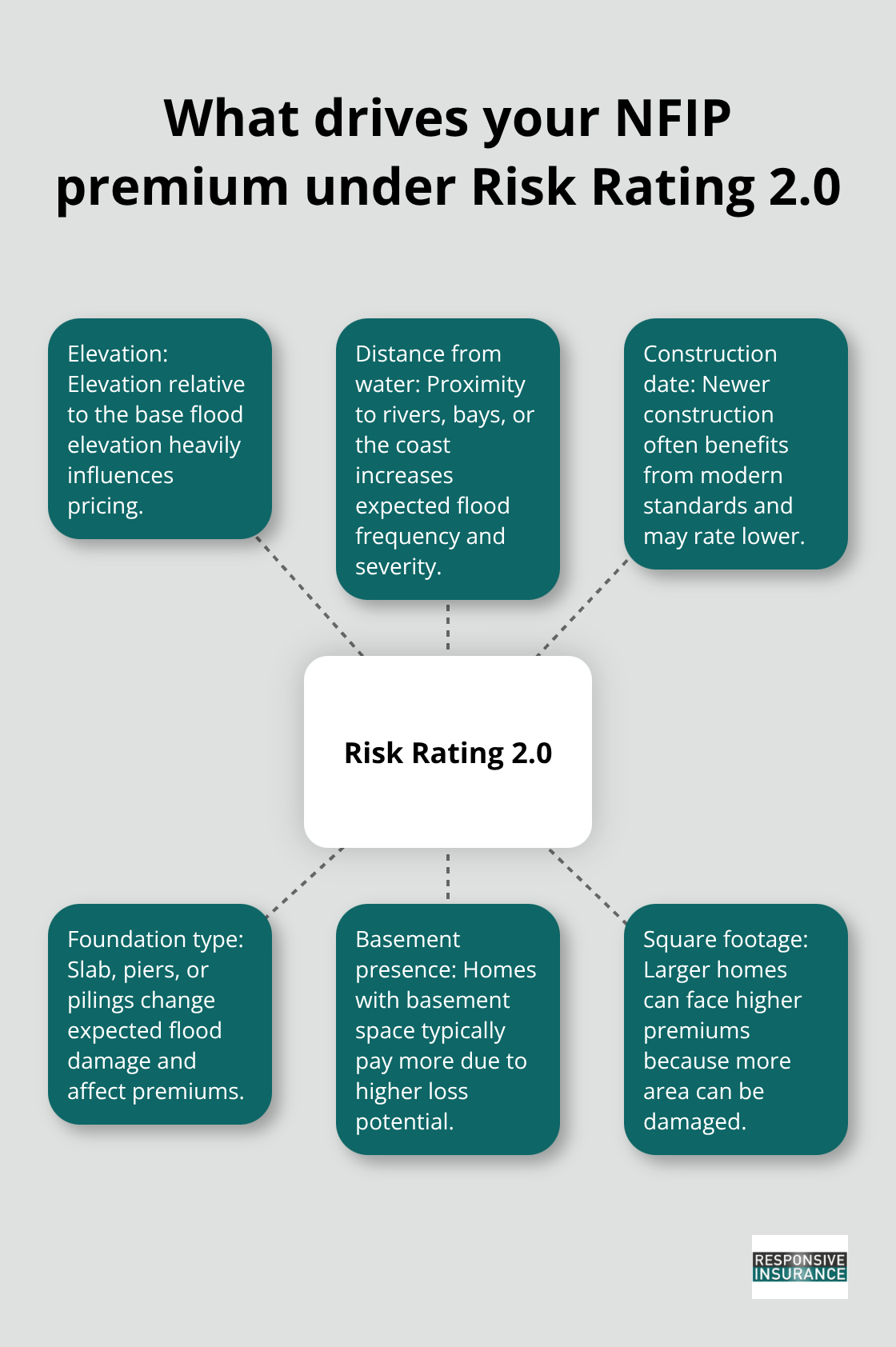

How Risk Rating 2.0 Determines Your Premium

Your NFIP premium depends far more on your specific property than on your flood zone designation. The program switched to Risk Rating 2.0, which evaluates individual characteristics rather than relying solely on zone-based pricing. Your home’s elevation relative to the base flood elevation directly impacts your rate, as does its distance from bodies of water and the construction date.

The type of foundation you have, whether the property has basement space, and the square footage all feed into the calculation. A property built in 1960 with a basement will pay significantly more than an identical home built in 2015 with a slab foundation, even if both sit in the same flood zone.

Premium Caps and Deductible Choices

The NFIP caps annual premiums at $10,000 per year according to federal law, which protects homeowners in the highest-risk areas from catastrophic rate increases. This cap means Naples residents in coastal properties or near rivers pay the same maximum regardless of how severe their individual risk profile becomes. Deductible selection offers the most direct way you control your premium costs, with options typically ranging from $500 to $10,000 per flood event. Choosing a $10,000 deductible instead of $500 can reduce your annual premium by 20 to 30 percent depending on your property characteristics. The financial trade-off makes sense if you have emergency savings available to cover a larger out-of-pocket loss but want to minimize monthly insurance expenses.

How Deductibles Apply to Flood Events

Your deductible applies per flood event, not annually, which is a critical distinction many homeowners misunderstand. If your home floods twice in one year, you pay your deductible twice, not once. A $1,000 deductible means the NFIP pays nothing for flood damage below that amount and applies the deductible before paying anything above it. For minor flooding that causes $2,500 in damage with a $1,000 deductible, the NFIP covers only $1,500. This structure means selecting a deductible requires honest assessment of your financial capacity to absorb losses. If you have $15,000 in accessible savings and your property sits in a moderate-risk area where small floods occur occasionally, a $5,000 deductible balances lower premiums with manageable out-of-pocket exposure. Conversely, if you have limited savings and high anxiety about unexpected expenses, the $500 or $1,000 deductible options provide peace of mind despite higher premiums. Naples residents shopping for NFIP coverage should obtain multiple quotes before deciding, as premium variations exist across the 47 private insurers that sell NFIP policies through the Write Your Own program. An independent insurance agent can provide access to these competitive quotes and expert guidance on selecting coverage levels and deductibles matched to your actual situation.

Final Thoughts

Flood insurance in Florida is not optional for most homeowners, and understanding your coverage options protects both your finances and your peace of mind. The National Flood Insurance Program provides the most accessible path to protection, with premiums capped at $10,000 annually and coverage available regardless of your property’s flood risk level. Your specific situation determines whether NFIP coverage alone suffices or whether layering excess flood insurance makes sense for your home’s replacement value.

Getting NFIP coverage starts with contacting your insurance agent or visiting FloodSmart.gov to obtain a free quote. The process takes minutes, and you’ll receive a personalized premium based on your property’s elevation, distance from water, and construction characteristics. A 30-day waiting period applies after purchase before your policy becomes effective, so timing matters if you’re concerned about an approaching storm season.

Reviewing your NFIP policy annually makes sense because your coverage needs may change as your home ages or your financial situation evolves. If you’ve made improvements that reduce flood risk (such as elevating utilities or installing flood vents), your premium may decrease under Risk Rating 2.0. Contact us at Responsive Insurance, Inc. to review your flood insurance situation and ensure your Naples home has appropriate protection aligned with this Florida NFIP policy guide.