Do I Need Flood Insurance in Florida? A Quick Guide

Florida’s geography makes flooding a real threat to homeowners. If you’re asking do I need flood insurance in Florida, the answer depends on where your property sits and what your mortgage lender requires.

At Responsive Insurance, Inc., we help Naples residents understand their flood risk and find the right coverage. Standard homeowners policies won’t protect you from flood damage, which is why separate flood insurance matters.

Why Florida’s Flood Risk Makes Insurance Essential

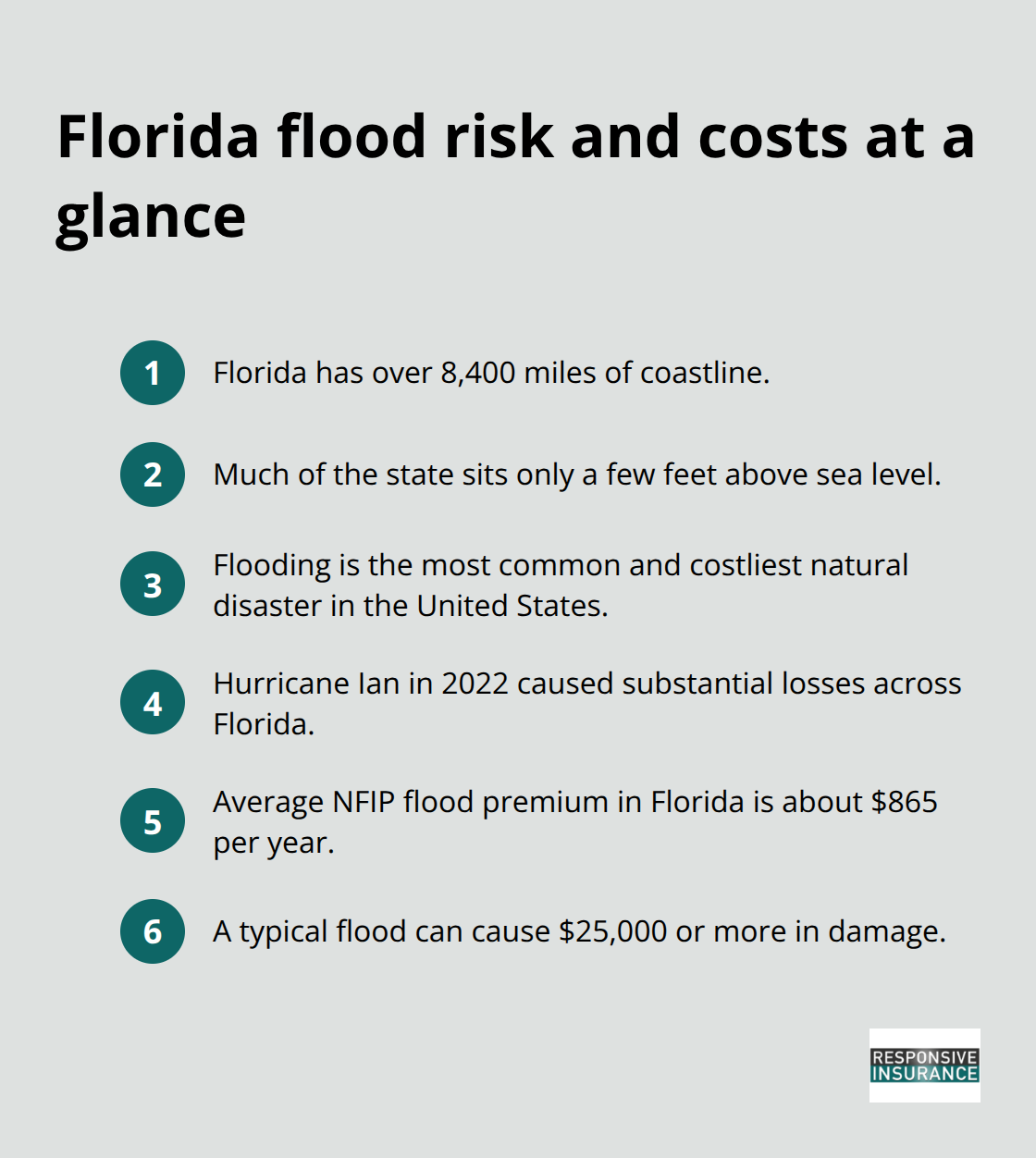

Florida sits at the intersection of multiple flood threats that make the state uniquely vulnerable. The state has over 8,400 miles of coastline, with much of it only a few feet above sea level. This flat terrain means water has nowhere to drain during heavy rainfall or storm surge events. Flooding is the most common and costliest natural disaster in the United States, and Florida experiences this reality more intensely than most states. Hurricane Ian in 2022 caused substantial losses across Florida properties, demonstrating exactly how devastating flood damage can be. Rising sea levels compound the problem further. Naples residents face particular exposure because the city sits in a coastal zone where both storm surge and rainfall flooding pose genuine threats. The average flood insurance premium in Florida runs about $865 per year through the National Flood Insurance Program, but this cost pales in comparison to the average flood event damage, which can easily reach $25,000 or more for even modest flood scenarios.

Understanding Your Mandatory Coverage Requirements

If you have a federally backed mortgage and your property sits in a Special Flood Hazard Area, your lender will require flood insurance. This isn’t optional-it’s a condition of your loan. Naples participates in the National Flood Insurance Program, so you can access NFIP coverage if needed. Flood zone designations are based on detailed risk data to help identify areas of concern. Zone AH indicates shallow flooding with 1-3 feet of water depth and requires mandatory coverage. Zone AE covers the 1% annual chance flood and also mandates insurance. Zone VE represents coastal high-hazard areas with significant wave action and carries the highest risk requirements.

Even if you’re in Zone X or outside mapped high-risk areas, about 40 percent of NFIP flood claims come from properties outside Special Flood Hazard Areas-this statistic matters because it shows that flood risk extends well beyond the officially designated danger zones. You can check your specific flood zone through the City of Naples interactive flood map tool or by contacting the Floodplain Coordinator at 239-213-5039. Florida Citizens policyholders with dwelling coverage exceeding $400,000 face a January 1, 2026 deadline to purchase flood insurance, with other policyholders having until January 1, 2027.

The Real Cost of Going Uninsured

Without flood insurance, you pay flood losses entirely out of pocket. Federal disaster assistance is not automatic and typically arrives as loans rather than grants. Only about half of flood events receive official disaster declarations, and those declarations depend on widespread damage across entire regions. A single flood event in your home could cost tens of thousands of dollars in structural repairs, appliance replacement, and flooring restoration. Standard homeowners policies explicitly exclude flood damage, leaving this gap completely uncovered. The gap between what people think they’re protected against and what they actually are protected against creates serious financial vulnerability. This protection gap affects most Florida homeowners, which is why understanding your specific flood zone and coverage options matters so much.

What Your Homeowners Policy Actually Covers

Your homeowners insurance policy protects against many things-theft, fire, wind damage, and liability-but flood damage isn’t one of them. This isn’t an oversight or fine print loophole. Standard homeowners policies explicitly exclude water damage from flooding because flood risk operates differently than other perils. Insurers price homeowners policies based on fire, theft, and weather events like hail and lightning. Flooding requires separate actuarial analysis because it affects entire regions simultaneously, concentrating claims in specific areas during storm events.

The National Flood Insurance Program exists precisely because private insurers won’t cover this exposure through standard homeowners policies. When Hurricane Ian struck Florida in 2022, homeowners who believed their standard policies covered storm damage faced devastating financial consequences. Many discovered too late that their coverage excluded surge and rainfall flooding entirely. Your homeowners policy might cover wind damage from that same hurricane, but the water that follows the wind remains completely uncovered. This distinction matters enormously because flood damage often exceeds wind damage in coastal events.

The Structural Damage Gap

Structural damage from flooding-water-soaked walls, ruined drywall, compromised electrical systems, and damaged HVAC equipment-falls entirely on you without flood insurance. An elevation certificate documenting your home’s lowest floor elevation can reduce flood insurance premiums substantially, but it won’t help your standard homeowners claim. The average flood event costs around $25,000 or more, yet most homeowners don’t realize this exposure exists until water enters their home.

Contents Coverage Exclusions

Contents coverage under your homeowners policy also excludes flood damage, meaning your furniture, electronics, clothing, and personal items destroyed by floodwater receive no protection. Federal disaster assistance won’t fill this gap reliably because only about half of flood events trigger official disaster declarations, and those declarations require widespread regional damage. When assistance does arrive, it typically comes as low-interest loans rather than grants, meaning you’ll repay borrowed money on top of your own out-of-pocket costs.

Why This Matters for Naples Residents

Naples residents particularly need to understand this gap because the city’s coastal location means both storm surge and heavy rainfall flooding pose real threats to properties. The math becomes straightforward: flood insurance through the NFIP protects against potential losses exceeding $25,000. Understanding what your homeowners policy excludes sets the stage for recognizing exactly what flood insurance must cover and how to determine whether you actually need it.

Finding Your Flood Zone and Getting the Right Coverage

Determine Your Flood Zone First

Start by identifying your exact flood zone because this single step shapes everything else about your flood insurance decision. Use the City of Naples interactive flood map tool and enter your address to see your zone designation instantly. If you’re outside Naples, the Collier County flood map or FEMA’s Flood Map Service Center will show your risk level. This matters because your zone determines whether flood insurance is mandatory, what coverage limits apply, and what you’ll pay annually. The 2024 Flood Insurance Rate Maps now in effect provide more detailed risk data than the 2012 maps they replaced, meaning your actual risk profile may have changed since your last policy review.

Zone AH means shallow flooding between 1 and 3 feet. Zone AE indicates a 1 percent annual chance flood. Zone VE represents coastal high-hazard areas with dangerous wave action.

About 40 percent of flood claims come from properties outside the officially designated high-risk zones, so even if you’re in Zone X or an unshaded area, flood risk still exists. Contact the City of Naples Floodplain Coordinator at 239-213-5039 or rdorta@naplesgov.com to confirm your exact zone if you’re uncertain.

Understand Coverage Limits and Options

Naples qualifies for a CRS Rating Class 5, which means standard NFIP policies can receive up to a 25 percent discount on premiums compared to other Florida cities. The NFIP structure coverage maxes out at $250,000 for single-family homes and contents coverage at $100,000, which may fall short if your home reconstruction cost exceeds these limits. Private flood insurance options now available in Florida can offer higher limits and potentially lower premiums than the NFIP, with some policies featuring shorter waiting periods than the standard 30 days.

If your property sits in a high-risk area, obtain an elevation certificate from a licensed surveyor or engineer. This document measures your home’s lowest floor elevation and can substantially reduce your annual premium. The investment in an elevation certificate often pays for itself through premium savings over just a few years.

Shop Multiple Markets for the Best Rate

Shop both NFIP and private markets because NerdWallet data shows Naples averages $1,498 annually for NFIP policies, but private alternatives might cost less depending on your specific risk factors. Request quotes from multiple insurers and ask specifically about deductible options and whether contents coverage is included. If you’re a renter, flood insurance protecting your belongings starts around $100 annually.

Know Your Deadlines

Florida Citizens policyholders with dwelling coverage above $400,000 must purchase flood insurance by January 1, 2026, while others have until January 1, 2027. Don’t wait for storm season to shop because the 30-day waiting period means coverage won’t activate during an emergency. This waiting period applies whether you choose NFIP or private flood insurance, so timing your purchase matters significantly for your protection.

Final Thoughts

Flood insurance in Florida isn’t a luxury or an afterthought-it’s a financial necessity that protects your home, your belongings, and your financial stability when water damage strikes. The question “do I need flood insurance in Florida?” has a straightforward answer for most homeowners: yes, you do. Whether your lender requires it or not, the statistics make the case clear: forty percent of flood claims come from properties outside high-risk zones, meaning danger extends far beyond official flood maps, and a single flood event costs $25,000 or more on average while your standard homeowners policy won’t cover a single dollar of that damage.

Check your flood zone using the City of Naples interactive map tool or by calling the Floodplain Coordinator at 239-213-5039-this single action tells you whether flood insurance is mandatory for your property and what coverage limits you’ll need. If you have a federally backed mortgage and live in a Special Flood Hazard Area, your lender will require coverage anyway, so don’t delay. Florida Citizens policyholders with high dwelling limits face January 2026 and 2027 deadlines that approach fast.

Once you know your zone, get quotes from both the National Flood Insurance Program and private insurers to compare rates and coverage options. Naples residents benefit from a 25 percent CRS discount on NFIP policies, but private options might offer better rates or higher limits depending on your specific situation, and an elevation certificate can substantially reduce your annual premium if you’re in a high-risk area. Contact us at Responsive Insurance, Inc. to discuss your flood insurance options and get the protection your home needs.

![Hurricane Insurance Florida [Everything You Need to Know]](https://responsiveinsurance.com/wp-content/uploads/emplibot/Hurricane-Insurance-Florida-_Everything-You-Need-to-Know__1769898428-80x80.jpeg)