What Is Excess Flood Insurance?

Standard flood insurance has limits. If you live in Naples, FL, those limits might not be enough to protect your home’s full value.

Excess flood insurance fills that gap. It covers costs that standard policies won’t, giving you real protection when flooding happens. We at Responsive Insurance, Inc. help homeowners understand what excess flood insurance is and why it matters for properties in high-risk areas.

How Excess Flood Insurance Works

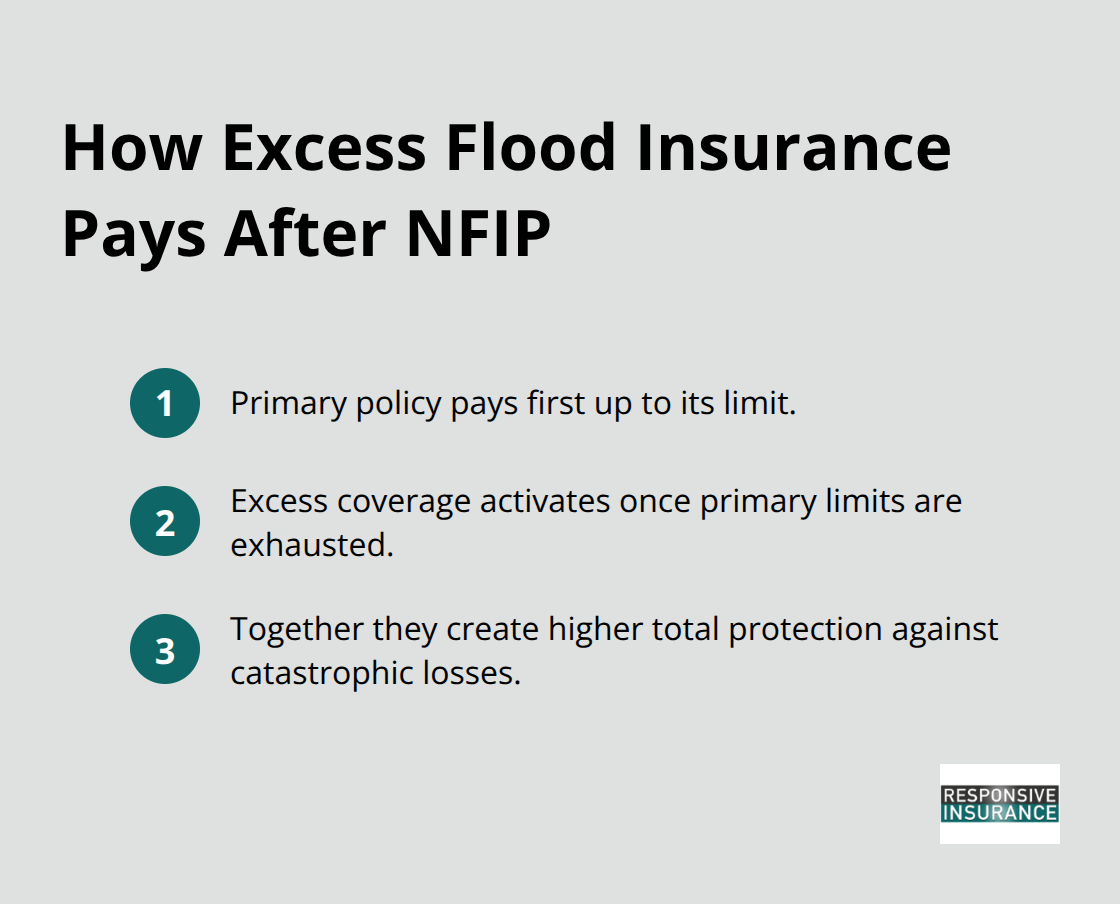

Excess flood insurance activates only after your primary flood insurance limits are exhausted. When a flood causes damage, your primary policy pays first up to its limit. Once that limit is reached, excess flood insurance kicks in and covers additional costs up to its own limit. This layered approach protects you from catastrophic losses that primary coverage alone cannot handle.

For homeowners in Naples, FL, this distinction matters because the National Flood Insurance Program (NFIP) caps residential structure coverage at $250,000 and contents at $100,000. If your home is worth $800,000, NFIP covers the structure damage up to $250,000, leaving a $550,000 gap. Excess flood insurance fills that gap, paying up to its limit after NFIP exhausts its $250,000. Without excess coverage, you absorb the remaining cost yourself.

What Excess Policies Cover That Primary Policies Don’t

Private excess flood policies offer features NFIP does not, such as additional living expense coverage if your home becomes uninhabitable due to flood damage. This means your policy pays for temporary housing, meals, and other necessities while repairs happen. Some excess policies also extend coverage to items your primary policy excludes, such as basement contents or detached structures. This flexibility makes excess flood insurance valuable for Naples homeowners with basements or outbuildings containing valuable equipment or stored items.

Why Primary Coverage Falls Short

The NFIP limits are standardized and fixed regardless of your home’s actual value. A $600,000 home and a $400,000 home both receive the same $250,000 structure limit under NFIP. High-value properties in Naples face real exposure because one flood event can trigger losses far exceeding NFIP’s ceiling.

Elevation also affects your risk. Properties in low-lying areas near water sources experience higher flood frequency and severity. Excess flood insurance accounts for this reality by allowing coverage limits to match your actual replacement cost, not an arbitrary federal cap.

How Deductibles Impact Your Protection

Deductibles matter significantly. Primary NFIP policies typically have deductibles of $1,000 to $10,000, while excess policies may have higher deductibles ranging from $10,000 to $25,000 or more. Choosing a higher deductible on your excess policy lowers your premium, making the coverage more affordable while still protecting against major losses.

Understanding Coverage Limits and Pricing

Excess flood insurance covers the same perils as primary coverage: heavy rainfall, rising water from rivers or lakes, storm surge, and flash flooding. The key difference is the dollar amount. If primary coverage pays $250,000 and excess covers the next $300,000, you have $550,000 total protection.

The cost of excess flood insurance varies by insurer, property elevation, proximity to water, and desired limits. Premiums are lower than you might expect because the excess policy only pays after primary limits are exhausted, meaning the risk to the insurer is lower. Obtaining quotes from multiple insurers reveals significant price differences, sometimes ranging from a few hundred to over a thousand dollars annually for the same coverage. Shopping multiple quotes is not optional if you want excess flood protection-it is essential.

Understanding what excess flood insurance covers and how it layers on top of primary policies sets the stage for determining whether your Naples home actually needs this protection.

When You Need Excess Flood Insurance in Naples

Property Value and Coverage Gaps

Not every Naples homeowner needs excess flood insurance, but many do. The question is whether your current coverage matches what you actually stand to lose. NFIP’s $250,000 structure limit works fine for modest homes, but Naples has plenty of properties worth far more. If your home is valued at $600,000 or higher, excess flood insurance stops being optional and becomes practical protection. The same applies if you have significant personal property inside your home-artwork, collectibles, equipment, or furnishings that could total hundreds of thousands of dollars. NFIP’s contents limit of $100,000 leaves enormous gaps for homeowners with valuable interiors.

Location and Flood Frequency

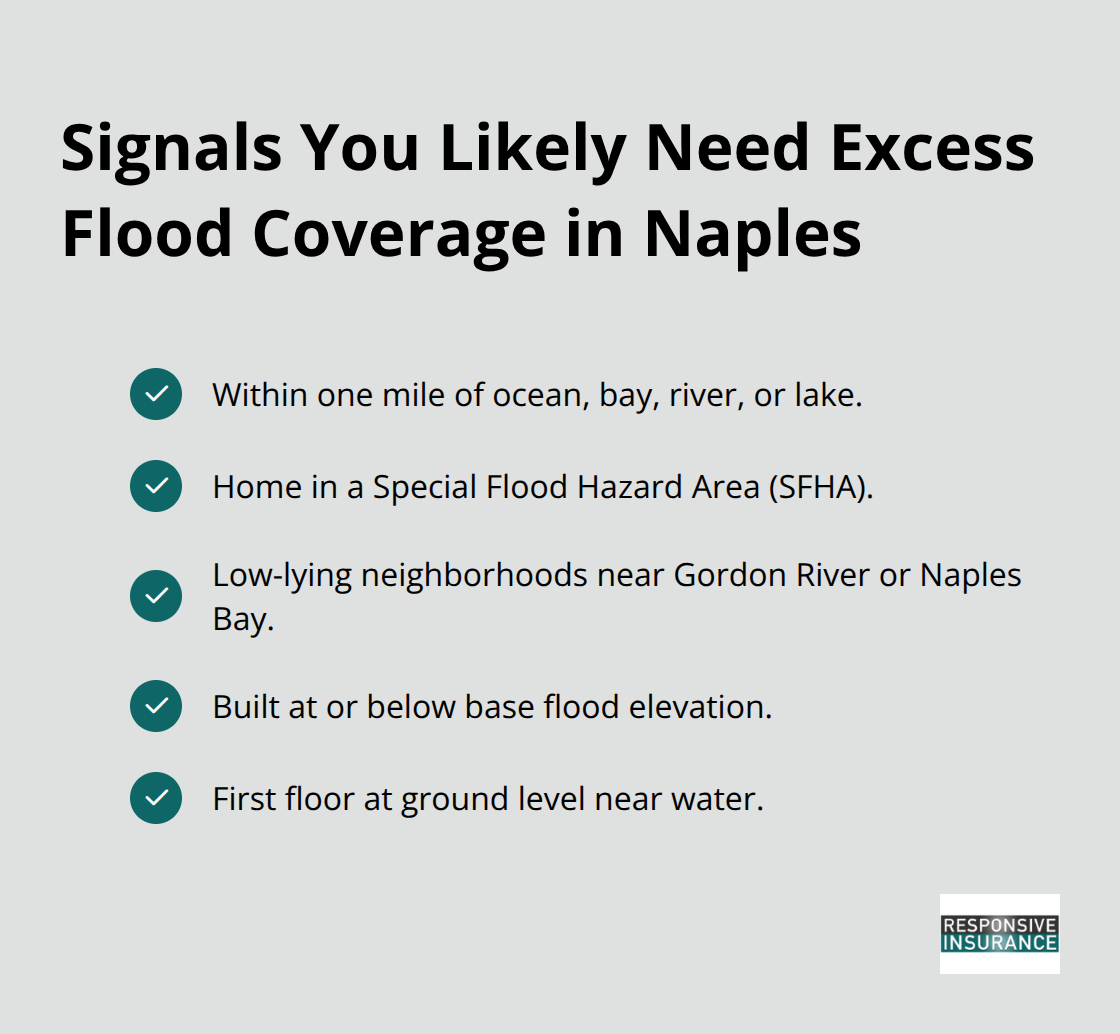

Your location determines whether excess coverage makes sense. Properties within one mile of water-whether ocean, bay, river, or lake-face substantially higher flood frequency. According to FEMA’s pricing data, homes in high-risk zones pay premiums reflecting that reality, and the damage when floods occur is correspondingly severe. If your property sits in a Special Flood Hazard Area or you live in Naples’ low-lying neighborhoods near Gordon River or Naples Bay, excess coverage isn’t theoretical protection-it’s essential. Elevation matters too.

Homes built at or below base flood elevation experience more frequent claims than elevated properties. If your first floor sits at ground level near water, your flood exposure is genuine and ongoing.

Living Expenses and Excluded Coverage

The coverage gaps in standard NFIP policies create a second reason to consider excess insurance. NFIP doesn’t cover additional living expenses if your home becomes uninhabitable, meaning you pay out-of-pocket for temporary housing, meals, and relocation costs while repairs happen. In Naples, temporary rental housing easily runs $2,000 to $4,000 monthly or more, and repairs after major flooding take months. Excess policies fill this gap by covering those expenses automatically. Similarly, NFIP excludes basement contents entirely, detached structures, and certain building components. If you have a pool equipment room, detached garage, or finished basement, NFIP provides zero protection for those areas. Private excess flood policies can extend coverage to these exclusions, protecting assets NFIP ignores completely.

Lender Requirements and Financial Exposure

Your mortgage lender may also influence this decision. Some lenders require flood insurance limits that match your home’s full replacement cost, not NFIP’s standardized caps. Meeting those requirements often means adding excess coverage on top of primary policies. The practical reality for most Naples homeowners with properties worth $500,000 or more is straightforward: NFIP alone leaves you financially exposed. Excess flood insurance closes that exposure at a cost that’s far lower than the risk you’d carry without it. Understanding whether your property falls into these categories helps you move forward with confidence about what coverage you actually need.

Getting Excess Flood Insurance in Naples

Finding excess flood insurance requires a different approach than shopping for standard homeowners coverage. You cannot walk into a bank and buy excess flood through the NFIP-it exists only in the private market, and access depends on working with the right professionals. An independent insurance agent with relationships across multiple private insurers offering excess flood policies serves you best. Independent agents differ fundamentally from captive agents who represent a single company. They shop your property across multiple carriers simultaneously, comparing coverage options, limits, and pricing in hours rather than days. When you contact an agent, provide specific information about your home: its replacement cost value, current flood insurance policy details, elevation relative to base flood elevation, distance from water sources, and any special features like basements or detached structures. Agents use this data to determine which insurers will consider your property and what limits they’ll approve. The underwriting process for excess flood moves faster than primary policies because the insurer’s risk is lower-they only pay after your primary policy exhausts its limits. Most carriers deliver quotes within one to two business days.

Price Variations Between Carriers

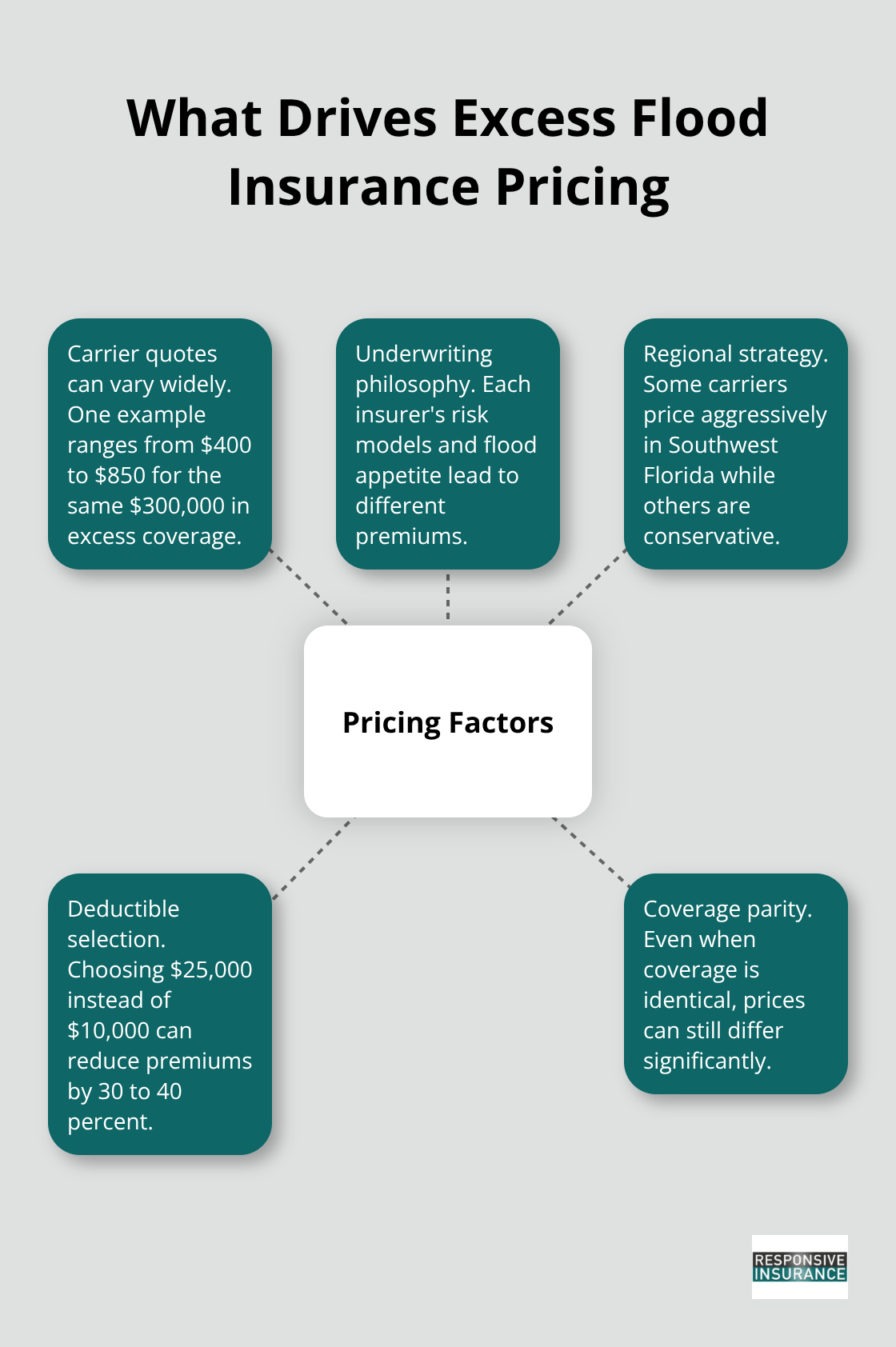

Price differences between insurers for identical coverage are substantial enough to warrant quotes from at least three carriers. One Naples homeowner seeking $300,000 in excess coverage on a home near Gordon River might receive quotes ranging from $400 annually from one insurer to $850 from another-a 112 percent difference for the same protection. These variations reflect different underwriting philosophies, risk models, and appetite for flood exposure. Some insurers price aggressively in Southwest Florida while others charge premiums reflecting their conservative stance on coastal properties. Deductible choices dramatically affect pricing too.

Selecting a $25,000 deductible instead of $10,000 reduces your annual premium by 30 to 40 percent, making excess coverage more affordable while still protecting against catastrophic losses.

Coverage Details Vary Significantly

Excess flood policies vary considerably in what they actually cover. Some policies extend your primary policy’s limits dollar-for-dollar, while others impose sublimits on specific coverages or exclude certain perils. A few insurers offer additional living expense coverage automatically; others require you to purchase it as an add-on. Some policies cover basement contents and detached structures; others don’t. The policy document itself contains the answers, but many homeowners skip this step or assume all excess policies are identical. That assumption costs money. Before you bind coverage, your agent should walk you through the specific exclusions, coverage triggers, and what happens if your primary policy is cancelled or lapses. Understanding whether your policy requires the primary flood insurance to remain active throughout the year matters-some excess policies become void if your primary coverage lapses, even temporarily. Ask your agent directly: What does this policy cover that my NFIP policy doesn’t? What is excluded? What happens if I file a claim? Asking these questions before you sign protects you from discovering gaps when you need the coverage most.

Final Thoughts

Excess flood insurance protects what standard policies won’t, and for Naples homeowners with properties worth $500,000 or more, this coverage bridges the gap between NFIP’s fixed limits and your actual replacement costs. NFIP caps residential structure coverage at $250,000 and contents at $100,000, leaving you exposed if your home exceeds those values. What is excess flood insurance fundamentally about is matching your protection to your actual exposure-it covers additional living expenses when your home becomes uninhabitable, protects basement contents and detached structures that NFIP excludes entirely, and provides the dollar limits your property genuinely needs.

The cost remains reasonable because the insurer’s risk is lower; they only pay after your primary policy exhausts its limits. Shopping multiple carriers reveals significant price variations, sometimes exceeding 100 percent for identical coverage, making comparison essential before you commit. Calculate your home’s true replacement cost value, review your current NFIP policy limits to identify specific coverage gaps, and contact an independent insurance agent who represents multiple excess flood carriers and can deliver quotes within days.

Contact Responsive Insurance, Inc. to discuss whether excess flood insurance makes sense for your home and to receive personalized quotes from carriers competing for your business. As an independent agency, we work with multiple A-rated insurance companies to compare excess flood options and find coverage matching your specific property and risk profile. We provide timely, complete answers to your questions and serve as your knowledgeable advocate throughout the process.