Florida Vacation Rental Policy Essentials for Hosts

Running a vacation rental in Florida means protecting a significant asset. A Florida vacation rental policy fills critical gaps that standard homeowners insurance simply won’t cover.

At Responsive Insurance, Inc., we’ve seen hosts lose thousands because they didn’t understand what their regular home policy excludes. The right coverage protects your property, your guests, and your income stream.

What Your Vacation Rental Policy Actually Covers

Property Damage Protection for Guest-Caused Losses

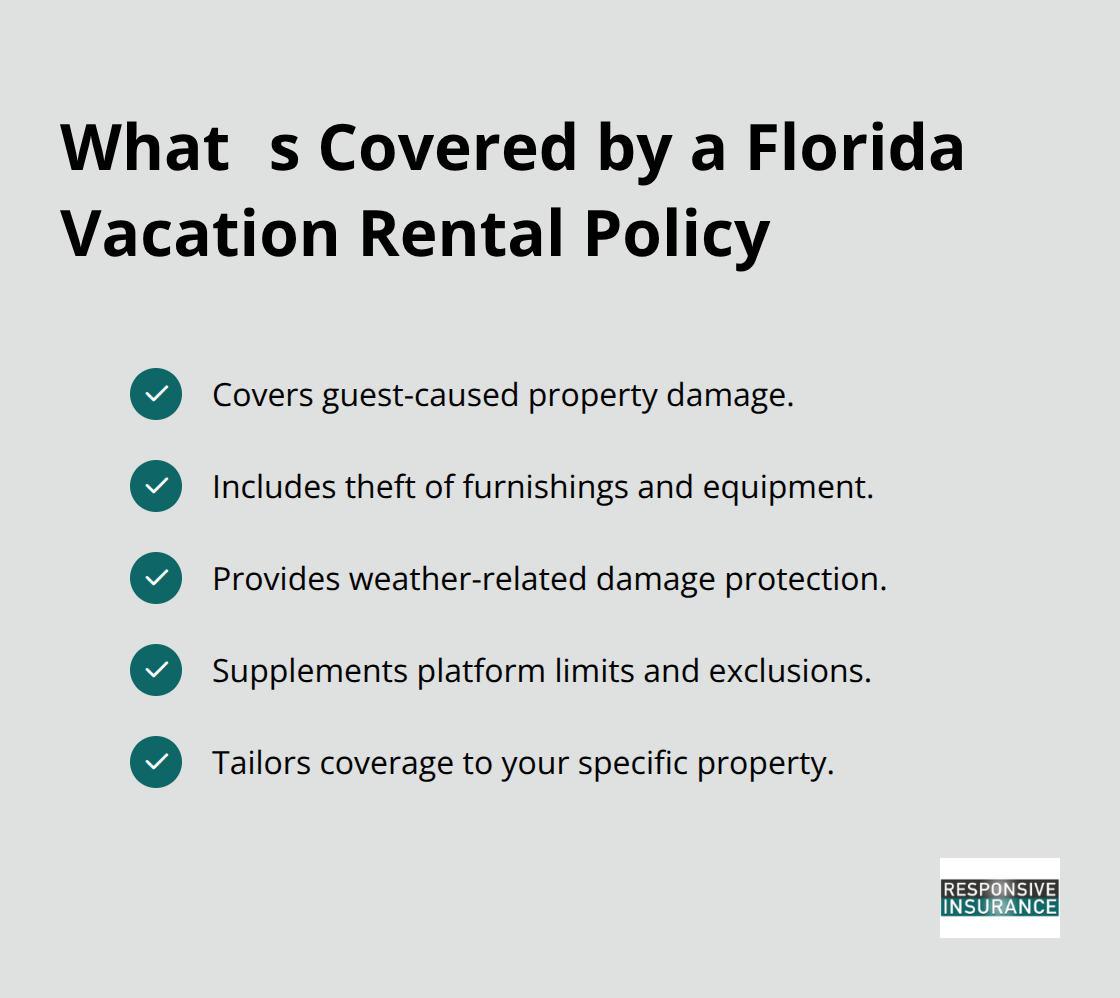

A Florida vacation rental policy protects your physical property when guests cause damage. Property damage coverage handles guest-caused destruction, weather events, and theft of your furnishings and equipment. If a guest breaks your kitchen cabinets, damages the air conditioning system, or steals outdoor furniture, your vacation rental policy covers repair or replacement costs. This matters because standard homeowners policies explicitly exclude business use, meaning a claim filed after guest damage could result in outright denial of coverage.

Airbnb’s Host Damage Protection provides up to $3,000,000 for damage to your place or belongings caused by a guest, though this applies only to Airbnb listings and comes with significant exclusions. A dedicated vacation rental policy fills these gaps with higher limits and broader protection tailored to your specific property.

Liability Coverage for Guest Injuries and Claims

Liability protection covers guest injuries and property damage claims that guests might file against you. Airbnb provides up to $1,000,000 per stay in Host Liability Insurance automatically, but this coverage has strict limits and numerous exclusions that leave you exposed. A dedicated vacation rental policy fills these gaps with higher limits and broader protection for injuries occurring on your property, medical payments for guest injuries, and damages guests cause to neighboring properties or common areas in condo buildings.

Loss of Rental Income When Disasters Strike

Loss of rental income coverage replaces the money you would have earned during repairs or remediation when a covered event makes your property temporarily uninhabitable. Florida hosts face particular exposure to hurricane season from June through November, and a single major storm can eliminate weeks or months of bookings. This coverage is essential financial protection that safeguards your income stream when circumstances beyond your control force you to close your doors.

Selecting the Right Coverage for Your Situation

When selecting a vacation rental policy, verify that your chosen plan includes all three components with limits appropriate to your property value and typical occupancy rates. Work directly with a licensed agent who understands Florida’s specific risks (including storm damage and seasonal variations) rather than relying solely on platform protections. The next step involves comparing what different carriers offer and understanding how their coverage options align with your property’s unique characteristics and your rental business model.

Key Gaps in Standard Homeowners Insurance

Why Your Home Policy Excludes Rental Activity

Standard homeowners insurance policies contain explicit business-use exclusions that activate the moment you start accepting paying guests. Insurers classify short-term rental activity as commercial use, and most homeowners policies simply do not cover business operations. When you file a claim after guest damage, the insurance company reviews your rental history and denies coverage outright, leaving you responsible for repair costs. This isn’t a gray area or a technicality that sympathetic adjusters might overlook-it’s a fundamental contract violation. The language in your current policy almost certainly states that coverage applies only to owner-occupied residential use, which excludes any property generating rental income.

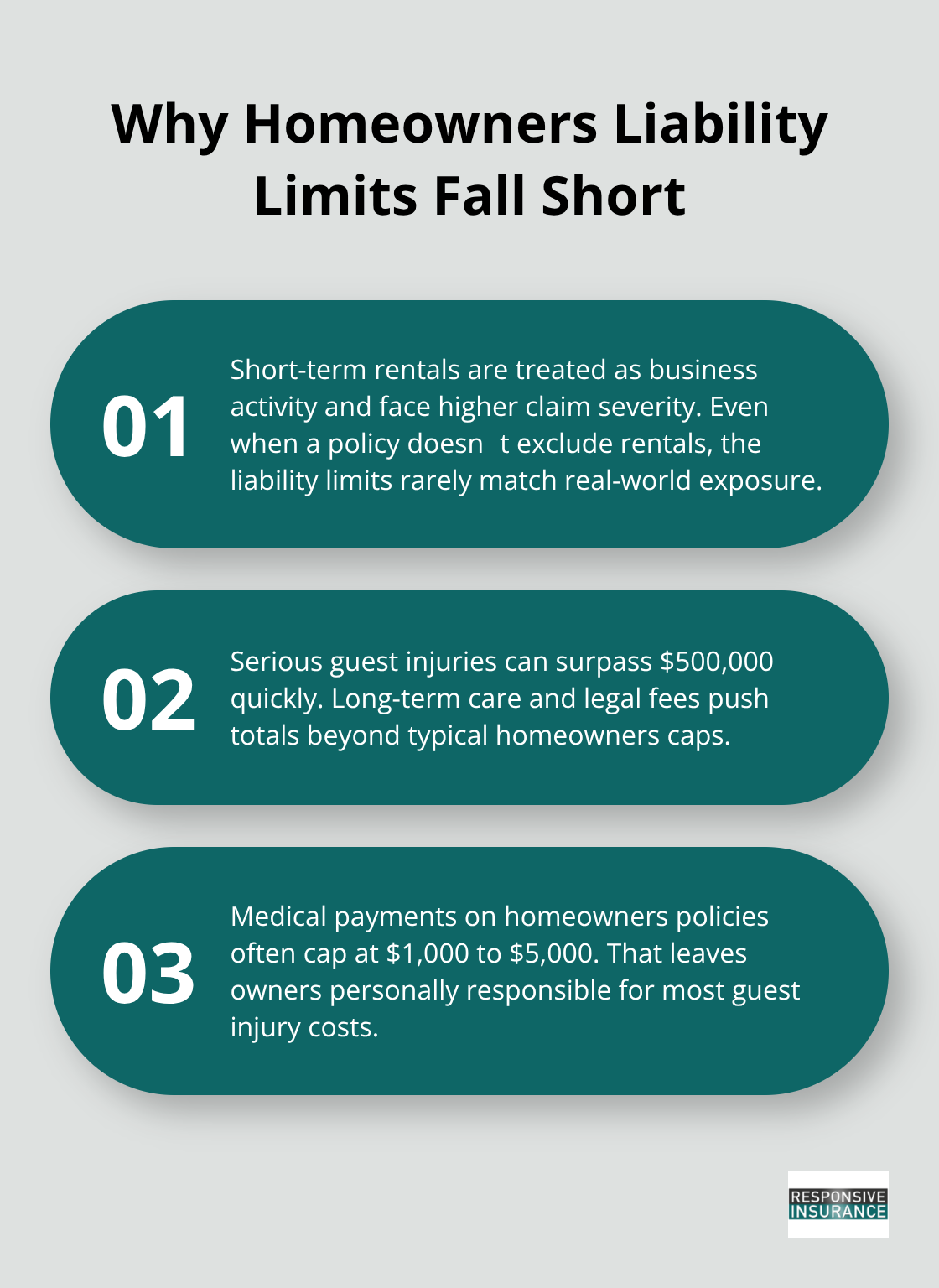

Liability Limits That Fall Short of Real Exposure

Coverage limits present a second critical gap. Even if your homeowners policy technically allowed rental activity, the liability limits fall catastrophically short of actual exposure. A single guest injury requiring hospitalization and long-term care can easily exceed $500,000 in medical costs and damages.

Florida’s legal environment favors guest claims, and juries routinely award damages well above standard homeowners limits. Medical payment coverage under homeowners policies maxes out at $1,000 to $5,000, leaving you personally liable for guest injuries.

Property Damage Coverage Designed for Owner-Occupants

Your property damage coverage also carries replacement cost limitations that don’t account for the accelerated wear from transient guests. A guest-caused kitchen fire triggers both property damage claims and liability claims simultaneously, potentially exhausting your entire limit on property damage alone while the liability exposure remains unaddressed. Standard homeowners policies simply weren’t designed to handle the frequency and severity of claims that vacation rentals generate.

The Real Financial Cost of Operating Unprotected

Operating without dedicated vacation rental coverage transforms every booking into financial risk. A single incident-a guest slip-and-fall, stolen artwork, or storm damage during peak season-can wipe out years of rental income and force you to liquidate assets to cover the gap between what insurance won’t pay and what you legally owe. This exposure explains why selecting the right vacation rental policy requires careful attention to coverage limits, exclusions, and the specific protections your property actually needs.

Selecting Coverage That Matches Your Property and Rental Business

Calculate Your Property’s True Replacement Cost

Choosing the right vacation rental policy starts with honest assessment of what you actually own and how intensively you rent it. A beachfront condo in Naples with year-round bookings faces entirely different risks than a seasonal mountain cabin with six weeks of summer guests. Document your property’s replacement cost by photographing all furnishings, equipment, and structural features, then obtain current replacement prices from local contractors and furniture retailers. This number drives your property damage coverage limit and prevents you from underinsuring your assets.

Determine Your Loss of Income Protection Needs

Calculate your average monthly rental income over the past twelve months and multiply by the number of months you typically close for maintenance or weather events. That figure determines your loss of income coverage limit. A property generating $8,000 monthly in peak season but sitting vacant three months annually for hurricane season needs income protection reflecting that $24,000 gap.

Many hosts underestimate this number and select limits that cover only partial losses, leaving them financially exposed when a major storm hits during booking season.

Review Policy Exclusions Rather Than Premium Price

Comparing policies requires examining what each carrier actually excludes rather than focusing on premium price alone. Request detailed policy documents from three carriers and review their specific exclusions for intentional acts, normal wear and tear, and guest negligence claims. Some carriers exclude coverage for pools and hot tubs entirely, while others charge endorsement premiums to add them. Airbnb’s platform protection caps at $3,000,000 for property damage but excludes theft by guests, intentional damage, and damage from normal use. A standalone vacation rental policy from a carrier typically provides broader coverage and higher limits without the platform restrictions.

Work with a Licensed Agent on Your Specific Situation

Request quotes that specify your exact coverage limits and ask the agent to identify gaps between what the policy covers and your actual exposure. The agent should also explain how your condo’s HOA rules or lease restrictions affect coverage eligibility. Many Naples properties fall under condo association restrictions that prohibit short-term rentals entirely or require owner approval, and insurance cannot protect you from regulatory violation. A licensed agent who has handled Florida vacation rental claims provides real insight into how policies perform when damage occurs, not just what the brochure promises. For properties in flood-prone areas, understanding excess flood insurance becomes critical-standard NFIP coverage is typically around $700 a year in high-risk areas, and property owners in low-to-moderate risk areas should ask their agents if additional protection is needed.

Final Thoughts

Your vacation rental investment in Florida requires protection that matches its actual value and the risks you face. Standard homeowners insurance excludes rental activity entirely, leaving you exposed to guest injuries, property damage, and income loss when disaster strikes. A Florida vacation rental policy fills those gaps with coverage designed specifically for properties that host transient guests and generate rental income.

Platform protections like Airbnb’s Host Damage Protection and Host Liability Insurance provide a baseline, but strict limits and exclusions leave significant exposure unaddressed. A single guest injury, theft, or storm damage can eliminate years of profit and force you to cover costs personally. You need dedicated coverage that reflects your property’s replacement cost, your typical occupancy rates, and Florida’s specific weather risks (particularly during hurricane season from June through November).

Start by documenting your property’s actual replacement cost and calculating your average monthly rental income to determine the coverage limits you actually need. Then request detailed policy documents from multiple carriers and compare what each one excludes rather than focusing solely on premium price. Contact Responsive Insurance, Inc. to discuss your property’s unique risks and receive a customized quote for vacation rental coverage that protects what matters most.