Florida Vacation Rental Insurance: Protecting Short-Term Rentals

Owning a vacation rental in Florida comes with unique risks that standard homeowners insurance simply won’t cover. Your guests, your rental income, and your property all need specialized protection.

Florida vacation rental insurance fills those gaps. We at Responsive Insurance, Inc. help property owners understand what coverage they actually need and how to avoid costly gaps in protection.

Why Standard Homeowners Policies Leave Vacation Rentals Unprotected

Standard homeowners insurance explicitly excludes short-term rental activity. If you rent your property to guests for stays under 30 days, your HO-3 policy will deny claims related to that business use. An insurer will refuse to pay for guest-caused damage, liability from guest injuries, or lost rental income if they discover you operate a vacation rental. This isn’t a gray area-it’s written directly into policy language. Many property owners discover this gap only after filing a claim and facing denial. In Florida, where the vacation rental market generates substantial income for homeowners, operating without proper coverage exposes you to catastrophic financial risk. A single guest injury lawsuit or major property damage event can result in tens of thousands of dollars in uninsured losses.

Rental Income Disappears Without Loss of Income Coverage

Your homeowners policy covers the physical structure and your personal belongings, but it will never reimburse lost rental income when damage forces you to cancel bookings. If a hurricane damages your kitchen or a guest accidentally causes a fire, you lose both the ability to rent and the income you depend on. Vacation rental insurance includes loss of rental income coverage, which replaces the money you would have earned during repairs or remediation. This coverage has clear limits and timeframes, so you know exactly what protection you have. Without it, you absorb 100 percent of the income loss yourself-a financial hit that can take months to recover from, especially during peak season cancellations.

Guest Liability Exposure Exceeds Standard Homeowners Limits

Vacation rentals attract higher liability exposure than owner-occupied homes. Guests cause damage at higher rates than permanent residents, and injury claims from guests unfamiliar with your property occur frequently. Standard homeowners liability limits of $100,000 to $300,000 fall short for rental properties. Vacation rental insurance provides commercial-grade liability protection starting at $1,000,000, which represents a smart minimum for properties in Southwest Florida. Additionally, vacation rental policies cover guest-caused theft and intentional damage-exposures that standard policies exclude entirely. A guest who damages furniture, breaks appliances, or steals electronics leaves you with no recovery path under a homeowners policy. Specialized vacation rental coverage closes these gaps and protects your investment from exposures that standard homeowners policies simply ignore.

What Vacation Rental Insurance Actually Covers

Vacation rental insurance replaces standard homeowners coverage with a policy designed specifically for properties rented to guests. Unlike an HO-3 policy that denies claims related to rental activity, vacation rental policies embrace short-term occupancy as their core purpose. The coverage typically includes property damage from guest-caused events, liability protection for injuries occurring on your property, loss of rental income when damage makes the property uninhabitable, and protection for amenities like pools, hot tubs, and provided equipment. Florida-specific risks such as hurricane damage and windstorm losses can be included, though flood coverage usually requires a separate policy through the National Flood Insurance Program or a private carrier. The policy also covers guest-caused theft and intentional damage, which standard homeowners policies exclude entirely.

This comprehensive approach means you’re protected against the exposures that actually threaten vacation rental owners, not the generic risks addressed by residential policies.

Guest Liability Claims Require $1 Million in Protection

A guest injured at your property can sue for medical bills, lost wages, and pain and suffering. If that guest hired an attorney and the injury was serious, the claim can easily exceed $300,000. Florida law requires a minimum of $1,000,000 in premises liability coverage for short-term rental properties in Southwest Florida. This limit covers you if a guest slips on a wet deck, falls down stairs, or suffers an injury from a pool or hot tub. The policy also covers liability for incidents that occur off-premises if they’re connected to your rental activity, such as a guest injured while using provided kayaks or bikes. Guest-caused damage claims represent another liability exposure. If a guest damages furniture, breaks windows, or causes a fire through negligence, your vacation rental policy covers the cost of repairs or replacement. Standard homeowners insurance would deny these claims outright.

Loss of Income Protection Covers Your Revenue Gap

When a hurricane, fire, or other covered loss damages your property, repairs typically take weeks or months. During that time, you cannot accept bookings and your rental income stops completely. Loss of rental income coverage reimburses you for the revenue you would have earned if the property remained available. The coverage has specific dollar limits and timeframes, so you know exactly how much protection applies. If your property generates $3,000 per month in average rental income and repairs take three months, loss of income coverage would reimburse up to your policy limit for that period. This protection matters in Florida, where weather-related damage frequently forces extended closures. Without it, you absorb the full income loss while still paying mortgage, property taxes, maintenance, and insurance premiums.

Additional Coverages That Protect Your Investment

Vacation rental policies extend beyond basic property and liability coverage. Amenities on and off-premises (pools, hot tubs, provided equipment, and outdoor furniture) receive protection under specialized endorsements. Guest-caused theft coverage shields you from losses when guests steal electronics, artwork, or other valuables-a gap that standard homeowners policies leave wide open. Some policies also include bed bug and flea protection, which covers extermination costs and lost revenue from canceled bookings due to infestations. Squatter protection provides legal support and lost revenue coverage if a guest refuses to vacate after their stay ends. These additional coverages address exposures unique to short-term rentals that traditional homeowners policies simply ignore.

Choosing the Right Coverage Limits for Your Property

The $1,000,000 premises liability minimum represents a starting point, not a ceiling. Higher-value properties or those with elevated risk factors (pools, hot tubs, multiple guest units) warrant higher limits or an umbrella policy for additional protection. Your loss of income coverage limit should align with your actual monthly rental revenue and account for seasonal fluctuations. If your property generates $4,000 per month during peak season but only $1,500 during off-season, your coverage limit should reflect the higher amount to protect your peak-season income. Property damage limits should cover the full replacement cost of your structure, furnishings, and amenities. An independent insurance agent can help you evaluate your specific property, occupancy patterns, and financial exposure to set appropriate limits that match your actual risk profile.

Key Considerations When Choosing Vacation Rental Insurance

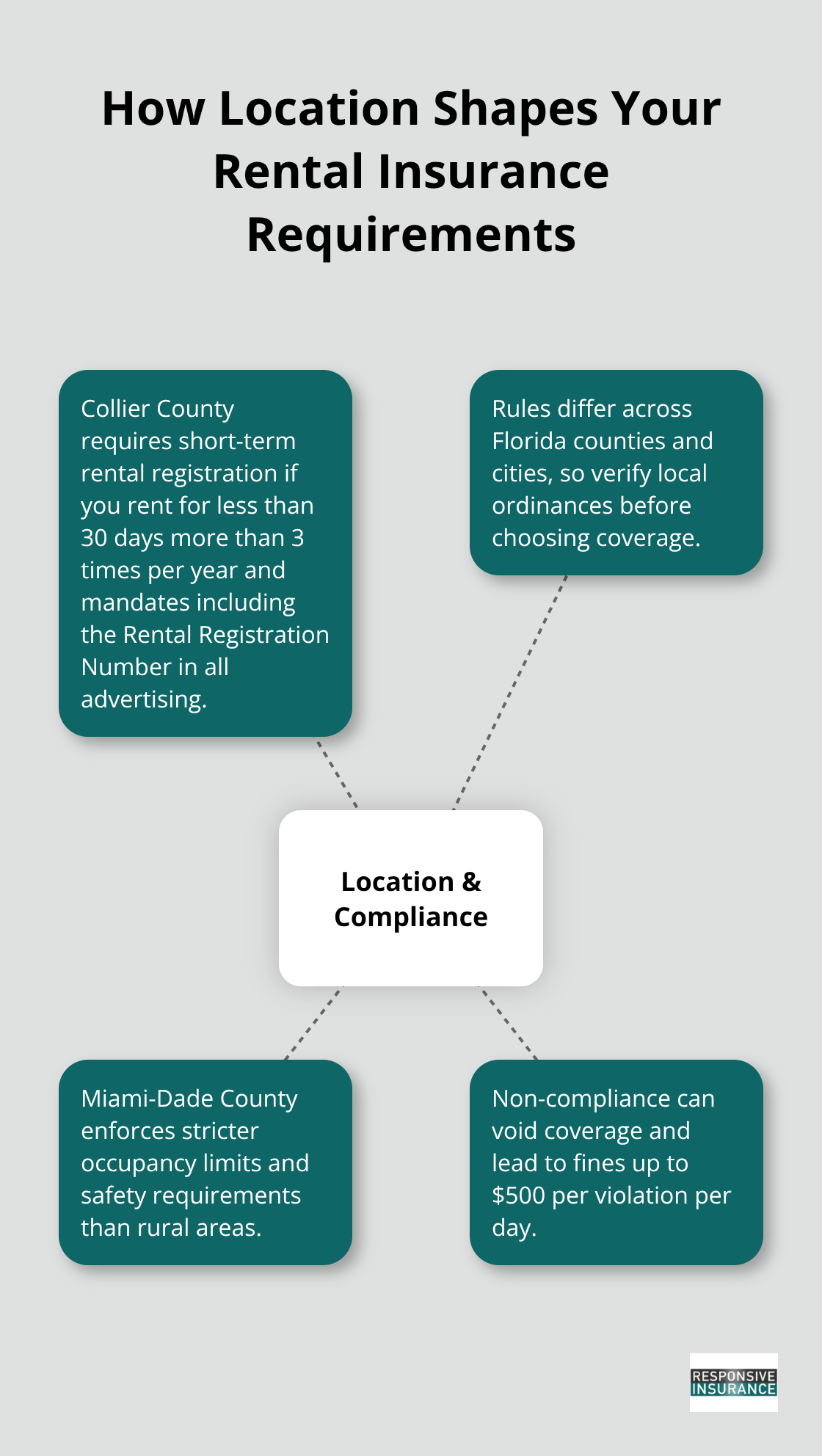

Location Determines Your Regulatory and Coverage Requirements

Your vacation rental’s location within Florida determines which regulations apply and what coverage gaps exist. Collier County requires short-term rental registration if you rent in increments of less than 30 consecutive days more than 3 times per year, and you must include your Collier County Rental Registration Number in all advertising across print, radio, video, online, social media, and sharing platforms. Other Florida counties and cities impose different rules. Miami-Dade County, for example, enforces stricter occupancy limits and safety requirements than rural areas. Before selecting a vacation rental policy, verify your specific county or city ordinances because non-compliance can void coverage or result in fines up to $500 per violation per day under the Consolidated Code Enforcement Ordinance.

Properties with pools face additional Florida pool safety requirements statewide, which means your liability coverage must account for this elevated exposure. Wind deductibles for hurricane coverage vary significantly by location. Coastal properties in Naples or Destin face higher wind deductibles than inland properties in Orlando, sometimes ranging from 1 percent to 5 percent of your home’s insured value. A $400,000 property with a 5 percent wind deductible means you pay $20,000 out-of-pocket before coverage kicks in for hurricane damage.

This geographic reality makes flood insurance critical for waterfront properties, since most vacation rental policies exclude flood damage. The National Flood Insurance Program or private flood carriers become mandatory additions for properties in flood zones.

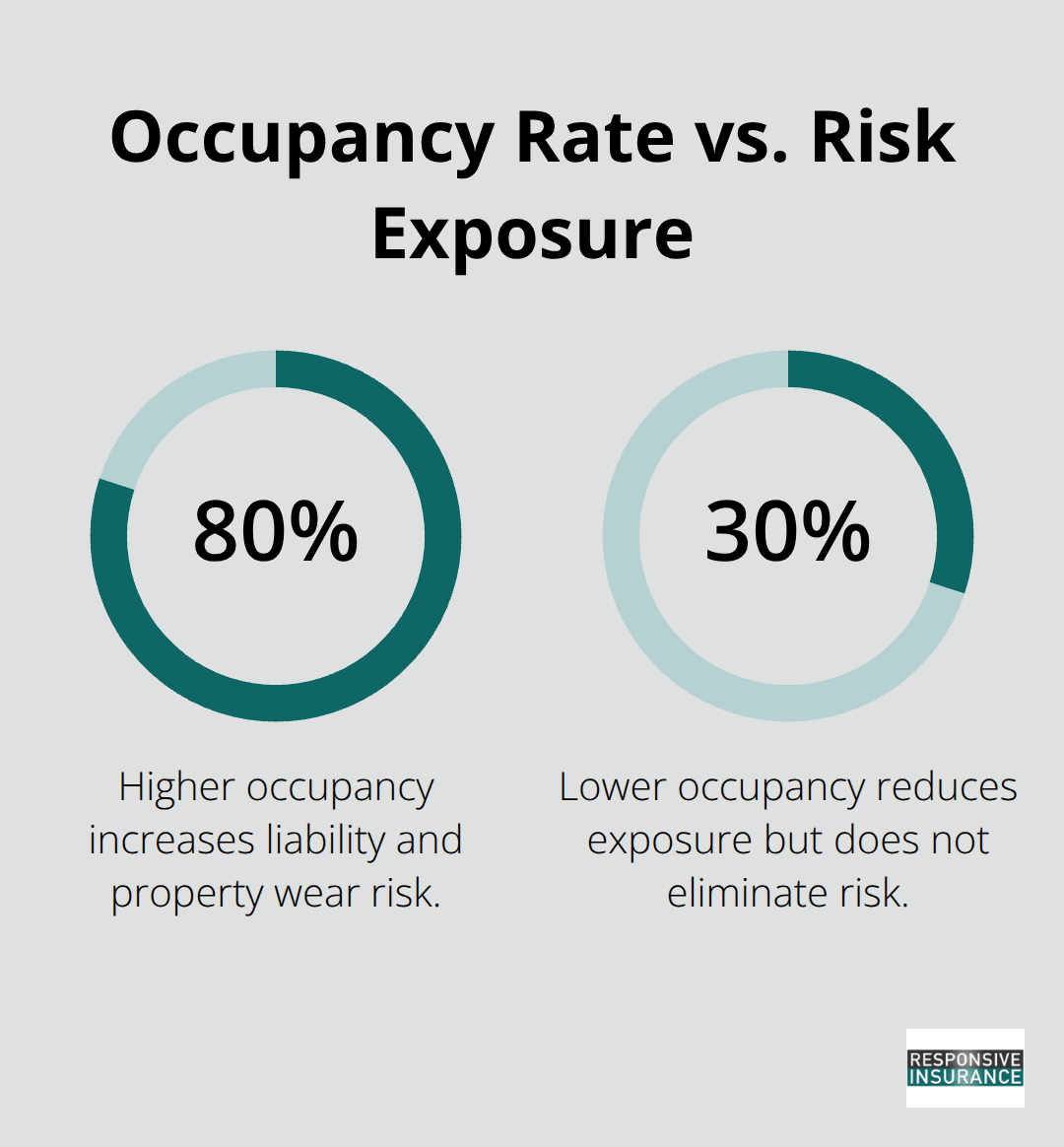

Guest Volume and Seasonal Patterns Impact Your Coverage Limits

Guest volume and seasonal patterns directly impact your income protection needs and claims risk. Properties that operate year-round with consistent bookings require different coverage limits than seasonal rentals that close for months. If your property generates $5,000 monthly during peak season but only $800 during off-season, your loss of income coverage limit should protect the higher amount.

Occupancy rates matter significantly. Properties booked 80 percent of the time face higher liability exposure than those booked 30 percent of the time, since more guests means more damage and injury incidents. A property with constant turnover experiences more wear on furnishings, appliances, and amenities, which translates to higher replacement costs and more frequent claims.

Comparing Quotes Requires More Than Price Comparison

When comparing quotes from multiple providers, request coverage from carriers that understand Florida’s specific risks. Admitted carriers regulated by the Florida Office of Insurance Regulation offer Florida Insurance Guaranty Association protection if the insurer fails, whereas surplus lines carriers lack this protection. The difference matters. If a surplus lines carrier becomes insolvent after you file a major claim, you have limited recourse.

Request quotes from at least three providers and compare not just premium but deductibles, exclusions, and limits. A policy priced $200 cheaper monthly might exclude guest-caused theft or cap loss of income at $2,000 per month, making it worthless when you need it. Proper Insurance, the top insurer of short-term rentals in Florida, offers commercial general liability starting at $1,000,000 with bed bug and flea protection plus squatter coverage included, addressing exposures that most standard policies exclude.

We at Responsive Insurance, Inc. help vacation rental owners in Southwest Florida evaluate multiple carriers and find policies that match your actual exposure rather than settling for the lowest price.

Final Thoughts

Florida vacation rental insurance protects your income, property, and financial future in ways that standard homeowners policies simply cannot. The gap between what you think you’re covered for and what you actually are covered for costs vacation rental owners thousands of dollars every year. A guest injury, fire damage, or hurricane forces you to choose between absorbing massive losses or fighting with an insurer who never intended to cover rental activity in the first place.

Setting appropriate coverage limits requires honest assessment of your actual exposure, not guessing based on what sounds reasonable. Your liability limits should reflect the real risk your guests present, your loss of income coverage should match your peak-season revenue, and your property damage limits should cover full replacement costs for your structure and amenities. These decisions demand careful evaluation of your specific property, location, and income needs.

Contact Responsive Insurance, Inc. today to request quotes from carriers that specialize in Florida vacation rental insurance and get the protection your investment deserves. We work with multiple A-rated insurance companies to compare coverage options and find policies that match your actual needs rather than settling for the cheapest option available. As an independent agency based in Naples, Florida, we understand the specific risks that vacation rental owners face in Southwest Florida.