Southwest Florida Rental Insurance: What You Need to Know

Renting in Southwest Florida comes with unique risks, from hurricane damage to theft. Most renters don’t realize their landlord’s insurance won’t cover their personal belongings or liability.

At Responsive Insurance, Inc., we’ve helped countless Naples renters understand what Southwest Florida rental insurance actually protects. This guide walks you through coverage options, how to choose the right policy, and why local expertise matters.

Understanding Rental Insurance in Southwest Florida

Rental insurance protects your personal belongings and shields you from liability claims when someone gets hurt in your apartment or you accidentally damage their property. In Southwest Florida, where hurricanes and theft pose genuine threats, this coverage becomes essential. Your landlord’s insurance covers only the building structure, not your furniture, electronics, clothes, or any other items you own. If a hurricane damages your belongings or a guest slips and sues you, your landlord’s policy won’t help. According to the Insurance Information Institute, renters insurance costs approximately $250 per year in Florida, yet many renters skip it entirely. That decision puts thousands of dollars at risk.

What Actually Gets Covered

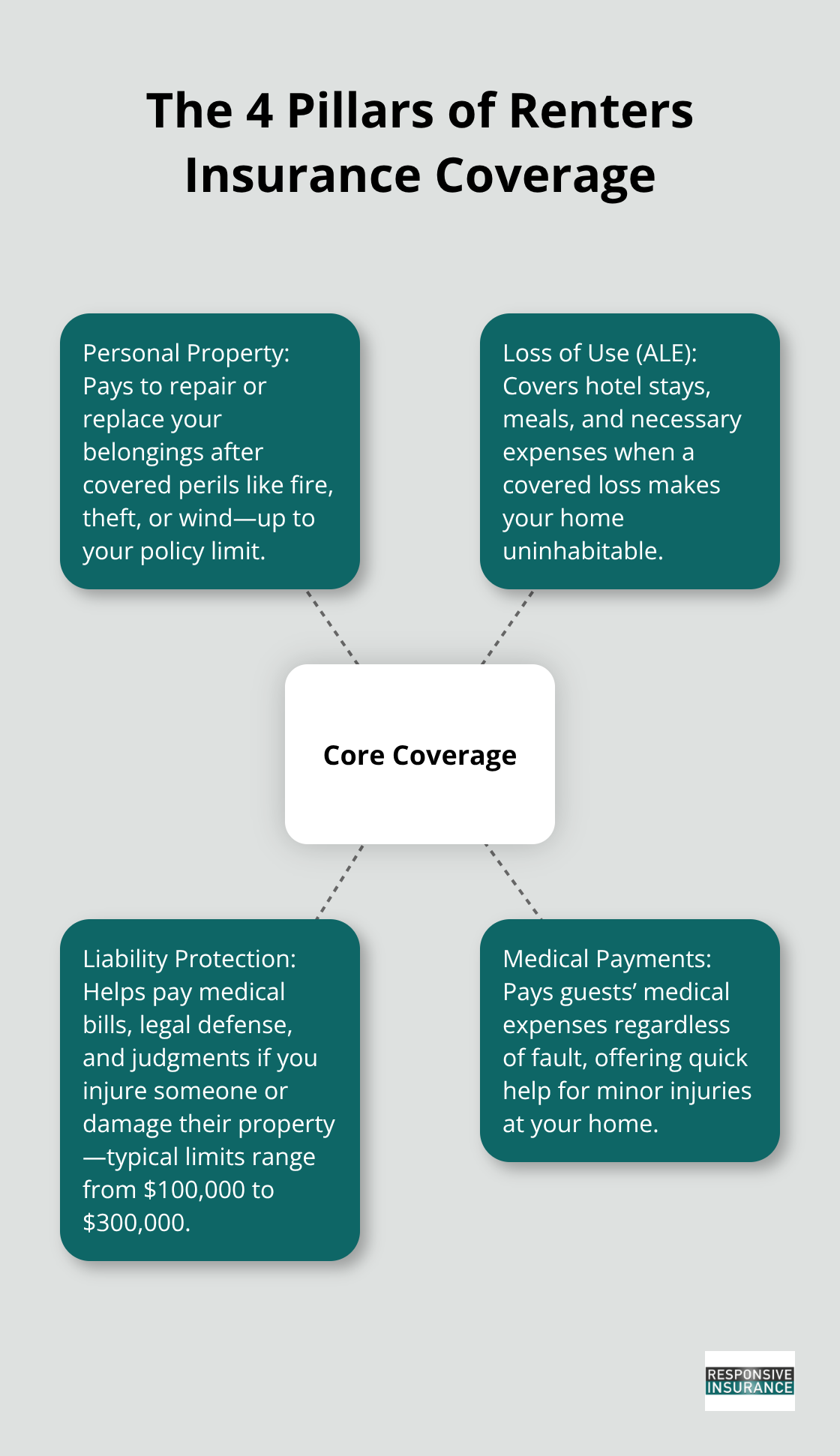

Rental insurance includes four main components. Personal property coverage pays to replace your belongings up to your policy limit if fire, theft, wind, or other covered perils damage them. Loss of use coverage pays for hotel stays and meals if your apartment becomes uninhabitable after a covered event.

Liability protection covers medical bills and legal defense if someone is injured at your place and sues you (typical limits range from $100,000 to $300,000). Medical payments coverage pays medical expenses for guests injured in your home, regardless of fault.

High-value items like jewelry or electronics often have sublimits on standard policies, meaning they won’t be fully covered unless you add a scheduled personal property endorsement. In Southwest Florida, wind damage to your belongings is typically covered, but flood damage is not and requires a separate flood insurance policy through the National Flood Insurance Program.

Why Naples Renters Underestimate This Risk

Most renters believe they don’t need insurance because they don’t own much, yet the average apartment contains $15,000 to $25,000 worth of belongings. A laptop, television, furniture, and clothing add up quickly. Southwest Florida residents face elevated hurricane risk during the June through November season, and flood zones cover significant portions of Naples and surrounding areas according to FEMA flood maps.

A single hurricane can destroy everything you own, and without renters insurance, you’ll absorb the entire cost.

Liability claims are equally serious-if a visitor is injured at your rental and sues, your personal assets could be at stake without liability protection. The cost of avoiding coverage is far higher than the cost of purchasing it. Understanding what your policy covers and what it doesn’t is the first step toward making an informed decision about your protection needs.

What Rental Insurance Actually Covers

Personal Property Coverage Protects Your Belongings

Personal property coverage pays to repair or replace your belongings when fire, theft, wind, or other covered perils damage them, up to your policy limit. Replacement cost value refers to the full cost to replace your items with new ones, while actual cash value refers to what your current items are worth in their depreciated condition. If your television is destroyed in a hurricane, replacement cost coverage pays what a new television costs now, not what yours was worth five years ago.

Most renters underestimate their belongings’ value until they actually inventory everything. Your furniture, clothing, electronics, kitchen items, bedding, and personal care products add up to thousands of dollars faster than you’d expect. FEMA and the Insurance Information Institute both suggest building a detailed home inventory with photos and receipts to prove what you owned if you need to file a claim. This documentation speeds up claim processing significantly and prevents disputes about item values.

High-Value Items Need Extra Protection

High-value items like jewelry, art, or expensive electronics often have sublimits on standard policies, meaning they cap out at $500 or $1,000 regardless of their actual value. If you own items worth more than standard limits cover, you’ll need a scheduled personal property endorsement that lists those items individually with their full values. This additional coverage ensures that your most valuable possessions receive adequate protection.

Liability Protection Shields Your Personal Assets

Liability protection is the coverage many renters ignore until they need it desperately. If someone is injured at your apartment and sues you, or if you accidentally damage someone else’s property, liability coverage pays their medical bills, legal defense costs, and court judgments up to your policy limit. According to the Insurance Information Institute and the National Association of Insurance Commissioners, most households should carry at least $100,000 in liability coverage, though $300,000 or more is increasingly common and strongly recommended.

A single lawsuit from a guest who slips and falls or a visitor injured by your dog could easily exceed $100,000 in medical bills and legal fees. Without adequate liability protection, a judgment could attach to your personal assets and wages. This coverage protects what you’ve worked hard to build.

Additional Living Expenses Cover Temporary Relocation

Additional living expenses coverage addresses what happens when your apartment becomes uninhabitable after a covered loss like a fire or hurricane damage. This coverage pays for hotel stays, restaurant meals, and other necessary expenses while repairs are underway, typically covering up to 20 to 40 percent of your personal property limit according to the Insurance Information Institute. In Southwest Florida, where hurricane season runs from June through November, this coverage becomes invaluable when storm damage forces you to relocate temporarily.

Understanding what each coverage component does positions you to make smart decisions about your protection. The next step involves assessing how much coverage you actually need based on your specific situation and belongings.

Choosing the Right Coverage for Your Naples Rental

Inventory Your Belongings Accurately

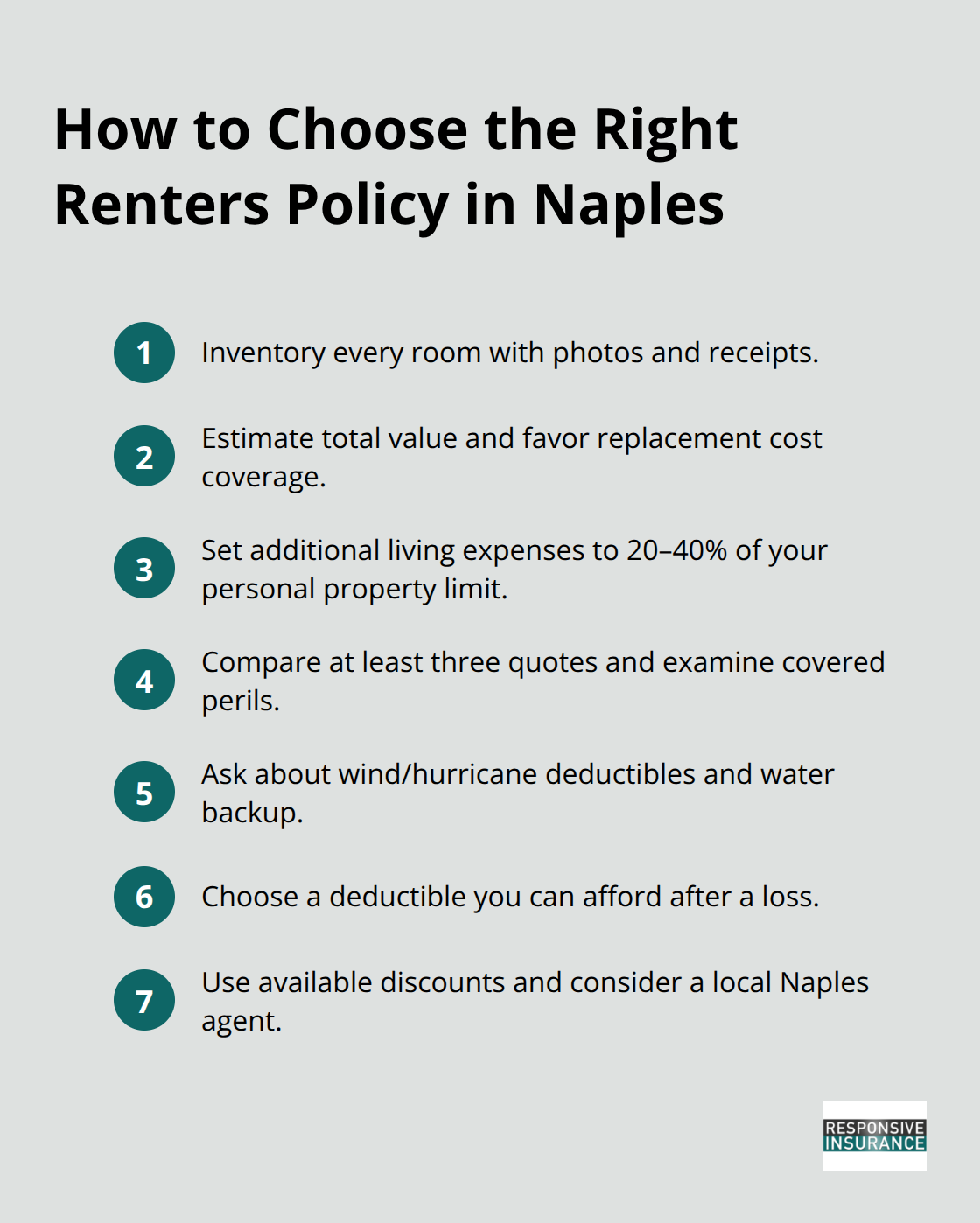

Start by listing everything you own. Walk through your apartment and document each item-furniture, electronics, clothing, kitchen appliances, bedding, and decorative pieces. The Insurance Information Institute recommends photographing everything and keeping receipts for major purchases. Personal property coverage baseline involves estimating your total belongings value through a thorough home inventory. Don’t guess at values or round down; accurate inventory prevents underpayment during claims.

Assess Your Liability Exposure

Determine your liability needs by considering your lifestyle. Do you host frequent gatherings? Do you have pets?

Are visitors regularly in your space? If you entertain often or own a dog, liability claims become more likely, which argues for $300,000 in coverage rather than the minimum $100,000. The cost difference between these limits is minimal-often just a few dollars monthly-yet the protection difference is substantial.

Calculate Additional Living Expenses Coverage

For additional living expenses, the Insurance Information Institute suggests covering 20 to 40 percent of your personal property limit. If your personal property coverage is $20,000, try $4,000 to $8,000 in additional living expenses coverage. During hurricane season in Southwest Florida, this cushion matters enormously when storm damage forces you into temporary housing.

Compare Quotes from Multiple Insurers

Quotes from at least three different insurers reveal significant price variations and coverage differences. Progressive reported average monthly renters insurance costs around $20.74 in Florida during 2024, but your actual rate depends on your location within Naples, deductible choice, coverage limits, and claims history. When comparing quotes, pay attention to what each policy actually covers. Some insurers cover wind damage to personal property more comprehensively than others, while coverage for water backup varies considerably. Ask each insurer specifically about hurricane deductibles-Florida policies often include separate wind or hurricane deductibles ranging from 2 to 10 percent of dwelling value.

Choose Your Deductible Wisely

Understand your deductible options thoroughly. Higher deductibles lower premiums, but only select a deductible you can realistically pay out of pocket after a loss. A $1,000 deductible saves money monthly, but if you cannot pay $1,000 when disaster strikes, that savings disappears. Many insurers offer discounts for bundling renters with auto insurance, installing security systems, or paying annually rather than monthly. These discounts can reduce your annual cost by 10 to 25 percent according to the Insurance Information Institute. A local agent in Naples provides advantages that online quotes cannot match-they understand Southwest Florida’s specific flood zones, hurricane exposure, and local building requirements that affect your coverage needs and pricing.

Final Thoughts

Southwest Florida rental insurance protects what matters most-your belongings and your financial security. Personal property coverage replaces your belongings up to your policy limit, liability protection shields your personal assets from lawsuits, and additional living expenses coverage pays for temporary housing when your rental becomes uninhabitable. These three components work together to address the specific risks renters face in Naples and surrounding areas.

Your next step is straightforward: inventory your belongings, determine how much liability coverage you need based on your lifestyle, and obtain quotes from multiple insurers. Compare what each policy actually covers rather than focusing solely on price. Pay special attention to hurricane deductibles, flood exclusions, and sublimits on high-value items. A $250 annual investment in Southwest Florida rental insurance prevents thousands of dollars in potential losses and protects you from liability claims that could devastate your finances.

An independent agency understands Naples’ flood zones, hurricane exposure, and local building requirements that affect your coverage needs and pricing. Rather than navigating online quotes alone, a local agent advocates for you by comparing multiple A-rated insurance companies to find the best fit for your specific situation. Contact Responsive Insurance, Inc. today to discuss your rental insurance needs and secure the coverage that protects your Naples home.