Airbnb Insurance Florida Your Guide for Short-Term Rentals

Renting out your Florida property on Airbnb can generate solid income, but your standard homeowners policy won’t protect you. At Responsive Insurance, Inc., we’ve seen hosts face unexpected gaps in coverage that cost them thousands.

This guide walks you through Airbnb insurance Florida options, what coverage actually matters, and how to pick the right policy for your rental business.

Why Standard Coverage Fails Florida Airbnb Hosts

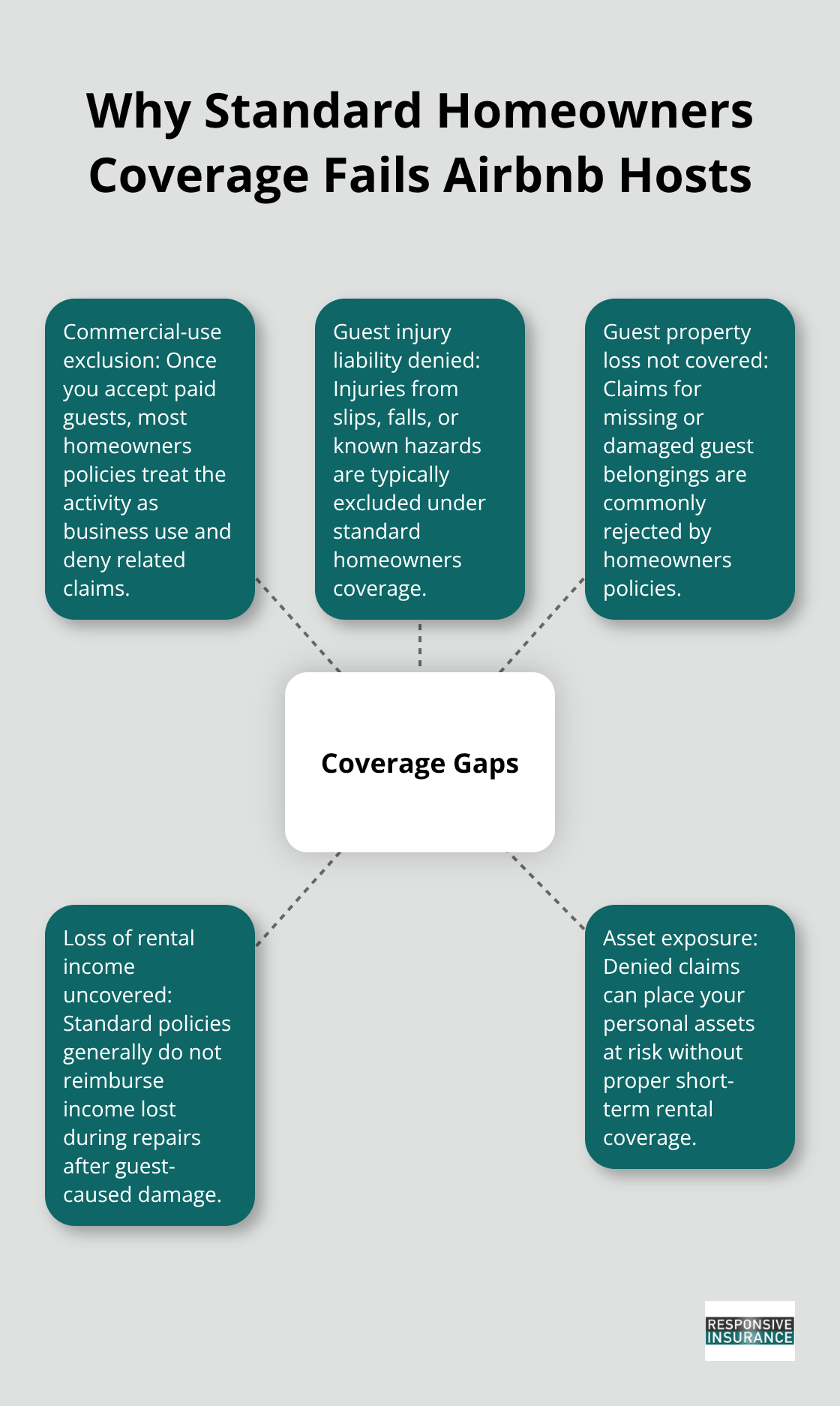

Your homeowners insurance policy covers you living in the home, not running a rental business from it. The moment you list your property on Airbnb and accept payment from guests, your standard policy no longer applies. Insurers classify this activity as commercial use, and standard homeowners insurance excludes commercial rental activities. If a guest slips on your kitchen tile and breaks their wrist, or if someone’s belongings go missing during their stay, your homeowners policy will deny the claim. Nearly every standard homeowners contract contains this exclusion. The reason is simple: if you generate income from the property, traditional coverage stops protecting you.

Florida Law Imposes the Highest Duty of Care

Florida law treats Airbnb guests as business invitees, which means you have the highest legal duty to keep your property reasonably safe. This obligation exceeds what you owe to social guests or trespassers. A guest injured due to a hazard you knew about but failed to fix can sue you for medical expenses, lost wages, and pain and suffering. Slip-and-fall injuries occur frequently in vacation rentals, along with burns from appliances and exposure to hazards like faulty electrical wiring or mold. A single injury claim can easily exceed $50,000 in medical costs and damages. Florida uses modified comparative negligence, meaning you can still face liability even if the guest bears some responsibility for the incident. Your personal assets remain at risk if you rely on a standard homeowners policy.

Guest Damage Drains Your Profits

Guests cause property damage at rates far higher than owner-occupied homes experience. Broken furniture, stained carpets, damaged appliances, and theft between turnovers represent routine expenses for short-term rental operators. A single week of property damage costs $2,000 to $5,000 in repairs, depending on severity. The real financial hit comes from lost rental income while you handle repairs and turnover. If a guest causes significant damage requiring two weeks to fix, you lose all bookings during that period. Your mortgage, property taxes, and maintenance costs continue regardless. Standard homeowners policies cover neither the guest-caused damage nor the resulting loss of rental income. Dedicated short-term rental insurance addresses both exposures, protecting the physical property and the income stream that makes your investment viable.

This protection becomes even more important when you understand what coverage options actually exist for Florida hosts.

What Insurance Actually Covers Your Airbnb Business

Airbnb’s Host Protection Insurance Has Critical Gaps

Airbnb’s Host Protection Insurance provides up to $1 million in liability coverage for bodily injury or property damage claims, which sounds substantial until you examine what it excludes. The coverage does not apply to intentional acts, or injuries from hazards you knew about but failed to fix. This last exclusion is particularly problematic in Florida, where premises liability law requires you to maintain the property to a reasonable standard. If a guest discovers mold you were aware of and suffers respiratory issues, Airbnb’s coverage will deny the claim because you had prior knowledge of the hazard. The $1 million limit also becomes inadequate when a serious injury occurs. A guest hospitalized after a slip-and-fall may incur $100,000 in emergency surgery and rehabilitation costs alone, leaving you responsible for anything exceeding the Airbnb limit.

Dedicated Short-Term Rental Policies Fill Coverage Voids

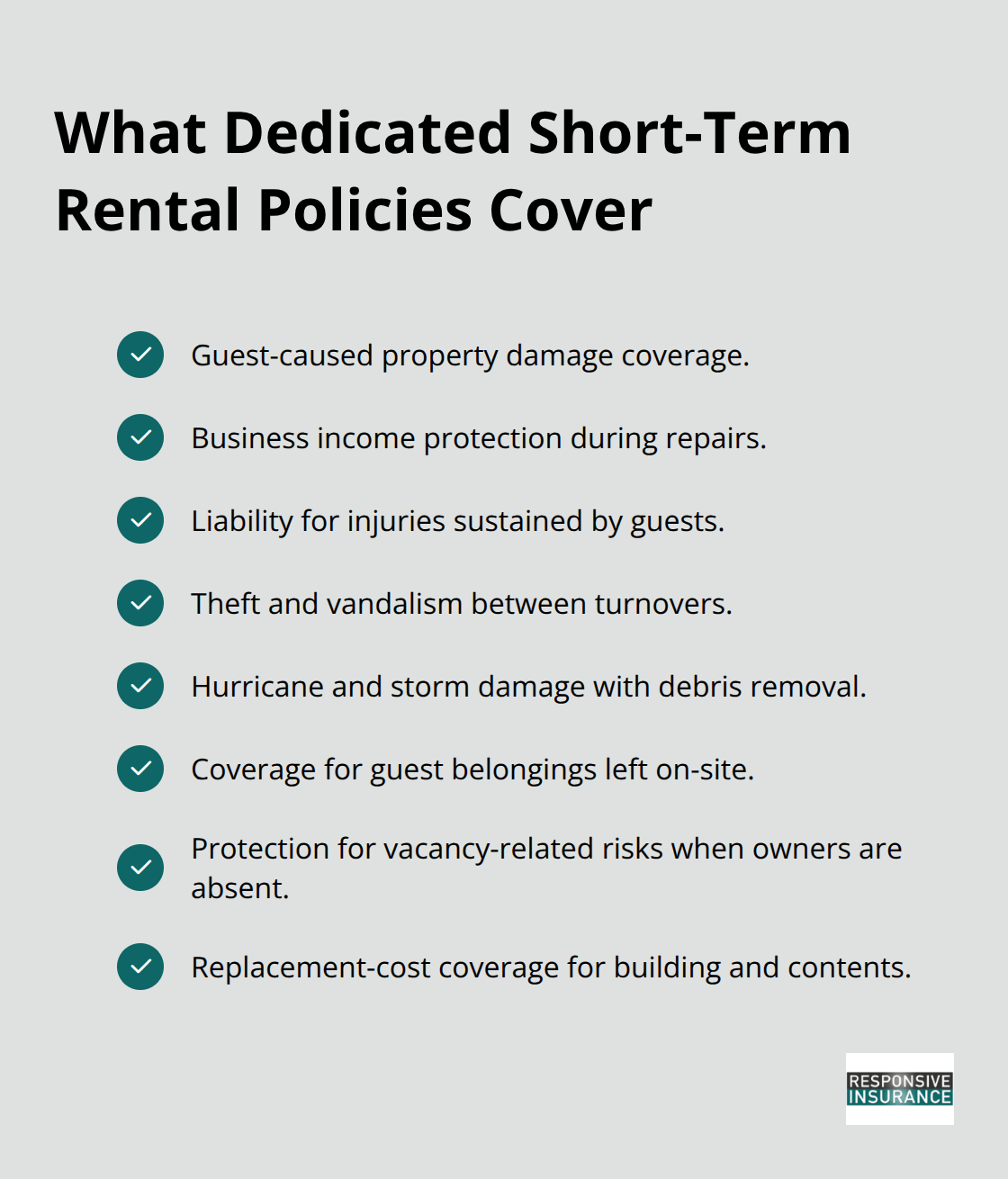

Dedicated short-term rental policies fill the voids that Airbnb’s coverage leaves open. These policies cover guest-caused property damage, loss of rental income during repairs, liability for injuries guests sustain on the property, theft and vandalism between turnovers, and damage from weather events like hurricanes. A comprehensive Florida short-term rental policy typically includes $1 million in general liability, replacement-cost coverage for building and contents, business income protection with no time limit, and coverage for guest belongings left on the property. If you furnish the home with expensive décor, artwork, or high-end appliances, the policy should reflect the actual replacement cost rather than depreciated value. Properties with pools, hot tubs, or guest amenities like kayaks require additional liability riders because these features increase injury risk. Coastal properties in Naples and surrounding areas face elevated hurricane exposure, making coverage for storm damage and debris removal essential. Insurers emphasize that vacation rental policies address vacancy-related risks that occur when owners are absent, a scenario standard homeowners policies explicitly exclude.

Cost and Coverage Considerations for Your Property

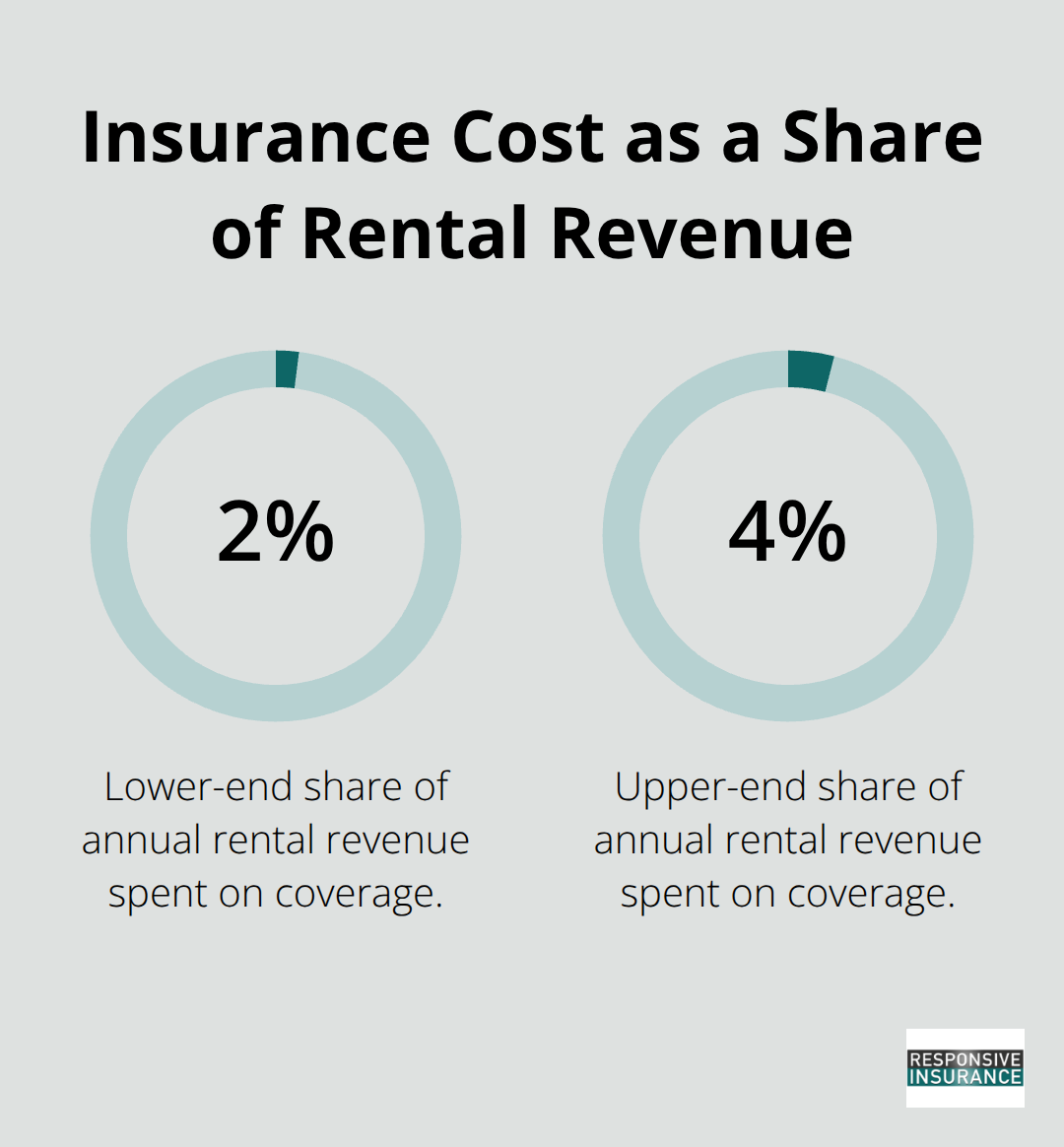

The cost difference between relying on Airbnb’s Host Protection Insurance and purchasing dedicated coverage typically ranges from $1,200 to $2,500 annually, depending on property value and location. For a property generating $40,000 to $60,000 in annual rental income, this investment represents 2 to 4 percent of gross revenue and protects against losses that could wipe out an entire year’s profits. High-value properties with guest amenities justify higher coverage limits and specialized endorsements.

If your rental includes a pool, fire pit, or activities like kayaking, standard liability limits become insufficient because guest injuries from these features trigger substantial medical claims. Some policies offer liquor liability coverage, which protects you if a guest becomes intoxicated and injures themselves or others-an exclusion in most standard homeowners policies. Properties in flood zones require separate flood insurance through the National Flood Insurance Program or private carriers, as neither homeowners nor short-term rental policies cover flood damage. Landlord insurance in Florida covers property damage, liability, loss of rent, and other essential protections that align with short-term rental needs.

Understanding what coverage exists allows you to make informed decisions about your protection strategy, but selecting the right policy requires careful evaluation of your property’s unique characteristics and rental activity.

Selecting the Right Coverage for Your Naples Property

Calculate Your Property’s True Replacement Cost

Start with your property’s actual replacement cost, not its market value. A $500,000 beachfront home might cost $800,000 to fully rebuild after a hurricane, plus additional expenses for debris removal and code upgrades required by current Florida Building Code standards. Insurance companies in Florida use replacement cost estimates that account for labor inflation and material scarcity post-disaster. Request a detailed property appraisal from your carrier or a professional appraiser to establish accurate building coverage limits. This step prevents you from underinsuring your investment and facing out-of-pocket losses after a major loss.

Protect Your Rental Income During Repairs

Track your rental income for the past 12 months and multiply that figure by the number of months required to complete significant repairs. If your property generates $5,000 monthly and repairs typically take 6 to 8 weeks, your business income protection should cover at least $10,000 to $15,000. This calculation ensures you can cover your mortgage, property taxes, and maintenance costs while the property sits vacant during reconstruction. Without this protection, a major hurricane or fire forces you to absorb all operating expenses while losing all revenue.

Match Liability Limits to Your Guest Activity

Guest volume matters directly to your liability exposure. A property rented 40 weeks annually with 4 guests per week faces higher injury risk than one rented 20 weeks with 2 guests per week. Insurers adjust premiums and coverage recommendations based on occupancy patterns, so provide accurate booking data when requesting quotes. Properties with pools, hot tubs, or guest amenities like kayaks require liability limits of at least $1 million, sometimes $2 million depending on local court awards. In Naples and Collier County, premises liability judgments for serious injuries frequently exceed $100,000, making adequate limits non-negotiable.

Select Deductibles You Can Actually Afford

Deductibles directly impact your out-of-pocket costs when claims occur, so select amounts you can actually pay. A $1,000 deductible reduces your premium by roughly 15 to 20 percent compared to a $500 deductible, but only choose this if you maintain emergency funds to cover it. Coastal properties in Naples should carry deductibles no higher than $2,500 for hurricane coverage, as storm-related claims happen frequently and repair costs accumulate rapidly.

Compare Specialized Carriers and Independent Agents

Compare quotes from at least three carriers that specialize in Florida short-term rentals, not general homeowners insurers. Specialized carriers understand local code requirements, flood zone complexities, and guest-activity risks in ways standard providers do not. Request detailed comparisons showing coverage for guest-caused damage, loss of rental income, theft between turnovers, and liability limits. Ask each carrier whether they cover liquor liability and what exclusions apply to guest injuries from property defects. Schedule a consultation with an independent agent who represents several carriers rather than relying on a single company’s offerings. Independent agents can access broader markets and negotiate better terms for properties with specific risk profiles.

Final Thoughts

Your Airbnb rental in Naples generates income only when guests feel safe and your property remains protected. Standard homeowners insurance abandons you the moment you accept payment from renters, leaving you exposed to liability claims, guest damage, and lost income during repairs. Dedicated short-term rental policies address these gaps by covering guest-caused damage, loss of rental income, theft between turnovers, and liability for injuries sustained on your property.

Airbnb’s Host Protection Insurance provides a baseline of coverage, but its exclusions for known hazards and its $1 million limit fall short when serious injuries occur. The cost of proper Airbnb insurance Florida typically ranges from $1,200 to $2,500 annually, a small percentage of your rental income that protects against losses exceeding $50,000 or more. Request quotes from at least three carriers specializing in Florida short-term rentals, comparing their coverage for guest damage, business income protection, and liability limits.

We at Responsive Insurance, Inc. work with multiple A-rated insurance companies to find coverage that protects your rental business and your personal assets. Contact Responsive Insurance, Inc. today to discuss your short-term rental insurance needs and secure the coverage your investment deserves.