Florida Insurer Comparisons Naples: How to Choose the Best Option

Choosing the right insurance in Naples means comparing options that actually fit your life, not settling for whatever sounds familiar. We at Responsive Insurance, Inc. know that Florida insurer comparisons can feel overwhelming when you’re juggling coverage types, costs, and local risks all at once.

This guide walks you through exactly what to evaluate so you can make a decision with confidence.

What Coverage Do You Actually Need in Naples

Start by listing what you own and what could hurt you financially. For homeowners, this means your house, contents, and liability if someone gets injured on your property. If you have a mortgage, your lender requires homeowners insurance, and if you’re in a flood zone, flood insurance is mandatory. Naples homeowners pay about $2,502 per year on average according to Policygenius data-9% higher than Florida’s state average and 43% above the national average. This high cost reflects real risk: Florida homeowners insurance has risen significantly over recent years due to hurricane losses and costly claims. For auto owners, Florida requires a minimum of $10,000 in personal injury protection and $10,000 in property damage liability. Many people stop there, but that’s a mistake-one serious accident can wipe out those limits fast. Business owners need to think bigger: general liability, commercial property coverage for buildings and equipment, commercial auto if you operate vehicles, and business owner policies that bundle multiple coverages. The key is matching coverage limits to what you’d actually owe if something goes wrong, not just checking boxes.

How Reconstruction Costs Drive Your Home Insurance Bill

Your dwelling coverage limit determines much of your premium. With $100,000 in coverage, you’ll pay around $851 annually in Naples; jump to $200,000 and it’s $1,726; at $400,000 it’s $3,336, according to Policygenius. This isn’t proportional-higher limits cost more per dollar because they reflect actual rebuild expenses in Southwest Florida. After a loss, underestimating reconstruction costs leaves you short, so get a contractor estimate for what it would cost to rebuild your home today, not what you paid for it years ago. Your deductible choice matters enormously: raising it from $500 to $1,000 can cut your annual Naples premium from about $3,271 to $2,046, saving roughly $1,000 yearly. That only works if you can actually afford that deductible out of pocket without hardship. For flood coverage, the National Flood Insurance Program caps building coverage at $250,000 for single-family homes, with a 30-day waiting period after purchase before protection kicks in-don’t wait for storm season to buy.

Local Risks That Standard Policies Often Miss

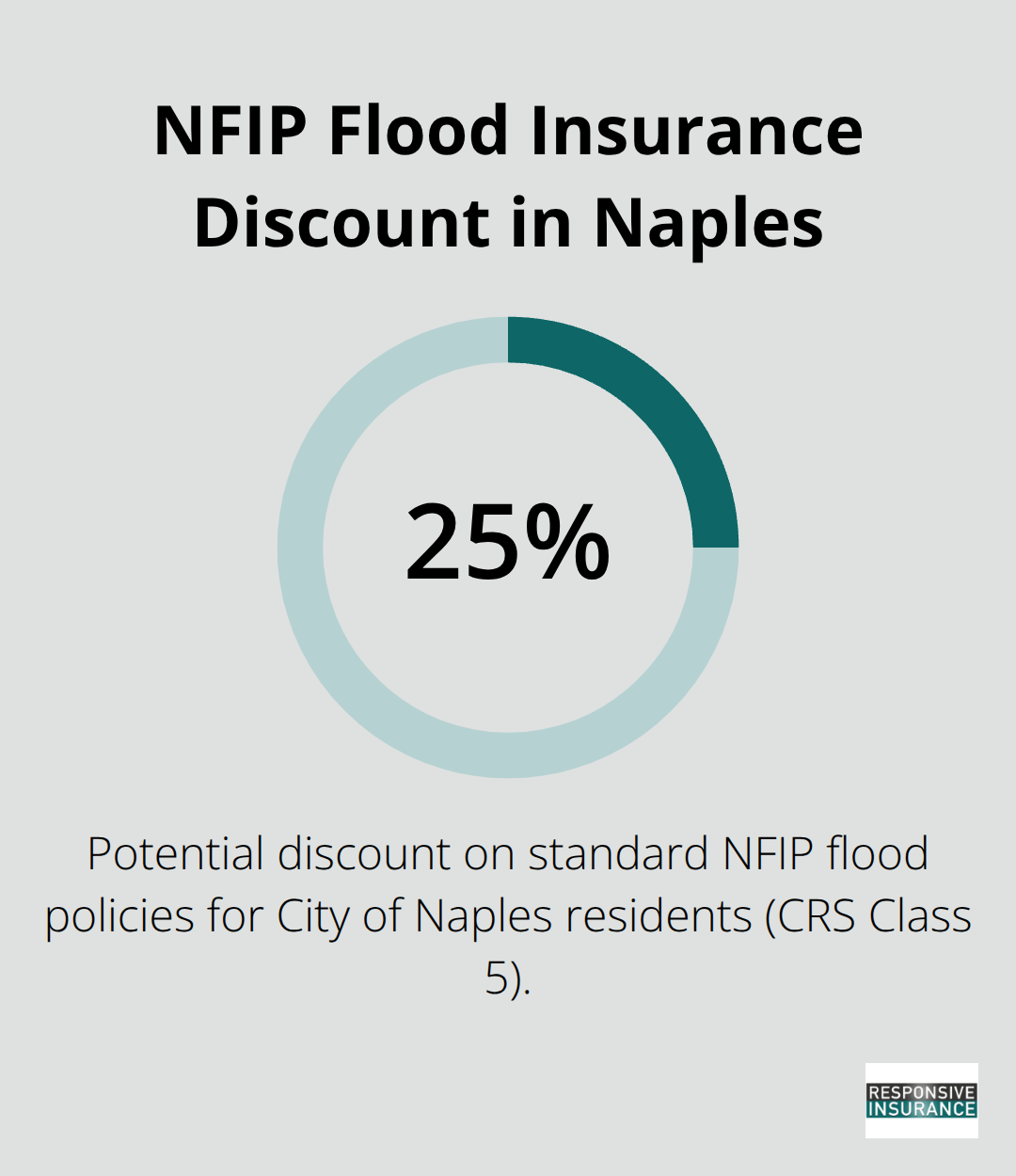

Most Naples homeowners policies exclude wind and hail damage, which means you need separate windstorm insurance or a dedicated wind policy to cover hurricane damage. Flooding is completely separate from standard homeowners insurance, so you must purchase it independently through either the National Flood Insurance Program or private flood insurers. The City of Naples participates in the NFIP and qualifies for Community Rating System Class 5 status, which yields up to a 25% discount on standard flood policies. Your ZIP code affects your rate significantly: 34109 averages about $2,434 per year while 34102 runs about $2,582 annually, according to Policygenius.

Contact the City of Naples Floodplain Coordinator at 239-213-5039 to confirm whether your property sits in a Special Flood Hazard Area, which determines both insurance requirements and your risk profile.

Comparing Carriers to Match Your Needs

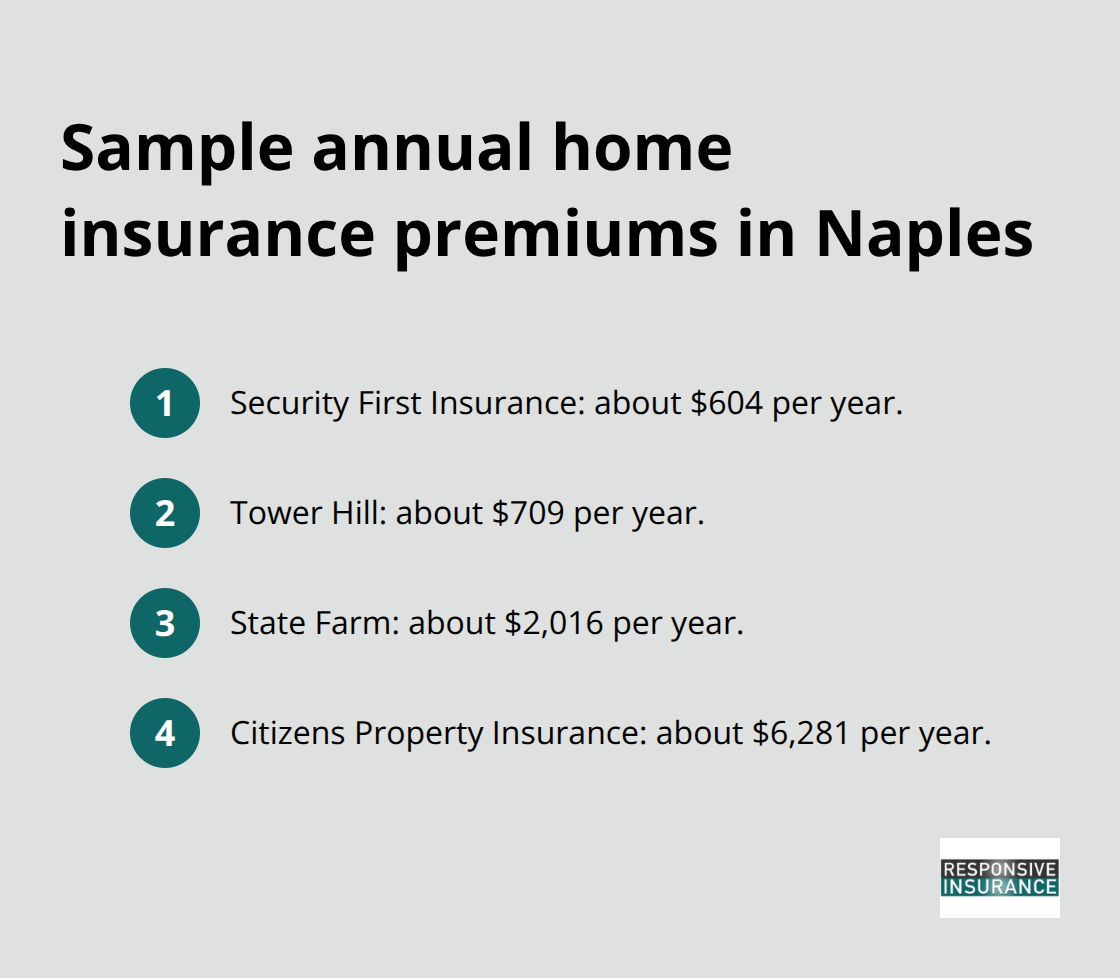

Once you know what coverage you need, you’ll want to see how different insurers price that protection. Rates vary dramatically by carrier: Security First Insurance costs about $604 per year in Naples, Tower Hill runs $709 annually, and State Farm averages $2,016, while Citizens Property Insurance reaches $6,281 per year according to Policygenius.

Your claims history, credit score, and home age all influence which carrier offers the best price for your situation. An older home (50 years or more) might find Security First at roughly $502 annually, whereas Citizens could charge $8,046 for the same property. If you’ve filed three claims in five years, Security First often remains the cheapest option at about $604 per year, with Citizens around $6,293. This variation means you can’t rely on one quote-you need multiple offers to find real savings.

What Makes One Insurer Better Than Another

Financial Strength Determines Claims Payment Reliability

Financial strength separates insurers that pay claims quickly from those that drag their feet or deny legitimate losses. Check AM Best or Demotech ratings before signing anything-these agencies grade insurers on their ability to pay out when disaster hits. State Farm carries an A++ rating from AM Best, Tower Hill holds a B rating, and Universal Property maintains an A rating according to Policygenius data. A lower rating doesn’t automatically mean you should avoid that carrier, but it does signal more risk that the company might struggle during a major hurricane season when thousands of claims flood in simultaneously. Beyond ratings, ask your prospective insurer directly: What’s your average claims processing time? Some carriers respond in days; others take weeks. For Naples homeowners dealing with water damage or wind loss, speed matters because you need repairs started before secondary damage spreads.

Coverage Customization Protects You From One-Size-Fits-All Gaps

Coverage customization separates insurers that force you into rigid policies from those willing to build protection around your actual situation. Universal Property, for example, offers private flood endorsements up to $5 million and covers older roofs up to 20 years old, according to Policygenius-valuable if you own an older Naples home. Tower Hill provides extensive flood-related add-ons and windstorm options that State Farm might not bundle the same way. This means the cheapest quote might exclude exactly the coverage you need most, leaving you underprotected at claim time. When you compare quotes, look beyond the price and verify that each option includes the specific protections your property requires.

Local Expertise Matters More Than National Brand Recognition

Customer service quality in a local market like Naples means having someone who understands Southwest Florida risks and can explain why your flood insurance waiting period matters or why your wind exclusion might be a problem. Gulf Coast Insurance, an independent Naples agency operating since 2000, represents over 50 carriers and maintains three Florida locations including Naples, enabling face-to-face conversations about your specific property and neighborhood. They emphasize education and no-pressure consultation, which matters because insurance decisions shouldn’t feel rushed. Responsive Insurance, Inc., an independent agency based in Naples, also works with multiple A-rated insurance companies to compare coverage and find the best fit for your needs, providing timely responses to client questions. Working with a local independent agency instead of a national call center gives you access to an agent who can spot coverage gaps you might miss and advocate for you during claims disputes.

How to Evaluate Service Quality Before You Buy

When you contact any insurer or agency, notice how they respond: Do they ask detailed questions about your home, business, or driving history? Do they explain why certain coverage matters, or do they just quote numbers? Do they follow up on promises, or do you chase them for answers? These patterns predict how they’ll treat you when you file a claim and need actual help. An insurer with poor local presence might offer the lowest quote, but if they can’t help you navigate a water damage claim or dispute a denial, that savings evaporates when you’re paying out of pocket for repairs. The next step involves gathering multiple quotes and comparing them side by side to identify which carriers offer the right combination of price, coverage, and service for your situation.

Getting Your Best Quote Without Wasting Time

Collecting quotes from multiple insurers is the only way to find what you actually owe in Naples, since rates vary wildly between carriers for identical coverage. Start with at least three to five different providers, including both national names and local independents. Contact State Farm, Tower Hill, Security First, and Universal Property directly or through their websites to request quotes, then reach out to a local independent agency like Gulf Coast Insurance to compare what those carriers offer against each other. Independent agencies matter here because they represent 50 or more carriers simultaneously, meaning one conversation with them produces multiple quotes instead of forcing you to call around for hours.

Provide Consistent Information Across All Quotes

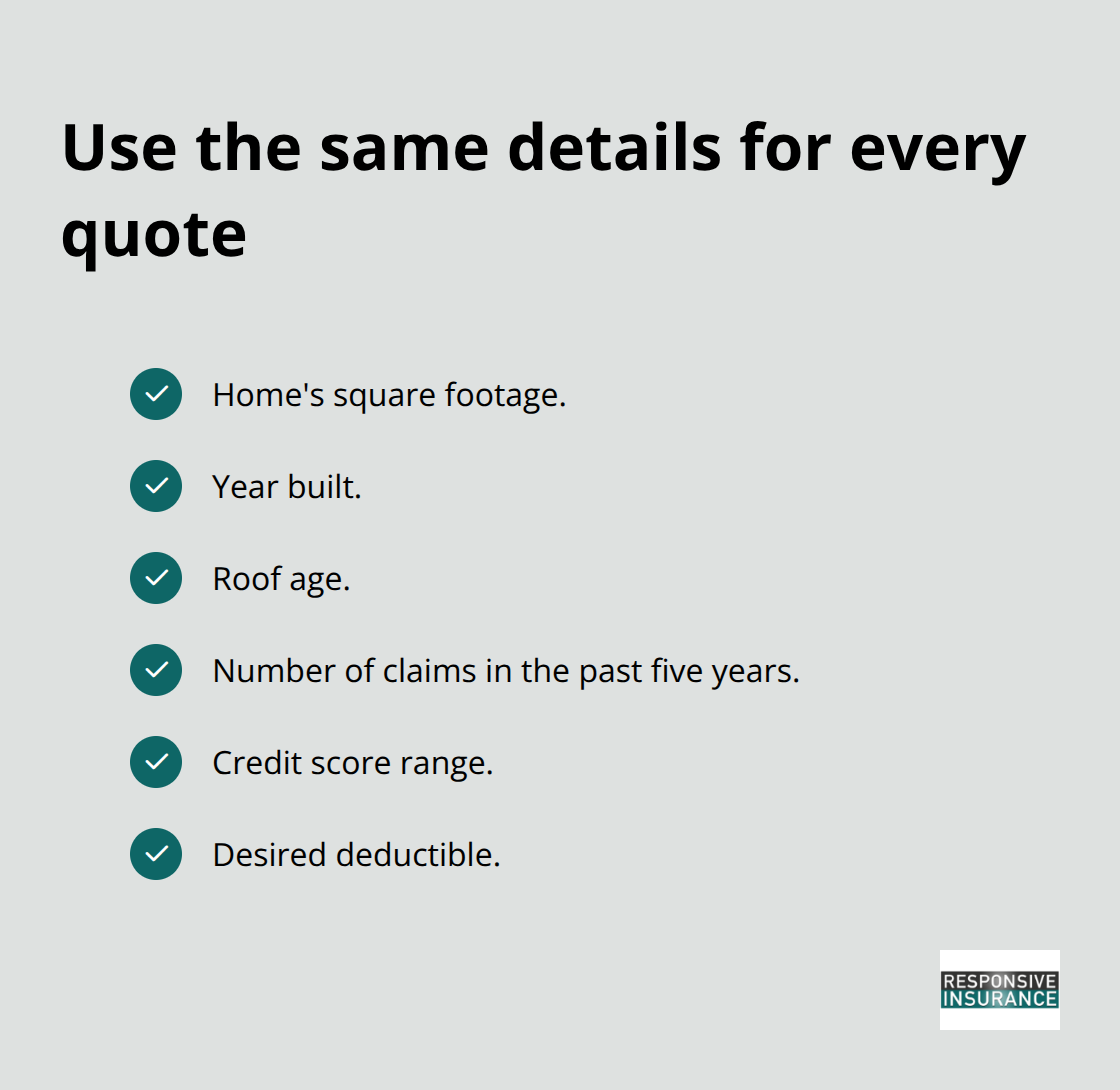

When you request a quote, provide identical information each time: your home’s square footage, year built, roof age, number of claims in the past five years, credit score range, and desired deductible. This consistency prevents you from comparing apples to oranges. Most online quote tools don’t bind coverage anyway, so getting preliminary numbers without a phone call saves time upfront.

However, any actual policy requires confirmation from a licensed agent to verify information and comply with state requirements.

Look Beyond the Lowest Price

Don’t fall for the lowest price immediately, because Security First Insurance at $604 per year might exclude wind coverage that Tower Hill includes at $709, or Universal Property’s $3,202 annual cost might include private flood coverage up to $5 million while State Farm’s $2,016 quote doesn’t. The difference between a cheap policy with dangerous gaps and a slightly pricier policy with real protection becomes painfully obvious when water enters your home or a storm damages your roof.

Create a Side-by-Side Comparison

Once you have three to five quotes in hand, create a simple spreadsheet listing each carrier’s name, total premium, deductible, dwelling coverage limit, flood coverage details, wind exclusions, and any discounts applied. This visual comparison stops you from relying on memory and reveals which carrier actually gives you the most protection for your money rather than just the lowest number. Verify that each quote reflects the same dwelling coverage amount, because a $2,000 difference might vanish if one insurer quoted $250,000 coverage while another quoted $400,000.

Verify Financial Strength and Ask Specific Questions

Check the AM Best or Demotech financial ratings for each carrier before narrowing your choices, since ratings range from “A++” (Superior) to “S” (Suspended), with “B+” or better indicating a financially secure carrier. Call your top two choices and ask three specific questions: What’s your average claims processing time for water damage, what discounts apply if you bundle auto and home coverage, and what happens if you increase your deductible further? A carrier offering a 10-day processing window beats one taking 30 days when you’re without power and water is still dripping through your ceiling. Verify that the agent actually answered your questions instead of redirecting you to a website, because that behavior predicts how responsive they’ll be during a claim.

Check Licensing and Read Customer Reviews

Finally, check that your chosen insurer holds a valid Florida license through the Florida Department of Financial Services website, and read recent customer reviews on independent sites like the National Association of Insurance Commissioners to spot patterns of claim denials or service failures (this step takes 30 minutes but prevents selecting an insurer with a documented history of fighting legitimate claims).

Final Thoughts

Comparing Florida insurers in Naples requires you to match coverage to what you actually own, verify that your chosen carrier pays claims quickly when disaster strikes, and select an agency that understands Southwest Florida risks well enough to spot gaps you might miss. The lowest quote rarely wins because it often excludes exactly the protection you need most, leaving you exposed when water damage or wind loss hits. Financial strength ratings, coverage customization options, and local expertise separate insurers that fight for you from those that fight against you during claims.

Working with a local independent agency changes the equation entirely. Instead of calling five different carriers and comparing quotes manually, you contact one agency representing 50 or more A-rated insurers simultaneously (saving hours of your time). That agent knows Naples neighborhoods, understands which carriers handle flood claims fastest, and can bundle your auto, home, and flood coverage for discounts a national call center would never offer. They advocate for you during disputes because their reputation depends on client satisfaction, not on denying claims to boost profit margins.

Your next step is straightforward: gather quotes from at least three carriers, create a side-by-side comparison showing premiums and coverage details, verify financial ratings, and contact your top choices with specific questions about claims processing time and available discounts. Then reach out to Responsive Insurance, Inc. to handle your Florida insurer comparisons in Naples with an independent agency that works with multiple A-rated insurance companies to compare coverage and find the best fit for your needs. The right coverage protects your financial security; the right agency makes sure you actually get paid when you need it most.