Commercial Auto Insurance Florida: Protect Your Fleet With Confidence

Running a fleet in Florida means managing real risks on real roads. Commercial auto insurance in Florida isn’t optional-it’s a legal requirement that protects your business from liability claims, accidents, and financial disaster.

At Responsive Insurance, Inc., we help Florida business owners find policies that match their actual fleet needs. This guide walks you through what coverage matters, why it’s required, and how to get the right protection without overpaying.

What Commercial Auto Insurance Actually Covers

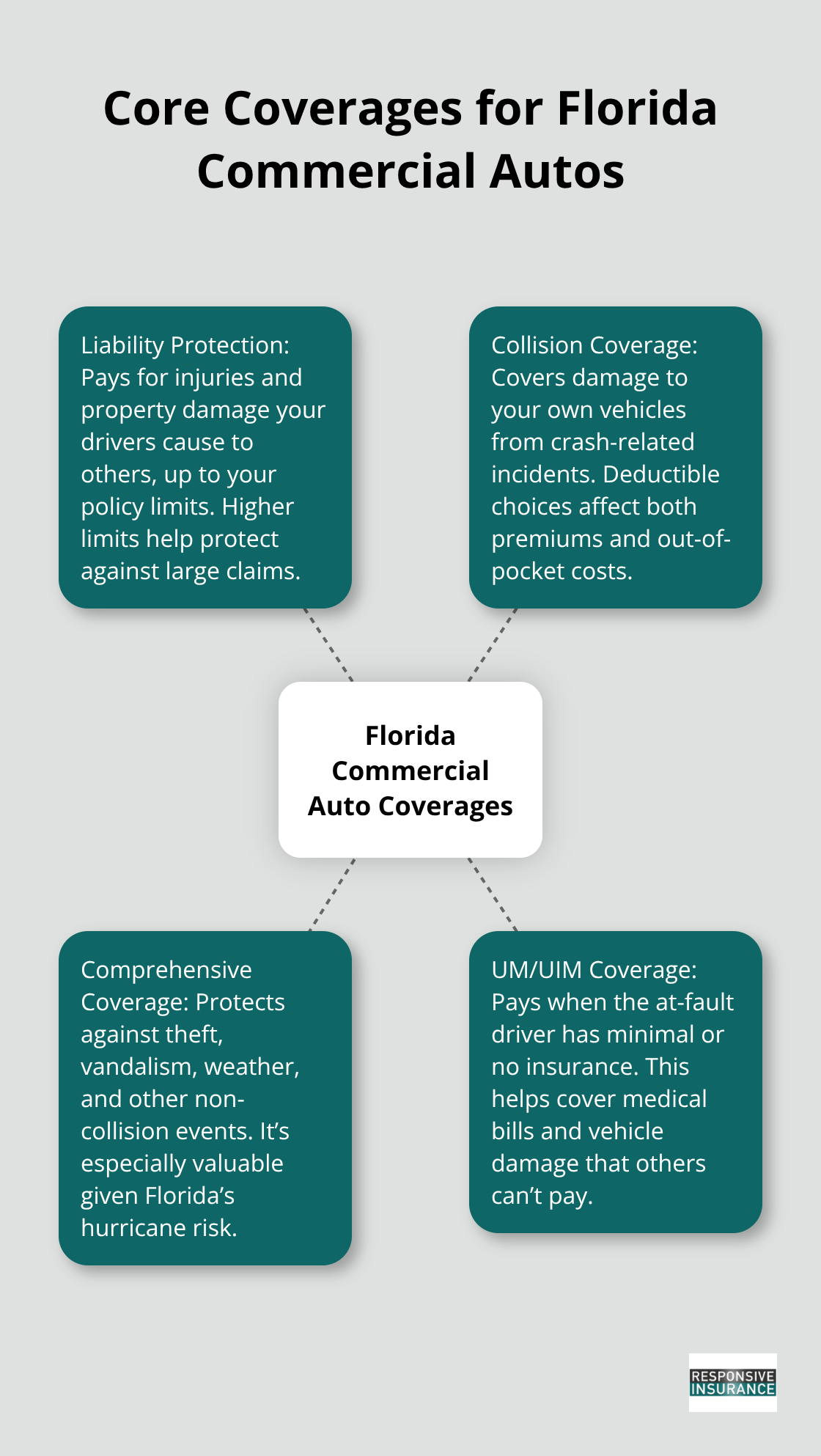

Liability Protection: The Foundation of Your Coverage

Florida commercial auto policies protect three critical areas that personal auto insurance ignores. Liability coverage pays for injuries or property damage your drivers cause to other people and their vehicles, up to your policy limits. Florida requires a minimum of $10,000 in property damage liability, though we at Responsive Insurance, Inc. strongly recommend higher limits-typically $25,000 to $100,000 depending on your fleet size and industry. This isn’t theoretical. If your delivery driver hits someone’s car and causes $50,000 in damages plus medical bills, that $10,000 minimum leaves your business responsible for the remaining $40,000 out of pocket.

Physical Damage Coverage for Your Vehicles

Collision coverage handles damage to your own vehicles from accidents, while comprehensive coverage protects against theft, vandalism, weather, and other non-collision events. Florida’s hurricane season and high theft rates in urban areas like Naples make comprehensive coverage more than optional-it’s practical protection. Uninsured and underinsured motorist coverage (UM/UIM) pays your claims when the at-fault driver lacks adequate insurance. This matters significantly in Florida, where accident investigations often reveal drivers with minimal or no coverage. According to the Insurance Information Institute, roughly one in eight drivers nationwide operates uninsured, and Florida’s numbers reflect similar exposure.

Coverage Gaps You Must Address Separately

Your fleet faces specific risks that standard coverage doesn’t address. If your drivers regularly carry business property in vehicles (equipment, inventory, or client materials), standard commercial auto policies exclude cargo contents. You need separate commercial property or cargo coverage for those assets. Medical expenses for your injured drivers fall under workers’ compensation, not auto liability, so confirm your workers’ comp policy covers vehicle-related injuries.

Tailoring Coverage to Your Industry and Operations

When selecting limits, consider your industry. Construction companies hauling expensive equipment need higher collision and comprehensive limits than service businesses. Delivery operations in high-density areas face greater accident frequency than those on rural routes. Getting this right prevents the painful discovery after a claim that your coverage was insufficient for your actual exposure. The next step involves understanding why Florida law mandates this protection and what financial risks your business faces without adequate coverage in place.

Why Your Business Needs Commercial Auto Insurance in Florida

Legal Requirements Protect Everyone on Florida Roads

Florida law mandates commercial auto insurance for any vehicle used in business operations. The Florida Department of Highway Safety and Motor Vehicles requires minimum coverage of $10,000 in personal injury protection and $10,000 in property damage liability for commercial vehicles, but these minimums fall far short of actual business protection needs. A single accident involving your delivery van or service truck can generate medical bills exceeding $100,000, vehicle damage of $50,000 or more, and lost income claims that stretch for months. Without commercial auto insurance, your business absorbs these costs directly, which often means depleting operating capital, taking on debt, or facing bankruptcy. Operating without coverage violates Florida statute, exposing your business to fines, license suspension, and personal liability lawsuits against you as the owner.

Real Financial Exposure From Single Accidents

The financial protection extends beyond single-vehicle accidents. Florida’s no-fault auto insurance system means your own PIP coverage applies first when your drivers suffer injuries, but commercial vehicle crashes involve multiple policies and complex liability questions that personal coverage cannot address. If your driver causes an accident that injures multiple people or damages multiple vehicles, your liability exposure multiplies quickly. The Insurance Information Institute reports that roughly one in eight drivers nationwide operate uninsured, and uninsured and underinsured motorist coverage becomes critical when the at-fault driver lacks sufficient insurance. Your business faces substantial out-of-pocket costs without proper UM/UIM protection in place.

Fleet Size and Driver Roster Complexity

Managing multiple vehicles and drivers across a fleet amplifies these risks exponentially. Each additional driver increases accident frequency exposure, and each additional vehicle increases the likelihood of theft, weather damage, or collision claims. Proper commercial auto policies allow you to list all active drivers, ensuring coverage applies regardless of which team member operates which vehicle. Leaving drivers off your policy or operating with outdated rosters creates claim denial situations that leave your business unprotected precisely when protection matters most. This reality makes selecting the right policy limits and coverage options essential for your fleet’s actual operations.

Selecting the Right Coverage for Your Fleet’s Actual Needs

Map Your Fleet’s Real Operational Profile

Start with your fleet’s actual composition and operational reality, not industry assumptions. A Naples delivery company running five vans through downtown traffic faces different risks than a service business with two trucks operating primarily on highways. Document your vehicle types, weights, annual mileage, primary service areas, and driver count. Florida commercial auto premiums range from $157 per month for a sedan to $1,013 per month for a limousine, reflecting real differences in exposure. A construction company hauling heavy equipment pays substantially more than a cleaning service with light vans because cargo weight, vehicle value, and accident frequency differ dramatically.

Calculate Your Realistic Liability Exposure

Determine your liability exposure through realistic damage scenarios. If your driver causes an accident injuring three people with combined medical costs of $150,000, your $10,000 minimum liability limit leaves your business responsible for $140,000 out of pocket. We at Responsive Insurance, Inc. recommend liability limits of $100,000 per person and $300,000 per accident as a practical baseline for most Florida fleets, with higher limits for industries handling hazardous materials or serving high-income clientele.

Choose Deductibles That Match Your Financial Position

Collision and comprehensive coverage deductibles deserve careful attention. A $1,000 deductible costs less monthly but means you absorb $1,000 of every claim. A $500 deductible increases your premium but reduces out-of-pocket costs when accidents happen. For fleets with strong safety records and adequate cash reserves, higher deductibles make financial sense. For businesses operating on tight margins, lower deductibles provide better cash flow protection.

Obtain Competitive Quotes From Multiple Insurers

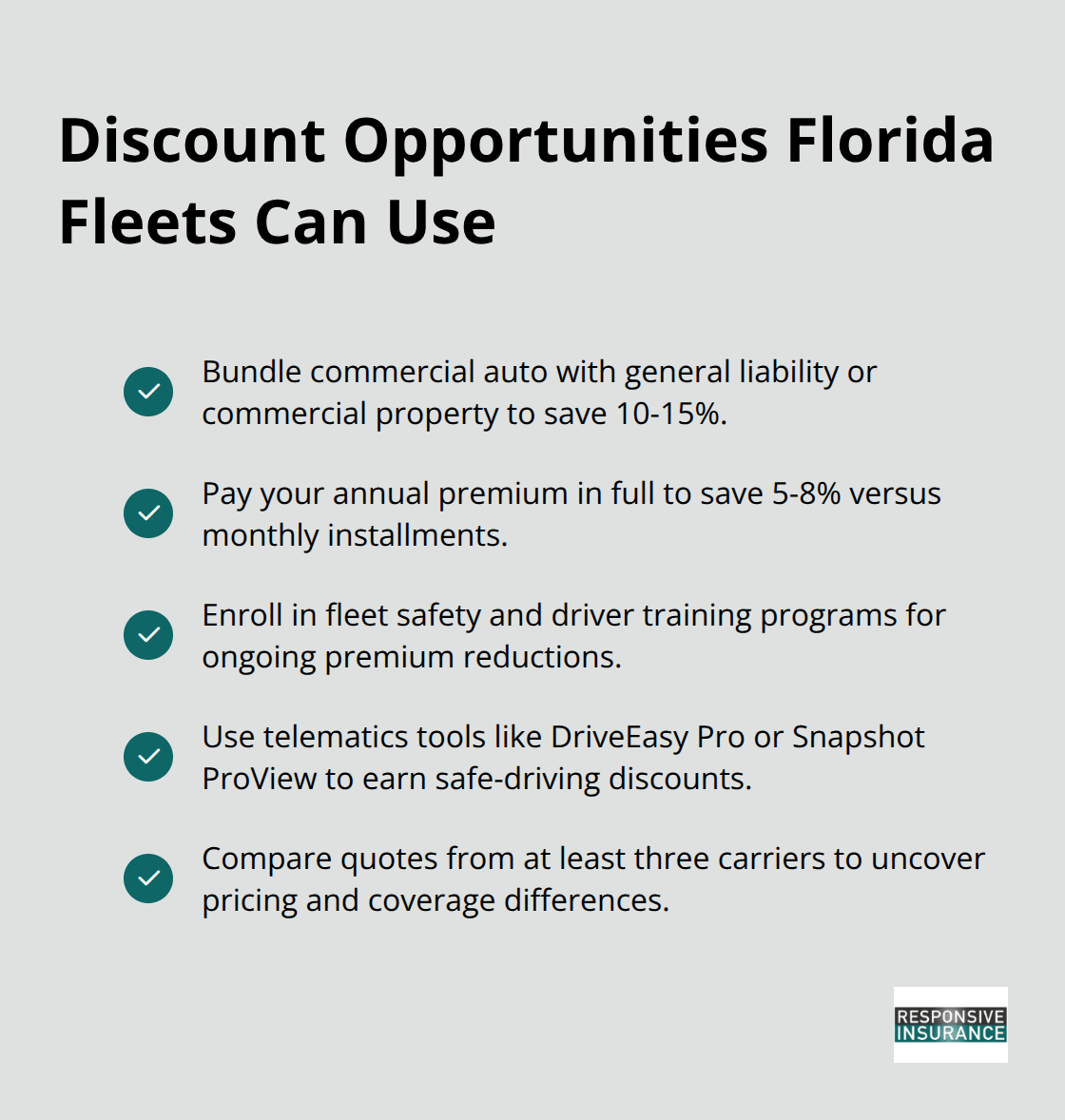

Your next critical step involves obtaining competitive quotes from multiple insurers rather than accepting the first offer. GEICO, Liberty Mutual, and Progressive all serve Florida commercial fleets with different strengths according to Insurify research. GEICO emphasizes telematics tools like DriveEasy Pro that monitor driver behavior and can reduce premiums by 10-15% for safe driving practices. Liberty Mutual offers customized coverage for specific business types with risk-control guidance that helps prevent claims before they occur. Progressive markets itself as the leading U.S. commercial auto insurer per AM Best ratings and provides fleet-focused tools through Snapshot ProView. Comparing quotes from at least three carriers reveals genuine pricing differences and coverage variations. One insurer might offer better hired and non-owned auto coverage for situations where your employees use personal vehicles for business, while another provides superior uninsured motorist limits. An independent agent can access multiple A-rated insurers simultaneously and identify which carrier offers the best combination of rates and coverage for your specific fleet profile. This approach eliminates the need to contact carriers individually and ensures you compare apples to apples across policies.

Identify Discounts That Apply to Your Operation

Ask each quote about available discounts that actually apply to your operation. Multi-product bundling, paying annual premiums upfront instead of monthly, and fleet safety programs can reduce costs meaningfully. Some insurers offer 10-15% reductions for bundling commercial auto with general liability or commercial property coverage.

Paying in full typically saves 5-8% compared to monthly installments. Fleet safety programs reward accident-free records and driver training participation with ongoing premium reductions, making them valuable for businesses serious about risk management.

Final Thoughts

Commercial auto insurance in Florida protects your fleet from financial devastation, legal penalties, and operational disruption that a single accident can trigger. The coverage you select determines whether a claim becomes manageable or transforms into a business-threatening crisis, and liability protection combined with collision, comprehensive, and uninsured motorist coverage addresses the real risks your drivers face on Florida roads. Without adequate limits tailored to your fleet’s actual operations, you expose your business to out-of-pocket costs that can exceed six figures and threaten your company’s survival.

Getting the right policy requires honest assessment of your fleet composition, realistic calculation of liability exposure, and competitive shopping across multiple insurers who serve your industry. Your deductible choices, coverage limits, and optional add-ons should reflect your business’s financial position and risk tolerance rather than industry defaults, and discounts for bundling, safety programs, and upfront payment can reduce your annual costs by 15-25% when you compare quotes carefully. This effort to shop competitively pays dividends through lower premiums and better coverage alignment with your actual needs.

We at Responsive Insurance, Inc. work with multiple A-rated insurance companies to find commercial auto insurance Florida policies that match your specific needs without unnecessary overpayment. Contact Responsive Insurance, Inc. today to discuss your fleet’s protection needs and obtain competitive quotes from carriers that serve Southwest Florida businesses.