Naples Flood Risk Assessment: How Your Home Stacks Up

Naples sits in one of Florida’s most flood-prone regions, with hurricane season and rising water tables creating real risks for homeowners. A Naples flood risk assessment isn’t just paperwork-it’s the foundation for protecting your property and your finances.

At Responsive Insurance, Inc., we help homeowners understand exactly where their homes stand and what coverage gaps exist. This guide walks you through flood zones, vulnerability factors, and the insurance solutions that actually work for Southwest Florida properties.

What Do Naples Flood Zone Maps Actually Tell You

FEMA’s 2024 Maps and What Each Zone Means

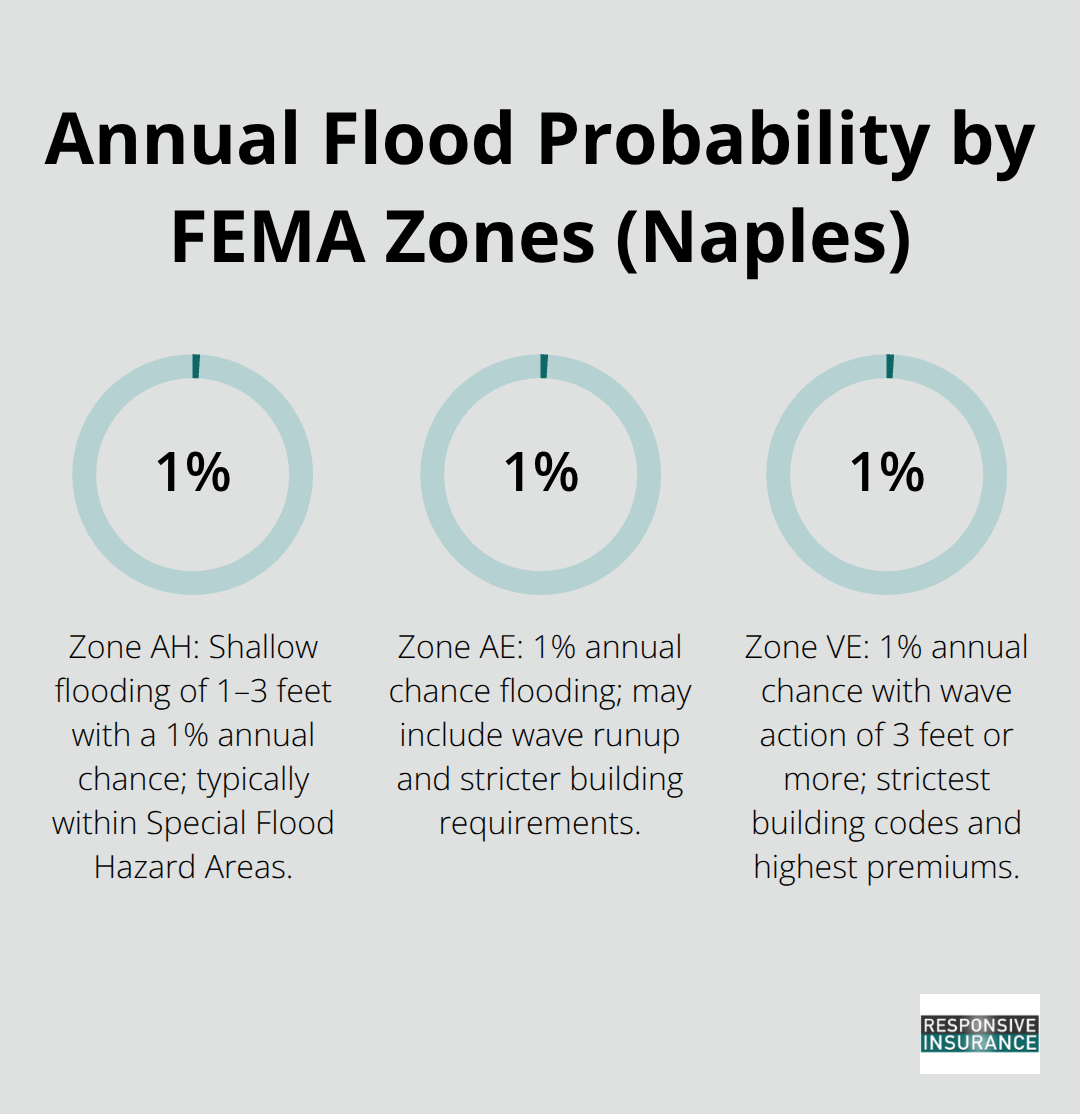

FEMA updated its Flood Insurance Rate Maps for Naples in 2024, replacing the 2012 versions with updated and more detailed information that directly affects your insurance rates and building requirements. The new maps classify properties into specific zones based on flood probability. Zone AH indicates shallow flooding with 1–3 feet of water and a 1% annual chance of occurring, while Zone AE covers similar 1% annual chance floods but may include wave runup.

Zone VE represents coastal high-hazard areas with 1% annual chance flooding and wave action of 3 feet or greater-these zones trigger the strictest building codes and highest insurance costs. Zone X (shaded) shows a 0.2% annual chance flood, and unshaded Zone X falls outside the mapped flood hazard entirely.

Each zone comes with a Base Flood Elevation, or BFE, which determines whether your home’s lowest finished floor meets minimum elevation standards. If your property sits below the BFE in a Special Flood Hazard Area, flood insurance becomes mandatory if you carry a federally backed mortgage. The City of Naples provides an interactive web tool where you can enter your address and instantly see your flood zone, but official confirmation should come from the Floodplain Coordinator at rdorta@naplesgov.com or 239-213-5039.

Multiple Water Sources Create Layered Risk

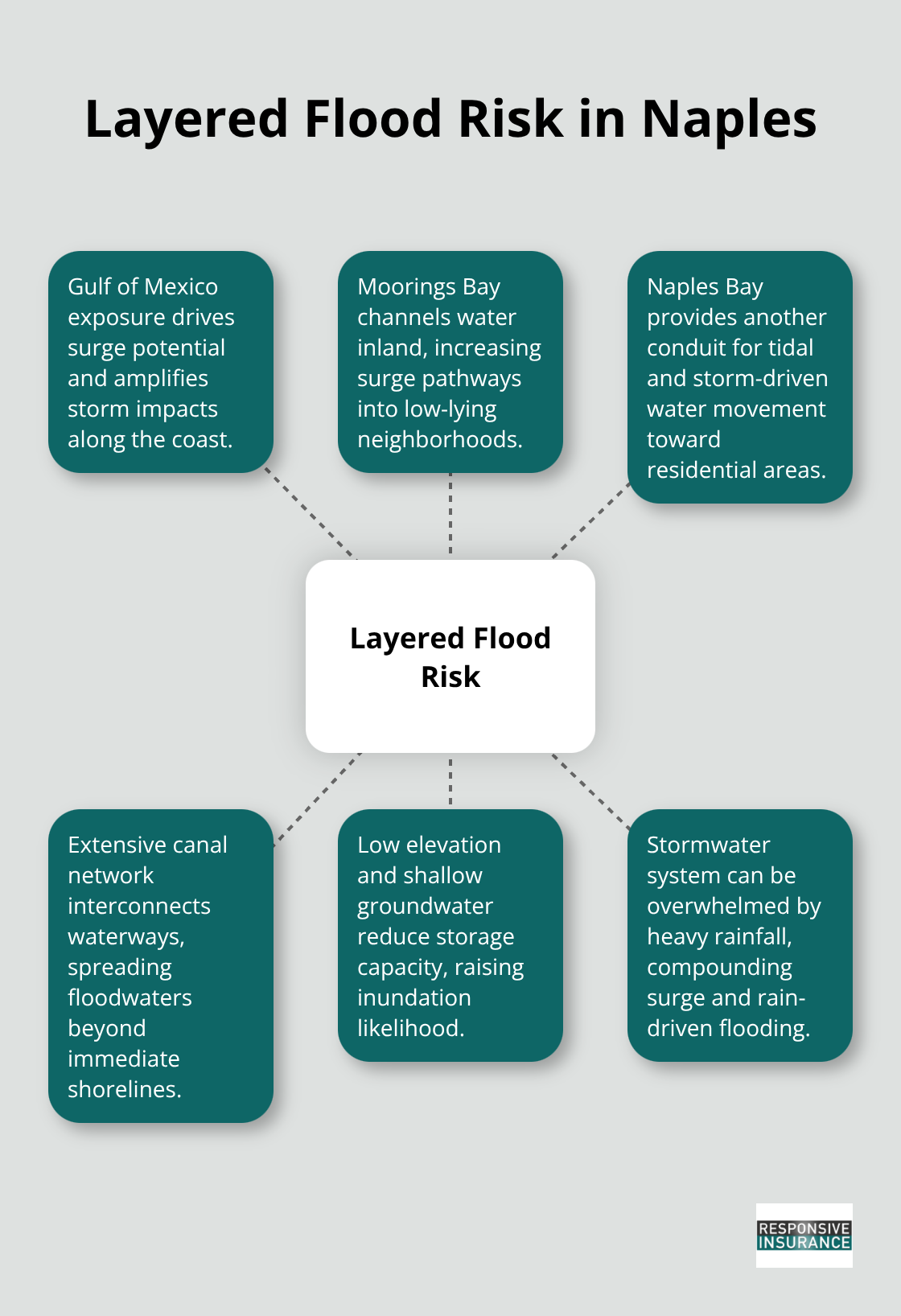

Naples faces concentrated flood risk from multiple sources that generic flood maps cannot fully capture. The city sits exposed to the Gulf of Mexico, plus it has Moorings Bay, Naples Bay, and an extensive canal network-all combining with low elevation and shallow groundwater to create layered vulnerability. Storm surge during hurricanes pushes saltwater inland through these waterways, while heavy rainfall events overwhelm the stormwater system in low-lying neighborhoods.

Drainage and elevation are the two factors that separate high-risk from moderate-risk properties in Southwest Florida. Properties with poor drainage or those built below the natural grade face substantially higher flood costs and recovery challenges. Location matters intensely-two houses on the same street can face vastly different flood exposure based on elevation, proximity to drainage corridors, and distance from bay or gulf water.

Map Updates and Future Refinements

The 2024 Collier County Coastal Flood Map reflects these realities with updated hazard data, and the county plans Future Physical Map updates for August through October 2026 that will refine flood zones further. What this means for your home is that your flood zone classification may shift as new data arrives. We at Responsive Insurance, Inc. recommend checking whether your property qualifies for a Letter of Map Amendment, which can remove your home from the flood zone if your elevation meets or exceeds the BFE. Processing a LOMA typically takes about 60 days after FEMA review, and it can eliminate the mandatory flood insurance requirement and lower your overall insurance costs significantly. Understanding your current zone is the first step-but verifying whether that zone actually applies to your specific property elevation comes next.

How to Verify Your Flood Risk Before It’s Too Late

Check Your Flood Zone Status First

Start with the City of Naples interactive flood map tool-enter your address and you’ll see which zone FEMA assigned to your property. This initial check takes two minutes and gives you a baseline understanding of your flood exposure. However, that zone designation may not be final. Your home’s actual flood risk depends on your property’s elevation relative to the Base Flood Elevation, or BFE. Two houses in the same zone can face completely different insurance requirements and costs based on whether their lowest finished floor sits above or below the BFE.

Get an Elevation Certificate to Unlock Savings

This is where most Naples homeowners miss a critical opportunity. If your elevation meets or exceeds the BFE, you may qualify for a Letter of Map Amendment that removes your property from the flood zone entirely. A Florida-licensed engineer, architect, or surveyor will prepare an Elevation Certificate for $300 to $600, but it can save you thousands in mandatory flood insurance premiums over time. Contact the Floodplain Coordinator at rdorta@naplesgov.com or 239-213-5039 to discuss whether a LOMA makes sense for your property. The review process takes roughly 60 days after FEMA receives your application, and if approved, your flood insurance requirement vanishes.

Neighborhood Characteristics Drive Real Risk

Your Naples neighborhood’s specific characteristics matter far more than the zone label alone. Properties in low-lying areas near Moorings Bay, Naples Bay, or the extensive canal network face flood damage that extends beyond the mapped zones during heavy rain or storm surge events. Homes with poor drainage or those sitting below the natural grade experience water intrusion during normal high tides, not just during hurricanes. Standard homeowners insurance covers absolutely nothing related to flooding-no water damage from rain, no storm surge damage, no cleanup costs.

Coverage Limits and Timing Create Hidden Gaps

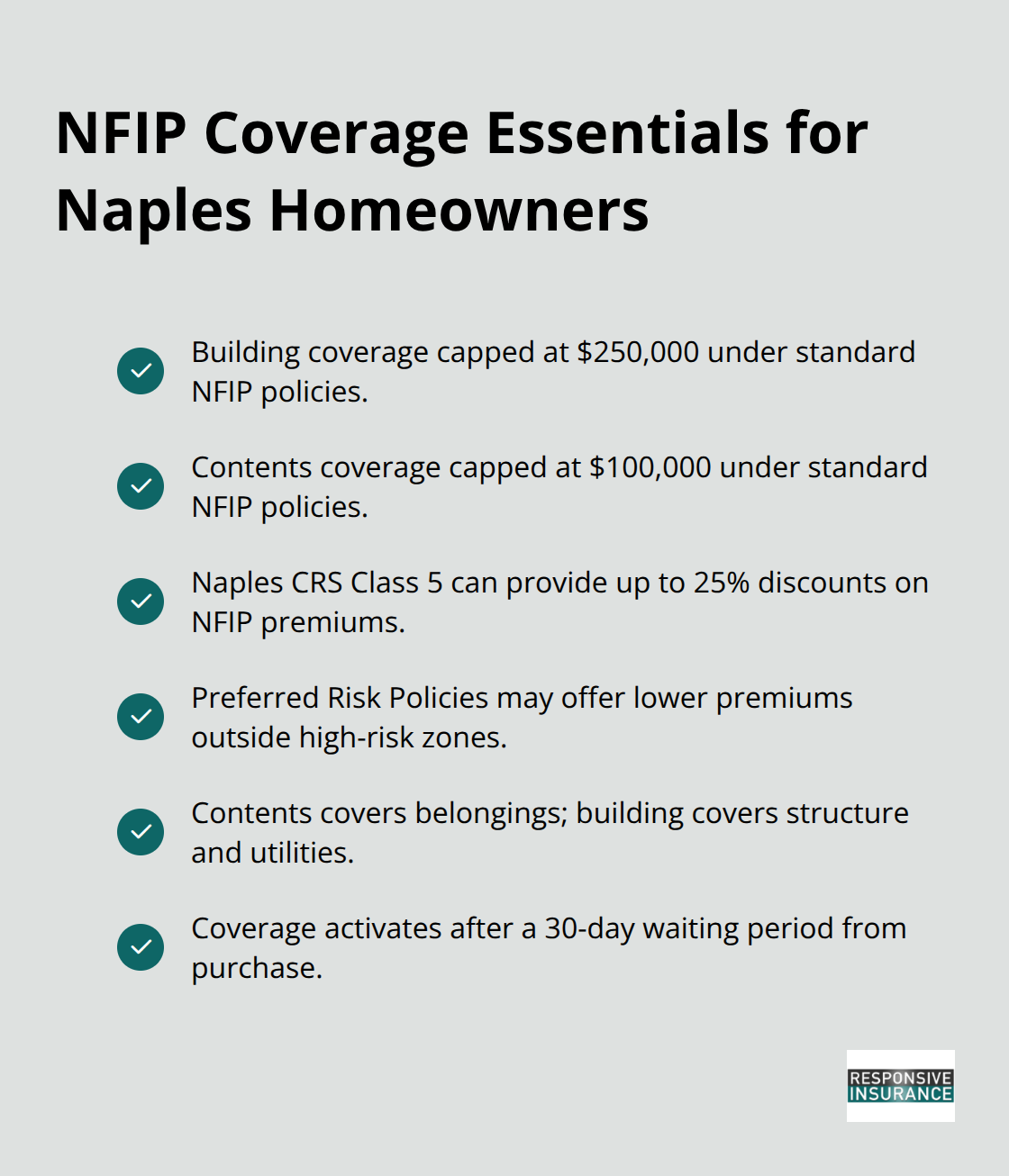

The National Flood Insurance Program caps residential building coverage at $250,000 and contents at $100,000, which sounds adequate until you experience actual flood damage. Typical flood damages easily exceed $25,000 per event, and catastrophic storms can total properties completely. Naples qualifies for Community Rating System Class 5, which means residents can access flood insurance discounts of up to 25% on standard NFIP premiums compared to other Florida communities. Preferred Risk Policies offer even lower premiums for properties outside high-risk zones.

Act Before Hurricane Season Arrives

The critical timing issue is the 30-day waiting period between policy purchase and coverage activation. Purchasing flood insurance in June when hurricane season peaks means you won’t have coverage until July. You should purchase coverage well before storm season arrives and review your policy limits annually as property values increase. Once you understand your flood zone status and elevation, the next step involves selecting the right insurance solution for your specific property and risk profile.

Choosing the Right Flood Insurance for Your Naples Home

NFIP Coverage: The Foundation for Most Naples Homeowners

The National Flood Insurance Program remains the foundation of flood protection for most Naples homeowners, particularly those in Special Flood Hazard Areas where it becomes mandatory for mortgaged properties. NFIP policies cap residential building coverage at $250,000 and contents at $100,000 through standard policies, though Preferred Risk Policies offer substantially lower premiums for properties outside high-risk zones. Naples qualifies as a Community Rating System Class 5 community, meaning residents access up to 25% discounts on NFIP premiums compared to other Florida areas. Contents coverage protects furniture, electronics, clothing, and jewelry, while building coverage addresses structural damage to walls, ceilings, floors, and utilities. Added coverages for additional living expenses during displacement-covering rent, hotel stays, and meals-exist but require explicit selection when purchasing.

Timing and Premium Comparisons Matter

The waiting period works against procrastination: coverage doesn’t activate until 30 days after purchase, so purchasing in September when a storm approaches leaves your home unprotected until October. FloodSmart.gov lets you compare standard and preferred risk options for your specific address before committing to a policy. This comparison takes minutes and reveals whether Preferred Risk qualifies for your property based on elevation and flood zone designation.

Private Flood Insurance as an Alternative

Private flood insurance has emerged as a legitimate alternative for homeowners seeking higher limits or lower premiums than NFIP offers. These carriers operate independently of the federal program and can offer building limits exceeding $250,000, which matters significantly for high-value Naples properties where reconstruction costs dwarf federal caps. Private policies sometimes include coverage options NFIP excludes, such as replacement cost for contents rather than actual cash value. However, private flood insurance requires careful vetting-verify that carriers hold A ratings from agencies like AM Best and maintain proper licensing in Florida before switching from NFIP.

Evaluating Your Property’s Specific Needs

The decision between NFIP and private coverage depends entirely on your property’s elevation, location within Naples, and replacement cost. A home in Zone X with elevation well above the BFE might qualify for NFIP Preferred Risk at minimal cost, while a high-value property in Zone VE might benefit from private coverage’s higher limits. Start by confirming your flood zone status and elevation, then request quotes from both NFIP and private carriers to see which option protects your investment most cost-effectively.

Final Thoughts

Your Naples flood risk assessment reveals whether your home faces genuine exposure or sits in a safer zone, but that knowledge demands action. Verify your flood zone through the City of Naples interactive map, then contact the Floodplain Coordinator to discuss whether an Elevation Certificate and Letter of Map Amendment could remove your property from the flood zone entirely. If your home sits in a Special Flood Hazard Area, obtain quotes for both NFIP standard and Preferred Risk policies, then compare those against private flood insurance options if your property value justifies higher coverage limits.

The 30-day waiting period means you cannot postpone coverage until August when hurricane season peaks. Most Naples homeowners either lack flood insurance entirely or carry limits that fall short of actual reconstruction costs, leaving a dangerous gap between perceived and actual protection. That gap is where financial disaster happens when water damage strikes.

We at Responsive Insurance, Inc. work with multiple A-rated insurance companies to compare flood coverage options and find solutions that actually protect your Naples property. Contact Responsive Insurance, Inc. to discuss your flood risk assessment results and receive personalized guidance on the coverage that fits your home and budget.