Protecting Your Investment: Short Term Rental Insurance Florida

Short-term rental properties in Florida generate significant income, but they expose you to risks that standard homeowners insurance won’t cover. Guest injuries, property damage, and lost rental income can quickly drain your profits without the right protection.

We at Responsive Insurance, Inc. help Naples property owners secure short term rental insurance Florida that actually covers what matters. This guide walks you through the coverage types you need and the gaps you must address.

Understanding Short-Term Rental Insurance in Florida

What Short-Term Rental Insurance Actually Covers

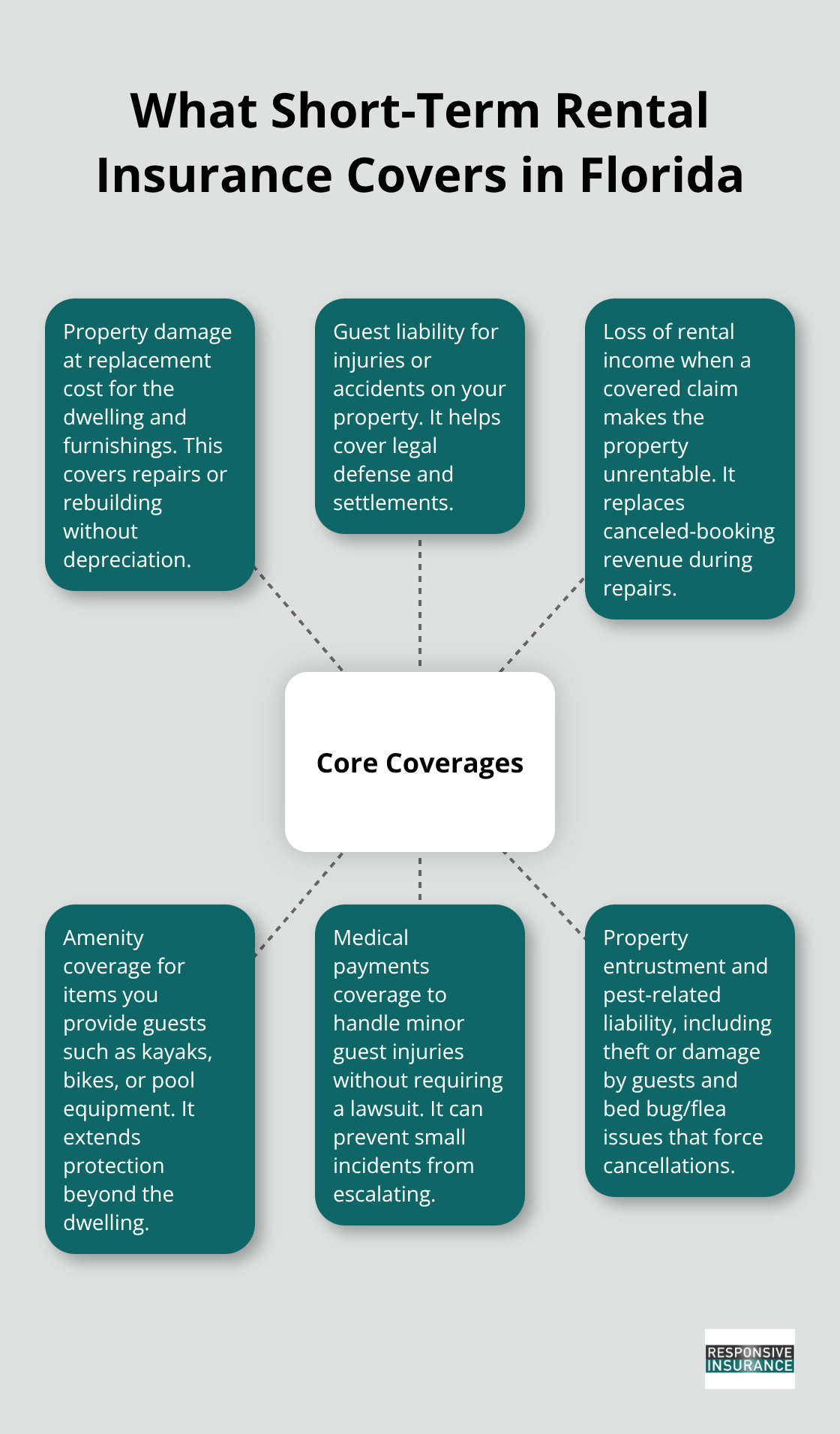

Short-term rental insurance replaces your standard homeowners policy with coverage specifically designed for guest-facing properties. Unlike homeowners insurance, which treats your home as a personal residence, short-term rental policies recognize that you operate a business with higher exposure. These policies cover property damage to your dwelling and furnishings at replacement cost, liability claims from guest injuries or accidents on your property, and loss of rental income if a covered claim makes your property unrentable. Some policies extend coverage to amenities you provide guests, such as kayaks, bikes, or pool equipment. Medical payments coverage helps cover minor guest injuries without requiring a lawsuit. You also receive protection against property entrustment losses, meaning theft or damage caused by guests to items left in their care. Bed bug and flea liability coverage addresses infestations that force you to cancel bookings and lose revenue.

If you operate in Collier County and comply with registration requirements under Ordinance 2021-45, your policy reflects that lower-risk profile.

Why Your Homeowners Policy Won’t Work

Standard homeowners insurance explicitly excludes business use and guest-related damages. If you rent your property to guests for stays under 30 days, your homeowners policy will deny claims related to that rental activity. Insurance companies view short-term rentals as commercial operations with significantly higher turnover and liability exposure than a primary residence. Guest injuries, property damage from frequent occupants, and lost income from cancellations fall outside homeowners coverage. Landlord policies designed for long-term rentals fail to work either because they require the property to be non-owner-occupied, making them unsuitable for vacation rentals where you might stay occasionally. Platform protections from Airbnb or VRBO provide only minimal coverage with substantial exclusions and low limits. Airbnb’s AirCover does not substitute for dedicated coverage and leaves critical gaps in liability and property protection. You need a policy built specifically for your rental model.

Florida’s Registration and Compliance Requirements

In unincorporated Collier County, short-term rental registration became mandatory on January 3, 2022 under Ordinance 2021-45. You must register with the county if you rent to guests for periods of less than 30 consecutive days more than three times per year. Properties inside the City of Naples, City of Marco Island, and Everglades City follow different rules, so verify your location before proceeding. The county requires a designated responsible party available 24/7 by phone and onsite within 24 hours of a violation or emergency. You must also obtain a Florida DBPR license to operate legally. All Florida short-term rentals must collect and remit state sales tax and the Collier County tourist development tax. Your insurance provider needs to know you comply with these requirements because non-compliance creates uninsurable risk and can void coverage. Contact Collier County Government at 239-252-8999 or access the GMD Public Portal to confirm your registration status and obligations for your specific address.

Now that you understand what coverage you need and why Florida’s regulations matter, the specific types of protection available for your property become your next priority.

Key Coverage Types for Short-Term Rental Properties

Liability Protection for Guest Injuries

Guest injuries on your property demand serious liability protection because a single accident can cost tens of thousands of dollars. Commercial General Liability coverage protects you when a guest is injured on your property or at amenities you provide off-site, such as a kayak or pool equipment. This coverage also extends to injuries that occur away from your property if they result from your rental operation. Medical payments coverage, typically $1,000 to $5,000 per person, handles minor injuries without requiring a lawsuit, which prevents small incidents from escalating into expensive claims.

If you have a pool or hot tub, verify that your liability policy explicitly covers these features because many standard policies exclude them or require additional endorsements. Liquor liability coverage protects you if a guest becomes intoxicated at your property and injures themselves or someone else. Without these protections, a guest’s medical bills and legal fees come directly from your pocket.

Property Coverage at Replacement Cost

Property coverage must reflect replacement cost, not the price you paid for your home or furnishings. If your rental property is worth $500,000 to rebuild, your dwelling coverage should equal that amount, not your purchase price from five years ago. Contents coverage should protect electronics, art, bikes, kayaks, and other amenities at replacement cost as well.

Bed bug and flea liability coverage is essential because infestations force you to cancel bookings and lose revenue, which standard policies ignore entirely. Property entrustment coverage protects against theft or damage caused by guests to items they use during their stay.

Understanding Hurricane Deductibles and Replacement Value

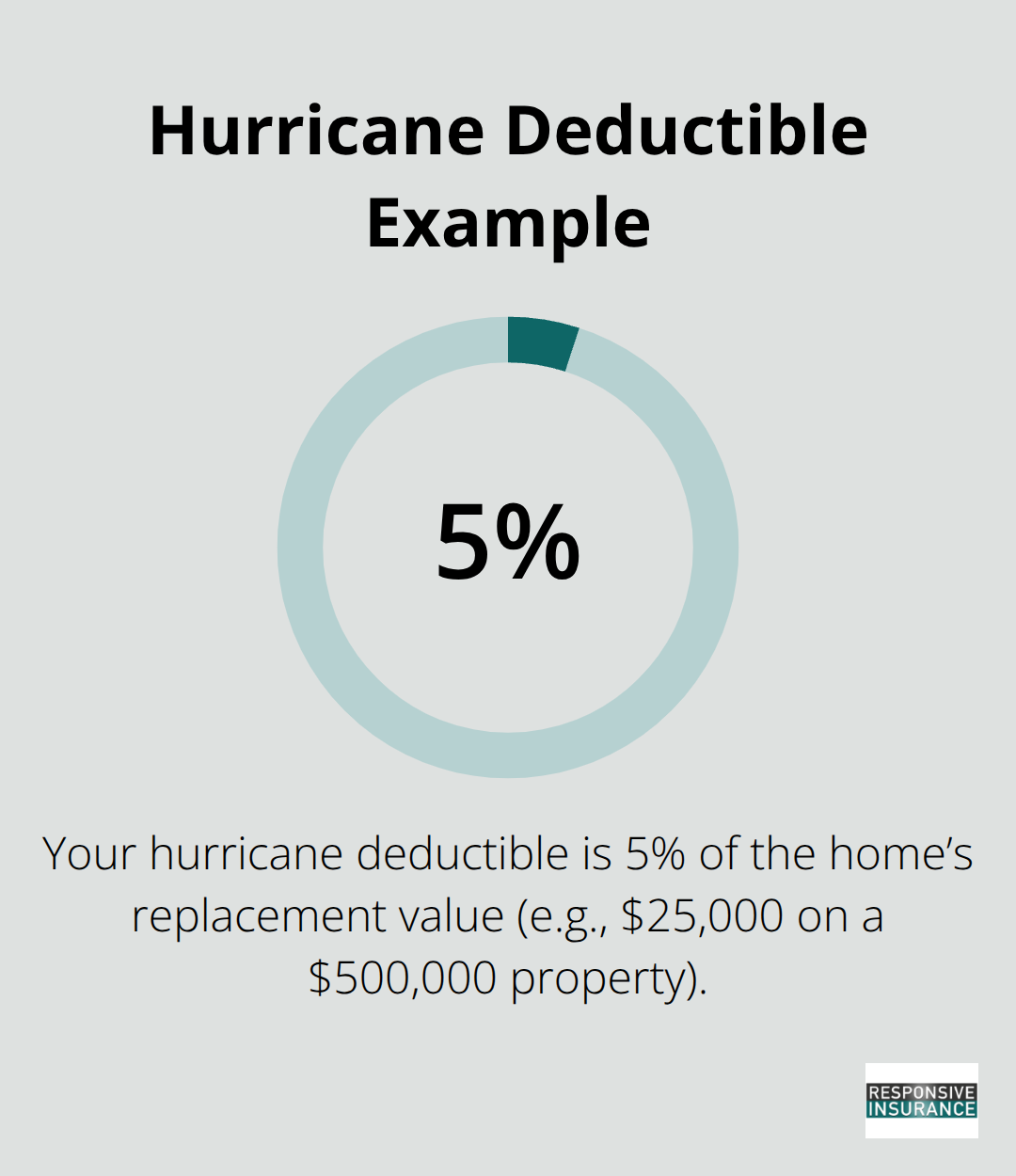

In Florida’s hurricane environment, understand your deductible structure carefully. A $10,000 hurricane deductible sounds manageable until you calculate it as 5 percent of your home’s replacement value, which could exceed $25,000 on a $500,000 property. This calculation matters because it determines how much you pay out of pocket when a hurricane damages your property.

Loss of Rental Income Protection

Loss of rental income protection compensates you when a covered claim makes your property unrentable, covering actual lost revenue from canceled bookings. This coverage has no time limit on some policies, meaning if a fire renders your property uninhabitable for six months, you receive compensation for those six months of lost bookings. Document your booking history and average nightly rate before you apply for this coverage, as insurers require this information to calculate your loss.

Once you understand these core coverages, you’ll want to identify the specific gaps that standard policies leave unaddressed-gaps that can expose your investment to significant financial risk.

Common Gaps in Coverage and How to Address Them

Guest Personal Property Leaves You Exposed

Your policy protects your dwelling and furnishings, but it does not cover a guest’s laptop, jewelry, or luggage if those items are stolen or damaged. Guests often assume their belongings fall under your coverage, then file claims against you when they discover otherwise. Require guests to carry their own renters insurance or clearly state in your booking terms that you do not cover their personal property. Document this requirement in your house rules and rental agreement to establish clear expectations upfront.

Additionally, some policies limit coverage for high-value items like electronics or artwork to $2,500 or $5,000 total, which falls far short if you furnish your rental with quality equipment. Review your specific policy limits for contents coverage and add scheduled personal property endorsements for items exceeding standard limits.

Hurricane Deductibles and Flood Risk Create Major Exposure

A hurricane deductible of 5 percent on a $500,000 property equals $25,000 out of pocket before insurance pays anything. That deductible applies separately to wind damage versus other perils depending on your policy language, so calculate your actual out-of-pocket costs before a storm hits. Flood damage receives no coverage under standard short-term rental policies, yet most Florida properties face flood risk regardless of zone designation. Federal flood insurance through the National Flood Insurance Program costs about $938 per year on average in Florida, and your lender may require it if your property sits in a mapped flood zone.

Fraudulent Claims Require Documented Defense

A guest might claim damage that existed before their stay, file a false injury report, or claim items were never returned. Your policy includes fraud protections, but you must document property conditions with photos and video before each guest arrives and photograph damage immediately after checkout. Create a pre-arrival and post-departure inspection checklist and photograph every room, appliance, and amenity systematically. This documentation becomes your defense against false claims and reduces claim settlement disputes.

Squatter Protection Addresses Extended Stays Gone Wrong

A guest who refuses to leave after their booking ends transforms a short-term rental into an illegal tenancy requiring formal eviction proceedings that can cost $3,000 to $8,000 and consume three to six months. Some policies include legal support and lost revenue protection for this specific risk, so verify your policy includes squatter coverage if you accept longer bookings or operate in markets with higher eviction risk.

Final Thoughts

Protecting your short-term rental investment in Florida requires three concrete actions. First, register your property with Collier County if you operate in unincorporated areas, obtain your Florida DBPR license, and document your compliance status for your insurance provider. Second, photograph your property before each guest arrives and immediately after checkout to defend against fraudulent damage claims. Third, calculate your actual out-of-pocket costs by translating hurricane deductibles into dollars and determining whether flood insurance makes financial sense for your location.

Short-term rental insurance Florida policies differ fundamentally from homeowners coverage because they account for guest turnover, higher liability exposure, and lost income risk. Your policy should include commercial general liability starting at $1 million, dwelling and contents coverage at replacement cost, loss of rental income protection with no time limits, and property entrustment coverage for guest-caused damage. If you provide amenities like pools or kayaks, verify those features receive explicit coverage, and if you accept longer bookings, confirm your policy includes squatter protection and legal support.

We at Responsive Insurance, Inc. work with multiple A-rated insurance companies to compare coverage options and find the policy that fits your specific property and rental model. Contact us at responsiveinsurance.com to discuss your short-term rental property and receive a quote tailored to your dwelling replacement cost, furnishings, location, and desired coverage limits.