Private Flood Florida: Exploring Your Insurance Options

Flooding poses a real threat to homeowners in Naples, FL, with the region experiencing some of the highest flood risk in the nation. Standard homeowners insurance won’t protect your property from flood damage, leaving many residents vulnerable.

At Responsive Insurance, Inc., we help homeowners understand their private flood insurance options and find coverage that fits their needs. This guide breaks down how private flood policies compare to the National Flood Insurance Program so you can make the right choice for your home.

Why Florida Faces Extraordinary Flood Risk

Geography Creates Perfect Conditions for Flooding

Florida’s geography makes it one of the most flood-prone states in America, and Naples residents face this threat more acutely than most. The state has roughly 8,400 miles of coastline, and much of Florida sits only feet above sea level. Rising tides, storm surge from hurricanes, and heavy rainfall all converge to create perfect conditions for flooding.

Flood Risk Extends Beyond High-Risk Zones

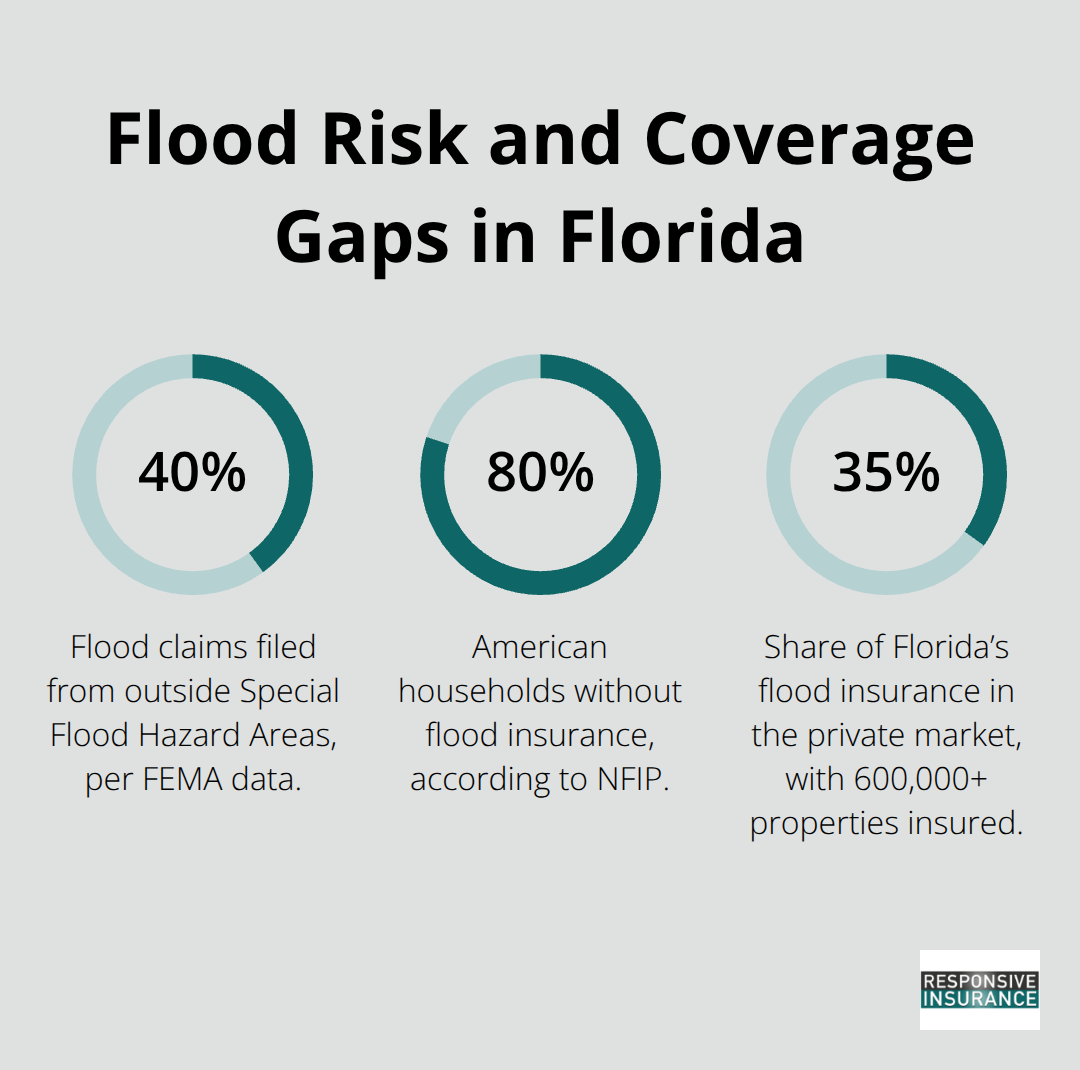

According to FEMA data, about 40 percent of flood claims come from properties outside Special Flood Hazard Areas, meaning homeowners in moderate and low-risk zones still face real exposure. This statistic reveals a critical truth: flood risk exists statewide, not just in the obvious danger zones. Your property’s location on a flood map does not determine whether water will reach your home during a major storm or heavy rainfall event.

Standard Homeowners Insurance Leaves You Unprotected

Standard homeowners insurance explicitly excludes flood damage, no matter how catastrophic the loss. Your homeowners policy covers wind damage from hurricanes, but the moment water rises and floods your home, that coverage stops. Mortgage lenders know this gap exists, which is why they require flood insurance on properties in designated flood zones.

The Protection Gap Puts Homeowners at Risk

The National Flood Insurance Program reports that roughly 80 percent of American households lack flood insurance, creating a massive protection gap. In Florida, where flooding is the costliest natural disaster, this gap puts thousands of homeowners at serious financial risk. The average NFIP flood insurance cost in Naples runs around $1,498 per year according to city-level data, but that investment protects against losses that regularly exceed $100,000. Without flood coverage, a single storm surge or heavy rain event can wipe out your savings and leave you personally liable for all repair costs.

Understanding Your Coverage Options

Now that you understand why Florida homeowners face such significant flood exposure, the next step involves comparing the two main paths to protection: the National Flood Insurance Program and private flood insurance policies. Each option offers distinct advantages and trade-offs that directly affect your coverage limits, costs, and long-term financial security.

NFIP vs. Private Flood Insurance

Coverage Limits Tell the Real Story

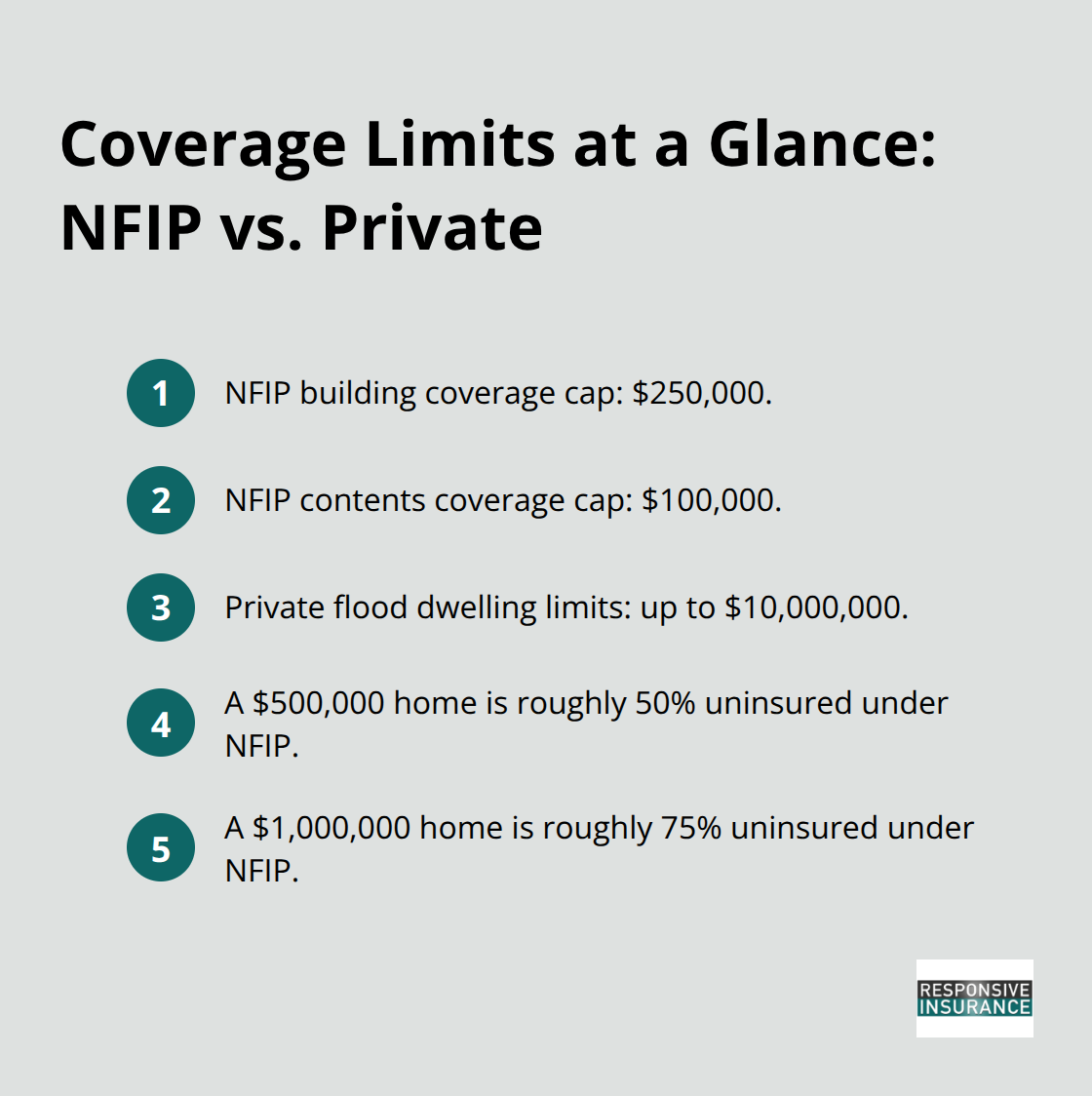

The National Flood Insurance Program and private flood insurers operate under fundamentally different models, and those differences directly impact your wallet and your protection level. NFIP coverage limits cap residential building coverage at $250,000 and contents at $100,000, which leaves significant gaps for Naples homeowners with properties worth more than that. Private flood carriers offer dwelling limits up to $10 million, replacement-cost contents coverage, and loss-of-use protection that NFIP simply does not provide.

For a $500,000 home, NFIP leaves roughly 50 percent of your structure value uninsured. For a $1 million property, that gap widens to 75 percent. Private flood insurance fills those gaps, making it the stronger choice for homeowners with substantial property values.

How Pricing Varies by Flood Zone

Pricing tells a different story depending on your flood zone and property characteristics. In moderate-risk Zone X areas, private flood typically costs 10 to 30 percent less than NFIP for newer, well-maintained properties, with private quotes ranging from $350 to $600 annually compared to NFIP rates of $500 to $800. In higher-risk Zone AE areas, NFIP averages $1,500 to $4,000 yearly while private carriers quote $1,200 to $5,000, meaning your property condition and elevation matter more with private underwriting.

Zone VE coastal areas present a different picture: NFIP charges $4,000 to $12,000 annually while private insurers quote $3,500 to $15,000, so NFIP may cost less in the highest-risk zones. This matters because Florida’s private flood market now accounts for roughly 35 percent of the state’s flood insurance business, with over 600,000 privately insured properties, making competition fierce and pricing more flexible than NFIP’s standardized rates.

What Private Carriers Actually Evaluate

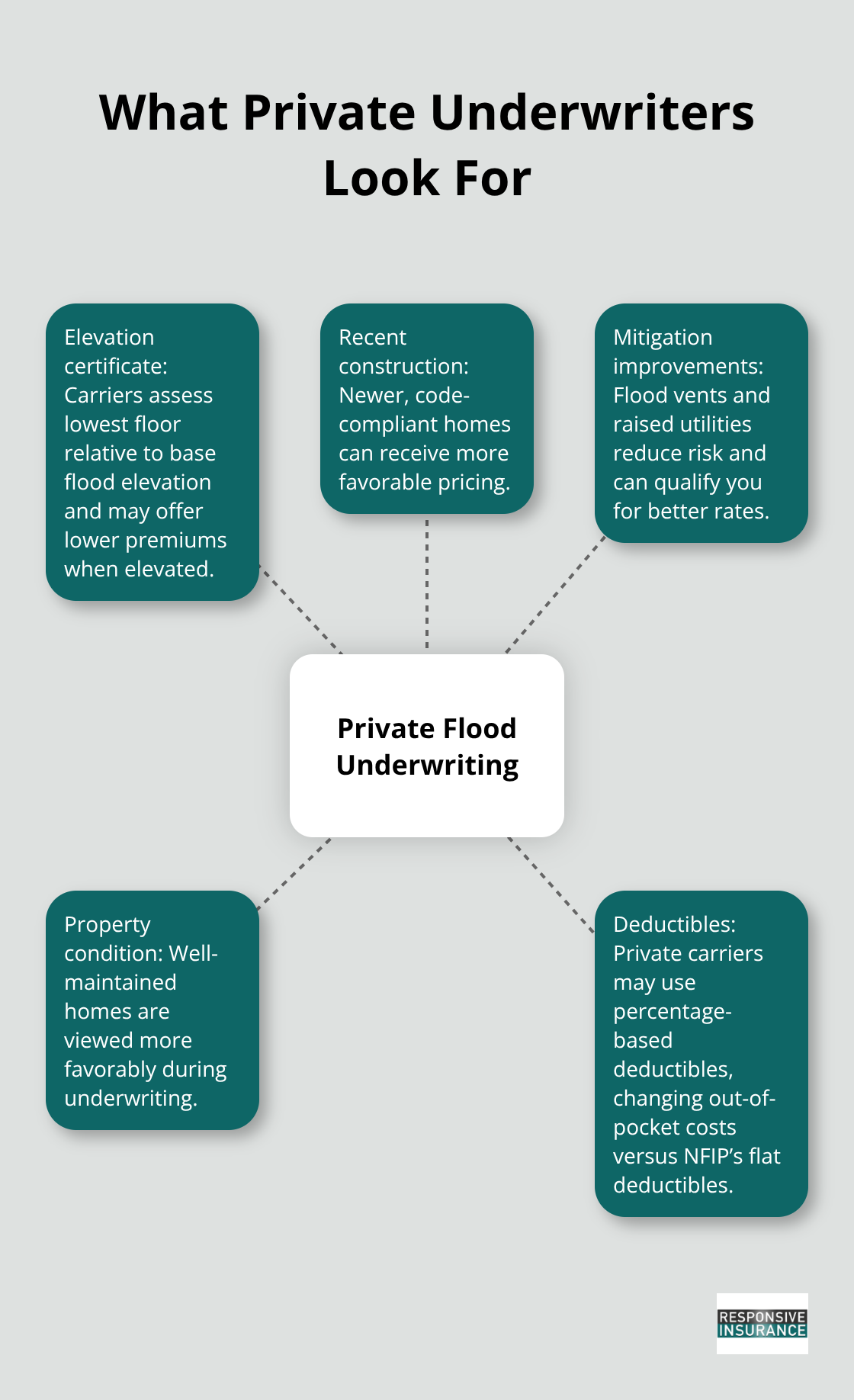

Private carriers evaluate elevation certificates, recent construction, mitigation improvements, and property condition, meaning an elevated home or one with flood vents can qualify for significantly better rates. NFIP applies zone-based pricing with less flexibility, so your specific improvements do not reduce your premium. Deductibles also differ: NFIP typically offers flat deductibles while private carriers may use percentage-based deductibles, affecting your out-of-pocket costs after a loss.

For Naples homeowners, the practical approach involves obtaining quotes from both NFIP and multiple private carriers to compare actual numbers for your specific property rather than relying on general ranges. This comparison reveals which option truly protects your home at the lowest cost, setting the stage for the next critical step in your decision-making process.

How to Find the Right Coverage for Your Home

Identify Your Flood Zone First

Start with your flood zone, because this single piece of information determines whether you face mandatory insurance requirements and dramatically affects your pricing options. The City of Naples provides an interactive flood map tool where you can enter your address and instantly see your zone designation-whether that is AH for shallow flooding, AE for standard risk, VE for coastal high-hazard areas, or one of the X zones for moderate-to-low risk. If you live outside Naples city limits, use FEMA’s Flood Map Service Center to locate your zone. Contact the City Floodplain Coordinator for official confirmation, especially if you plan to challenge your designation or apply for a mortgage. This step takes 15 minutes and eliminates guesswork about your actual risk level.

Obtain an Elevation Certificate to Lower Your Premiums

Next, obtain an elevation certificate if your property sits in a Special Flood Hazard Area, because this document directly reduces your premiums and opens access to private carrier options that NFIP cannot match. A licensed surveyor prepares the certificate by measuring your home’s lowest floor elevation relative to the base flood elevation, typically costing $300 to $500. For a home elevated above the base flood elevation, this investment pays back in 5 to 15 years through premium reductions of 15 to 30 percent with private carriers. NFIP does not reward elevation with lower rates, so if your home sits above base flood elevation, private flood becomes the obvious financial choice. You need this certificate before requesting quotes from private carriers, so obtain it early in your shopping process.

Compare Multiple Quotes and Coverage Types

Gather three key quotes: one from NFIP through your current homeowners insurer or a participating agent, and at least two from different private carriers like Neptune Flood, Palomar, or Wright Private Flood. Compare not just the annual premium but the actual coverage differences. NFIP pays actual cash value for contents, meaning your 5-year-old furniture depreciates significantly, while major private carriers pay replacement cost. NFIP caps dwelling coverage at $250,000, leaving a $500,000 home 50 percent uninsured. Private policies close these gaps entirely. For Naples properties valued above $500,000, private flood becomes non-negotiable because NFIP simply cannot protect your full investment.

Work with an Independent Agent

Work with an independent agent who represents multiple carriers, because they spend their time comparing policies rather than pushing a single option. Your agent should explain what happens after a claim, including how quickly each carrier processes payments and whether they offer loss-of-use coverage that reimburses temporary housing costs. Ask about the carrier’s financial strength rating from Demotech or A.M. Best, because private carriers have occasionally exited the Florida market after major hurricanes, while NFIP guarantees renewal regardless of claims history. An independent agent evaluates these exact scenarios, matching specific properties to the carriers offering the best combination of price, limits, and stability.

Final Thoughts

Private flood insurance in Florida offers Naples homeowners protection that NFIP alone cannot match. NFIP caps dwelling coverage at $250,000 and contents at $100,000, leaving a $500,000 home 50 percent uninsured and a $1 million property 75 percent unprotected. Private carriers eliminate these gaps entirely, offering dwelling limits up to $10 million and replacement-cost contents coverage that reimburses what your belongings actually cost to replace rather than their depreciated value.

Private flood Florida options also reward your mitigation investments in ways NFIP ignores completely. If you elevated your home, installed flood vents, or raised utilities above the base flood elevation, private carriers reduce your premiums by 15 to 30 percent while NFIP applies the same rate regardless of your improvements. This means your investment in flood protection pays dividends through lower insurance costs that compound over years, making private flood the financially smarter choice for properties with substantial improvements.

Your next step involves obtaining quotes from both NFIP and multiple private carriers for your specific property, because your flood zone, elevation, and property condition all influence pricing differently depending on the carrier. We at Responsive Insurance, Inc. work with multiple A-rated insurance companies to compare coverage and find the best fit for your needs-contact us today to discuss your flood risk and secure the protection your home deserves.