How Much is Flood Insurance in Florida?

Flood insurance costs in Florida vary significantly based on your home’s location, elevation, and flood risk zone. At Responsive Insurance, Inc., we’ve seen premiums range from a few hundred to several thousand dollars annually, depending on these factors.

Understanding your options between the National Flood Insurance Program and private providers can help you find the right coverage at the best price. This guide breaks down exactly what you’ll pay and how to reduce those costs.

What You’ll Actually Pay for Flood Insurance in Florida

Florida flood insurance premiums swing wildly depending on where your home sits and how exposed it is to water. The National Flood Insurance Program reports that statewide average costs hover around $792 annually, but that number masks the real story. A homeowner in Miami might pay $344 per year through NFIP coverage, while someone in Cape Coral faces $1,508. Private insurers often undercut NFIP by 20 to 40 percent for moderate-risk properties, making comparison shopping non-negotiable. Your actual bill depends on four concrete factors: flood zone designation, elevation relative to flood levels, construction year, and the deductible you choose.

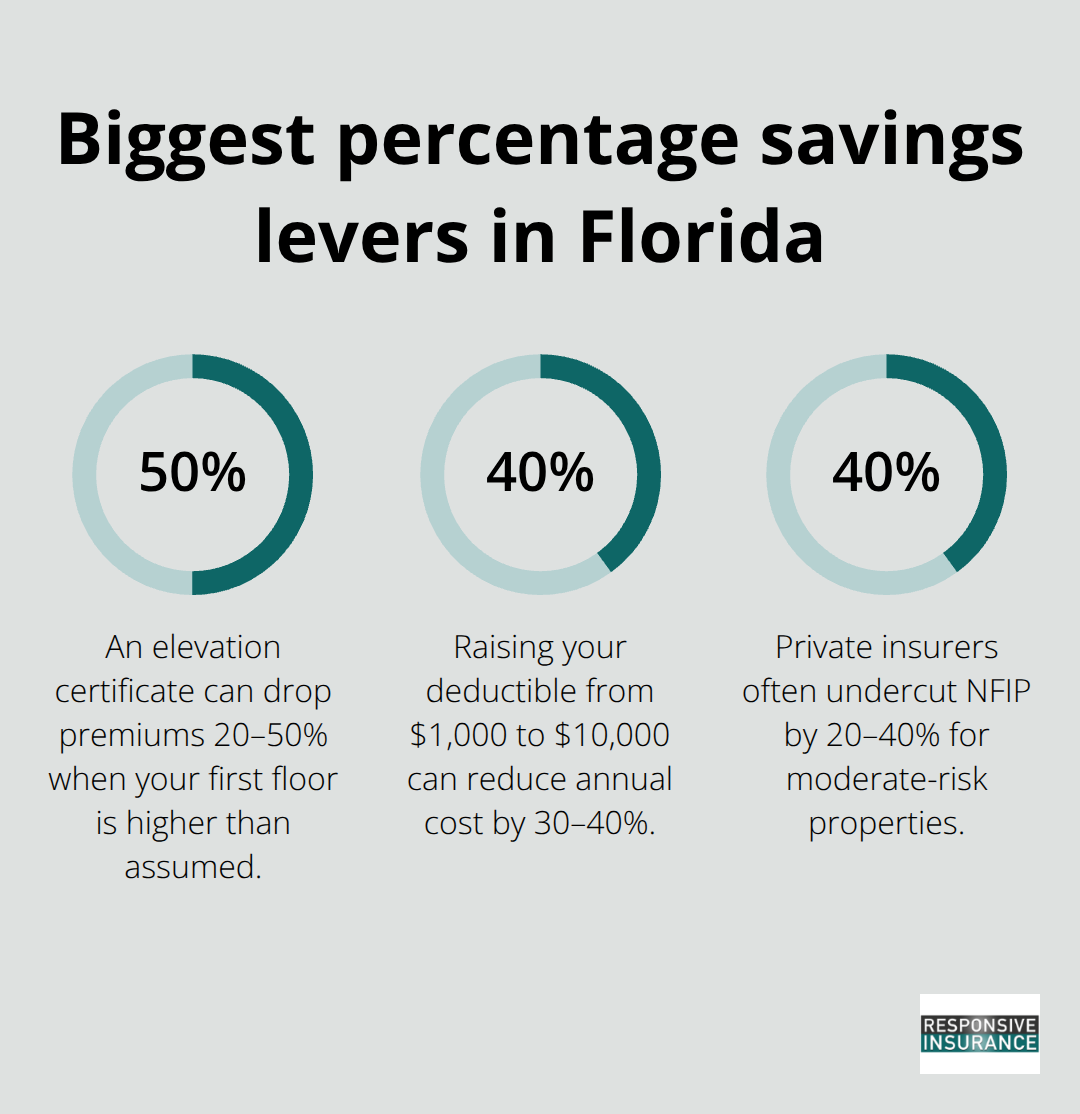

An older home built before 1974 in a high-risk zone can easily cost $5,000 to $15,000 annually with NFIP, whereas a newer elevated home in a moderate zone might run $400 to $1,000. Deductible selection alone shifts your premium significantly-jumping from $1,000 to $10,000 can reduce your annual cost by 30 to 40 percent, though you’ll shoulder more risk in a claim.

Your Flood Zone Determines Your Starting Price

FEMA assigns your property to a flood zone, and this single factor shapes your baseline premium more than anything else. High-risk zones labeled AE or VE carry NFIP costs between $2,000 and $15,000 annually depending on elevation, while moderate-risk X zones typically run $400 to $1,200. Coastal properties in Naples that sit in velocity zones-where storm surge combines with wave action-pay the steepest rates because damage potential is highest. You can verify your flood zone free through FEMA’s Flood Map Service Center, and this step should happen before you request any quote. The difference between zones often justifies hiring a surveyor to obtain an elevation certificate, which documents your home’s exact height relative to flood levels. If that certificate shows your first floor sits higher than assumed, your premium can drop 20 to 50 percent retroactively.

Elevation and Home Features Cut Costs Substantially

Homes elevated on stilts or with first floors well above base flood elevation pay dramatically less than ground-level properties. Risk Rating 2.0, FEMA’s current pricing model, rewards each foot above flood level with roughly 10 to 20 percent premium reduction. Flood vents in foundation walls and elevated utilities like water heaters and HVAC systems on higher floors qualify you for rate discounts that compound over time. These mitigation investments typically cost $5,000 to $25,000 upfront but can save $100 to $300 monthly on premiums, recouping the investment within five to ten years. Your insurance agent can identify which improvements your specific property needs and connect you with contractors experienced in flood mitigation. Understanding these cost-reduction strategies positions you to make informed decisions when you compare NFIP and private flood insurance options.

NFIP or Private Flood Insurance

The National Flood Insurance Program dominates Florida’s flood insurance market because it remains the only option available in many areas and because federal law requires it for mortgaged homes in high-risk zones. NFIP charges according to FEMA’s Risk Rating 2.0 model, which prices each property individually based on flood zone, elevation, construction year, and distance to water. You’ll pay anywhere from $344 annually in low-risk Miami to $1,924 in high-risk Franklin County through NFIP, with the statewide average around $792. The program caps your building coverage at $250,000 and contents at $100,000, which falls short for valuable homes. NFIP policies also come with a standard 30-day waiting period before coverage activates, meaning you cannot buy coverage today and have it protect you tomorrow. This waiting period disappears only during mortgage closings, so timing matters if you’re purchasing a home.

Private Insurers Offer Speed and Higher Limits

Private flood insurers like Allstate, Liberty Mutual, and USAA now compete in Florida and often undercut NFIP by 20 to 40 percent for moderate-risk properties. Private carriers frequently offer building limits up to $1.5 million or higher, contents coverage to $750,000, and loss-of-use benefits that reimburse temporary housing costs if you cannot occupy your home. These companies typically activate coverage within 7 days instead of 30, giving you faster protection. The trade-off is that private insurers can cancel policies if your property deteriorates or risk increases, whereas NFIP provides government-backed stability.

How to Compare Your Options

You must compare actual quotes for your property rather than relying on averages. Request NFIP quotes through your homeowners insurance agent or directly from participating insurers, then ask that same agent to pull private quotes from carriers they represent. An elevation certificate costs $500 to $1,500 but often reveals you qualify for substantially lower rates once your actual first-floor height is documented instead of assumed. If you’re in Naples and carry a mortgage, verify whether your lender or Citizens Property Insurance imposes flood insurance requirements, as Citizens now mandates flood coverage for wind policies on homes valued above $400,000 starting in 2026.

Coverage for Renters and Special Situations

For renters, flood coverage starts around $100 annually and protects your belongings since landlord policies exclude tenant property. Private insurers sometimes offer renters flood insurance with broader protections than NFIP’s standard contents-only policies. The decision ultimately hinges on three factors: your flood zone designation, the value of your home and possessions, and your tolerance for waiting periods. High-risk coastal properties in velocity zones almost always cost less through private insurers despite NFIP’s 18 percent annual rate cap. Moderate-risk homes inland frequently find better value with NFIP’s standardized pricing, especially if you’ve obtained an elevation certificate showing height above base flood elevation.

Stay Current With Annual Rate Changes

You should shop annually because rates and coverage options shift, and maintaining continuous flood insurance preserves grandfathered rates that can save 40 to 60 percent compared to new policies after FEMA map updates. As you evaluate these options, the specific mitigation improvements available to your property can further reduce what you ultimately pay, which we’ll explore in the next section.

Reducing Premiums Through Home Improvements

Elevation and Utility Upgrades Deliver Fast Savings

Structural elevation or utility upgrades produce the fastest return on investment when you want to lower flood insurance costs. FEMA’s Risk Rating 2.0 model allows FEMA to calculate premiums across all policyholders based on the value of their home and individual property’s flood risk. Utility upgrades like moving water heaters, HVAC systems, and electrical panels to higher floors qualify you for immediate discounts without the expense of structural elevation. These improvements cost $5,000 to $8,000 and save $100 to $300 monthly, recouping the investment within two to four years while your home becomes more flood-resistant.

Flood Vents Reduce Structural Damage Risk

Flood vents in foundation walls cost $1,500 to $3,000 but allow floodwaters to equalize pressure on walls and foundations, reducing structural damage risk and triggering rate reductions of 5 to 15 percent depending on your flood zone. These vents open automatically when water pressure builds, preventing catastrophic foundation failure that insurance claims often cover. Properties where structural elevation isn’t feasible benefit most from flood vents because they generate meaningful savings without major construction work.

Drainage Improvements Support Overall Resilience

Improving site drainage and landscaping around your property matters less for premium reduction than elevation and vents, but it still counts toward mitigation discounts. Regrading soil away from your foundation, installing French drains, or clearing gutters and downspouts costs minimal money yet signals to insurers that you take flood risk seriously. Naples properties sitting in moderate-risk zones benefit most from drainage improvements because they face occasional localized flooding rather than major storm surge events. Drainage improvements rarely justify expense solely for insurance savings, but they improve your property’s overall resilience and complement other mitigation work.

Get an Elevation Certificate First

The practical path forward involves obtaining an elevation certificate first, then consulting with a flood mitigation contractor about which improvements make financial sense for your specific situation. An elevation certificate costs $500 to $1,500 and documents your home’s exact first-floor height relative to base flood elevation, often revealing you already qualify for lower rates than you’re paying. Once that certificate is in hand, request updated quotes from both NFIP and private insurers because the new documentation frequently unlocks rate reductions of 20 to 50 percent. If those quotes still feel high, ask your insurance agent which mitigation improvements would generate the largest savings for your property.

Take Action Rather Than Accept Default Rates

These concrete actions separate homeowners who passively accept whatever premium they’re quoted from those who actively reduce their insurance costs through documented risk reduction. After you obtain your elevation certificate, ask your insurance agent which improvements would deliver the largest savings for your property. Replacing critical systems costs less than structural elevation but generates smaller annual savings, making them ideal for properties where raising the home isn’t feasible. The specific mitigation improvements available to your property can further reduce what you ultimately pay.

Final Thoughts

Florida flood insurance costs hinge on three factors you control: your flood zone, your home’s elevation, and the coverage limits you select. Homeowners who take action pay significantly less than those who accept default quotes, and the difference often reaches hundreds of dollars annually. An elevation certificate costs $500 to $1,500 but frequently unlocks rate reductions of 20 to 50 percent, making it the single most valuable step you can take before requesting quotes from NFIP and private carriers.

Your actual premium for how much is flood insurance in Florida depends entirely on your specific property and the choices you make. Compare quotes from both NFIP and private insurers through your agent rather than assuming one option costs less, and verify whether your mortgage lender or Citizens Property Insurance imposes flood insurance requirements that affect your timeline. Mitigation improvements like elevated utilities, flood vents, or drainage work can generate substantial savings once your agent identifies which ones apply to your Naples home.

Contact Responsive Insurance, Inc. to request quotes from multiple A-rated carriers and discuss which improvements make financial sense for your property. Our independent agency works with multiple insurers to compare coverage options and find the best fit for your needs, so you understand exactly what you’re paying and why.