Do I Need Flood Insurance in Florida? A Quick Guide

Florida faces some of the highest flood risks in the United States, with over 2.5 million properties at risk of flooding. Many Naples residents ask: “Do I need flood insurance in Florida?”

The answer depends on your specific location, mortgage requirements, and risk tolerance. At Responsive Insurance, Inc. help Florida homeowners navigate these complex decisions to protect their most valuable investment.

Why Is Florida So Flood-Prone

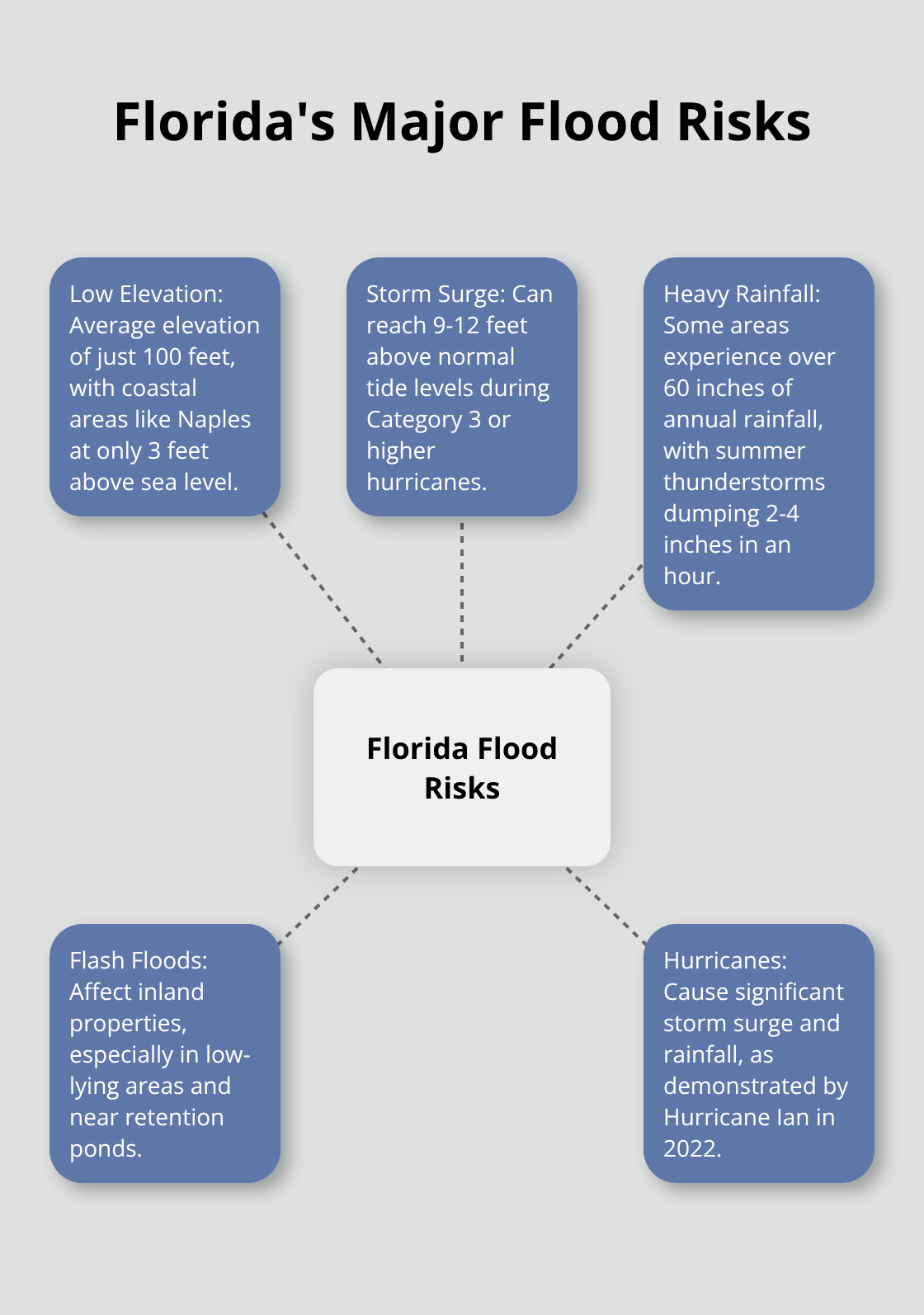

Florida’s geography creates a perfect storm of flood risks that homeowners must understand before they make insurance decisions. The state sits barely above sea level with an average elevation of just 100 feet, while coastal areas like Naples hover at only 3 feet above sea level. This low elevation means even minor storm surge or heavy rainfall can quickly overwhelm drainage systems and flood properties.

Storm Surge Devastation Along the Coast

Hurricane Ian in 2022 demonstrated the power of storm surge when it pushed 12-15 feet of water inland along Southwest Florida’s coast. Storm surge causes significant hurricane-related fatalities and billions in property damage. Naples residents face particular vulnerability during Category 3 or higher hurricanes, where surge heights can reach 9-12 feet above normal tide levels.

Floodwater causes substantial damage to homes, with even small amounts creating expensive repairs. Properties within one mile of the coast face the highest storm surge risk, but surge can penetrate several miles inland through rivers and canals.

Rainfall Floods Affect Everyone

Florida receives substantial annual rainfall statewide, with some areas experiencing over 60 inches. Summer thunderstorms regularly dump 2-4 inches of rain in just one hour and overwhelm municipal drainage systems. Most flood-related deaths occur in vehicles, often from drivers who attempt to cross flooded roads with moving water.

Inland properties face significant risk from flash floods, especially in low-lying areas and near retention ponds. Even areas outside flood zones experience floods – a significant percentage of flood insurance claims come from moderate-to-low risk areas.

These flood risks make insurance requirements vary significantly across Florida, which depends on your specific location and mortgage situation.

When Flood Insurance is Required vs Optional

Florida law mandates flood insurance for specific properties, while other homeowners face optional coverage decisions. Properties located in Special Flood Hazard Areas with federally backed mortgages must carry flood insurance – this affects roughly 25% of Florida homeowners. FEMA designates these high-risk zones as A and V areas, where properties face at least a 1% annual chance of flooding each year. Lenders require this coverage because standard homeowner policies exclude flood damage, which leaves mortgage holders exposed to significant financial losses.

Mandatory Coverage Under New Florida Laws

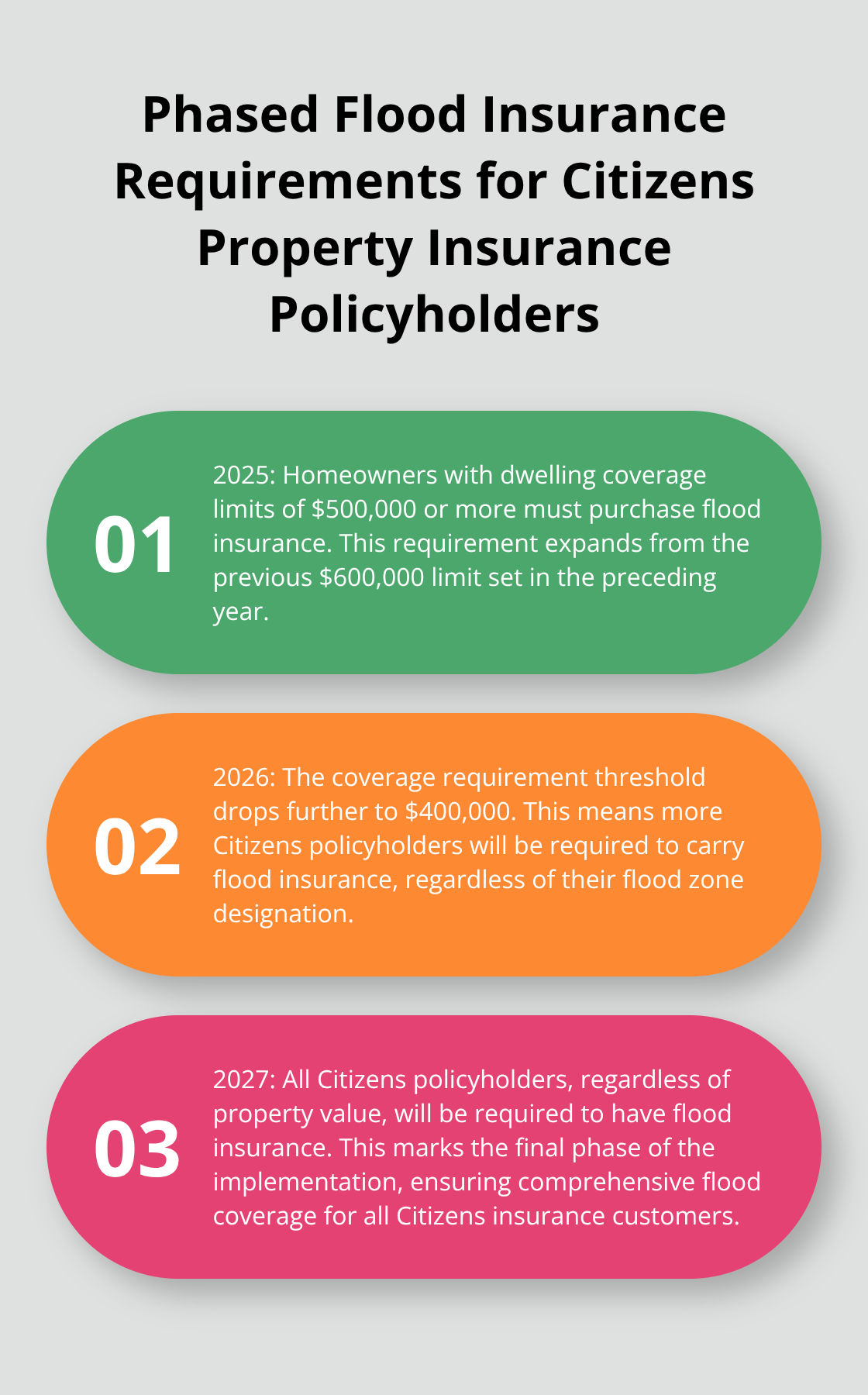

Senate Bill 2A creates phased flood insurance requirements for Citizens Property Insurance policyholders. As of 2025, state law requires many Citizens policyholders to carry separate flood insurance, even if you’re not in a designated high-risk flood zone. Homeowners with dwelling coverage limits of $600,000 or more must purchase flood insurance immediately. Coverage requirements drop to $500,000 in 2025, then $400,000 in 2026. All Citizens policyholders need flood insurance regardless of property value when 2027 arrives. Upper-floor condominiums receive exemptions due to reduced flood susceptibility. These requirements affect thousands of Naples residents who rely on Citizens as their insurer of last resort.

Smart Coverage for Optional Properties

Homeowners outside high-risk zones should strongly consider flood insurance despite no legal requirements. Approximately 40% of National Flood Insurance Program claims originate from moderate-to-low risk areas according to FEMA data. Properties in preferred risk zones qualify for lower-cost policies that start around $400 annually (making protection affordable for most budgets). Flood insurance policies require a mandatory 30-day waiting period before coverage begins, which makes advance planning essential.

Timing Restrictions and Coverage Gaps

Homeowners cannot purchase coverage immediately before hurricanes threaten the area, which leaves procrastinators without protection during critical storm seasons. The 30-day waiting period applies to all new policies and coverage increases (though some exceptions exist for property sales). This timing restriction means homeowners must plan ahead rather than wait for storm forecasts to purchase protection.

Understanding these requirements helps homeowners determine their legal obligations, but the types of coverage available offer different levels of protection and cost structures worth exploring.

Types of Flood Insurance Coverage Available

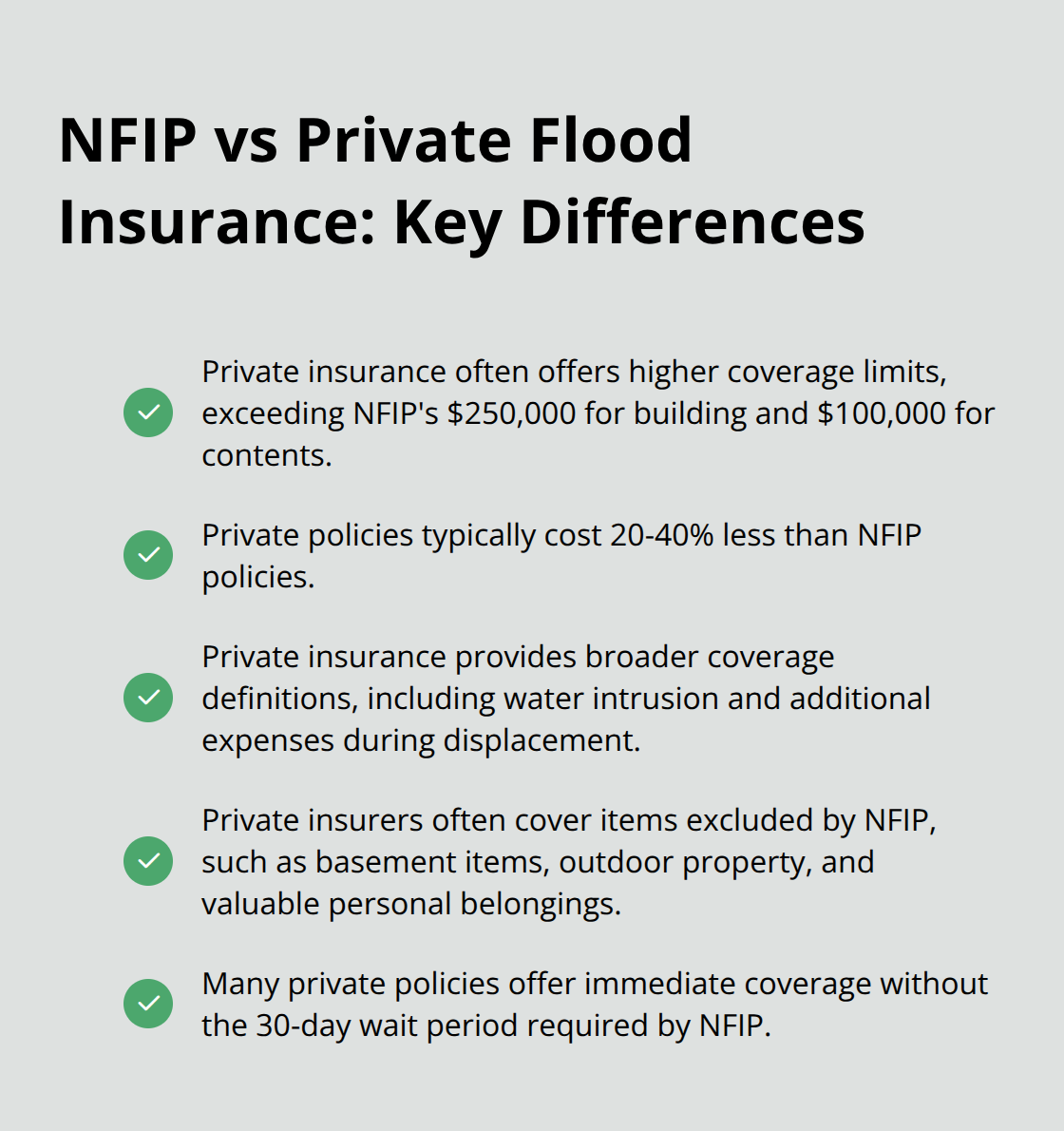

Florida homeowners choose between National Flood Insurance Program policies and private flood insurance options, each with distinct advantages and limitations. NFIP policies provide standardized coverage with building protection up to $250,000 and contents coverage up to $100,000, while private insurers often exceed these limits with building coverage that reaches $500,000 or more. The average NFIP policy costs $865 annually in Florida, though Risk Rating 2.0 implementation means many Naples residents face premium increases that reflect true flood risk. Private flood insurance typically costs 20-40% less than NFIP policies while it provides broader coverage definitions that include water intrusion and additional expenses during displacement.

NFIP Coverage Limitations You Must Know

National Flood Insurance Program policies exclude basement items, currency, precious metals, and most outdoor property from coverage. NFIP policies also impose a 30-day wait period and limit additional expenses, which creates gaps during extended displacement periods. The program defines flood as water that affects two or more properties simultaneously, which excludes isolated incidents like burst pipes or localized drainage problems. NFIP policies provide replacement cost coverage for residential structures but actual cash value for contents (meaning depreciation reduces your claim payments for personal belongings).

Private Insurance Advantages and Flexibility

Private flood insurers offer customized policies that surpass NFIP limitations with higher coverage limits, lower deductibles, and expanded definitions of flood damage. These policies frequently include coverage for temporary housing, meal expenses, and property not covered under NFIP such as pools, fences, and landscaping. Private insurers also provide immediate coverage in many cases without wait periods, though rates vary significantly based on property elevation, age, and specific location within Naples flood zones.

Coverage Limits and What Protection Includes

Standard NFIP policies cover structural damage, debris removal, and basic household utilities up to policy limits. Contents coverage protects furniture, clothing, electronics, and appliances but excludes items stored in basements below ground level. Private policies often extend protection to include jewelry, artwork, and other valuable items that NFIP excludes (with higher limits available for comprehensive protection). Both policy types cover foundation damage and structural repairs necessary to restore your home to pre-flood condition, though detached structures require separate consideration for coverage.

Final Thoughts

Do I need flood insurance in Florida? The evidence overwhelmingly points to yes for most Naples homeowners. With 40% of flood claims that come from moderate-risk areas and new state requirements that expand coverage mandates, flood insurance transforms from optional protection to financial necessity. Florida’s unique geography and storm intensity make flood damage inevitable rather than possible.

Standard homeowner policies exclude flood damage, which leaves uninsured property owners who face repair costs that often exceed $25,000 per incident. The 30-day wait period means you cannot purchase coverage when storms approach. Advance planning becomes essential for protection since you must secure coverage before you need it.

Smart homeowners act before they need coverage and determine their flood zone status through FEMA maps. They compare NFIP and private insurance options to find the best rates and coverage limits for their property (properties outside high-risk zones often qualify for preferred risk policies that start around $400 annually). We at Responsive Insurance, Inc. help Naples families navigate complex coverage decisions and find flood insurance that fits their specific needs and budget.

Trackbacks & Pingbacks

[…] in a standard HO-3 policy in Florida, you do have the option to exclude it to save on premiums. Flood coverage is almost never included in standard homeowners policies anywhere in the country, so you must purchase flood insurance separately through either private […]

Comments are closed.