Private Flood Insurance vs FEMA What’s the Difference?

Flooding poses a real threat to Naples homeowners, and choosing the right insurance protection matters. When comparing private flood insurance vs FEMA coverage, understanding the key differences helps you make an informed decision for your property.

At Responsive Insurance, Inc., we’ve helped countless residents navigate these options and find the protection that fits their needs and budget.

Understanding FEMA Flood Insurance

FEMA flood insurance, officially called the National Flood Insurance Program (NFIP), is a federal program that has protected American homeowners since 1968. Unlike private insurance, NFIP coverage is backed by the federal government, which means it operates under different rules and pricing structures than standard homeowners policies. The program currently serves about 5.2 million policyholders across the United States, according to FEMA data. For Naples residents, NFIP policies are often the most accessible option because they’re available regardless of your property’s flood risk level, though rates vary significantly based on your specific flood zone designation. The program requires that if your home is in a high-risk flood zone and you have a mortgage from a federally regulated lender, you must carry flood insurance as a condition of your loan.

What NFIP Actually Covers

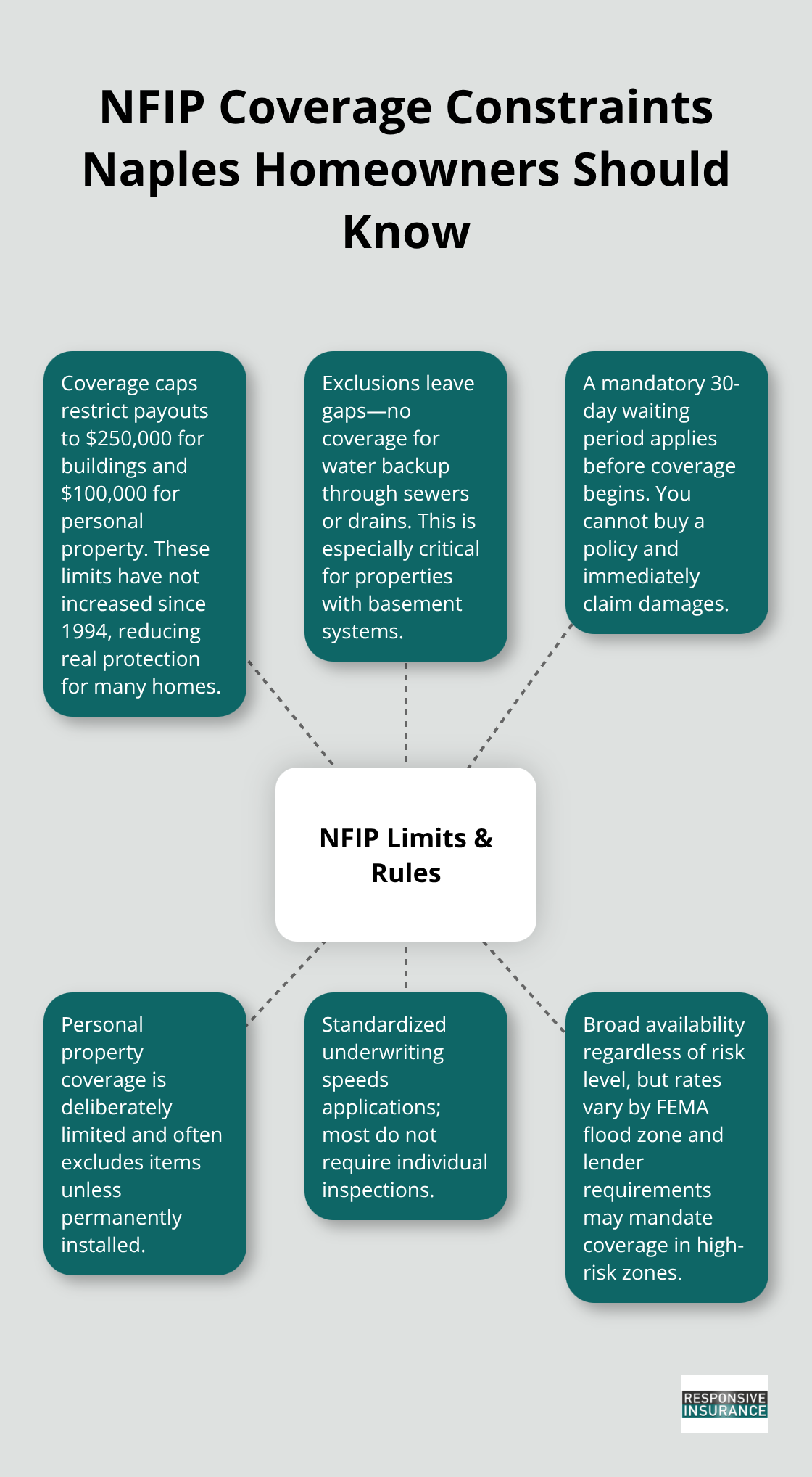

NFIP policies cap coverage at $250,000 for building damage and $100,000 for personal property damage, which is a significant limitation for many Naples homes. These limits haven’t increased since 1994, meaning they cover far less than the actual replacement cost of most modern properties in our area. The coverage pays for structural damage caused by flooding, including foundation repairs, electrical systems, and permanent fixtures, but excludes damage from water backup through sewers or drains (a critical gap for properties with basement systems).

Personal property coverage in an NFIP policy is deliberately limited and won’t cover items like furniture, appliances, or clothing unless they’re permanently installed. NFIP policies carry a mandatory waiting period of 30 days before coverage begins, so you can’t purchase a policy and immediately claim damages.

How NFIP Premiums Get Calculated

NFIP rates depend almost entirely on your property’s flood zone designation, which FEMA determines through Flood Insurance Rate Maps. Homes in high-risk zones (designated as Special Flood Hazard Areas) pay significantly more than those in moderate or low-risk zones. A Naples property in a high-risk zone might pay $800 to $2,000 annually, while a similar home in a lower-risk zone could pay $300 to $600. FEMA recently implemented Risk Rating 2.0, a newer pricing model that considers additional factors like elevation, distance to water, and property characteristics, making rates more individualized than before. However, these federally set rates are often lower than what private insurers charge, especially for newer or elevated homes, which is why many homeowners initially choose NFIP despite its coverage limitations.

The Application Timeline and Process

Applying for NFIP coverage is straightforward and can typically be completed within a few days. You’ll need your property’s address, mortgage information if applicable, and details about your home’s construction and elevation. Most NFIP policies become effective 30 days after purchase, so timing matters when you’re trying to meet lender requirements. Licensed insurance agents in Florida can sell NFIP policies rather than requiring you to go directly to FEMA. The underwriting process is faster than private insurance because FEMA uses standardized criteria and doesn’t conduct individual property inspections for most applications.

Why Some Naples Homeowners Look Beyond NFIP

The coverage limits and exclusions in NFIP policies leave many Naples homeowners underprotected, especially those with properties worth significantly more than $250,000. The 30-day waiting period also creates problems for homeowners who need immediate coverage before closing on a property. These gaps in federal coverage have led many residents to explore private flood insurance options that offer higher limits and more flexible terms. Understanding what NFIP doesn’t cover sets the stage for evaluating whether private flood insurance might fill those protection gaps for your specific situation.

What Private Flood Insurance Offers That NFIP Doesn’t

How Private Coverage Exceeds Federal Limits

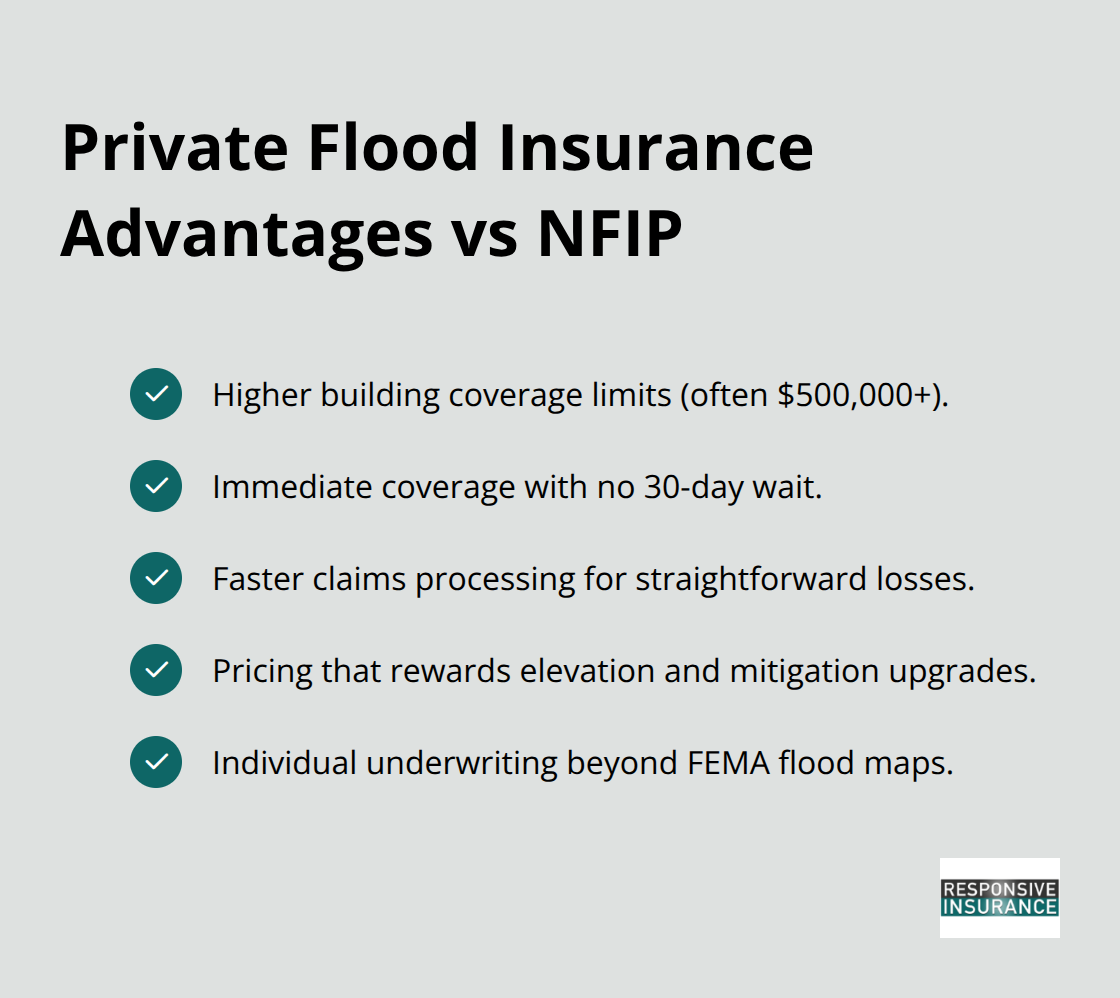

Private flood insurance has grown significantly in recent years, with the private market now covering approximately 1 million policies according to the American Property Casualty Insurance Association. Unlike NFIP’s one-size-fits-all approach, private insurers in Florida compete aggressively on coverage limits and pricing, which means Naples homeowners can find policies tailored to their actual property values. Private carriers typically offer building coverage up to $500,000 or higher, compared to NFIP’s $250,000 cap, and some specialize in protecting high-value homes where federal coverage falls drastically short. The underwriting process differs fundamentally-private insurers conduct individual property assessments using elevation data, construction details, and proximity to water sources rather than relying solely on FEMA flood maps.

Why Private Insurers Price Policies Differently

This detailed evaluation often results in lower premiums for elevated homes or properties with modern flood-resistant construction, whereas NFIP charges the same rates regardless of these protective features. Private policies also eliminate the 30-day waiting period that plagues NFIP applications, meaning coverage starts immediately when you need it most. The pricing structure for private flood insurance varies considerably between carriers, and this competition benefits Naples residents shopping around. Some private insurers use dynamic risk models that reward homeowners for specific flood mitigation measures like installing backflow preventers or elevating utilities, while NFIP ignores these improvements entirely.

Claims Processing and Availability Considerations

Claims processing through private insurers typically moves faster than federal programs, with many companies offering online claim filing and expedited adjustments for straightforward losses. However, private flood insurance isn’t universally available in all flood zones, and carriers may decline coverage or charge substantially higher rates for homes in very high-risk areas near waterfront properties. Your property’s location, value, and personal risk tolerance determine which option works best for your situation-not what sounds cheapest initially. Understanding these differences prepares you to evaluate how each option aligns with your specific needs before comparing the direct cost differences between NFIP and private policies.

How NFIP and Private Coverage Actually Compare in Real Dollars

Coverage Limits That Make a Real Difference

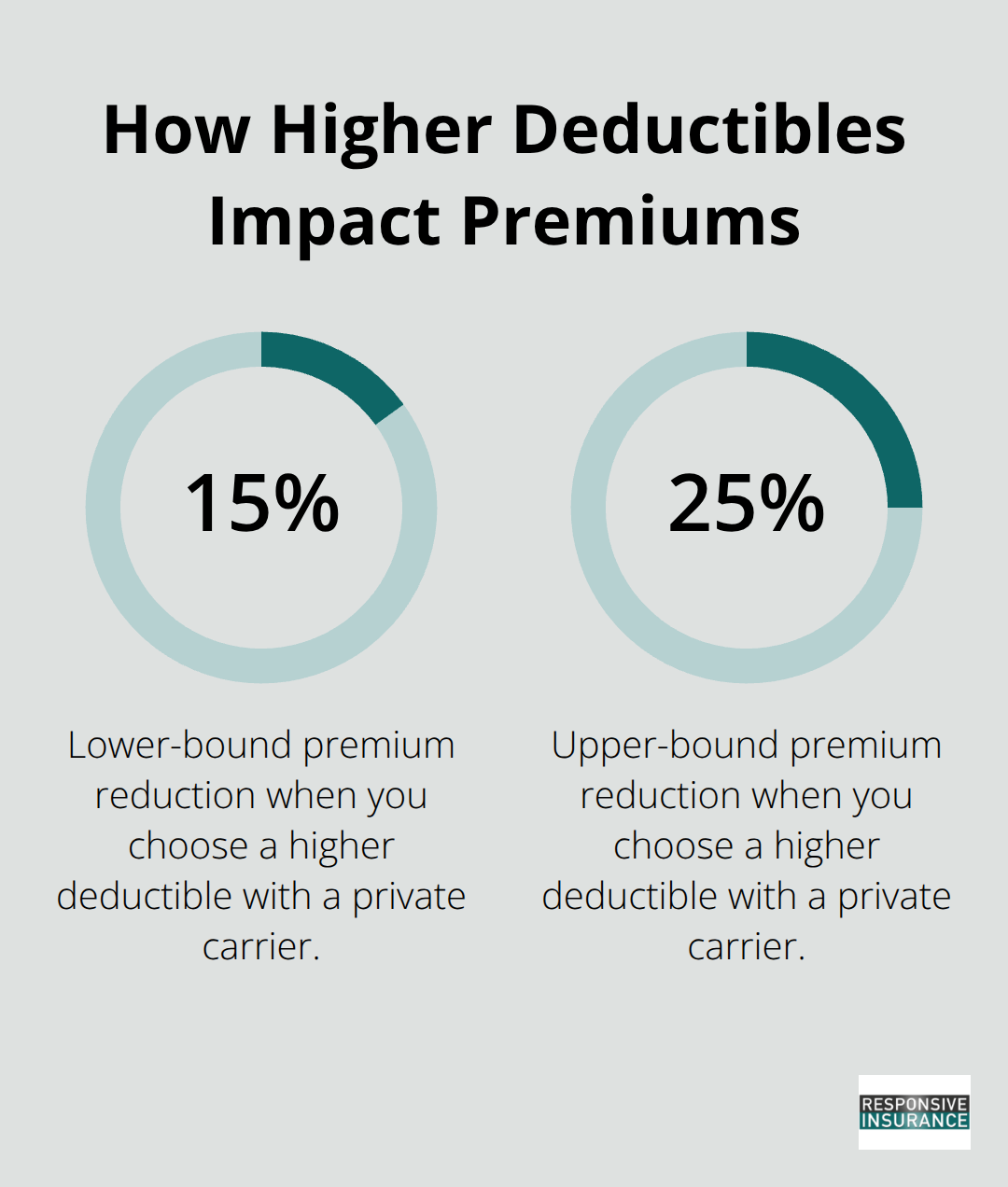

NFIP caps your building coverage at $250,000 and personal property at $100,000, while private insurers routinely offer $500,000 or more in building coverage with higher personal property limits. For Naples homeowners with properties valued above $400,000, this difference isn’t academic-it’s the gap between full protection and significant out-of-pocket losses. A $600,000 home sustaining $350,000 in flood damage would recover only $250,000 from NFIP, leaving a $100,000 shortfall that comes directly from your savings. Private policies also handle deductibles differently than federal coverage; NFIP deductibles range from $500 to $5,000 depending on your zone, while private carriers often allow you to select deductibles from $1,000 to $25,000 based on your risk tolerance and budget.

The tradeoff matters significantly. Choosing a higher deductible with a private carrier typically reduces your annual premium by 15 to 25 percent, making this a legitimate strategy for homeowners who can absorb smaller losses themselves.

How Pricing Models Reward Smart Homeowners

Pricing between these two options depends heavily on your property’s characteristics and location within Naples. NFIP uses a standardized formula based primarily on flood zone designation, meaning an elevated home with modern construction pays the same rate as an older, flood-prone structure in the same zone. Private insurers reward flood mitigation-homes elevated above base flood elevation, properties with backflow preventers, or those using flood-resistant materials can see premiums 20 to 40 percent lower than NFIP quotes for comparable coverage.

A Naples property in a high-risk zone might pay $1,500 annually with NFIP but qualify for $900 to $1,100 through private coverage if it has recent elevation improvements. This pricing advantage makes private insurance particularly attractive for homeowners who have invested in flood-resistant upgrades.

Speed Matters When You Need Coverage

Claims processing favors private carriers significantly; most process straightforward claims within two to four weeks, while NFIP claims average six to eight weeks. Private insurers also eliminate the 30-day waiting period, meaning coverage activates immediately rather than requiring you to wait a month before protection begins. This immediate activation proves critical when you’re closing on a property or need coverage before hurricane season arrives.

Availability Constraints in High-Risk Areas

The availability question cuts against private options for homes in very high-risk zones near waterfront areas, where carriers either decline coverage entirely or charge premiums approaching or exceeding NFIP rates. In these situations, federal coverage becomes your only practical choice. Your property’s location, value, and personal risk tolerance determine which option works best for your situation-not what sounds cheapest initially.

Final Thoughts

Your property’s value, location within Naples, and protection needs determine whether private flood insurance vs FEMA coverage serves you better. If your home exceeds $250,000 in value or you’ve invested in flood mitigation improvements, private insurance typically delivers superior coverage at competitive rates. NFIP remains your best option for very high-risk waterfront zones where private carriers decline coverage, or when you prioritize the lowest possible premiums.

Calculate your property’s actual replacement cost before selecting coverage limits, since most Naples homeowners underestimate what rebuilding would truly cost after a major flood. Request quotes from both NFIP and private carriers, as pricing varies dramatically based on your specific property characteristics and elevation. An elevated home with modern construction might save thousands annually through private coverage, while an older structure in a high-risk zone may find NFIP more accessible and affordable.

We at Responsive Insurance, Inc. work with multiple A-rated insurance companies to compare both NFIP and private flood insurance options for your situation. Contact Responsive Insurance, Inc. to review your current protection and explore whether adjusting your coverage makes sense for your home.