What to Know About Flood Insurance: Essential Insights for Florida Homeowners

Florida homeowners face flood risks that most people underestimate. Standard homeowners insurance won’t protect your property when water damage strikes, leaving you financially exposed.

At Responsive Insurance, Inc., we know what to know about flood insurance can mean the difference between recovery and financial hardship. This guide walks you through your coverage options and how to safeguard your home.

Understanding Flood Risk in Florida

Why Florida’s Geography Makes Flood Risk Unavoidable

Florida sits at a disadvantage when it comes to flood protection. The state’s average elevation is just six feet above sea level, with some areas barely above three feet. Water doesn’t need much help to overwhelm your property. According to the National Oceanic and Atmospheric Administration, Florida experiences more frequent nuisance flooding than any other state. Naples sits directly in this vulnerable zone, with both storm surge and heavy rainfall creating dual threats that homeowners can’t ignore.

How Flood Zones Determine Your Risk

The Federal Emergency Management Agency maps flood zones based on historical data and rainfall patterns, but these maps lag behind reality. A property in a lower-risk zone can still flood if your neighborhood has poor drainage or sits in a depression that collects water. FEMA updates its flood maps periodically, yet they don’t account for the rapid changes happening in Florida right now. Your home’s actual flood risk depends on elevation, proximity to water bodies, local drainage infrastructure, and how storm patterns have shifted over the past decade. Check your property’s elevation against local flood data and talk to neighbors about their recent flooding experiences rather than relying solely on zone designations.

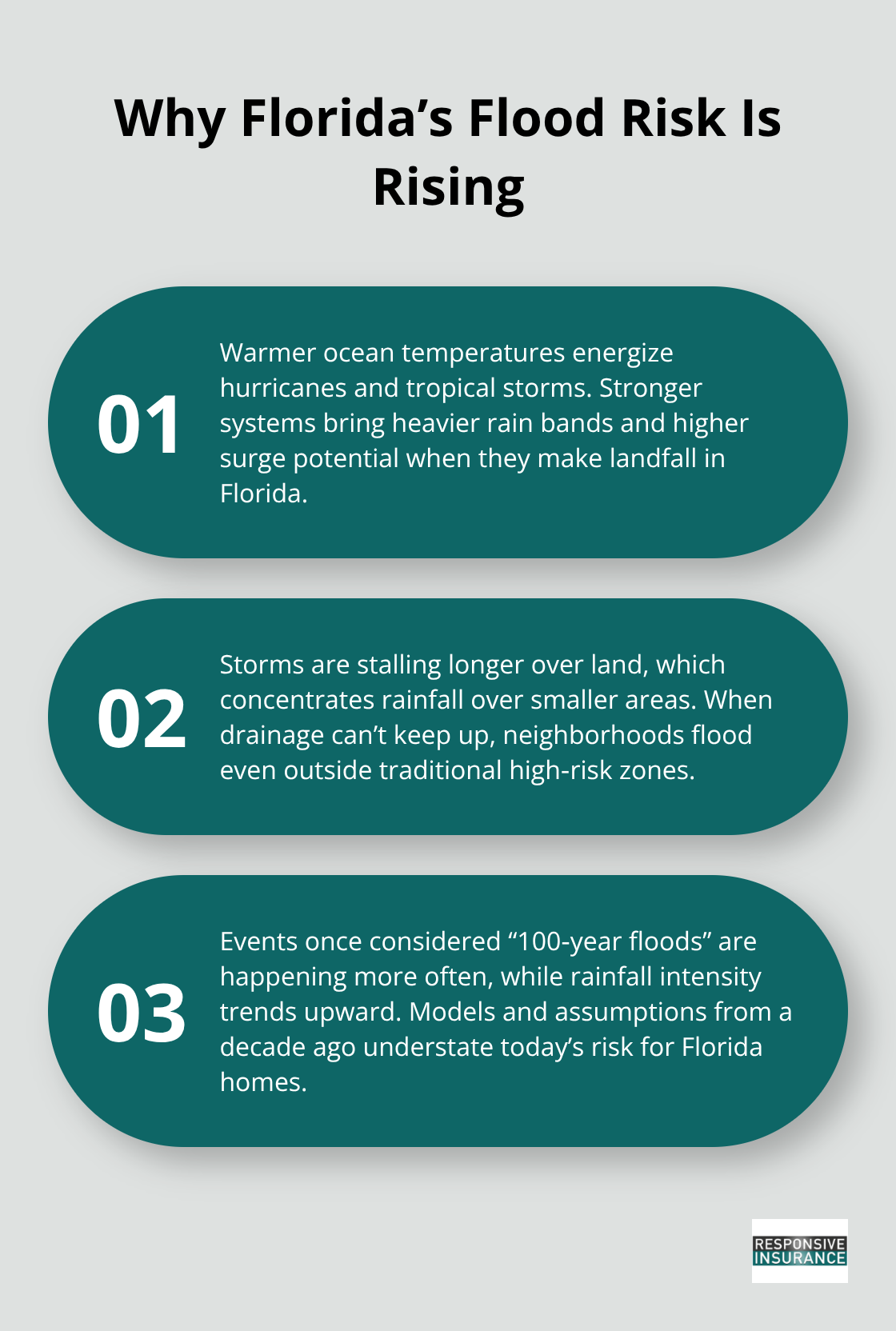

Climate Patterns Are Intensifying Flood Events

Warmer ocean temperatures make hurricanes and tropical storms more severe when they hit Florida. The National Hurricane Center data shows that storms stall longer over land, dumping more rain in concentrated areas. What used to be a 100-year flood event now happens more frequently, and rainfall intensity has increased dramatically. This trend means the flood risk your home faced five years ago is significantly lower than the risk it faces today. Insurance models that worked a decade ago are already outdated, which is why adequate coverage now protects you against tomorrow’s weather patterns.

These shifting conditions make understanding what your current homeowners policy actually covers more important than ever.

What Your Homeowners Policy Actually Leaves Unprotected

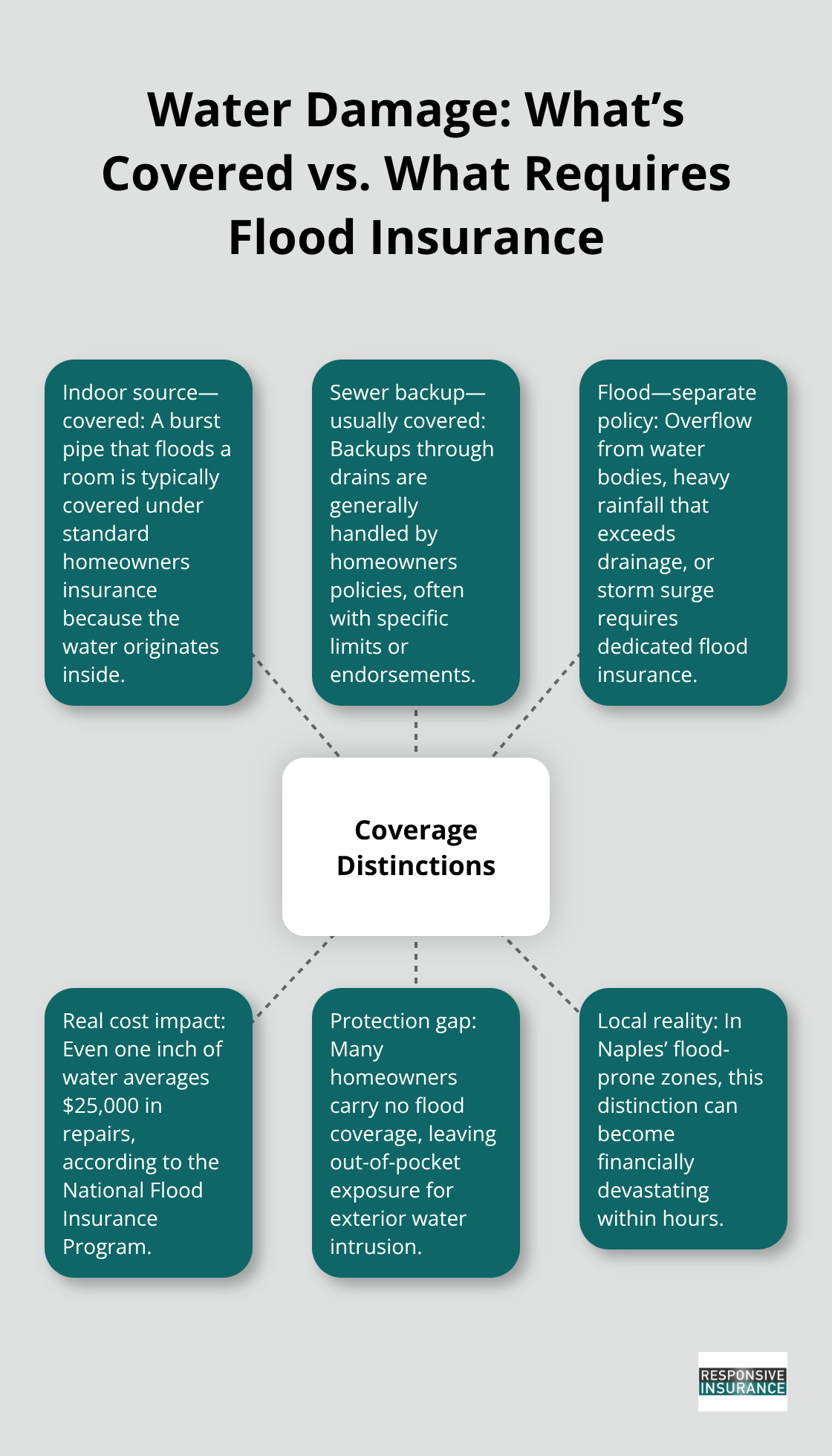

Your homeowners insurance stops the moment water enters your home from outside sources. Standard homeowners policies exclude flood damage entirely, which means a hurricane bringing storm surge, heavy rainfall causing neighborhood flooding, or a swollen river breaching your property line leaves you completely uninsured. This isn’t a loophole or oversight-it’s intentional policy language. Insurers classify flood as a separate peril requiring separate coverage because flood events affect large geographic areas simultaneously, creating catastrophic losses across thousands of policies at once. A single hurricane can cost the insurance industry billions of dollars, making it impossible for standard homeowners policies to absorb that risk. Homeowners who discover this gap after water damage realize too late that their six-figure policy doesn’t cover their five-figure loss.

The Distinction Between Water Damage Types Matters

Your policy distinguishes between water damage that originates inside your home and water that enters from outside. A burst pipe floods your basement under standard homeowners insurance because the water originates indoors. Sewage backs up through drains and falls under standard coverage as well. However, flood-defined as water overflowing from natural or artificial water bodies, heavy rainfall accumulating faster than drainage systems can handle, or storm surge pushing ocean water inland-requires separate flood insurance. This technical distinction creates confusion because homeowners assume water damage is water damage. The National Flood Insurance Program clarifies that even one inch of water in your home costs an average of $25,000 in repairs, yet most homeowners carry zero flood coverage.

Your property sits in a Naples flood zone where this distinction transforms from theoretical to devastating within hours.

Common Beliefs That Leave You Exposed

Many homeowners believe their homeowners insurance covers flood if they purchased a comprehensive or all-risk policy. It doesn’t. All-risk policies still exclude flood explicitly. Others assume that if their home sits outside a designated flood zone, they don’t need coverage. Federal data shows that 20 percent of flood insurance claims come from properties outside high-risk zones, meaning moderate-risk and low-risk areas flood regularly. Some homeowners think their mortgage lender will require flood insurance if they truly needed it. Lenders only mandate coverage for properties in high-risk zones, leaving owners in moderate-risk areas unprotected despite genuine exposure. The final misconception is that government disaster assistance will cover your losses. FEMA assistance comes as low-interest loans you must repay, not grants, and the maximum individual assistance amount sits far below typical home repair costs. Only flood insurance pays claims without repayment obligations, making it your actual safety net.

Understanding these coverage gaps explains why your next decision matters. Choosing the right flood insurance policy requires comparing your actual options and understanding what each one protects.

Selecting the Right Flood Insurance for Your Naples Home

NFIP Policies Versus Private Flood Insurance

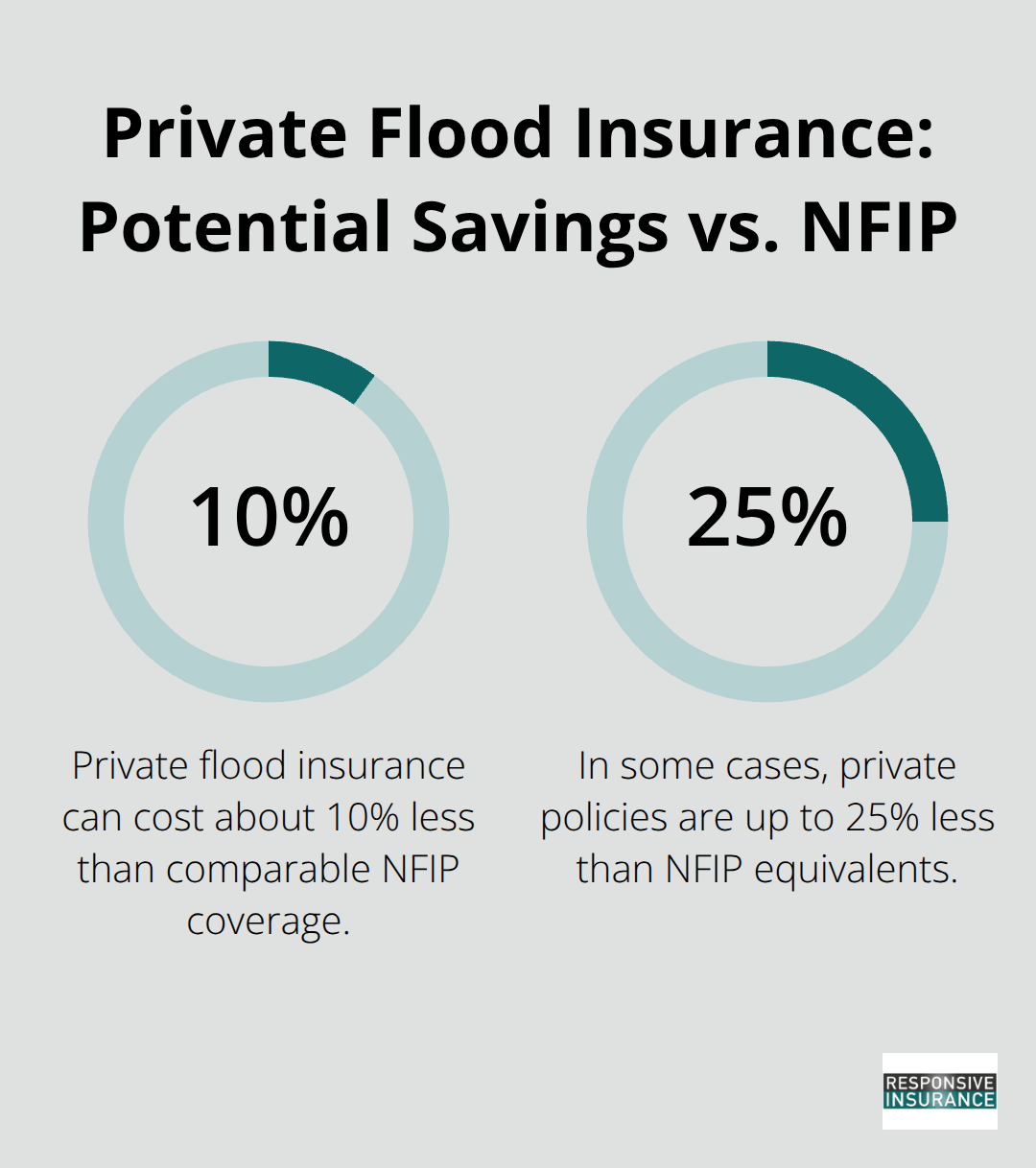

Flood insurance comes in two distinct forms, and the choice between them significantly impacts your protection and cost. The National Flood Insurance Program, or NFIP, is a federal program that sells policies through private insurance agents and covers up to $250,000 for your home’s structure and $100,000 for personal belongings. Private flood insurance policies, offered by non-government insurers, often provide higher coverage limits, sometimes reaching $500,000 or more for structural damage.

NFIP premiums vary based on your property’s flood risk zone and elevation. Private policies typically cost 10 to 25 percent less than NFIP equivalents for the same coverage, according to industry data from the American Insurance Association. However, lower cost does not always mean better protection.

NFIP policies come with consistent terms nationwide and are backed by the federal government, meaning claims get paid even if a catastrophic event bankrupts the insurer. Private insurers have no such guarantee, though most carry strong financial ratings.

Deductible Selection Shapes Your Out-of-Pocket Risk

Your deductible choice matters as much as the policy type. Standard NFIP deductibles start at $1,000, but you can select $2,500, $5,000, or $10,000 to lower your premium. A Naples homeowner with a $300,000 home might save $150 annually by choosing a $5,000 deductible instead of $1,000, but you must be able to afford that out-of-pocket amount when water enters your property.

Gathering Information for Accurate Quotes

Getting a flood insurance quote takes less than an hour when you have your property address and know your home’s replacement cost. Your elevation relative to the base flood elevation directly affects your rate, so have your flood zone information ready before requesting quotes. Most insurers ask about your home’s age, construction materials, and whether you have a basement or crawl space, since these factors influence flood damage severity.

Comparing Multiple Policies Side by Side

Request quotes from at least three different sources, including your current homeowners insurance agent, because many agents represent multiple carriers and can show you options you would not find shopping independently. Compare the total annual premium, deductible amounts, coverage limits for both structure and contents, and what additional endorsements cost if you want to raise your limits. Do not automatically choose the cheapest option without understanding what you sacrifice in coverage. A policy that costs $200 less annually but covers only $150,000 in structural damage instead of $250,000 leaves you exposed in a significant flood event.

Timing Your Purchase Before Hurricane Season Arrives

Purchase your flood insurance before you need it, since policies include a 30-day waiting period before they take effect in most cases. Hurricane season in Florida runs from June through November, meaning you should finalize your flood insurance decision by late spring at the latest to avoid gaps in coverage when storm activity peaks.

Final Thoughts

Florida homeowners who act now protect their families and finances from flood damage that standard homeowners insurance ignores. Water from external sources costs thousands to repair, your actual flood risk depends on elevation and drainage rather than zone designation alone, and comparing NFIP versus private policies takes hours rather than days. The 30-day waiting period means delays cost you protection during hurricane season, so purchasing coverage before June matters more than waiting for the perfect policy.

We at Responsive Insurance, Inc. work with multiple A-rated insurance companies to compare coverage and find the best fit for your specific situation. As an independent agency based in Naples, we understand the flood risks your property faces and can walk you through your options without pushing you toward one choice. Contact us to discuss your flood insurance needs and receive quotes that reflect your actual risk profile, or visit our flood insurance guide to learn more about your coverage options.

Hurricane season arrives in June, and policies include waiting periods that leave you unprotected if you postpone your decision. Your home’s value and your family’s security depend on having flood coverage in place before the next heavy rain or tropical system approaches Naples. Acting this month ensures you face the storm season with the protection you need.