Vacation Rental Insurance Florida: A Host’s Guide to Peace of Mind

Your vacation rental in Naples is an asset worth protecting. Standard homeowners insurance won’t cover guest-related incidents, leaving you exposed to significant liability claims.

We at Responsive Insurance, Inc. created this guide to help you understand the coverage gaps and find the right vacation rental insurance in Florida for your specific situation. The right policy protects your investment and gives you genuine peace of mind.

Why Your Homeowners Policy Won’t Protect Your Rental

Standard Homeowners Insurance Explicitly Excludes Rental Activity

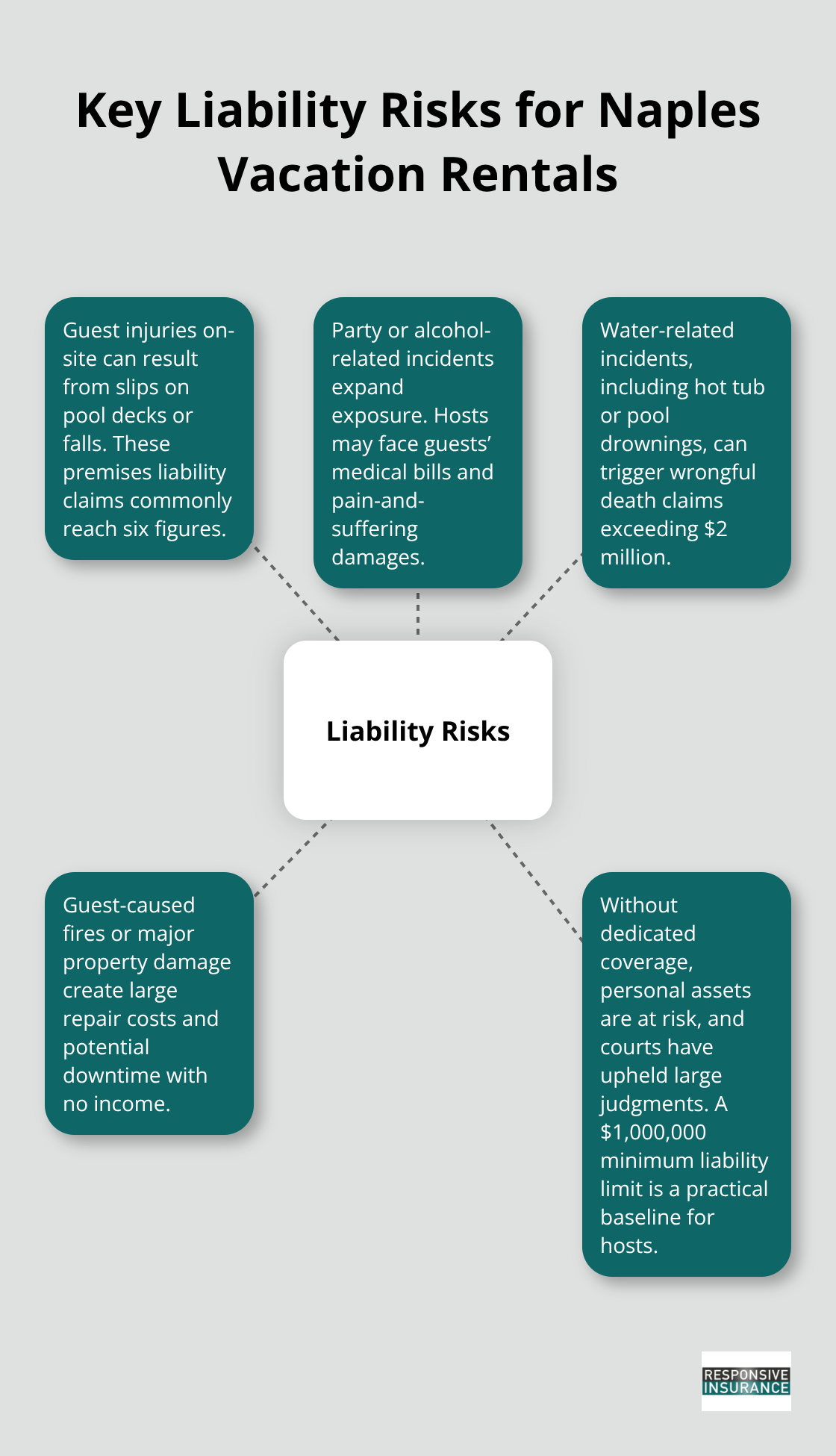

Standard homeowners insurance explicitly excludes short-term rental activity, and this isn’t a minor limitation-it’s a complete coverage denial. If a guest suffers an injury on your Naples property, damages your furniture, or causes a fire, your homeowners policy will reject the claim outright. Florida law treats short-term rentals (stays under 30 days) as commercial activity, not residential occupancy, which means your HO-3 policy simply doesn’t apply. Insurance companies make this distinction clear in policy language: coverage terminates the moment you rent the property to guests for fewer than 30 consecutive days. This gap matters enormously because guest-related liability claims in Florida regularly exceed $300,000, and a single incident could wipe out your entire rental income and savings.

The Real Liability Exposure You Face

Vacation rental hosts in Southwest Florida face liability risks that standard homeowners policies were never designed to handle. A guest slips on your pool deck and suffers a broken hip-that’s a premises liability claim potentially worth six figures. Another guest throws a party, alcohol is served, and someone leaves injured-your liability exposure includes the guest’s medical costs and pain and suffering damages. A third scenario: a guest’s child drowns in your hot tub, and the resulting wrongful death claim reaches $2 million or more. Florida courts have consistently upheld large judgments in these cases, and your personal assets are at risk if you lack adequate liability coverage. The practical minimum liability coverage recommended for Southwest Florida short-term rentals is $1,000,000, yet many hosts operate with zero dedicated coverage, relying on the false assumption that their homeowners policy will step in during a crisis.

Loss of Income Protection Addresses Your Biggest Financial Risk

Beyond liability, your biggest financial exposure is lost rental income during repairs or remediation. If a guest causes damage that requires your property to remain uninhabitable for two months, you lose $6,000 in monthly revenue while still paying your mortgage, property taxes, and maintenance costs. Standard homeowners policies don’t reimburse this lost income-they only cover the physical damage to the structure itself. Vacation rental insurance includes loss of income coverage that reimburses your actual revenue during the repair period, protecting your cash flow when you need it most. For Naples hosts earning $3,000 to $5,000 monthly during peak season, three months of repairs without income protection means $9,000 to $15,000 in uninsured losses.

What Dedicated Vacation Rental Policies Actually Cover

Dedicated vacation rental policies address the specific financial risks that come with operating a rental business, not just the property damage risks that homeowners policies cover. These policies protect against guest-caused theft, intentional damage, and liability claims that standard coverage excludes entirely. They also cover amenities like pools and hot tubs (which increase your liability exposure significantly) and provide coverage for bed bug or flea infestations that force you to cancel bookings. When you compare what you’re exposed to against what your current homeowners policy covers, the gaps become impossible to ignore. The next section walks you through the specific coverage options available to Naples hosts and how to evaluate which protections fit your rental operation.

Vacation Rental Insurance Coverage Options

Platform Protection Programs Leave Critical Gaps

Airbnb’s Host Protection and Vrbo’s AirCover sound comprehensive until you read the fine print. Airbnb’s Host Protection covers up to $1 million in liability but excludes guest-caused property damage, theft, and loss of income-the exact exposures that create financial disasters for Naples hosts. Vrbo’s AirCover similarly caps coverage at $1 million liability and excludes damage to your furnishings, guest theft, and revenue loss during repairs. These programs exist primarily to protect the platforms themselves, not your investment.

A guest steals your $8,000 television or damages your kitchen appliances, and you’re out the full amount because platform protection doesn’t cover guest-caused theft or intentional damage. A covered loss forces two months of repairs, costing you $8,000 in lost rental income, and again the platform coverage leaves you exposed. Experienced Naples hosts view platform protection as a starting point, not a complete solution.

Dedicated Vacation Rental Policies Fill Every Gap

Dedicated vacation rental insurance policies cover guest-caused damage and theft, from broken furniture to stolen electronics. These policies include loss of income coverage that reimburses your actual monthly revenue during repairs-critical protection when a single claim could eliminate three to six months of earnings. They cover bed bug and flea infestations that force booking cancellations, and squatter protection when a guest refuses to leave.

Liability coverage starts at $1 million as the practical minimum for Southwest Florida properties, though pools, hot tubs, or higher-value properties often require $2 million or more. Property and contents coverage use replacement cost valuation, meaning you receive enough to replace damaged items at current prices, not depreciated values. Proper Insurance, endorsed by Vrbo as a preferred provider and underwritten by Lloyd’s of London, offers this comprehensive protection across Florida including Naples and the surrounding coastal markets.

How Commercial General Liability Works for Rental Hosts

Commercial general liability coverage in a dedicated vacation rental policy applies to incidents involving guests whether they occur on your property or when guests use off-premises amenities you provide (such as beach equipment or recreational gear). This distinction matters because standard homeowners liability stops at your property line, leaving you exposed for guest injuries that occur away from the house itself.

The underwriting process takes your specific property type, guest volume, and local exposure into account-a beachfront property faces different wind and flood risks than a downtown Naples apartment, and your policy should reflect those differences. Multiple A-rated carriers offer vacation rental policies with varying coverage limits and exclusions, so comparing quotes across at least three providers helps you identify which policy matches your actual exposure and budget.

Choosing Between Coverage Options

Your next step involves assessing your specific rental operation to determine which coverage limits and additional protections fit your property and guest volume.

How Much Coverage Do You Actually Need

Calculate Your Property’s True Replacement Value

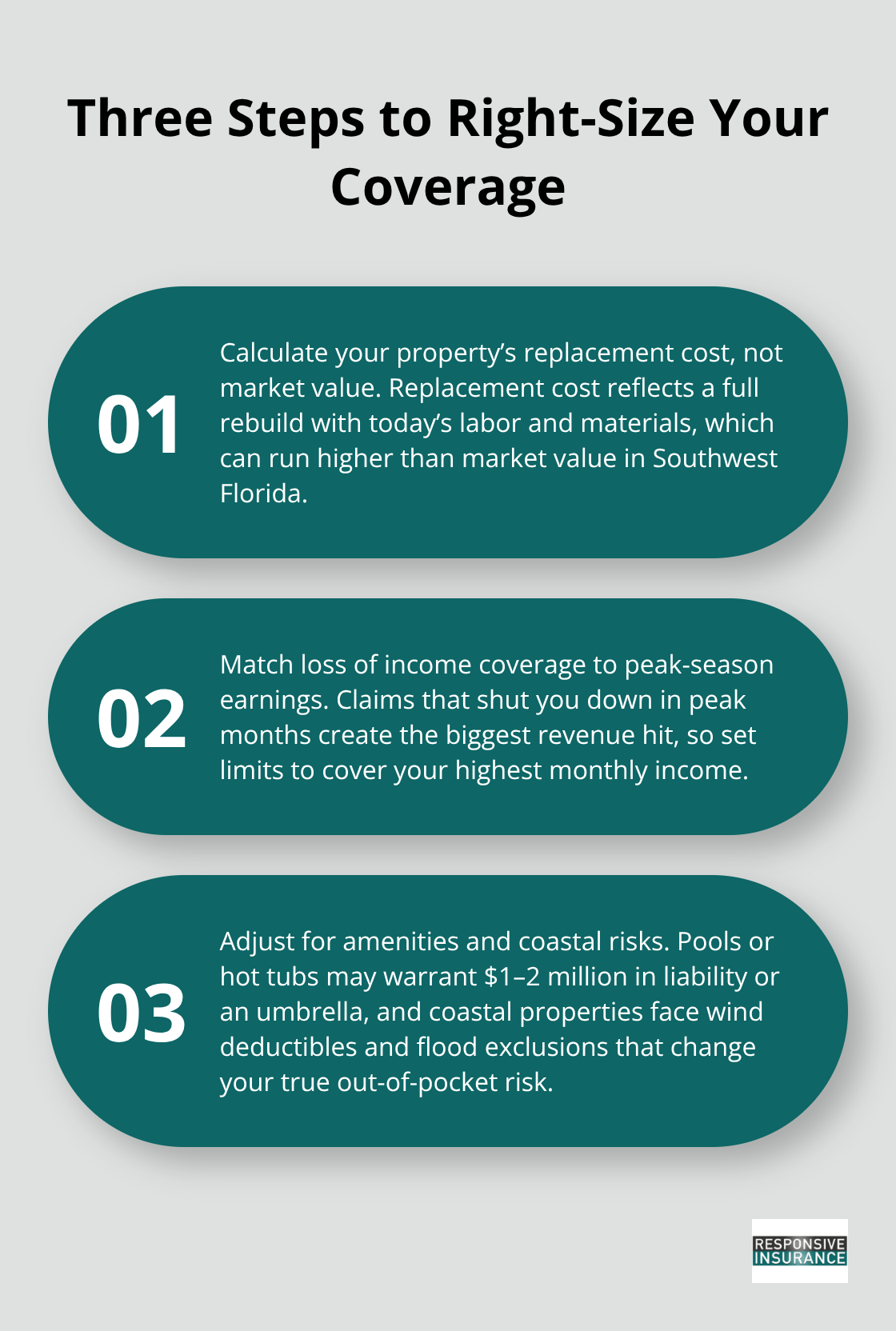

Determining the right coverage limits for your Naples vacation rental depends on three concrete factors: your property’s replacement value, your monthly rental income, and the specific amenities that increase liability exposure. A beachfront cottage worth $800,000 with a pool and hot tub faces dramatically different risks than a downtown apartment worth $300,000 without amenities, yet many hosts apply generic coverage limits that don’t match their actual exposure. Start by calculating your property’s replacement cost, not its market value. Replacement cost reflects what it would cost to rebuild from scratch using current labor and materials, which typically runs 10 to 15 percent higher than market value in Southwest Florida due to construction demand and coastal building codes.

Match Loss of Income Coverage to Your Peak Season Earnings

Document your actual monthly rental income during peak season and off-season separately. If you earn $4,500 monthly from June through August and $2,500 from September through May, your loss of income coverage should reflect peak season earnings since that’s when a claim hits your finances hardest. A covered loss that forces two months of repairs during peak season costs you $9,000 in lost revenue, while the same loss during off-season costs only $5,000. Your policy’s loss of income limit should cover your actual peak season earnings, not an average that underestimates your real exposure.

Account for Amenities That Multiply Your Liability Risk

Inventory your amenities carefully. Pools increase liability exposure substantially, and Florida courts have awarded damages exceeding $2 million in drowning cases involving vacation rentals. Hot tubs, trampolines, and other guest amenities create additional exposure that standard homeowners policies exclude entirely. A practical starting point for liability coverage is $1,000,000 minimum, but properties with pools, hot tubs, or guest volumes exceeding 30 bookings annually should carry $2,000,000 or consider an umbrella policy for additional protection.

Understand Wind Deductibles and Coastal Risk Factors

Wind deductibles for hurricane coverage vary significantly by coastal location within Southwest Florida, and this affects your actual out-of-pocket cost during a claim. Properties in high-risk coastal zones often face 2 to 5 percent deductibles on wind damage, meaning a $500,000 property could require a $10,000 to $25,000 deductible before coverage applies. When comparing quotes from multiple carriers, focus on what’s excluded, not just the premium price. A policy that caps loss of income at $5,000 monthly is worthless if your actual revenue is $8,000. Flood insurance deserves separate attention since standard vacation rental policies exclude flood damage. The National Flood Insurance Program covers properties in flood zones, though private flood carriers sometimes offer better rates and coverage limits for higher-value properties.

Compare Quotes Across Multiple A-Rated Carriers

Request quotes from at least three A-rated carriers because premium differences for identical coverage can exceed 30 percent, and each carrier weights coastal exposure and property-specific risks differently. Request quotes that specify coverage limits, deductibles, loss of income caps, and exclusions side-by-side so you can compare what you’re actually purchasing rather than focusing on price alone. An independent agent familiar with Naples rental properties can identify coverage gaps that online quote tools miss-for example, bed bug protection or squatter liability coverage that protects you when a guest refuses to leave and demands eviction proceedings.

Final Thoughts

Your Naples vacation rental represents a significant financial investment that demands protection beyond what standard homeowners policies provide. The coverage gaps are real, the liability exposure is substantial, and operating without dedicated vacation rental insurance Florida exposes you to devastating financial consequences. A single guest injury claim or theft incident can eliminate years of rental income and threaten your personal assets if you lack adequate liability protection.

Start by gathering your property details: replacement cost, monthly rental income during peak and off-season, amenities like pools or hot tubs, and your current homeowners policy documents. Request quotes from at least three A-rated carriers that specialize in vacation rental coverage, comparing liability limits, loss of income caps, and specific exclusions rather than focusing solely on premium price. Identify any coverage gaps between what platform protection programs offer and what your actual exposure demands.

An independent agent familiar with Naples rental properties understands Southwest Florida’s specific risks in ways national carriers don’t (coastal wind exposure, hurricane deductibles, flood zone requirements, and local rental registration ordinances all affect your coverage needs). Contact Responsive Insurance, Inc. to review your current coverage and explore dedicated vacation rental insurance options tailored to your specific property and guest volume. Your investment deserves protection from someone who knows the local market and your actual exposure.