Naples Homeowners Quotes: Compare, Save, and Protect

Homeowners in Naples face unique insurance challenges, from hurricane exposure to rising property values. Getting accurate Naples homeowners quotes is the first step toward protecting your investment.

At Responsive Insurance, Inc., we help you understand what coverage you actually need and where you can save money. This guide walks you through comparing options, avoiding costly mistakes, and securing the right protection for your home.

What Coverage Do You Actually Need in Naples

Naples homeowners must understand that standard homeowners insurance splits into several distinct coverage types, and most people remain underinsured because they don’t grasp how these pieces work together. Dwelling coverage rebuilds your home’s structure, but here’s the critical part: it must reflect your home’s actual replacement cost, not its market value. A Naples home worth $500,000 might cost $600,000 to rebuild due to labor shortages and material costs in Florida. According to Bankrate data, Naples homeowners pay roughly $6,442 annually for a $300,000 dwelling policy, which works out to about $537 per month. Personal property coverage protects your belongings inside the home, typically capped at 50–70% of your dwelling limit. Liability coverage shields you if someone gets injured on your property and sues, and this matters enormously in Florida where litigation is common. Loss of use coverage pays your living expenses if your home becomes uninhabitable after a covered loss. Most Naples policies exclude wind and flood damage entirely, which is a massive problem given hurricane exposure. Wind coverage often requires a separate windstorm policy or hurricane deductible of around 2% of your dwelling coverage instead of a fixed dollar amount. Flood insurance is absolutely separate and not included in any standard homeowners policy, yet much of Naples sits in FEMA-designated flood zones where it’s mandatory if you have a federally backed mortgage.

How Your Premium Gets Calculated

Your premium hinges on replacement cost first and foremost. Moving from $100,000 to $500,000 in dwelling coverage jumps your annual premium from roughly $851 to $4,193, according to data analyzed across Naples ZIP codes. Home age matters tremendously because properties built after 2001 meet updated construction codes and cost less to insure, while homes over 20 years old typically require a 4-point inspection before qualifying for coverage. Your deductible choice directly impacts price: raising it from $500 to $1,000 saves approximately $1,000 annually on Naples policies. Wind mitigation improvements like hurricane straps, hip roofs, and impact-resistant windows can reduce premiums by 15–45% depending on what you upgrade. Location within Naples creates significant variation-34102 averages $2,582 yearly while 34109 averages $2,434, reflecting local flood risk and rebuild costs. Claims history and credit score shape rates substantially, with clean records and good credit yielding lower premiums. Collier County has seen 42% premium increases from 2022 to 2024, so rates are climbing faster in Naples than many other Florida markets.

What Happens When You File a Claim

When you file a claim, the insurer sends an adjuster to inspect damage and verify it’s covered under your specific policy language. This is where coverage gaps hurt: if your roof failed due to age rather than a covered peril, the claim gets denied. Replacement cost coverage rebuilds your home at today’s prices with no depreciation, while actual cash value depreciates your home’s value, leaving you short when rebuilding. Naples homeowners should demand replacement cost coverage because actual cash value leaves you vulnerable to massive out-of-pocket expenses. If your home sits in a flood zone and you lack flood insurance, you remain entirely unprotected-federal disaster aid is not automatic and typically arrives as loans, not grants. Wind mitigation improvements documented with certificates can yield discounts when you renew, so you should keep records of upgrades. The waiting period for flood coverage is 30 days after purchase, so you cannot wait for a storm forecast to buy protection.

Why Shopping Around Matters More Than You Think

Most Naples homeowners accept the first quote they receive, which costs them thousands over time. Rates vary dramatically across carriers: State Farm averages about $2,016 yearly in Naples while Citizens Property Insurance costs about $6,281 for the same coverage (roughly 211% more). Tower Hill stands out with very low base rates around $709 annually, though you’ll want to verify that coverage meets your actual needs. Universal Property offers relatively affordable options at about $3,202 yearly and includes a rare private flood endorsement up to $5 million. The difference between the cheapest and most expensive option for identical coverage can exceed $5,000 annually, making comparison shopping non-negotiable. Bundling homeowners with auto, flood, or umbrella coverage typically yields multi-policy discounts of 10–25%, so you should ask each carrier about these savings. Local agents can uncover discounts not visible on national sites, and an independent Naples-based agency can compare multiple carriers in one conversation.

How to Get the Best Naples Quote Without Wasting Time

The price difference between carriers in Naples is so extreme that skipping comparison shopping costs you thousands of dollars. State Farm quotes at roughly $2,016 annually while Citizens Property Insurance charges about $6,281 for identical coverage, meaning one decision could save or cost you $5,000+ per year. Tower Hill’s base rates hover around $709 yearly, yet most homeowners never even request a quote from them because they lack visibility on national insurance sites. This is the reality: the first quote you accept is almost certainly not your best option. As an independent agency based in Naples, Responsive Insurance, Inc. works with multiple A-rated insurance companies, which allows us to show you the actual range of pricing available in Naples rather than forcing you to accept whatever one carrier offers. The variation exists because insurers price risk differently based on their claims experience, financial models, and appetite for coastal Florida properties. Some carriers have exited Florida entirely over the past two years due to hurricane losses, while others expanded aggressively and now offer competitive rates. This market volatility means your neighbor’s renewal rate tells you nothing about what you should pay.

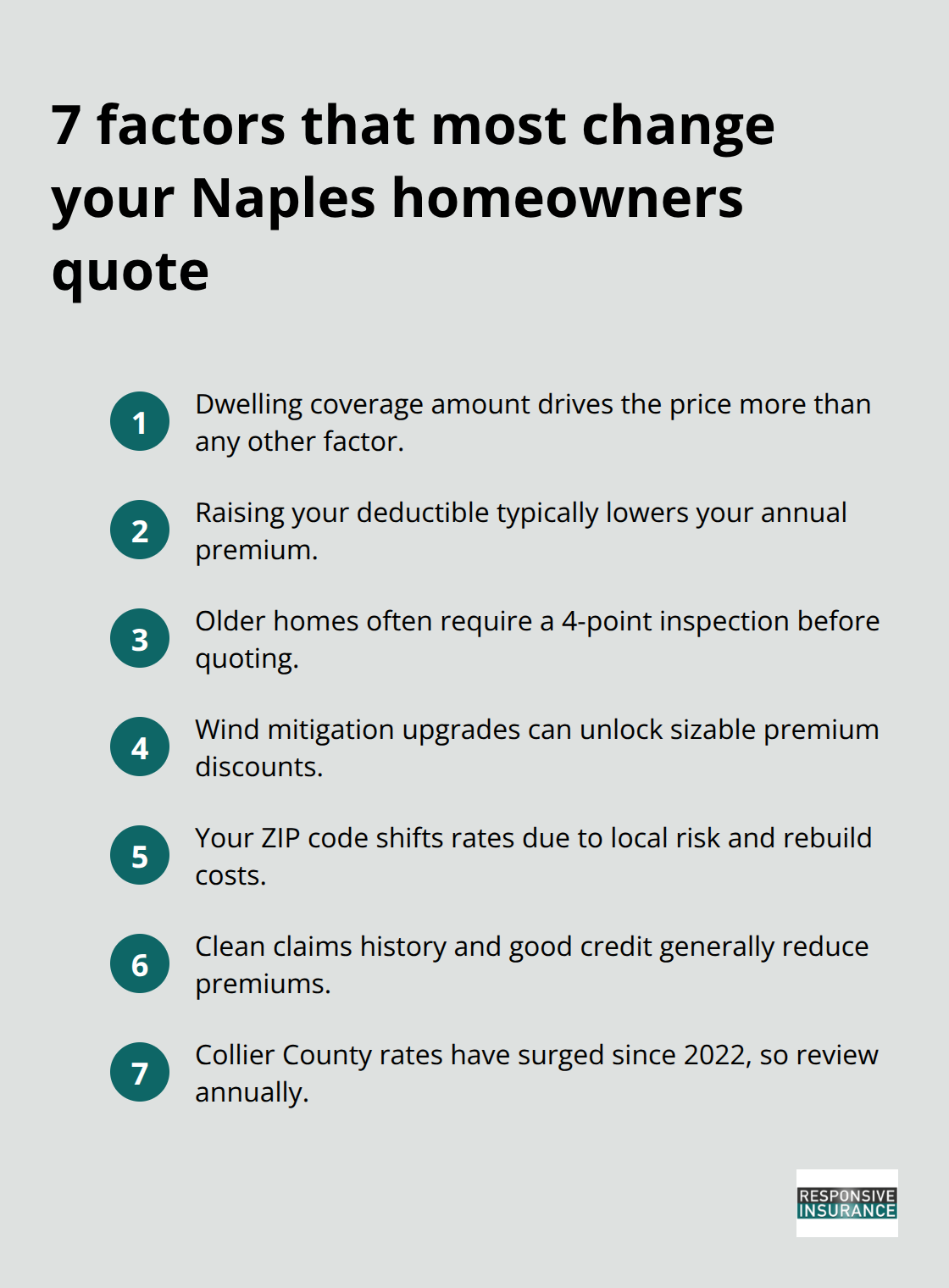

What Changes Your Quote Most Dramatically

Dwelling coverage amount dominates your premium calculation more than any other factor. The difference between $100,000 and $500,000 in dwelling coverage is roughly $3,342 annually according to Naples ZIP code analysis, so you cannot skip this decision. Your deductible choice ranks second in impact: moving from $500 to $1,000 saves approximately $1,000 per year, while jumping to $2,500 cuts another 5–20% off your premium. Home age determines whether you can even qualify for certain carriers, and homes over 20 years old require mandatory 4-point inspections that can delay quotes by weeks.

Wind mitigation improvements offer the fastest payback of any home upgrade because homeowners report savings of 20%, 30%, or even higher on their wind portion of their premium, and a single wind mitigation inspection often pays for itself within one year through premium reductions. Your claims history and credit score operate as permanent rate factors that you cannot change immediately, though improving credit over time does eventually lower premiums. Location within Naples matters more than most homeowners realize: ZIP code 34102 averages $2,582 yearly while 34109 averages $2,434, a difference driven purely by localized flood risk and rebuild costs. Collier County has absorbed a 42% premium increase from 2022 to 2024, so whatever you paid two years ago no longer reflects current market rates.

Getting Quotes That Actually Compare Apples to Apples

Online quote tools provide initial estimates, but they often exclude details that change your actual premium by hundreds of dollars. Progressive and other digital platforms offer quote tools, yet many Florida carriers do not provide online quotes and require agent involvement, which means you cannot complete a full comparison without calling local agencies. Bundling homeowners with auto, flood, or umbrella coverage typically yields 10–25% discounts across multiple carriers, but you must ask each insurer about their specific bundling savings because they vary wildly. An independent Naples-based agency can access multiple carriers in a single conversation and pull quotes with identical coverage parameters, which saves you hours of phone calls and ensures you actually compare the same thing. Universal Property includes a rare private flood endorsement up to $5 million within their homeowners policy, while most carriers force you to purchase separate NFIP flood coverage that caps at $250,000 for dwelling, so this detail alone could justify choosing one carrier over another depending on your flood risk. When you request quotes, ask each carrier explicitly about wind coverage, whether a hurricane deductible applies, and what their replacement cost definition includes, because these details shift your actual protection significantly.

Avoiding the Replacement Cost Trap

Do not accept a quote without confirming whether it includes replacement cost coverage or actual cash value, as this difference alone can cost you tens of thousands during a major claim. Replacement cost coverage rebuilds your home at today’s prices with no depreciation applied, while actual cash value depreciates your home’s value and leaves you short when rebuilding. A Naples home worth $500,000 might cost $600,000 to rebuild due to labor shortages and material costs in Florida, so your coverage must reflect actual reconstruction expenses rather than market value. Most homeowners discover this gap only after filing a claim, which is far too late to correct the problem. Insurers sometimes offer both options at different price points, and you must actively select replacement cost rather than accepting whatever default the quote tool presents. This single choice determines whether you can actually rebuild your home or face a devastating financial shortfall after a major loss.

Moving Forward With Your Comparison

The next step involves identifying which carriers serve your specific Naples ZIP code and gathering quotes with identical dwelling limits, deductibles, and coverage types. This approach reveals the true price variation available to you and exposes which carriers offer the best value for your particular situation.

Three Costly Mistakes That Drain Your Naples Insurance Budget

Naples homeowners consistently make three decisions that cost them thousands of dollars over time, and most never realize the damage until after a major loss. These mistakes stem from misunderstanding how coverage works, not from carelessness, but the financial consequences remain severe regardless of intent.

Underinsuring Your Home Based on Market Value

The first mistake involves basing your dwelling coverage on market value instead of actual replacement cost coverage. A Naples home worth $500,000 might cost $600,000 to rebuild because Florida labor shortages and material costs exceed what you paid for the property years ago. According to Bankrate data, Naples homeowners pay roughly $6,442 annually for a $300,000 dwelling policy, yet many choose lower coverage limits to save money on premiums, then face catastrophic shortfalls when rebuilding.

The math seems simple: lower coverage means lower premiums. This calculation ignores the reality that replacement cost coverage is not optional in Naples given hurricane exposure and construction costs. You must calculate your actual reconstruction expense by consulting local contractors or using replacement cost estimator tools available through your agent, then match your dwelling limit to that figure. Underinsurance by even $100,000 can leave you unable to rebuild, forcing you to accept a smaller home or relocate entirely after a major loss.

Ignoring Flood Coverage in High-Risk Areas

The second mistake involves ignoring flood coverage because your standard homeowners policy excludes all flood damage entirely. Much of Naples sits in FEMA-designated flood zones, yet homeowners either skip separate flood insurance or purchase the minimum required by their lender rather than adequate coverage for their actual property value.

The National Flood Insurance Program caps dwelling coverage at $250,000 for single-family homes, which means homeowners with higher-value properties face substantial uninsured exposure unless they purchase private flood endorsements that extend up to $5 million. Universal Property offers private flood coverage up to $5 million within their homeowners policies, giving you options that standard NFIP policies cannot match. Without flood coverage, federal disaster aid is not automatic and typically arrives as loans rather than grants, leaving you responsible for financing your own reconstruction.

Failing to Review Your Policy Annually

The third mistake is failing to review your policy annually because rates in Collier County have increased 42% from 2022 to 2024, and your current premium likely no longer reflects market conditions. Many homeowners keep the same policy for five or ten years without shopping, missing opportunities to save hundreds annually through carrier switches or newly available discounts.

Wind mitigation improvements you completed last year might qualify for discounts you never claimed, and your home improvements could justify lower rates from carriers focused on updated construction. Getting fresh quotes every one to two years takes a few hours but typically saves $1,000 or more annually, making this the fastest way to recover money you are currently overpaying. Collier County’s rapid rate increases mean that what you paid two years ago no longer reflects current market conditions, and carriers adjust their pricing based on claims experience and competitive positioning.

Final Thoughts

Naples homeowners quotes reveal a stark reality: the difference between your cheapest and most expensive option often exceeds $5,000 annually for identical coverage. This gap exists because insurers price risk differently, and most homeowners never discover their actual savings potential because they accept the first quote without comparison shopping. Replacement cost must match your actual reconstruction expense, not your home’s market value, since a $500,000 property might cost $600,000 to rebuild in Florida due to labor shortages and material costs.

Flood coverage demands immediate attention because much of Naples sits in FEMA-designated flood zones where standard homeowners policies provide zero protection. The National Flood Insurance Program caps dwelling coverage at $250,000, forcing higher-value properties to seek private flood endorsements that extend up to $5 million. Without separate flood insurance, federal disaster aid remains uncertain and typically arrives as loans rather than grants, leaving you responsible for financing your own recovery.

Your next step involves gathering Naples homeowners quotes from multiple carriers with identical coverage parameters so you actually compare apples to apples. Responsive Insurance, Inc. can access multiple A-rated insurance companies in a single conversation, eliminating hours of phone calls and ensuring you see the true range of pricing available in your specific ZIP code. Contact a local agent today to start comparing your options and protecting your investment.