Best Homeowners Insurance Florida: How to Choose a Policy You Can Trust

Finding the best homeowners insurance in Florida requires understanding what actually protects your home and wallet. Hurricane season, coastal weather, and mortgage lender requirements make Florida homeowners face unique challenges that standard policies often miss.

At Responsive Insurance, Inc., we help Naples homeowners cut through the confusion and find coverage that matches their real needs. This guide walks you through coverage types, policy comparisons, and the discounts that actually save money.

Why Homeowners Insurance Matters in Florida

Hurricane Season and Year-Round Weather Threats

Florida’s hurricane season runs officially from June through November, but the financial threat extends year-round. Wind and hail claims affect about 1 in 40 insured homes annually in Florida, with average payouts around $11,000 according to the Insurance Information Institute. Water damage claims hit nearly 1 in 50 insured homes each year, often from storm surge, heavy rain, or burst pipes-and standard homeowners policies frequently exclude flood damage entirely. This gap between what homeowners think they’re covered for and what they actually are protected against creates dangerous exposure across the state.

Mortgage Lenders Require Proof of Coverage

If you carry a mortgage, your lender will not close on your home without proof of homeowners insurance. This is not optional. Most mortgage lenders demand replacement cost coverage, meaning your policy must cover the full cost to rebuild your home from scratch. Lenders also set minimum liability coverage requirements, typically $100,000 or more. Skipping insurance or letting a policy lapse puts you in violation of your mortgage agreement and opens you to foreclosure risk. The cost of compliance-roughly $2,017 annually for a standard Florida policy according to U.S. News & World Report-is far cheaper than the financial catastrophe of an uninsured home damaged by a hurricane or fire.

Claims Happen More Often Than You Think

In the five-year period from 2019 to 2023, 5.6 percent of insured homes filed a homeowners claim, showing that claims strike more frequently than many people realize. Fire and lightning claims average around $80,000 per claim-amounts most homeowners cannot absorb without insurance. A single hurricane can destroy or severely damage your home, vehicles, and personal property simultaneously. Without adequate coverage, you face the choice of going into debt, losing your home, or both.

Rising Premiums Reflect Real Risk

Florida’s rising premiums reflect the state’s genuine risk profile. The Consumer Federation of America reported in 2025 that Florida homeowners experienced average premium increases of about $2,118 from 2021 to 2024, the highest in the nation. This increase frustrates homeowners, but it underscores how seriously insurers view Florida’s exposure to wind, water, and weather-related damage. Adequate insurance is not a luxury expense-it is the financial foundation that keeps you solvent when disaster strikes. Understanding what your policy covers and what it excludes determines whether you have real protection or dangerous gaps in your coverage.

Coverage Types and What You Actually Need

Dwelling Coverage and Replacement Cost

Your homeowners policy consists of several distinct coverage types, and understanding what each one does is the difference between having real protection and discovering gaps when you file a claim. Dwelling coverage pays to rebuild your home structure itself if a covered peril like wind, fire, or hail damages it. This is the foundation of your policy, and it must reflect your home’s actual replacement cost valuation for homeowners insurance, not its market value. A home worth $400,000 on the market might cost $450,000 to rebuild from scratch due to labor and material costs, so work with your agent to calculate replacement cost accurately.

Personal Property and High-Value Items

Personal property coverage protects your belongings inside the home-furniture, electronics, clothing, appliances-up to a limit set in your policy, typically 50 to 70 percent of your dwelling coverage amount. If you own high-value items like jewelry, art, or collectibles, standard personal property coverage often caps payouts at $2,500 per item, which means a $5,000 watch or painting gets paid at only half its value. You can add scheduled personal property coverage to insure specific valuable items at their full replacement cost, and this costs far less than you might expect.

Liability and Medical Payments Protection

Liability coverage protects you if someone is injured on your property and sues you for medical bills or damages; most policies offer $100,000 to $300,000 in liability protection, though Florida’s litigation environment makes higher limits worth serious consideration. Medical payments coverage is separate from liability and pays small medical expenses for guests injured on your property, regardless of fault, typically up to $5,000 per person.

Naples-Specific Coverage Considerations

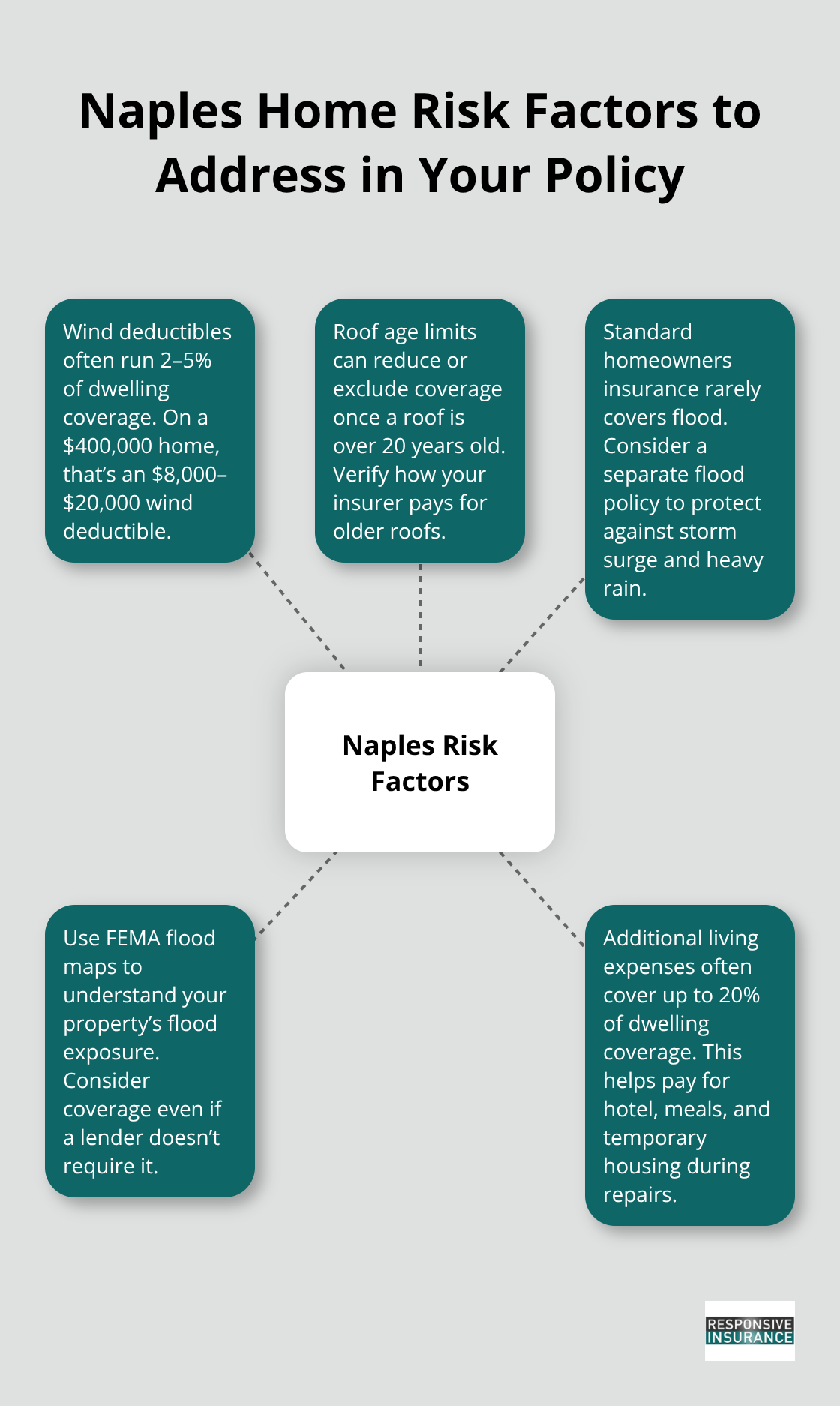

The coverage choices you make must match Naples’ actual risk profile, not a generic Florida template. Wind and hail deductibles in coastal areas often run 2 to 5 percent of your dwelling coverage instead of a flat dollar amount, meaning a $400,000 home could have an $8,000 to $20,000 deductible for wind damage alone. Some policies exclude or limit coverage for roof damage if your roof is over 20 years old, so verify your roof’s age and confirm what the insurer will actually pay.

Flood damage is almost never covered by standard homeowners insurance in Florida, which means a storm surge event, heavy downpour, or drainage backup leaves you completely unprotected unless you buy a separate flood policy. Naples homeowners should review their flood risk through FEMA’s flood maps and seriously consider flood coverage even if your lender doesn’t require it, given the rising severity of rainfall events. Additional living expenses coverage pays for hotel, meals, and temporary housing if a covered peril makes your home unlivable-typically covering up to 20 percent of your dwelling coverage-and this is critical in Florida where repairs take months.

Exclusions Matter More Than Inclusions

When comparing policies, focus on what each insurer excludes rather than what they include, because exclusions determine whether you have protection or exposure when disaster strikes. These gaps in coverage shape your actual financial risk far more than the marketing language insurers use to describe what they do cover.

How to Compare Policies and Find the Right Fit

Request Quotes from Multiple Insurers

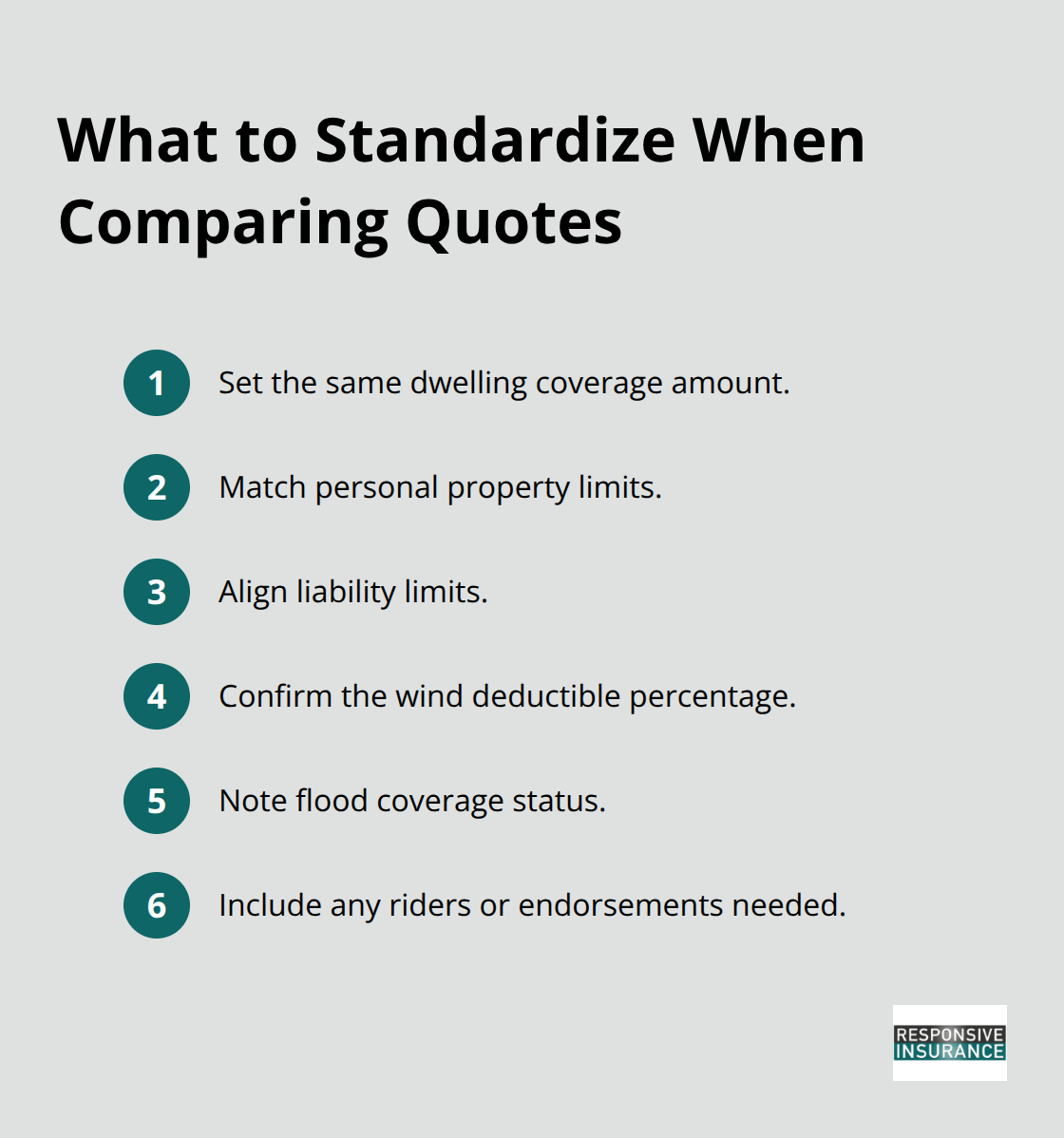

Multiple quotes from different insurers reveal the true cost of coverage in Naples, yet most homeowners skip this step and overpay for years. State Farm offers the cheapest sample Florida homeowners premium at about $2,017 per year according to U.S. News & World Report, but Florida Peninsula might quote $2,792 for identical coverage, while Homeowners Choice could come in at $3,802 annually-all for the same $400,000 dwelling limit and $100,000 liability. The gap between the lowest and highest quote often exceeds $1,500 per year, which means skipping the comparison process costs thousands in unnecessary premiums. Request quotes from at least three different insurers, and specify exactly what you want compared: dwelling coverage amount, personal property limits, liability limits, wind deductible percentage, flood coverage status, and any riders you need. Online quote tools work for some carriers, but State Farm and other major insurers in Florida require you to contact a local agent directly, so plan for phone calls rather than instant results.

When you receive each quote, verify that the coverage limits and deductibles match across all quotes so you compare apples to apples and not accidentally compare a $300,000 policy to a $400,000 policy.

Choose Deductibles That Match Your Financial Reality

Deductibles and coverage limits determine whether you pay too much for protection you don’t need or face dangerous gaps when you file a claim. A $1,000 deductible versus a $2,500 deductible might save $200 to $400 annually in premiums, but only select the higher deductible if you can actually afford to pay it out of pocket when a claim occurs-most homeowners cannot. Wind deductibles in Naples operate separately from your standard deductible and often run 2 to 5 percent of dwelling coverage, meaning a $400,000 home could require you to pay $8,000 to $20,000 out of pocket for wind damage alone. This separate wind deductible applies specifically to hurricane and wind-related damage, so understand how it functions before you commit to a policy.

Maximize Discounts and Bundle Coverage

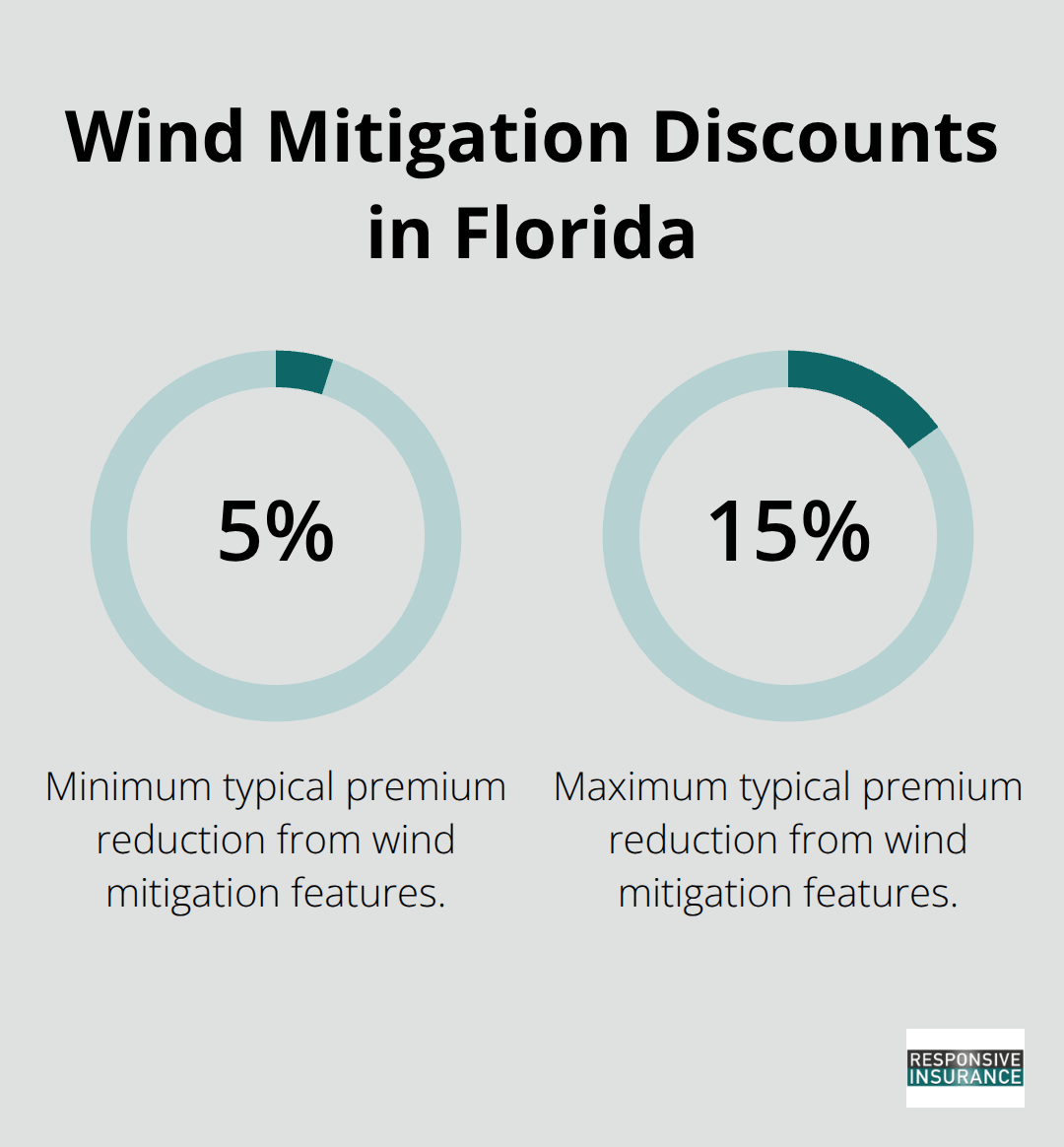

Bundling discount options with the same company can provide significant savings on your combined premiums, and this discount often exceeds the savings from shopping individual policies separately. Ask each insurer about wind mitigation discounts for features like impact-resistant windows, reinforced roof systems, or hurricane shutters-Florida regulators require insurers to offer these discounts, and they can reduce your annual premium by 5 to 15 percent. Additional discounts apply for home security systems, fire alarms, claims-free history, and multiple policy bundling, so request a complete discount breakdown before you finalize your decision.

As an independent insurance agency based in Naples, Responsive Insurance, Inc. works with multiple A-rated insurance companies to compare coverage and find the best fit for your needs, helping you access discounts and options that individual shopping often misses.

Match Coverage to Your Home’s Real Risk Profile

The policy you select should reflect your home’s actual replacement cost, your personal liability exposure, and the real risk profile of Naples rather than the lowest price alone. Wind deductibles, roof age restrictions, and flood exclusions create gaps that low-price policies often contain, so focus on what each insurer excludes rather than what they include. A policy that costs $500 less annually but excludes water damage or limits roof coverage leaves you exposed to the exact perils that strike Naples homes most frequently.

Final Thoughts

Selecting the best homeowners insurance in Florida requires you to match your coverage to your home’s replacement cost, understand what each policy excludes, and compare quotes across multiple insurers to avoid overpaying. Your dwelling coverage must reflect the actual cost to rebuild your home, not its market value, while your personal property limits should account for high-value items through scheduled coverage. Wind deductibles, roof age restrictions, and flood exclusions create the gaps that expose you to financial disaster, so review these exclusions carefully before you commit to any policy.

Request quotes from at least three different insurers and verify that coverage limits match across all quotes so you compare actual apples to apples. Calculate your home’s replacement cost accurately rather than guessing based on market value, and confirm your roof’s age and condition since many insurers restrict or exclude coverage for roofs over 20 years old. Evaluate your flood risk through FEMA maps and purchase separate flood coverage if you live in or near a flood zone, because standard homeowners policies exclude flood damage entirely.

An independent insurance agent brings expertise that individual shopping cannot match, and we at Responsive Insurance, Inc. work with multiple A-rated insurance companies to compare coverage options and find the best homeowners insurance Florida policy that fits your specific needs and budget. We help Naples homeowners understand wind deductibles, roof restrictions, and coverage gaps before they file a claim, and we identify discounts you qualify for while explaining how bundling policies reduces your overall cost. Contact Responsive Insurance, Inc. to discuss your home’s protection and find the coverage you can trust.