Florida Flood Insurance Options: Compare, Choose, Save

Living in Naples, FL means understanding that flood risk isn’t optional-it’s a reality. Standard homeowners insurance won’t protect your property from flooding, which is why exploring Florida flood insurance options is essential for any homeowner in our area.

At Responsive Insurance, Inc., we help residents navigate the choices between the National Flood Insurance Program and private providers. This guide breaks down your options, shows you how to compare coverage, and reveals concrete ways to reduce your premiums.

Why Florida Homeowners Need Flood Insurance Now

Florida’s Geography Creates Unavoidable Flood Risk

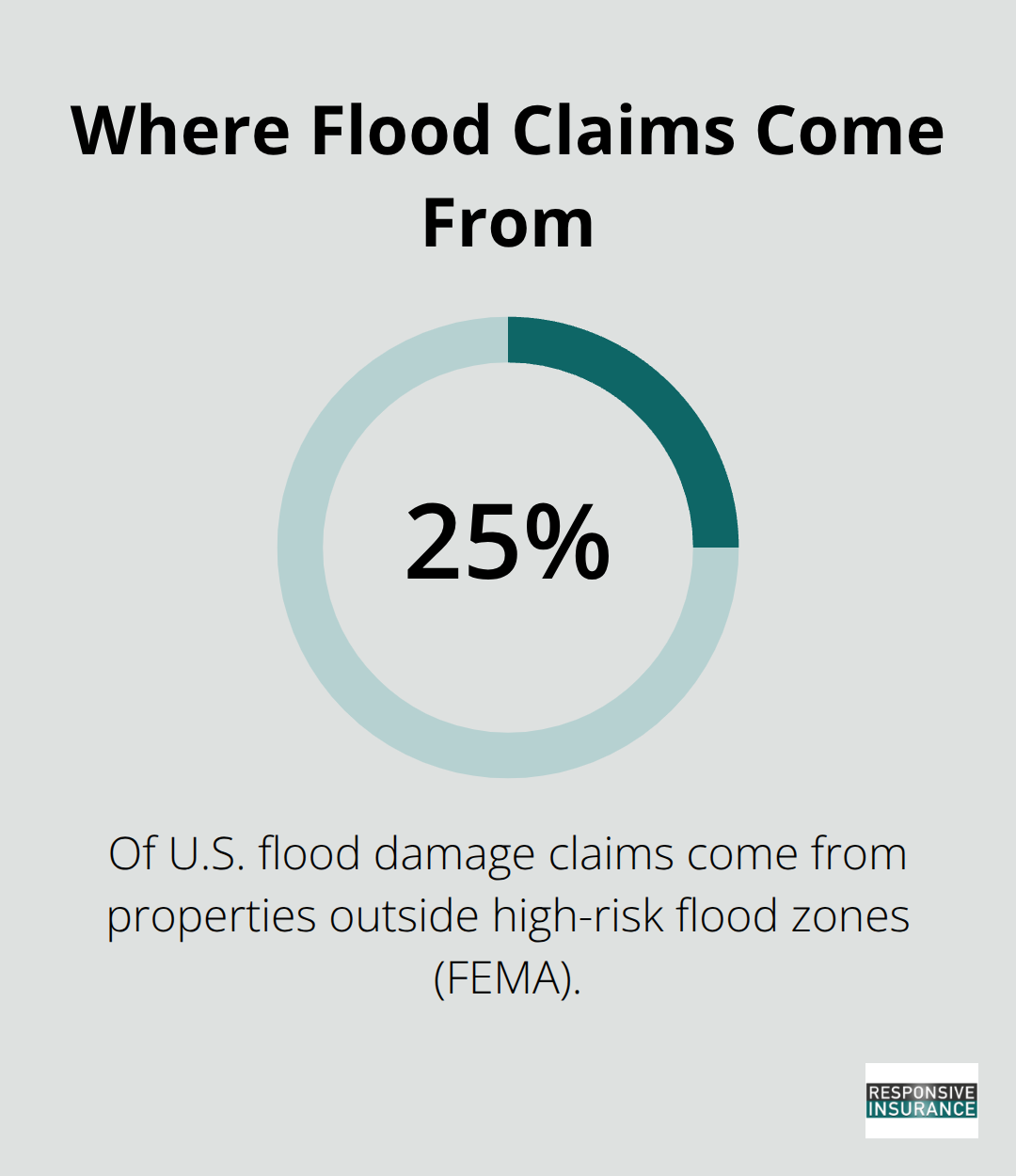

Florida’s geography makes flooding inevitable rather than unlikely. The state sits at an average elevation of just six feet above sea level, and much of Naples sits even lower, creating a perfect storm for water intrusion during heavy rainfall, storm surge, and hurricane season. FEMA data shows that about 25% of flood damage claims come from properties outside high-risk flood zones, which means your address doesn’t have to be marked as a Special Flood Hazard Area for flooding to devastate your home.

The True Cost of Flood Damage

Just one inch of floodwater costs around $25,000 to repair. That number climbs quickly with additional inches. Standard homeowners insurance explicitly excludes flood damage, treating rising water as a separate peril that requires its own dedicated policy. Your homeowners policy covers damage from wind, hail, fire, and theft, but the moment water rises from ground level into your home, you’re on your own unless you hold flood insurance.

The National Flood Insurance Program

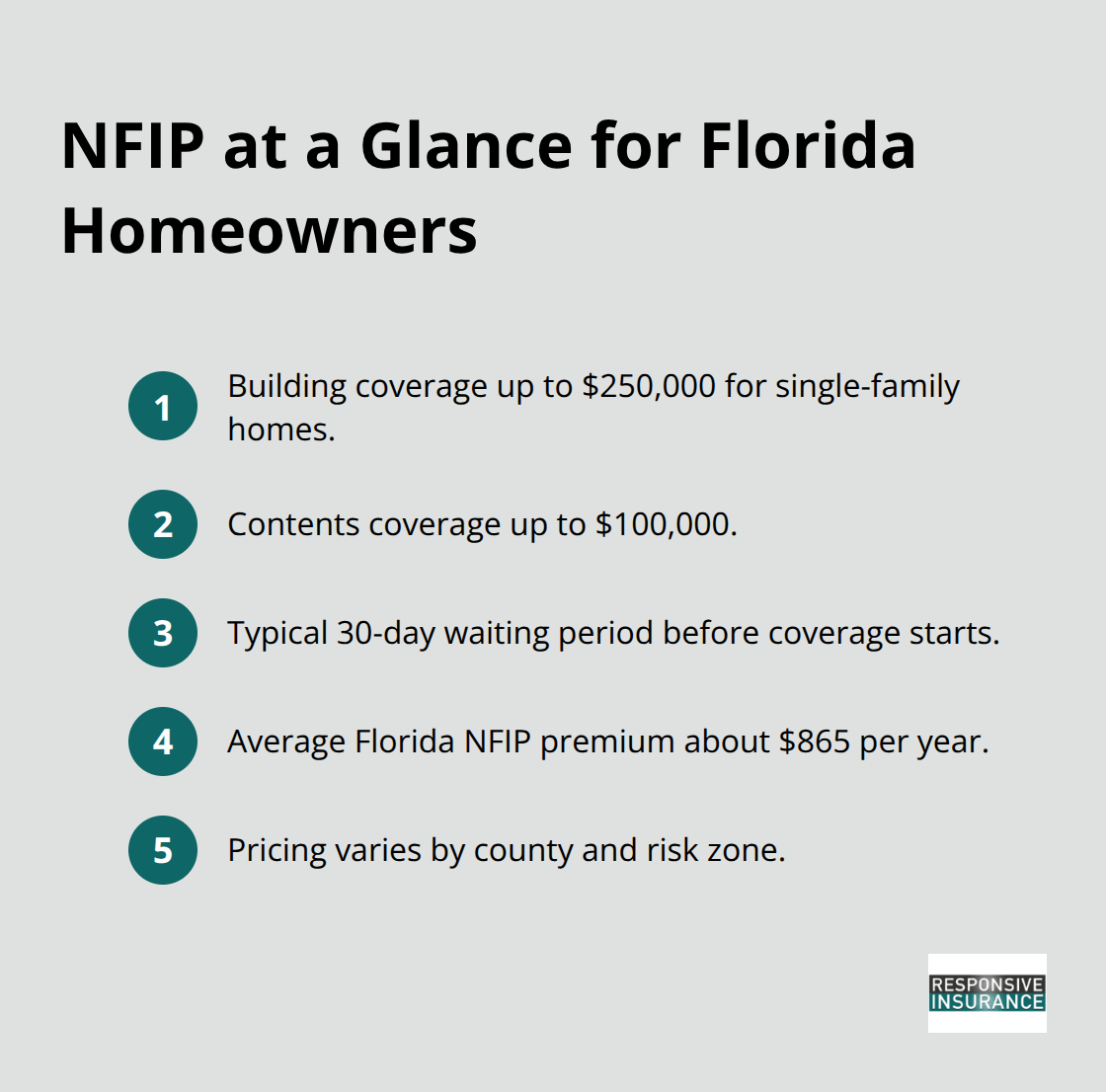

The National Flood Insurance Program, run by FEMA, offers standardized coverage nationwide with building limits up to $250,000 and contents coverage up to $100,000 for single-family homes. NFIP policies typically include a 30-day waiting period before coverage activates, so purchasing now matters if you want protection in place before hurricane season. The average Florida flood insurance premium under NFIP runs about $865 per year, though this varies significantly by county and risk zone.

Private Flood Insurance as an Alternative

Private flood insurance providers represent an alternative worth exploring. These carriers often offer higher coverage limits (sometimes exceeding $1 million for buildings), faster waiting periods as short as 15 days, and additional living expenses coverage if your home becomes uninhabitable. Private policies may also cover replacement cost for personal belongings instead of actual cash value, which means you recover more when items are damaged. The tradeoff is that private policies require underwriting approval and aren’t available for every property, making an independent agent invaluable for comparing both NFIP and private quotes side by side.

With both NFIP and private options available to you, the next step involves understanding how to evaluate these quotes and select the coverage that protects your Naples home most effectively.

Which Flood Insurance Option Fits Your Naples Home

NFIP Coverage Limits and How They Affect Your Protection

NFIP policies come with fixed coverage limits that work well for many homeowners but fall short for high-value properties. Building coverage maxes out at $250,000 and contents at $100,000 for single-family homes, which means if your home is worth $500,000 or more, you face immediate underinsurance. The program calculates premiums based on risk zone, property elevation, and claim history, offering standardized pricing across Florida. Naples residents in lower-risk flood zones qualify for preferred risk policies under NFIP, which can cut your annual premium substantially compared to standard rates.

However, NFIP policies don’t cover additional living expenses if your home becomes uninhabitable, and they pay actual cash value on contents rather than replacement cost. This leaves you short when furnishings and belongings need replacing after a flood event.

Private Flood Insurance Advantages and Trade-offs

Private flood insurance addresses these gaps directly. Carriers offer building limits exceeding $1 million, replacement cost coverage for personal property, and additional living expenses that cover temporary housing during repairs. Private policies can activate in as few as 15 days versus NFIP’s standard 30-day waiting period, which matters if hurricane season approaches and you lack coverage.

The catch is that private insurers underwrite each property individually, so high-risk properties or those with previous flood damage may not qualify. Premiums vary by carrier based on their own risk models, and not every property receives approval from every insurer.

How to Evaluate Quotes and Select the Right Policy

Evaluating quotes requires comparing three specific elements that matter most. First, check whether each quote covers your actual replacement cost for the structure and contents, not just actual cash value, since depreciation can leave you thousands short after a claim. Second, confirm the coverage limits match your home’s true value and your belongings’ worth, accounting for inflation in Southwest Florida’s real estate market. Third, ask whether the policy includes additional living expenses and what those limits are, because temporary housing costs add up fast when you’re displaced for months during repairs.

Get quotes from both NFIP through local agents and from private carriers to see the price difference, but don’t choose based on premium alone. A policy $200 cheaper annually that caps your building coverage at $250,000 costs far more than a private policy that covers $500,000 when flood damage strikes. Work with an independent agent in Naples who can access multiple carriers and explain the differences in plain terms (rather than trying to navigate NFIP’s website or calling individual private insurers separately). This comparison process reveals which option truly protects your property and finances.

Once you understand your options and have quotes in hand, the next step involves identifying concrete ways to reduce what you’ll actually pay for flood insurance coverage.

How to Actually Lower Your Flood Insurance Premiums

Elevation Certificates Unlock Immediate Rate Reductions

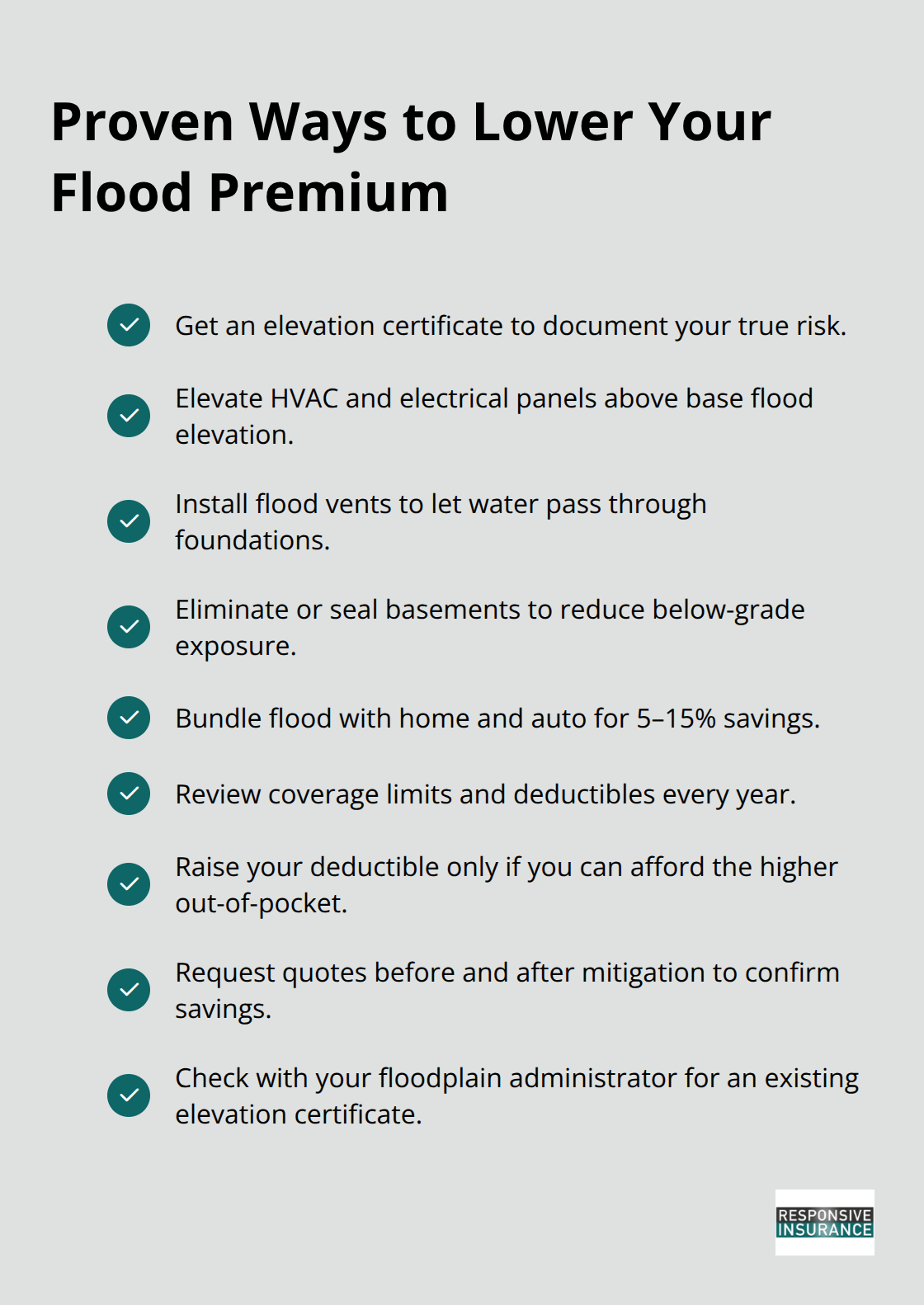

Your property’s height relative to the base flood elevation determines much of what you pay for flood insurance. Elevation certificates enable insurance companies to assess your property’s flood risk accurately. A surveyor charges $300 to $500 to obtain one, but the premium savings often recoup that investment within one to two years. If your home was built before elevation data was recorded in your county, this certificate becomes even more valuable because it proves your actual flood risk to underwriters. Contact your local floodplain administrator first to check whether an elevation certificate already exists on file for your property. If one does, you’ve already cleared the path to lower rates without spending anything.

Physical Improvements That Reduce Premiums

Physical improvements to your property directly reduce what insurers charge. Elevating utilities like HVAC systems and electrical panels above the base flood elevation signals lower risk and triggers premium reductions on both NFIP and private policies. Installing flood vents in foundation walls allows water to flow through rather than accumulate, which prevents structural damage and qualifies you for discounts.

Filling or sealing basements eliminates below-grade exposure that insurers view as high-risk, though this requires careful planning with a contractor familiar with flood mitigation. These improvements cost money upfront-flood vents run $300 to $1,000 per opening, and utility elevation can exceed $5,000-but they reduce annual premiums by 10 to 20 percent on many policies. A $1,500 annual premium could drop to $1,200 or $1,350 after mitigation work. Get quotes before and after completing mitigation work so you see the actual savings rather than assuming discounts will apply.

Bundling and Deductible Strategies

Bundling flood insurance with your homeowners and auto policies through the same carrier typically yields 5 to 15 percent savings on your total premium. Some insurers offer additional discounts if you maintain multiple policies without gaps in coverage. Review your coverage limits and deductibles annually, because as property values in Southwest Florida continue climbing, your $250,000 NFIP building limit may leave you underinsured relative to replacement costs. Raising your deductible from $500 to $1,500 cuts your annual premium by roughly 10 to 15 percent, but only if you can actually afford to pay that larger deductible when a claim occurs. This strategy works best for homeowners with emergency savings set aside.

Final Thoughts

Florida flood insurance options require you to weigh standardized NFIP coverage against customized private policies based on your home’s value and risk tolerance. NFIP offers predictable premiums and fixed building limits up to $250,000, while private carriers provide higher limits, faster activation, and additional living expenses coverage when your home becomes uninhabitable. Calculate your actual replacement cost for both structure and belongings, then verify that your chosen policy covers that amount before you commit to a plan.

Start by checking your property’s flood zone status on FEMA maps and obtaining an elevation certificate if one doesn’t already exist on file with your local floodplain administrator. This single step often qualifies you for lower rates immediately, and the investment pays for itself within one to two years through premium reductions. Contact Responsive Insurance, Inc. to compare NFIP and private quotes side by side, since we work with multiple A-rated carriers to find coverage that matches your budget and protects your Naples property.

The 30-day waiting period on most policies means you should purchase coverage now rather than waiting until hurricane season approaches. We help you navigate these choices and secure the protection your home needs before storms arrive.