Florida Home Flood Insurance: Practical Guide for Homeowners

Florida home flood insurance isn’t optional for most homeowners-it’s a financial necessity. Nearly one in four insured homes in Florida have flood coverage, and that number keeps growing as residents recognize the real risks.

At Responsive Insurance, Inc., we’ve helped countless Naples homeowners navigate flood insurance decisions. This guide walks you through everything you need to know, from understanding your flood zone to filing claims after water damage.

Why Florida Homeowners Need Flood Insurance Now

Florida’s Geography Makes Flooding Inevitable

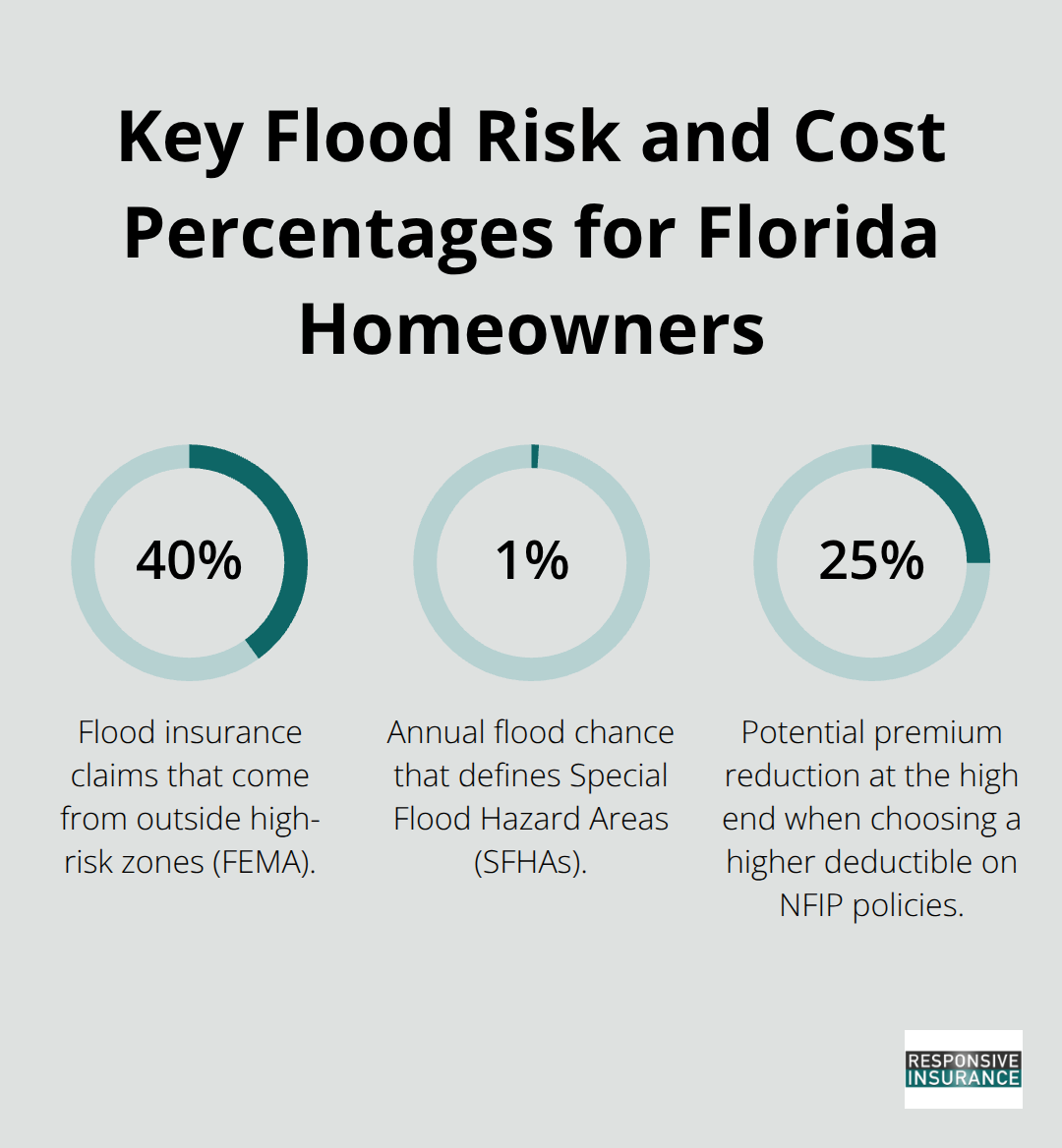

Florida’s geography makes flooding inevitable, not just possible. The state sits at an average elevation of just six feet above sea level, with some areas in Naples and coastal Collier County sitting even lower. Storm surge from hurricanes, heavy rainfall, and high tides push water onto your property faster than drainage systems can handle it. According to FEMA data, about 40 percent of all flood insurance claims come from properties outside high-risk zones, proving that water doesn’t respect official flood maps. Your standard homeowners insurance policy will not cover any of this damage-not the structural repairs, not the ruined appliances, not the water-logged furniture.

Homeowners without flood coverage face out-of-pocket losses that often exceed $25,000.

Federal disaster aid is never guaranteed. It only arrives after a presidential disaster declaration, and even then it typically comes as a loan you must repay, not a grant. This means most homeowners who experience flood damage without insurance must pay for repairs themselves or carry debt for years.

Standard Homeowners Insurance Won’t Protect You

Water damage from flooding is explicitly excluded from every homeowners policy in Florida. If floodwater enters your home through doors, windows, or foundation cracks, your insurer will deny the claim. The only way to cover flood damage is through a dedicated flood insurance policy purchased separately. You need both: homeowners insurance for fire, theft, and wind damage, plus flood insurance for water damage from rising water.

The National Flood Insurance Program offers building coverage up to $250,000 and contents coverage up to $100,000 for residential properties, while private flood carriers may offer higher limits. In Naples, where Gulf exposure and low elevation create widespread risk, the average NFIP premium runs around $865 per year according to NFIP data, though costs vary significantly by property location and elevation. Private flood insurance can sometimes cost less, especially for lower-risk properties, making it worth comparing options before you buy.

High-Risk Areas Have Mandatory Requirements

If your property sits in a Special Flood Hazard Area-FEMA’s term for zones with at least a 1 percent annual chance of flooding-your mortgage lender will require flood insurance. This applies to Zone AE, Zone AH, and coastal Zone VE properties in Naples. The 2024 Flood Insurance Rate Maps now in effect for Collier County show which properties fall into these mandatory zones.

If you received federal disaster assistance for past flood damage, you must maintain continuous flood insurance to qualify for future federal aid. This requirement stays with the property, not just the owner, so even if you pay off your mortgage, you cannot drop the coverage without losing eligibility for future disaster assistance. Lenders use these maps to determine whether flood insurance is mandatory at closing, and they verify compliance annually.

Starting January 1, 2026, Citizens Property Insurance policyholders with wind coverage must carry flood insurance if their dwelling coverage is $400,000 or more, with additional requirements phasing in for lower coverage amounts by January 1, 2027. These aren’t suggestions-they’re legal requirements enforced by lenders and tracked by the state. Understanding your flood zone and lender requirements is the first step toward protecting your home, which leads directly into evaluating your specific property’s risk level and choosing the right coverage for your situation.

Finding the Right Flood Policy for Your Home

Identify Your Flood Zone First

Check your flood zone on FEMA’s flood maps before you compare policies. Visit floodsmart.gov, enter your address, and identify whether you occupy Zone AE, AH, VE, or one of the lower-risk zones like X. This single step determines everything that follows: whether flood insurance is mandatory, what your baseline premium will be, and which coverage options make sense for your situation. Properties in high-risk zones pay substantially more, but even moderate-risk properties see real savings when you shop private flood insurance against NFIP rates.

Naples properties in Zone AE, for example, might pay $1,000 to $1,500 annually through NFIP, while similar properties in Zone X could qualify for preferred risk rates starting around $400 to $600 per year according to NFIP data.

Use Elevation Certificates to Lower Your Costs

Your elevation relative to the base flood elevation matters enormously. If your home sits well above the BFE, an elevation certificate can reduce your premiums significantly, with annual savings typically ranging from $500 to $1,100. Conversely, if your first floor sits below or near the BFE, expect higher costs. Request an elevation certificate from your local floodplain coordinator or hire a surveyor to obtain one-this document pays for itself through premium reductions within a year or two.

Match Coverage Limits to Your Home’s Value

Compare building coverage limits against your home’s actual replacement cost. NFIP caps building coverage at $250,000 for residential properties, which may fall short if your Naples home costs $350,000 or more to rebuild. Private flood carriers often offer limits up to $500,000 or higher, making them essential for higher-value homes. Contents coverage also matters: NFIP covers up to $100,000, but that may not protect your furniture, electronics, artwork, and clothing adequately. Private policies sometimes offer higher contents limits and additional living expense coverage if you need to relocate during repairs.

Select Deductibles That Fit Your Budget

Deductibles typically range from $500 to $5,000 on NFIP policies, and selecting a higher deductible reduces your annual premium significantly-sometimes by 15 to 25 percent. Calculate whether you can afford out-of-pocket costs before a claim occurs, then choose accordingly. This decision directly affects both your monthly costs and your financial exposure when water damage strikes.

Compare Multiple Carriers Side by Side

An independent agent can run quotes through multiple carriers simultaneously, showing you NFIP options alongside private flood insurers like Neptune Flood, Flow Flood, and others operating in Florida. This comparison takes one conversation instead of contacting multiple carriers yourself. Request quotes with identical coverage limits and deductibles so comparisons are meaningful. The cheapest premium isn’t always the best choice if coverage gaps exist-verify that building damage, contents, and any optional living expenses align with your actual needs before deciding. Once you’ve selected the right policy and locked in your rate, the next critical step involves preparing your home and documentation before flood season arrives, ensuring you can respond quickly if water damage threatens your property.

Protecting Your Home Before Water Strikes and After Damage Occurs

Document Your Home’s Condition Now

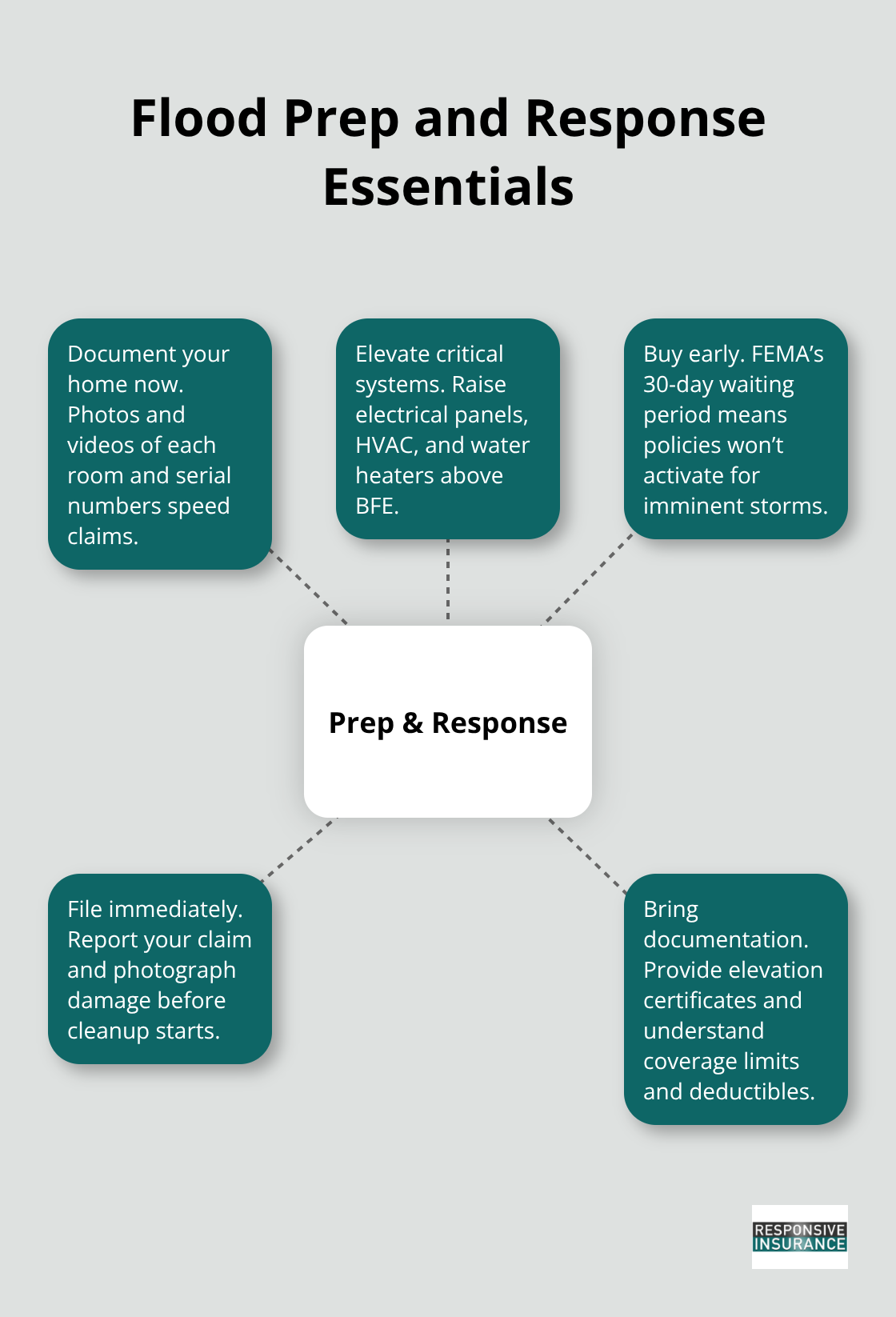

Preparation for flood season starts months before rain falls, not days before a storm arrives. You should photograph and video every room, closet, and storage area in your home, including serial numbers on appliances and electronics. Store this documentation in a waterproof container or cloud storage service where you can access it after damage occurs. This step takes a few hours now but saves weeks of frustration when you file a claim, since insurers require proof of what you owned and its condition before water damage struck.

Elevate Critical Systems and Reduce Basement Risk

You can lower repair costs significantly by elevating your electrical panel, HVAC system, and water heater above your property’s base flood elevation. Install flood vents in foundation walls if your home sits in a flood zone, allowing water to flow through rather than building pressure against walls. Fill basement spaces with gravel or remove items permanently, since finished basements rarely recover from flooding and contents rarely survive water damage. These mitigation steps reduce both your flood risk and your insurance premiums in many cases.

Purchase Your Policy Well Before Storm Season

You must buy your flood insurance policy now rather than waiting for a storm forecast, because FEMA imposes a 30-day waiting period before coverage takes effect. That delay means you cannot buy protection once a hurricane enters the forecast cone. Contact an independent agent to lock in your policy well before June when Atlantic hurricane season peaks, ensuring your coverage is active when it matters most.

File Your Claim Immediately After Floodwater Recedes

You should file your claim immediately rather than waiting for adjusters to contact you. Photograph all visible damage before cleaning anything, as insurers need documentation of conditions immediately after the event. Keep receipts for any emergency repairs like tarping roofs or removing standing water, since many flood policies cover reasonable mitigation costs that prevent further damage. When the adjuster arrives, walk through your property together and point out every affected area, from water stains on drywall to damaged insulation in crawl spaces.

Provide Documentation and Understand Your Coverage Limits

You should provide your elevation certificate and any previous elevation surveys if you have them, since these documents directly affect claim calculations. Your deductible applies per occurrence, not per item, meaning a $1,000 deductible covers your entire loss rather than reducing each damaged item separately. If your claim seems undervalued, hire an independent public adjuster who works on your behalf for a percentage of the settlement, typically ranging from 5 to 10 percent. This cost often returns itself through higher settlements on substantial claims exceeding $10,000. NFIP coverage limits cap at $250,000 for building damage and $100,000 for contents, which may fall short of your actual replacement costs if you selected insufficient coverage limits before the flood. This reality underscores why matching your coverage to your home’s true replacement value matters so much when you purchase your policy.

Conclusion

Florida home flood insurance protects your family’s financial security in ways standard homeowners policies simply cannot. About 40 percent of flood claims come from properties outside high-risk zones, meaning your address matters far less than your preparedness. Whether you live in a mandatory flood zone or a lower-risk area, the difference between having coverage and facing $25,000 in out-of-pocket repairs comes down to decisions you make today.

Start by checking your flood zone on floodsmart.gov and requesting an elevation certificate if your home sits above the base flood elevation. Compare NFIP rates against private flood insurance through an independent agent who can access multiple carriers simultaneously, and the savings often surprise homeowners in moderate-risk zones where private insurers offer preferred risk rates starting around $400 to $600 annually. Match your coverage limits to your home’s actual replacement cost, select a deductible you can afford out-of-pocket, and purchase your policy months before hurricane season peaks (the 30-day waiting period means you cannot buy protection once a storm threatens your area).

We at Responsive Insurance, Inc. help Naples homeowners navigate Florida home flood insurance decisions every day. Contact us today to discuss your specific situation and lock in protection before the next storm arrives.