Understanding Flood Insurance: What You Need to Know

Florida homeowners face a reality that catches many off guard: standard homeowners insurance doesn’t cover flood damage, no matter how comprehensive your policy seems.

At Responsive Insurance, Inc., we’ve seen too many Naples residents learn this lesson the hard way after a storm or heavy rainfall causes devastating losses. Understanding flood insurance isn’t optional in Florida-it’s a financial necessity that protects your home and savings from one of the state’s most common natural disasters.

Why Flood Insurance Matters in Florida

Standard Homeowners Policies Leave You Exposed

Your standard homeowners policy has a massive blind spot, and it costs Florida residents billions every year. Flood damage simply isn’t covered under homeowners insurance, no matter how expensive or comprehensive your policy appears. This gap exists because flooding is treated as a separate peril entirely, requiring its own dedicated coverage through the National Flood Insurance Program or private flood insurers. Most people discover this limitation only after water enters their home, which is far too late.

Floods cause approximately $8.2 billion in damages annually across the United States, making them the most frequent and costliest natural disaster. Florida shoulders a disproportionate share of this burden due to the state’s geography, weather patterns, and increasing development in flood-prone areas.

Your Flood Risk Is Higher Than You Realize

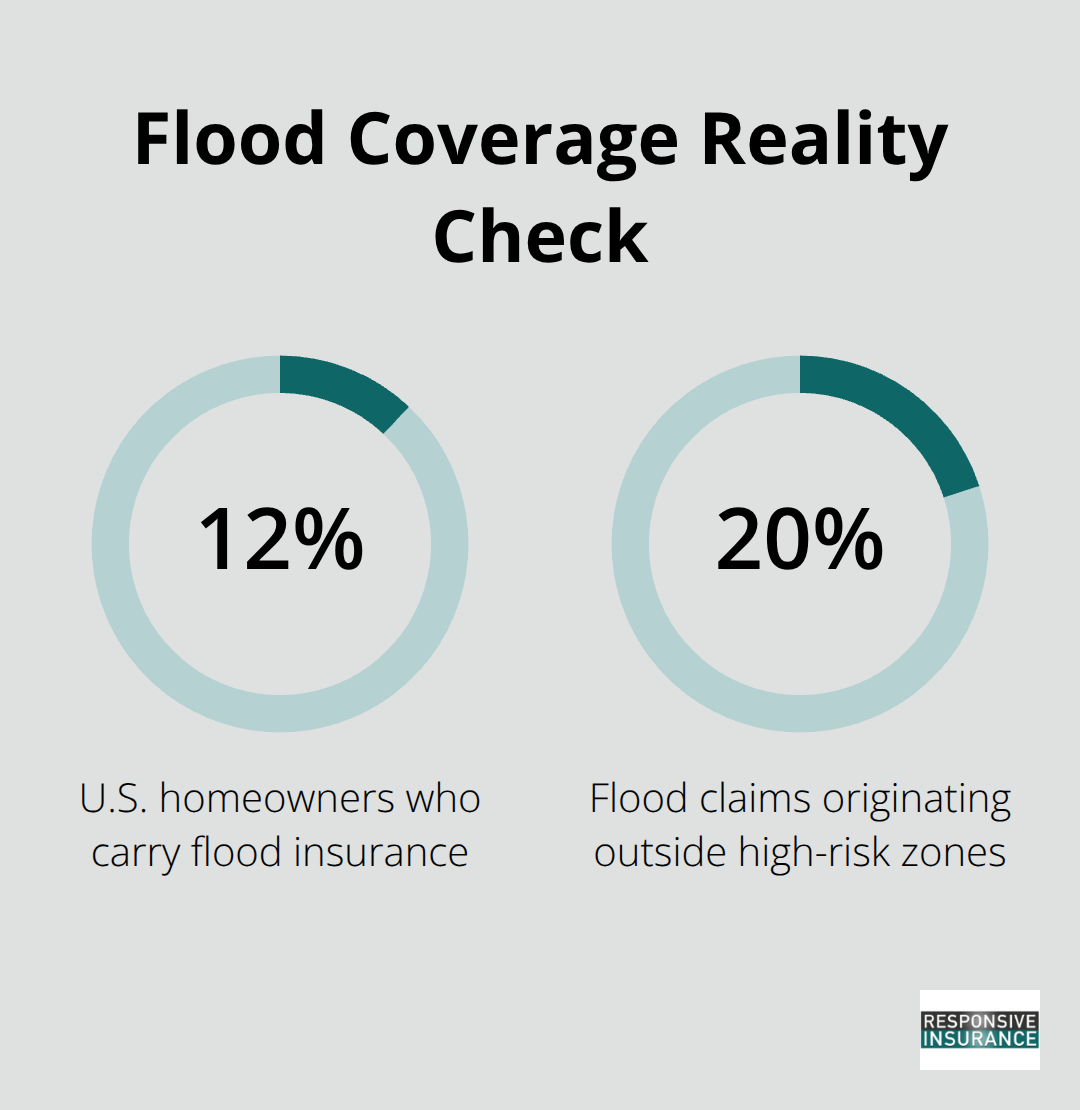

Your flood risk is almost certainly higher than you think. Only about 12 percent of U.S. homeowners carry flood insurance, yet roughly 20 percent of flood claims come from outside high-risk zones designated on official flood maps. This statistic destroys the common assumption that you’re safe if you’re not in a Special Flood Hazard Area.

Naples residents face particularly acute exposure given the city’s coastal location and participation in the National Flood Insurance Program since 1970. The 2024 Flood Insurance Rate Maps now in effect across Collier County provide updated flood risk data that reflects current hazards more accurately than the previous 2012 maps. Even properties in moderate-to-low-risk areas need protection because heavy rainfall, storm surge, and drainage issues can overwhelm local systems regardless of zone designation.

The True Cost of Going Without Coverage

Without flood insurance, your only option after a flood is paying losses out of pocket, since federal disaster assistance isn’t automatic and requires a presidential disaster declaration that occurs in fewer than half of flood events. The average flood claim exceeds $25,000 in structural damage alone, plus additional costs for displaced living expenses and personal belongings. This financial reality makes flood insurance a practical safeguard that separates manageable recovery from financial devastation.

Understanding these risks sets the stage for exploring the specific coverage options available to you. The National Flood Insurance Program and private insurers each offer distinct advantages that address different needs and budgets.

Types of Flood Insurance Coverage Available

The National Flood Insurance Program: Standard Protection with Trade-Offs

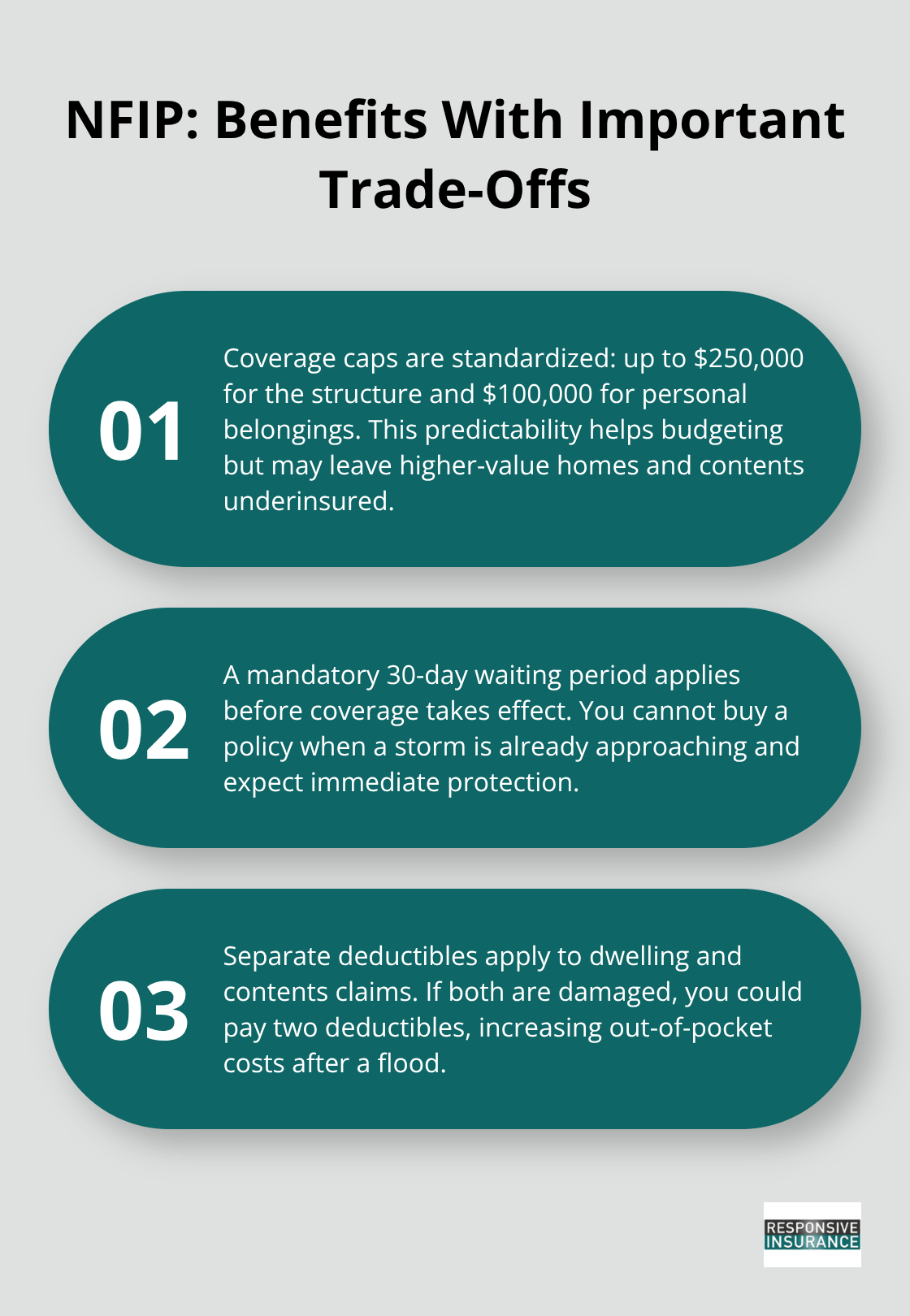

The National Flood Insurance Program dominates Florida’s flood insurance market, offering standardized coverage up to $250,000 for structural damage and $100,000 for personal belongings. In Naples, NFIP policies cost an average of $865 annually according to recent data. However, this program carries significant limitations that affect real homeowners. A 30-day waiting period prevents you from purchasing protection once a storm approaches, so timing matters enormously.

The program also charges separate deductibles for dwelling and contents damage-if both your home and belongings flood, you pay two deductibles instead of one.

Risk Rating 2.0, which rolled out beginning in 2021, prices policies based on individual property risk rather than zone-wide averages. Florida’s average single-family premium jumped from approximately $776 to roughly $1,363 under this system, though about 20 percent of policyholders actually saw rate decreases. If your home sits outside a high-risk zone, you might qualify for a preferred risk policy at substantially lower rates, potentially saving thousands annually.

Reducing Your NFIP Costs Through Documentation

An elevation certificate documenting your home’s lowest floor height can reduce premiums significantly. Contact the City of Naples Floodplain Coordinator at 239-213-5039 if you want to explore this option. This single document often pays for itself within a year or two through premium savings, making it a practical investment for homeowners serious about controlling flood insurance costs.

Private Flood Insurance: Coverage Beyond NFIP Limits

Private flood insurance has emerged as a legitimate alternative that many Naples homeowners overlook entirely. Private carriers offer coverage limits exceeding NFIP maximums, sometimes with faster activation periods and more flexible deductible structures. Renters can obtain private flood coverage starting around $100 annually, far below NFIP rates. The Florida Office of Insurance Regulation maintains a list of approved private insurers you can contact directly.

Comparing actual quotes matters more than assumptions about cost-some private policies cost less than NFIP equivalents while providing broader protection. The difference between adequate and inadequate coverage could mean the difference between recovering from a flood or facing financial ruin. Understanding both programs positions you to make an informed decision about which option protects your Naples home most effectively.

How to Choose the Right Flood Insurance for Your Home

Identify Your Flood Zone First

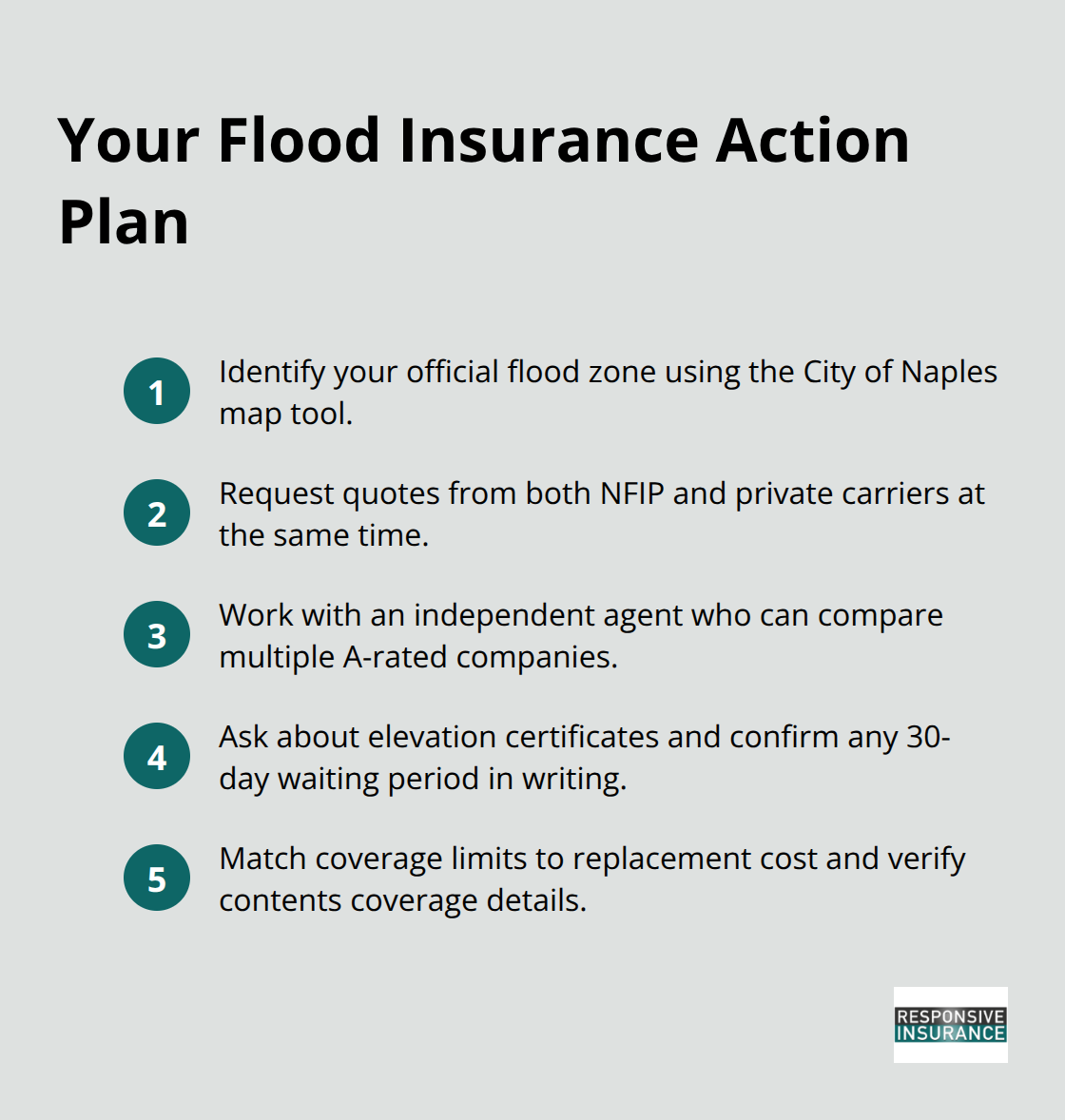

Start with your property address and the City of Naples interactive flood map tool, which reveals your official flood zone designation in seconds. This step eliminates guesswork and grounds your decision in actual risk data rather than assumptions. Zones AH, AE, and VE carry a 1% annual chance of flooding and trigger mandatory coverage if you have a federally backed mortgage, while Zone X (500-year) and unshaded areas don’t legally require it but still warrant protection given that roughly 20% of flood claims originate outside high-risk zones according to FEMA data. Contact the City of Naples Floodplain Coordinator at 239-213-5039 or rdorta@naplesgov.com if the map leaves questions unanswered.

Request Multiple Quotes Simultaneously

Once you know your zone, request quotes from both NFIP and private carriers at the same time rather than shopping one source at a time. Naples residents face average NFIP costs around $1,498 annually, but private options sometimes undercut this significantly while offering higher limits up to $10 million for structural coverage. The comparison matters because a $250,000 NFIP limit covers only the structure itself, leaving your personal belongings capped at $100,000 combined. Homes with valuable furnishings, artwork, or collectibles frequently need private coverage to avoid substantial gaps. Renters in Naples can obtain flood protection starting around $100 yearly through private carriers, making this protection accessible regardless of income level.

Work with an Independent Agent

An independent insurance agent becomes invaluable at this stage because they access multiple carriers and understand which ones serve Naples properties most effectively. Agents compare coverage options across partner networks of A-rated companies to identify policies matching your specific risk profile and budget constraints. Request quotes that specify deductible structures since NFIP policies charge separate deductibles for dwelling and contents damage, potentially doubling your out-of-pocket costs after a flood, while some private carriers consolidate this into a single deductible.

Optimize Your Coverage and Costs

Ask agents whether elevation certificates could reduce your premiums, as documented proof of your home’s lowest floor elevation sometimes generates annual savings exceeding $500. Request the 30-day waiting period in writing when purchasing NFIP coverage, since this delay prevents last-minute purchases once storms approach. Review each quote’s coverage limits against your home’s actual replacement cost rather than its market value, since rebuilding after flooding often costs more than the original construction. Verify that contents coverage includes the items you actually own, not just generic categories, since flood policies exclude damage from pipe bursts or internal water system failures that homeowners insurance might cover.

Final Thoughts

Flood insurance isn’t a luxury in Florida-it’s a financial necessity that protects your Naples home from one of the state’s most destructive natural disasters. Understanding flood insurance means recognizing that your standard homeowners policy leaves a critical gap, that your actual flood risk likely exceeds what you assume, and that the cost of remaining uninsured far outweighs the cost of coverage. The statistics are clear: floods cause $8.2 billion in annual damages across the U.S., and roughly 20 percent of claims originate outside designated high-risk zones, proving that geography alone doesn’t determine your vulnerability.

The good news is that multiple coverage pathways exist to fit different budgets and protection needs. The National Flood Insurance Program offers standardized protection with average Naples costs around $1,498 annually, while private carriers frequently provide higher limits and competitive pricing that sometimes undercuts NFIP rates. Whether you choose NFIP or private coverage, the key is moving forward with actual quotes rather than assumptions about cost or availability.

The 30-day waiting period built into most flood policies means that waiting until a storm approaches guarantees you’ll be unprotected when you need coverage most. Contact Responsive Insurance, Inc. today to request quotes and move your home from exposed to protected. Your financial security depends on taking this step now, not after the next heavy rainfall or coastal storm reminds you why flood insurance matters.