Airbnb Insurance Florida Your Guide for Short-Term Rentals

Florida’s short-term rental market generates a lot of revenue and there are many rentals hosts in the state, making proper insurance protection essential to protect the asset so important to so many Floridians.

Standard homeowners policies typically exclude coverage for rental activities, leaving Airbnb hosts exposed to significant financial risks. We at Responsive Insurance, Inc. help Naples property owners navigate the complex world of Airbnb insurance Florida requirements and find protection for their rental investments.

Understanding Airbnb Insurance Requirements in Florida

Florida State Licensing and Registration

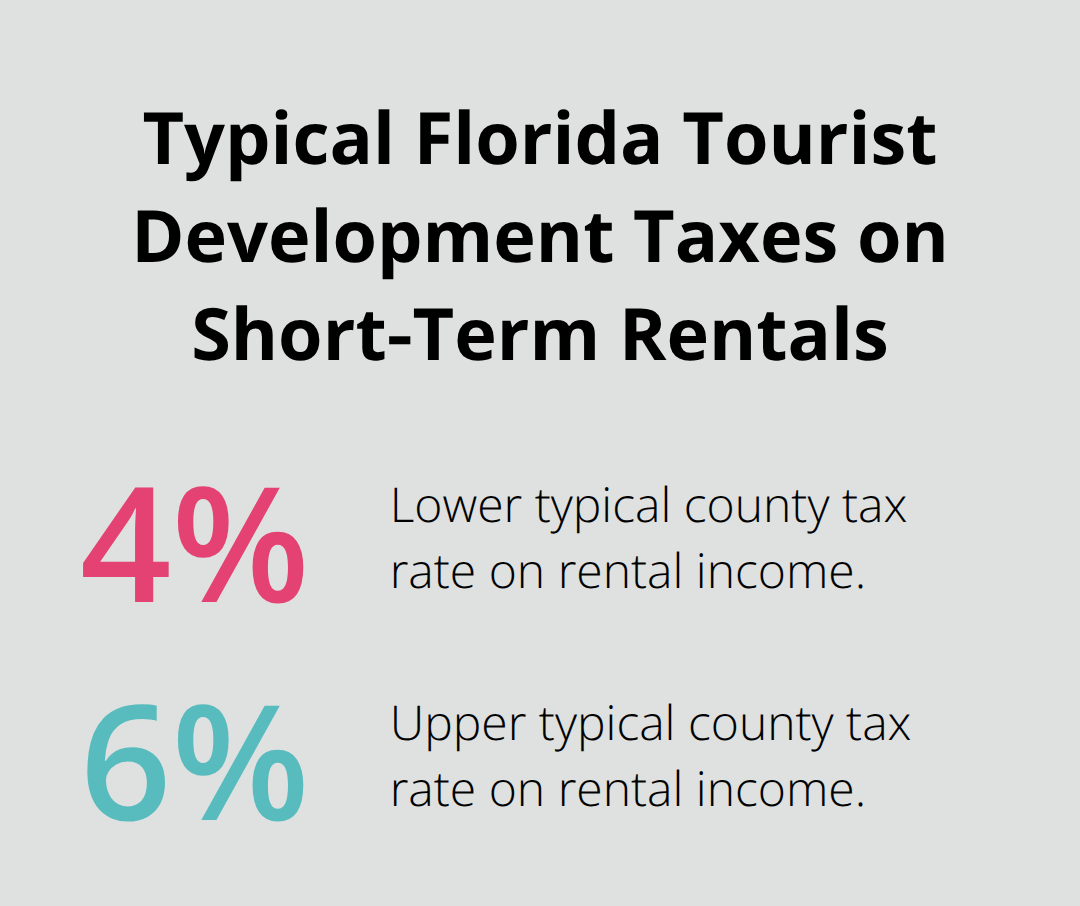

Florida requires all short-term rental operators to obtain a state license through the Department of Business and Professional Regulation before they accept guests. This mandatory license applies to any property rented for periods under 30 days, with annual renewal fees that range from $50 to $200 based on property size. The state also mandates that hosts collect and remit tourist development taxes, which vary by county but typically range from 4% to 6% of rental income.

Hosts who fail to comply with these requirements face potential fines and/or potential shutdown of rental operations.

Local Municipality Restrictions and Permits

Collier County implemented requirements for property owners to register certain short term rentals. The registration process requires a one time fee of $50 and requires proof of state license, a designated 24/7 responsible party contact, and compliance with occupancy limits. City of Naples, Marco Island, and Everglades City maintain exemptions from county registration but enforce their own zoning restrictions. Failure to register can result in fines up to $500 per day, per violation. Many municipalities also restrict short-term rentals in residential zones (making location verification critical before property purchase).

Insurance Coverage Gaps Between Home Insurance and Rental Property Coverage

Traditional homeowners insurance often explicitly excludes rental activities, which can leave hosts without protection for things like guest injuries, some types of property damage, or theft that occurs during rental periods. Short-term rental policies are designed to accommodate the rental exposure and often include coverage for lost rental income.

These regulatory and insurance requirements create a complex landscape that directly impacts the coverage options available to Florida Airbnb hosts.

Insurance Coverage Options for Florida Airbnb Hosts

Proper Property Insurance Protects Your Investment

Florida Airbnb hosts must secure rental property insurance that covers short-term rental operations, since standard homeowners policies are insufficient once rental activity starts. These policies can protect against perils that standard homeowners insurance excludes during rental periods.

Liability Protection Shields Against Guest Lawsuits

Often the underlying rental property coverage is capped at liability limits at approximately $300,000. Liability coverage of at least $1 million can provide additional protection for hosts against lawsuits from guest injuries, which average $75,000 in settlement costs according to industry data. This additional liability coverage can come from an excess comprehensive personal liability policy or a personal umbrella policy. Responsive Insurance can offer both.

Policies should also include coverage for vacant periods between guests, as most incidents occur during turnovers when cleaning crews and maintenance workers access properties (creating additional exposure points).

Business Interruption Coverage Replaces Lost Income

Business interruption insurance protects your Florida short-term rental revenue. Typical policies cover a specified amount of “fair rental value”. This coverage protects against significant financial losses during repair periods when a covered peril made the property unfit to live in.

The coverage becomes particularly valuable during Florida’s hurricane season, when storm damage can force properties offline for extended periods (potentially costing hosts thousands in lost bookings).

Common Insurance Gaps and How to Address Them

Personal Property Risks Standard Policies Ignore

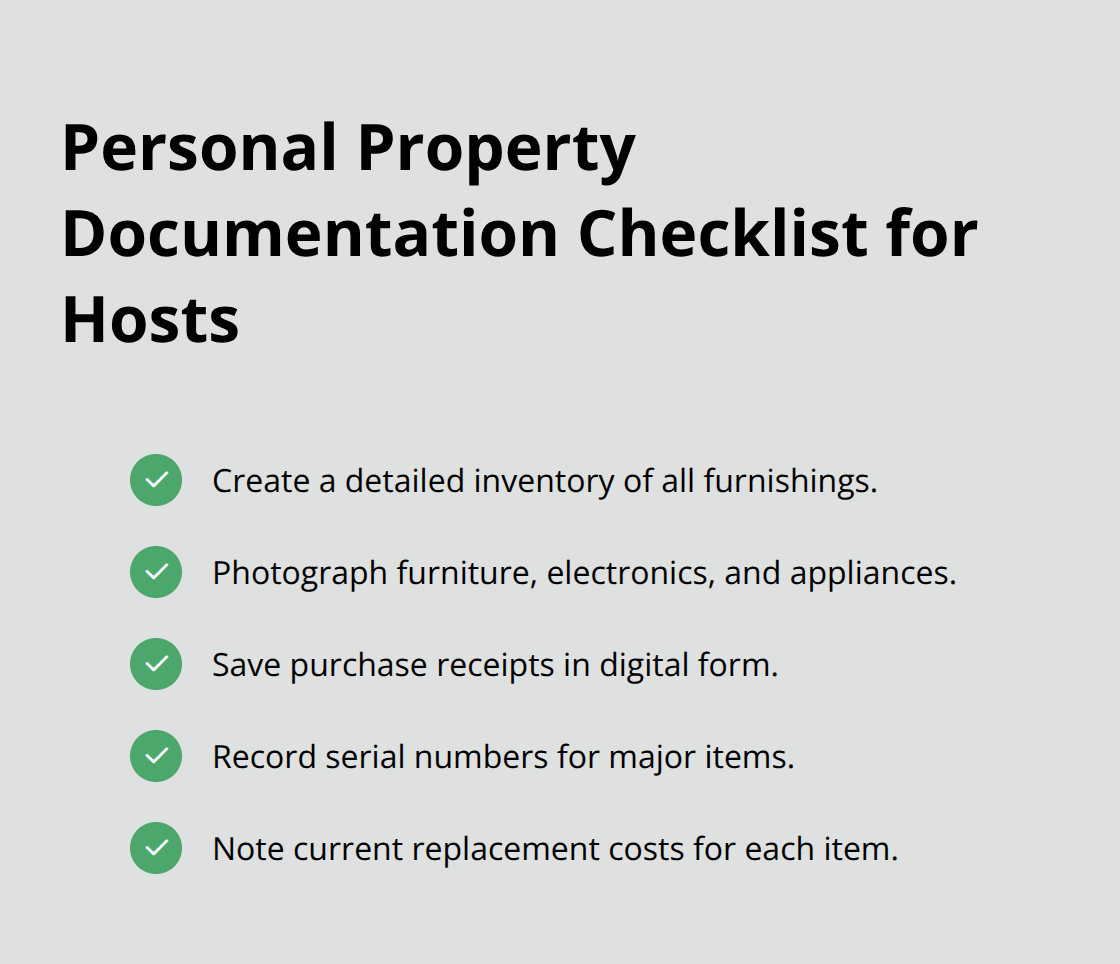

Most Airbnb hosts in Naples underestimate the value of their furnishings until damage occurs. A fully furnished three-bedroom vacation rental typically contains substantial replaceable items including furniture, electronics, linens, and kitchen equipment. Standard homeowners policies limit or exclude certain personal property coverage during rental periods, which leaves hosts with financial exposure.

Smart hosts create digital records of all furnishings with serial numbers and replacement costs before their first guest arrives. This documentation becomes essential during claims processing, as insurers ask for evidence of ownership and value for every damaged item.

Vandalism Protection

Guest vandalism represents a significant threat that platform protections inadequately address. Industry data shows that malicious damage claims average $8,500 per incident, with bathroom and kitchen vandalism most common in Florida rentals. Airbnb’s AirCover may be an option for some damage protection but being informed of coverage limitations and options is important BEFORE a loss occurs.

Coverage During Occupancy Periods Between Guests

Taking steps to monitor and protect the home is important between guests. As properties sit unoccupied, preventive steps related to water damage avoidance, for example, can be smart steps by hosts. Options include turning off the water, installing water flow monitoring or moisture monitoring devices, among other options. Insurance companies define “vacant” in different ways within their policies and this plays a role in how/if coverage applies. It’s important for hosts to familiarize themselves with how their insurer defines vacant and how coverage is affected.

Final Thoughts

Florida Airbnb and short term rental hosts face complex insurance requirements that standard homeowners policies cannot address. Proper short-term rental coverage, comprehensive liability protection, and loss of rental income insurance form the foundation of proper protection for rental properties.

Successful Airbnb and rental property protection in Florida requires work with experienced independent agents who understand short-term rental risks. These professionals compare coverage options from multiple insurance companies to find comprehensive protection that fits specific rental property needs and within the carrier guidelines. Independent agents serve as knowledgeable advocates who help property owners navigate the complex insurance landscape (particularly in Southwest Florida’s unique market conditions).

We at Responsive Insurance, Inc. provide complete responses to insurance questions for Florida-based property owners. Our team works with multiple insurance carriers to find the right coverage for your short-term rental investment. The investment in proper insurance coverage protects both your property and rental income while meeting Florida’s strict regulatory requirements for short-term rental operations.

![What Does Landlord Insurance Cover? [A Complete Guide]](https://responsiveinsurance.com/wp-content/uploads/emplibot/What-Does-Landlord-Insurance-Cover_-_A-Complete-Guide__1761430072-80x80.jpeg)