Naples Homeowners Insurance Options: How to Find the Right Coverage

Finding the right Naples homeowners insurance options takes more than a quick online search. Your home is likely your biggest investment, and protecting it properly requires understanding what coverage actually matters for your situation.

At Responsive Insurance, Inc., we help Naples homeowners cut through the confusion and build policies that match their real needs. This guide walks you through assessing your coverage requirements, comparing what’s available, and selecting a policy that gives you genuine peace of mind.

Understanding Your Home Insurance Needs in Naples

What Should Your Dwelling Coverage Actually Be

Your home’s replacement cost is the single most important number you need to get right, and most Naples homeowners get it wrong. Replacement cost means what it would actually cost to rebuild your home from the ground up if it were completely destroyed, not what you paid for it or what it’s worth on the market. A home you bought for $450,000 might cost $550,000 to rebuild because construction costs have climbed significantly in Southwest Florida. This shows that your coverage level directly drives your premium, so picking the wrong number wastes money either way-you’re either overpaying for coverage you don’t need or underinsured when a loss happens. A local contractor or appraiser who understands current Southwest Florida building costs, including materials, labor, and permit fees specific to this region, can provide a professional home valuation.

Protecting Your Personal Property and Liability Exposure

Personal property coverage protects your belongings-furniture, electronics, clothing, kitchen items-and it’s separate from dwelling coverage. Standard homeowners policies typically cover personal property at 50 to 70 percent of your dwelling coverage amount, which often isn’t enough. If your home has $300,000 in dwelling coverage, your personal property might only be covered for $150,000 to $210,000, leaving valuable items vulnerable. High-value items like jewelry, art, or collectibles have even lower limits under standard policies, sometimes capped at $1,500 to $2,500 per item. A scheduled personal property endorsement properly covers anything irreplaceable or expensive. Liability coverage protects you financially if someone is injured on your property or you accidentally damage someone else’s property, and Florida law doesn’t set a minimum, but carrying at least $300,000 is standard practice in Naples. If your net worth exceeds $500,000, a personal umbrella policy adding another $1 million in liability protection costs surprisingly little-often $150 to $300 annually-and provides critical protection against lawsuits that could devastate your finances.

Addressing Southwest Florida’s Unique Environmental Risks

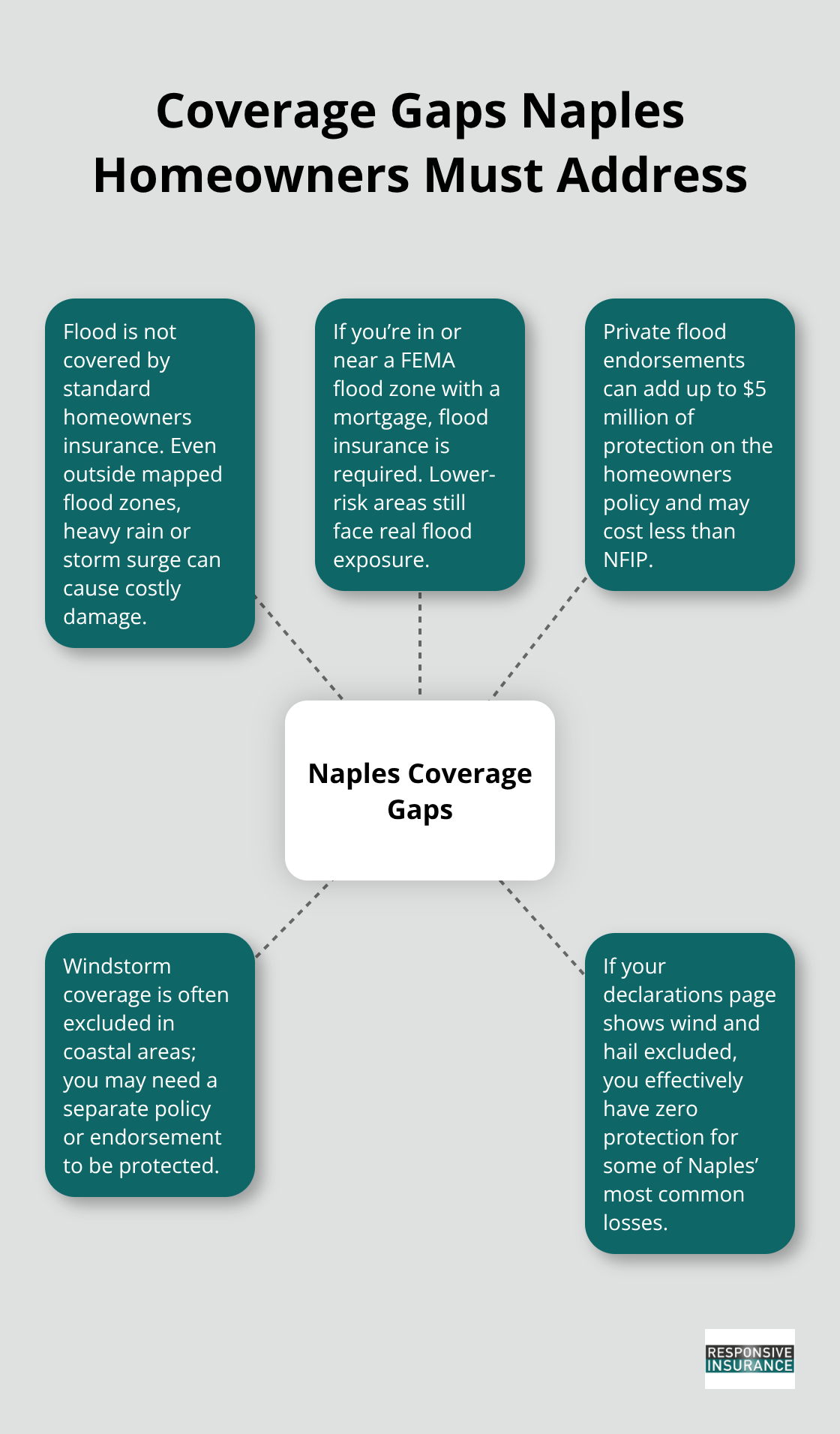

Flood damage is not covered by standard homeowners insurance, period, and this is where most Naples homeowners face a coverage gap. If you’re in or near a FEMA-designated flood zone, you’re legally required to carry flood insurance if you have a mortgage, but many homeowners in lower-risk zones skip it and regret that decision when heavy rain or storm surge causes damage. Private flood endorsements, available through carriers like Tower Hill, can add up to $5 million in flood protection directly to your homeowners policy and often cost less than standalone National Flood Insurance Program policies.

Windstorm coverage is another gap you can’t ignore. Standard homeowners policies often exclude wind and hail damage in high-risk coastal areas, so you need either a separate windstorm policy or a windstorm endorsement added to your homeowners policy. Check your current declarations page-if it says wind and hail are excluded, you have zero protection against what could be your most common loss in Naples. These gaps in standard coverage shape how you’ll approach comparing policies and selecting the right carrier for your situation.

What Coverage Types Matter Most in Naples

Dwelling Coverage Sets Your Protection Foundation

Dwelling coverage protects the physical structure of your home-the roof, walls, foundation, built-in appliances, and attached systems like HVAC and plumbing-but it does not cover the contents inside. Most Naples homeowners make critical mistakes here. You need dwelling coverage set to your home’s actual replacement cost, not its market value. A home you bought for $450,000 might cost $550,000 to rebuild because reconstruction costs in Southwest Florida range from $150–$180 per square foot.

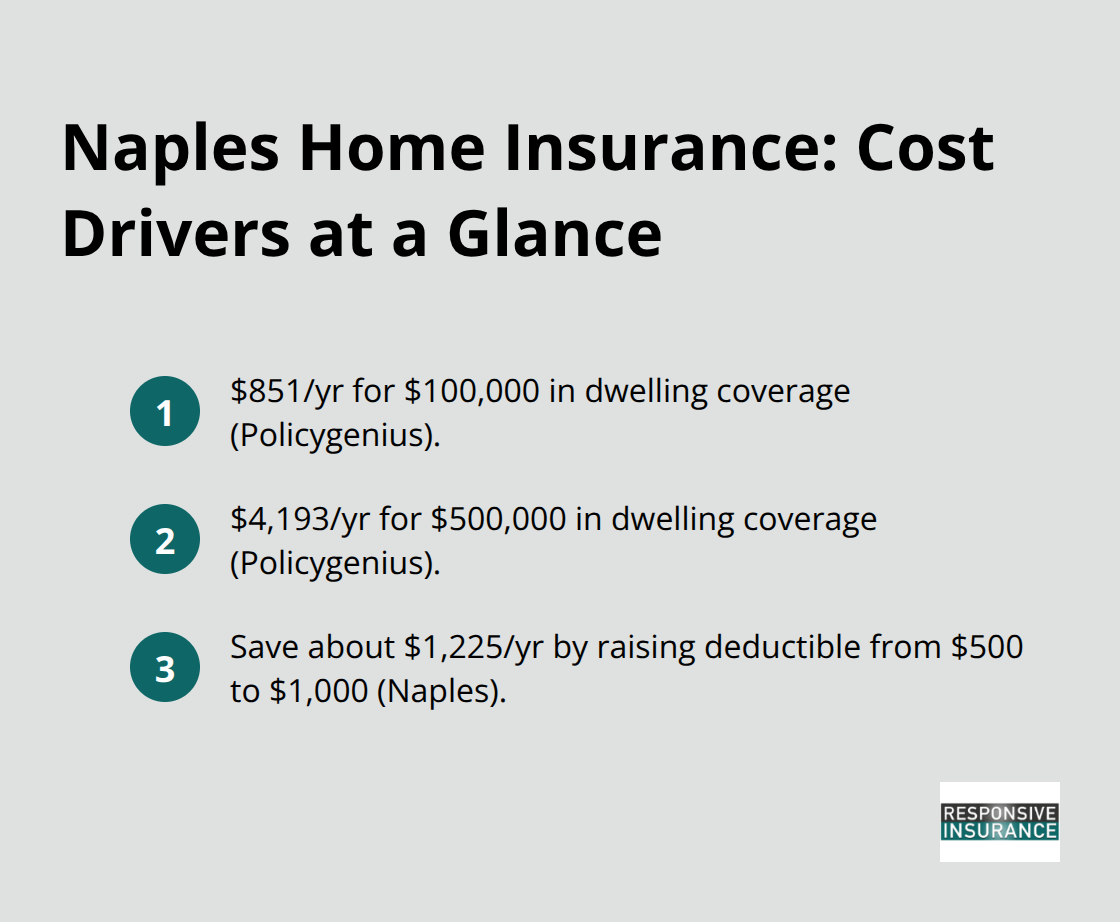

The numbers tell a clear story. According to Policygenius, a Naples home with $100,000 in dwelling coverage costs around $851 yearly, while $500,000 in dwelling coverage runs approximately $4,193 annually. The relationship is direct and substantial. Your deductible choice matters enormously. Choosing a $1,000 deductible instead of $500 saves you roughly $1,225 per year in Naples, according to Policygenius data.

That’s a meaningful reduction if your financial situation allows you to absorb a higher out-of-pocket cost when a loss occurs.

Personal Property Coverage Protects What You Own

Personal property coverage operates independently from dwelling coverage and protects your belongings-furniture, electronics, clothing, kitchen items. Your belongings are covered at a percentage of your dwelling limit, typically 50 to 70 percent. If you have $300,000 in dwelling coverage, personal property might cover only $150,000 to $210,000 of your possessions. High-value items face even stricter limits; jewelry, art, and collectibles are often capped at $1,500 to $2,500 per item under standard policies.

A scheduled personal property endorsement removes these artificial caps and covers specific valuable items at their full replacement cost. This endorsement is essential if you own anything irreplaceable or worth more than those standard limits. Without it, a loss of expensive jewelry or artwork leaves you significantly underprotected.

Liability Coverage Shields Your Financial Assets

Liability coverage protects you when someone is injured on your property or you accidentally damage someone else’s property. This protection is often underestimated by Naples homeowners. Florida has no legal minimum, but carrying at least $300,000 is standard in Naples. Most homeowners stop there and miss a critical gap.

If your net worth exceeds $500,000, a personal umbrella policy adding $1 million in additional liability protection costs surprisingly little-often $150 to $300 annually. This umbrella sits above your homeowners liability limit and activates when that limit is exhausted. Without it, a serious injury lawsuit exposes your personal assets directly. A lawsuit from a guest who falls on your property or a neighbor whose fence you damage could otherwise devastate your finances.

Coordinating Coverage Types for Complete Protection

These three coverage types work together but operate independently, and getting each one right prevents costly gaps when loss occurs. Dwelling coverage protects your structure, personal property coverage protects your belongings, and liability coverage protects your finances. Most Naples homeowners carry these three elements, but they often carry them at levels that don’t match their actual situation. A contractor or appraiser who understands current Southwest Florida building costs can provide a professional home valuation to set your dwelling coverage correctly. An inventory of your belongings helps you understand whether your personal property limit is adequate. Your net worth and lifestyle determine whether you need an umbrella policy.

Once you understand what coverage types matter and what levels make sense for your home and financial situation, the next step is comparing what different carriers actually offer and finding the policy that delivers the protection you need at a price that fits your budget.

Comparing Policies and Finding the Best Fit

Shopping for Naples homeowners insurance without comparing multiple carriers is like accepting the first price quote on a home renovation-you’re almost certainly overpaying. The Naples insurance market shifts constantly, and what was competitive last year may be significantly more expensive this year. Policygenius data shows that premiums for identical coverage vary by thousands of dollars across carriers in Naples. State Farm averages around $2,016 annually for comparable coverage, while Tower Hill runs approximately $709 yearly-a difference of $1,307 that reflects how dramatically carrier selection impacts your costs.

Get Quotes from Multiple A-Rated Carriers

You need quotes from at least three A-rated insurers to understand what the market actually offers. State Farm carries an AM Best A++ rating, Tower Hill holds a B rating, and Universal Property also rates B, so financial stability exists across multiple options. Request quotes with the same dwelling coverage amount, deductible, and coverage limits so you’re actually comparing apples to apples. Most Naples homeowners focus only on the annual premium and miss critical differences in what’s actually covered. One carrier might include windstorm coverage in the base policy while another requires a separate endorsement. Some offer private flood protection up to $5 million on the homeowners policy itself, while others force you into the National Flood Insurance Program, which often costs more and covers less. These coverage gaps determine whether a lower premium actually represents better value or just means you’re paying less for worse protection.

Understand How Deductibles Control Your Costs and Risk

Your deductible choice matters far more than most homeowners realize because it directly controls both your premium and your out-of-pocket risk. Increasing your deductible from $500 to $1,000 saves approximately $1,225 annually in Naples according to Policygenius, but only if you can comfortably absorb that $1,000 when a loss occurs. This trade-off between lower premiums and higher out-of-pocket costs requires honest assessment of your financial situation. If you have substantial savings and can handle a $1,000 deductible without stress, the annual savings justify the higher deductible. If a $1,000 unexpected expense would strain your budget, the lower deductible protects your finances even though you pay more annually.

Leverage Bundling and Carrier-Specific Discounts

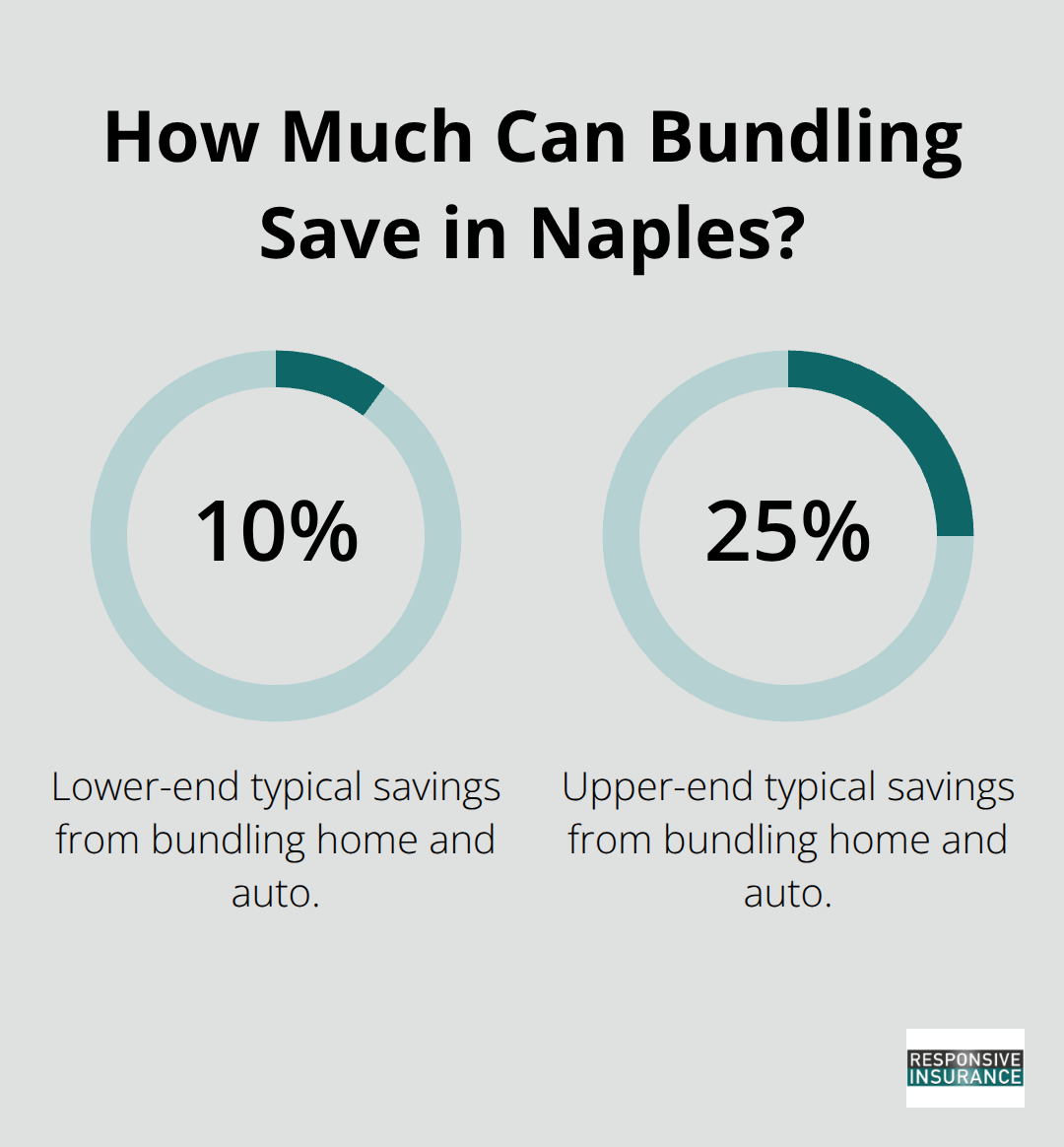

Bundling your home and auto insurance with the same carrier typically unlocks 10 to 25 percent in combined savings, which often exceeds any premium difference between carriers. If you’re paying $2,016 at State Farm for home insurance and another $1,200 for auto elsewhere, bundling might save you $300 to $600 yearly across both policies. Ask each carrier specifically about discounts for security systems, impact-resistant windows, newer roofs, hurricane shutters, and claims-free history-these discounts vary substantially.

Some carriers offer 5 percent for a security system while others offer 15 percent. Universal Property explicitly covers homes up to 70 years old with older roofs, which matters if you own an older Naples property that other carriers won’t even quote.

Recognize When Citizens Property Insurance Becomes Your Only Option

Citizens Property Insurance, the state’s insurer of last resort, averages $6,281 annually-roughly three times what competitive private carriers charge-so exhausting private options before turning to Citizens is financially critical. You land in Citizens only when private carriers decline to quote your home, typically because of age, condition, location, or claims history. This backstop protects homeowners who can’t find coverage elsewhere, but the cost reflects the higher risk that private carriers won’t accept. Spending two hours to obtain three solid quotes with identical coverage specifications prevents you from overpaying at Citizens when private options still exist.

Compare Total Value, Not Just Price

Price alone tells an incomplete story about what you’re actually purchasing. One carrier might charge $1,800 annually but exclude wind coverage, while another charges $2,100 but includes it. The second carrier costs more but delivers better protection for Southwest Florida’s actual risks. Tower Hill’s private flood endorsement (up to $5 million) on the homeowners policy itself often costs less than standalone National Flood Insurance Program policies, which cover less and cost more. Universal Property’s willingness to insure older homes means you might find competitive rates where other carriers won’t quote at all. Compare not just price but what each carrier actually covers for wind, flood damage, and other critical protections.

Final Thoughts

Securing adequate home coverage in Naples requires three concrete steps that take only a few hours but prevent years of regret when a loss occurs. First, get your dwelling coverage amount right by consulting a local contractor or appraiser who understands current Southwest Florida reconstruction costs. Second, inventory your personal belongings and determine whether standard coverage limits protect what you actually own, or whether a scheduled personal property endorsement makes sense. Third, assess your liability exposure honestly and add an umbrella policy if your net worth justifies the protection.

Working with a local independent agent transforms this process from overwhelming to manageable because they understand Naples homeowners insurance options and Southwest Florida’s specific risks in ways that online shopping cannot replicate. An agent explains why flood coverage matters even if you’re not in a mapped flood zone, why windstorm endorsements are non-negotiable, and which carriers actually deliver on claims after a hurricane. They access multiple A-rated carriers simultaneously, compare coverage specifications alongside price, and identify discounts you’d miss shopping alone.

At Responsive Insurance, Inc., we work with multiple A-rated insurance companies to compare coverage and find the best fit for your specific situation (as an independent agency based in Naples, we understand the risks that matter here and the coverage gaps that catch homeowners off guard). Contact us to discuss your Naples homeowners insurance options and build a policy that actually protects what matters to you.