Florida Hurricane Insurance Requirements: What to Prepare For

Living in Naples, Florida means understanding that standard homeowners insurance often falls short when hurricanes strike. Florida hurricane insurance requirements exist for good reason-they protect both you and your lender when storms hit.

At Responsive Insurance, Inc., we’ve helped countless homeowners navigate these requirements and close coverage gaps before disaster strikes. This guide walks you through what you need to know and do right now.

Why Hurricane Coverage Matters in Florida

Wind Damage and Hurricane Deductibles

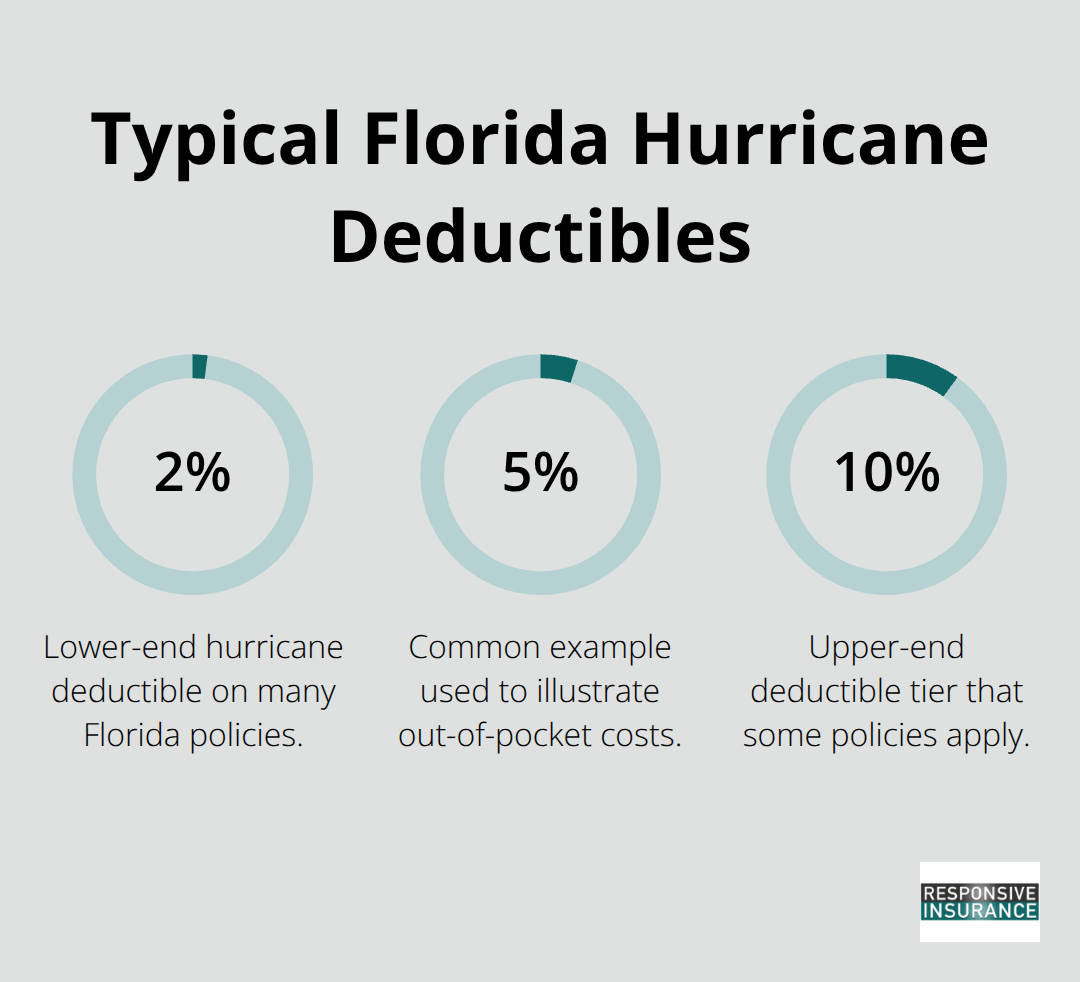

Florida’s coastal location and frequent hurricane activity make specialized insurance requirements non-negotiable. Standard homeowners policies cover wind damage to your home’s structure, but the coverage comes with a separate hurricane deductible that typically ranges from 2% to 10% of your home’s insured value. For a home insured at $400,000, a 5% hurricane deductible means you’d pay $20,000 out of pocket before coverage kicks in. This deductible amount can shock homeowners who expect their standard policy to protect them fully when a storm hits.

Flood Coverage Gaps You Cannot Ignore

Flood damage receives zero protection under standard homeowners insurance. Since hurricanes frequently bring storm surge and flooding, most Naples homeowners need additional flood coverage through the National Flood Insurance Program or private insurers. The average Florida flood insurance policy costs around $700 annually, though coastal properties in high-risk zones regularly exceed $2,000 per year depending on elevation and flood zone designation. Without this separate policy, a single hurricane can leave you financially devastated.

Rising Costs in Florida’s Shifting Insurance Market

The insurance market in Florida has shifted dramatically over the past five years. Many national carriers have reduced their exposure after high claim volumes, pushing more policies toward state-run carriers and regional insurers that often charge higher premiums or offer more restrictive terms. The average Florida homeowners premium now ranges from $2,000 to over $6,000 annually, with hurricane coverage comprising a significant portion. Proximity to the coast drives these costs substantially higher-Naples and other coastal cities pay considerably more than inland areas like Gainesville.

Windstorm Insurance as a Separate Requirement

If your current homeowners policy doesn’t explicitly include wind damage coverage, you’ll need to purchase separate windstorm insurance, which averages around $2,600 annually in coastal Florida. This additional layer of protection addresses a critical gap that many homeowners overlook until it’s too late. At Responsive Insurance, Inc., we work with multiple A-rated insurance companies to help Naples homeowners find coverage that actually fits their risk profile and budget rather than accepting whatever a single insurer offers.

Taking Action Before Hurricane Season

The critical step is reviewing your current policy now to confirm what’s covered, what isn’t, and whether your deductible amounts align with your emergency savings. This assessment becomes the foundation for the home hardening measures and insurance adjustments you’ll want to complete before the first storm threatens the coast.

Strengthen Your Home and Coverage Before Storm Season

Install Hurricane-Resistant Upgrades

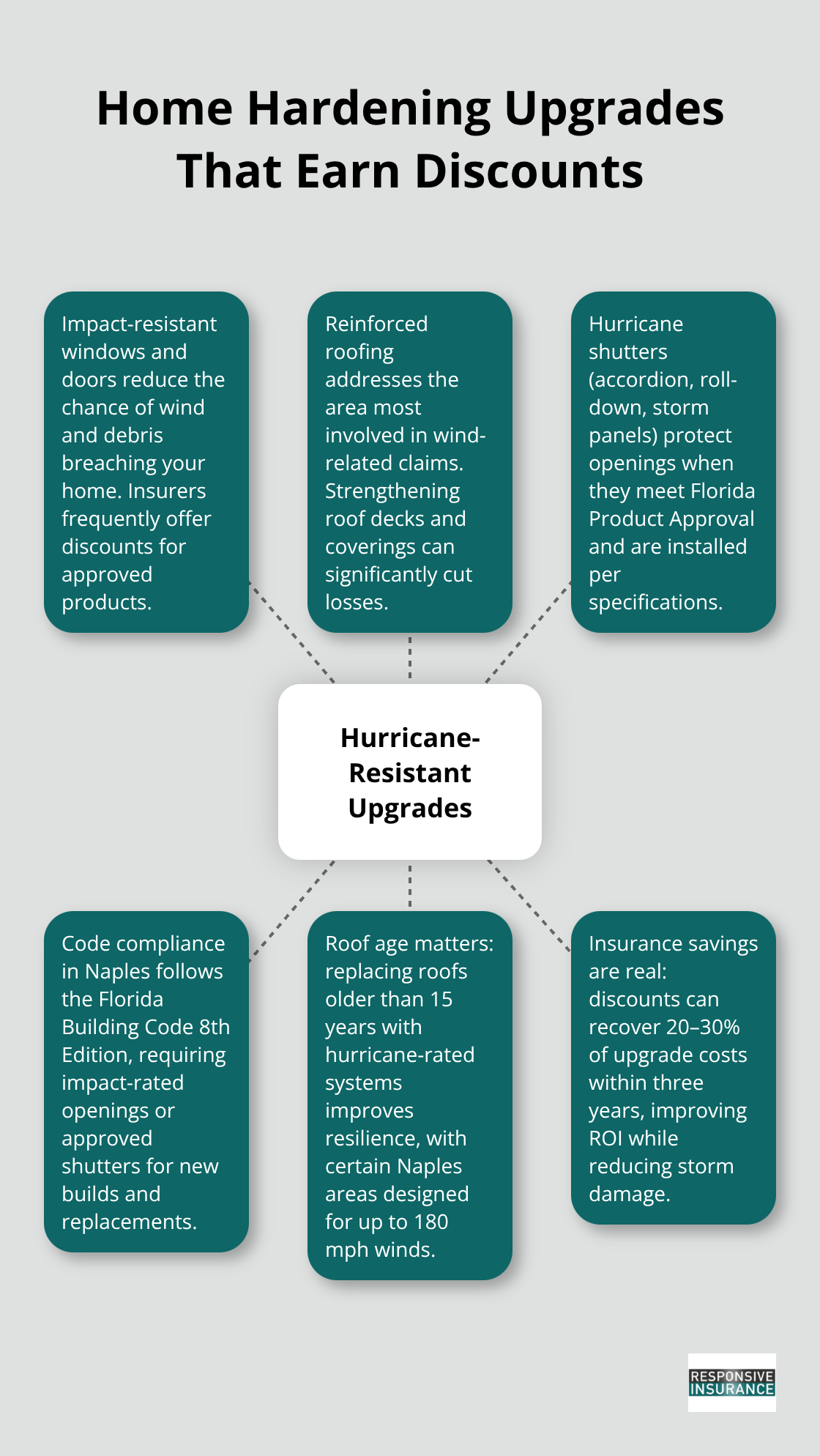

The weeks leading up to hurricane season offer a limited window to make meaningful improvements that lower both your risk and your insurance costs. Home hardening investments directly reduce the damage hurricanes inflict, and insurance companies reward these improvements with tangible discounts. Impact-resistant windows and doors, reinforced roofing, and properly installed hurricane shutters address the most vulnerable points where wind and debris enter homes.

The Florida Building Code 8th Edition, adopted in Naples as of December 31, 2023, requires all windows and doors in new construction to be impact-rated or shielded by approved shutters, and these same standards apply when you replace windows or doors on existing homes. Accordion shutters, roll-down shutters, and storm panels all qualify if they meet Florida Product Approval standards and are installed per manufacturer specifications.

Installing these upgrades costs between $3,000 and $10,000 depending on your home’s size and window count, but insurance discounts typically recover 20 to 30 percent of that investment within the first three years. Roof reinforcement matters equally because wind-related claims predominantly involve roof damage. If your roof exceeds 15 years old, replacing it with a hurricane-rated system qualifies for additional discounts and significantly improves your home’s ability to withstand 180 mph winds, which is the design standard for certain Naples locations under current building code requirements.

Review Your Insurance Before Making Upgrades

Your insurance review must happen before you make any home improvements so that you understand exactly what coverage gaps exist and what discounts you’ll qualify for after upgrades are complete. Contact your current insurer or work with an independent agency to obtain a detailed breakdown of your hurricane deductible amount in dollars, your flood insurance status, and whether your windstorm coverage is included or requires a separate policy. An independent agency like Responsive Insurance, Inc. works with multiple A-rated insurance companies, allowing you to compare coverage options and find the best fit for your specific situation rather than accepting whatever a single insurer offers.

Document Your Property and Belongings

Document your home’s contents and condition now through photographs and video, storing copies in a secure location separate from your home (such as cloud storage or a safe deposit box). Photograph the exterior including roof condition, siding, and foundation, then move inside to document furniture, electronics, appliances, and valuable items with close-ups showing brand names and condition. This documentation becomes invaluable if you need to file a claim after a storm, as it establishes what you owned and its condition before damage occurred.

Capture Insurance Discounts After Improvements

Once improvements are complete, request updated insurance quotes to capture the discounts your new shutters, windows, or roof now qualify for, and confirm that your flood insurance reflects your actual flood zone designation rather than a generic or outdated assessment. FEMA notes that help can take three days or longer to arrive after a major hurricane, which underscores why advance preparation prevents financial catastrophe. With your home hardened and your coverage optimized, you’re positioned to respond effectively when hurricane season arrives.

When Hurricane Season Arrives

Prepare Your Home and Family in the Final 48 Hours

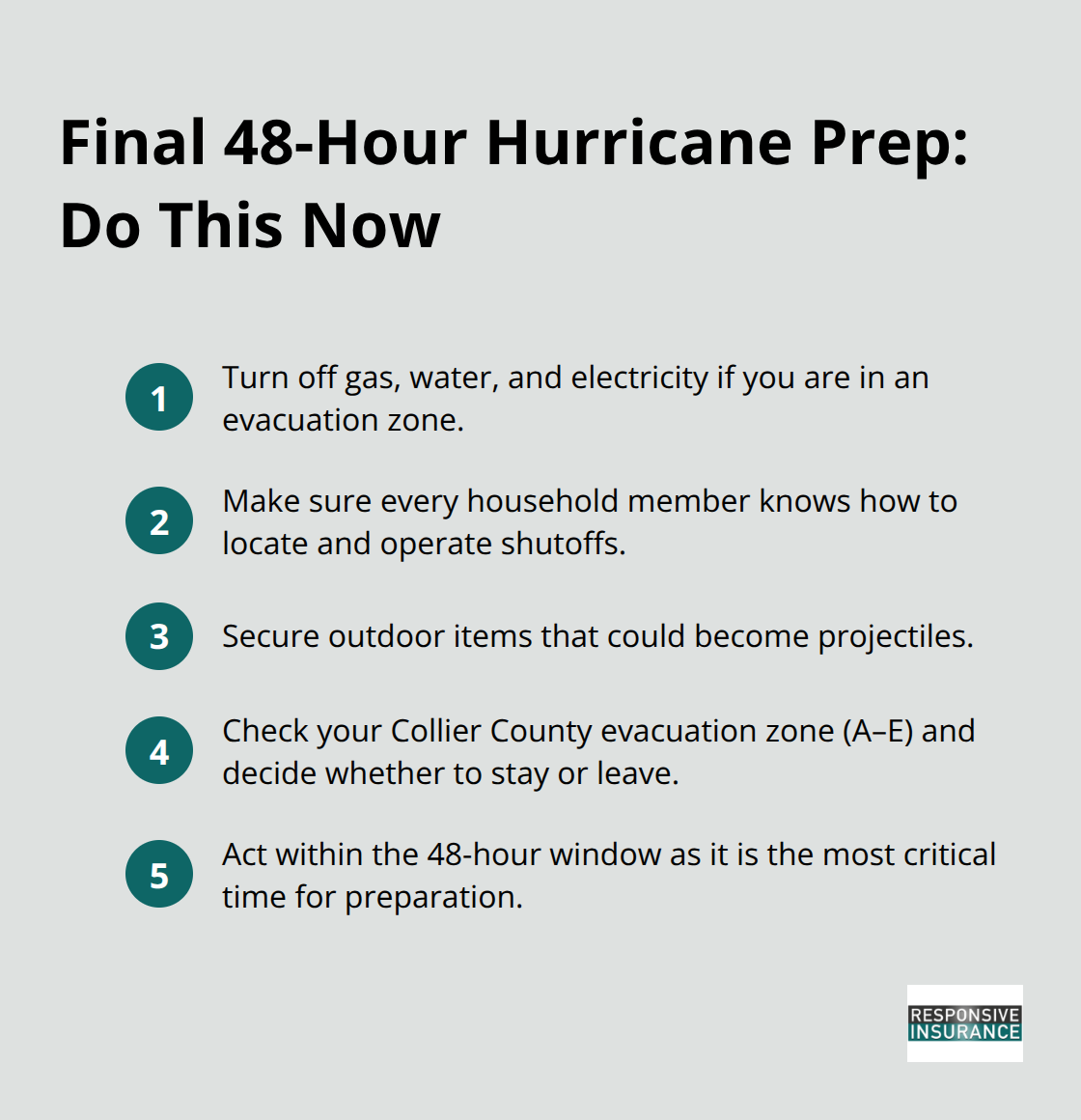

The 48 hours before a hurricane hits your area represent the most critical window for action. FEMA recommends that you turn off gas, water, and electricity if you’re in an evacuation zone, so every household member needs to know how to locate and operate these shutoffs in advance. Secure all outdoor objects that could become projectiles, including trash cans, patio furniture, and loose landscaping materials. Check your evacuation zone immediately using the Collier County Evacuation Zone Map, as zones are designated A through E based on storm surge risk rather than storm category, and this determines whether you stay or leave.

Stay Informed and Evacuate When Ordered

Sign up for emergency alerts through Everbridge and follow official channels including the City of Naples government, Naples Fire-Rescue, and Naples Police for real-time storm information. Your vehicle should be in good working condition with a full tank of gas, and you need an emergency supply kit assembled for at least five days since FEMA notes help can take three days or longer to arrive after a major hurricane. Create a family communication plan with an out-of-state contact number that everyone memorizes, and designate a safe destination outside the storm’s path before warnings are issued. Know which shelters accept pets in your area, as Collier County pet-friendly shelters require preregistration by contacting Emergency Management at 239-252-3600.

Document Damage and Contact Your Insurer Immediately

When damage occurs, your insurance claim starts with documentation you collected before the storm and photographs or video taken immediately after the damage is visible but before cleanup starts. Contact your insurance company within 48 hours of damage discovery, not weeks later, and request a specific claim number for reference. The insurer will assign an adjuster who inspects your property, but you should also obtain independent repair estimates from licensed contractors to compare against the adjuster’s assessment.

Challenge Inadequate Claim Payouts

If your claim is denied or the payout seems inadequate, you have the right to request a detailed explanation of the denial, gather additional evidence, and negotiate directly with the insurer. Do not accept underpayment without question, as many homeowners settle for less than they’re entitled to receive. If disputes continue, consult an experienced hurricane claims attorney who can review your policy, challenge lowball estimates, and pursue legal action if necessary.

Navigate Rebuilding Requirements and Compliance

Throughout recovery, follow official guidance from FEMA and local authorities regarding permits and rebuilding standards, as Naples requires permits for restoration work including drywall, trim, electrical repairs, and window or shutter replacement. The FEMA 50% Rule states that if repair costs exceed 50% of your home’s market value in special flood hazard areas, the entire structure must comply with current floodplain regulations, potentially requiring foundation raising or floodproofing. Non-compliance can affect future insurance eligibility and resale value, making it essential to understand these requirements before reconstruction begins.

Final Thoughts

Florida hurricane insurance requirements protect you and your lender when storms strike, but understanding these requirements demands action before hurricane season arrives. The gaps in standard homeowners policies-hurricane deductibles ranging from 2% to 10% of your home’s value, zero flood coverage, and windstorm insurance that may require a separate policy-create real financial exposure that preparation prevents. Your strategy combines three essential steps: review your current coverage to identify what’s protected and what isn’t, invest in home hardening measures that reduce damage and qualify for insurance discounts, and document your property and belongings before any storm arrives.

When hurricane season arrives, the 48-hour window before a storm hits determines whether you evacuate safely and protect your family. After damage occurs, your documented property inventory and immediate contact with your insurer within 48 hours become the foundation of your claim. If your claim is denied or underpaid, you have the right to challenge it and pursue additional compensation through negotiation or legal action.

Navigating Florida hurricane insurance requirements alone creates unnecessary stress and risk that an independent agency eliminates. We at Responsive Insurance, Inc. work with multiple A-rated insurance companies to compare coverage options and find solutions that fit your home’s risk profile and your budget. Contact us today to review your current coverage, identify gaps, and implement the protection strategy that gives you confidence when storms approach.