![Florida Home Insurance Quotes [2026 Guide]](https://responsiveinsurance.com/wp-content/uploads/emplibot/Florida-Home-Insurance-Quotes-_2026-Guide__1770848603-1030x589.jpeg)

Florida Home Insurance Quotes [2026 Guide]

Finding the right Florida home insurance quotes takes more than a quick online search. You need to understand what coverage you actually need, how rates are calculated, and which insurers offer the best value for your situation in Naples.

At Responsive Insurance, Inc., we’ve helped countless homeowners navigate Florida’s unique insurance landscape. This guide walks you through everything from state requirements to rate factors that directly impact your premiums.

What Florida Actually Requires for Home Insurance

Your mortgage lender mandates that you carry homeowners insurance before closing on a property, and that coverage must include at least enough to rebuild your home’s structure. This isn’t optional-it’s a condition of your loan. Florida itself doesn’t require homeowners insurance by law, but lenders do, and most homeowners in Naples carry policies that go well beyond the minimum. Standard homeowners policies in Florida cover the dwelling structure, personal property inside the home, liability protection if someone is injured on your property, and additional living expenses if you need temporary housing after a covered loss. However, while you’re automatically covered for wind damage in a standard HO-3 policy in Florida, you do have the option to exclude it to save on premiums. Flood coverage is almost never included in standard homeowners policies anywhere in the country, so you must purchase flood insurance separately through either private carriers or the National Flood Insurance Program.

Wind and Flood Coverage in Naples

Many Naples homeowners assume their standard policy covers everything after a hurricane hits. It doesn’t. Wind and flood coverage is critical in Naples because you may need separate coverage depending on your policy choices. If you live near the coast or in a flood zone, you need mandatory separate flood coverage. Tower Hill offers a private flood endorsement up to $5 million as an add-on to its standard policy, which supplements coverage in flood-prone areas. Shopping for private flood insurance alongside the National Flood Insurance Program gives you options and often reveals significant savings compared to NFIP alone.

How Deductibles Impact Your Costs

Your deductible choice directly affects your annual premium. Moving from a $500 deductible to $1,000 in Naples can save around $1,000 annually, which is substantial enough to affect your overall coverage strategy. This savings allows you to redirect funds toward additional coverage or other financial priorities. Higher deductibles work best for homeowners who can afford out-of-pocket costs if a claim occurs.

Understanding Coverage Limits and Premiums

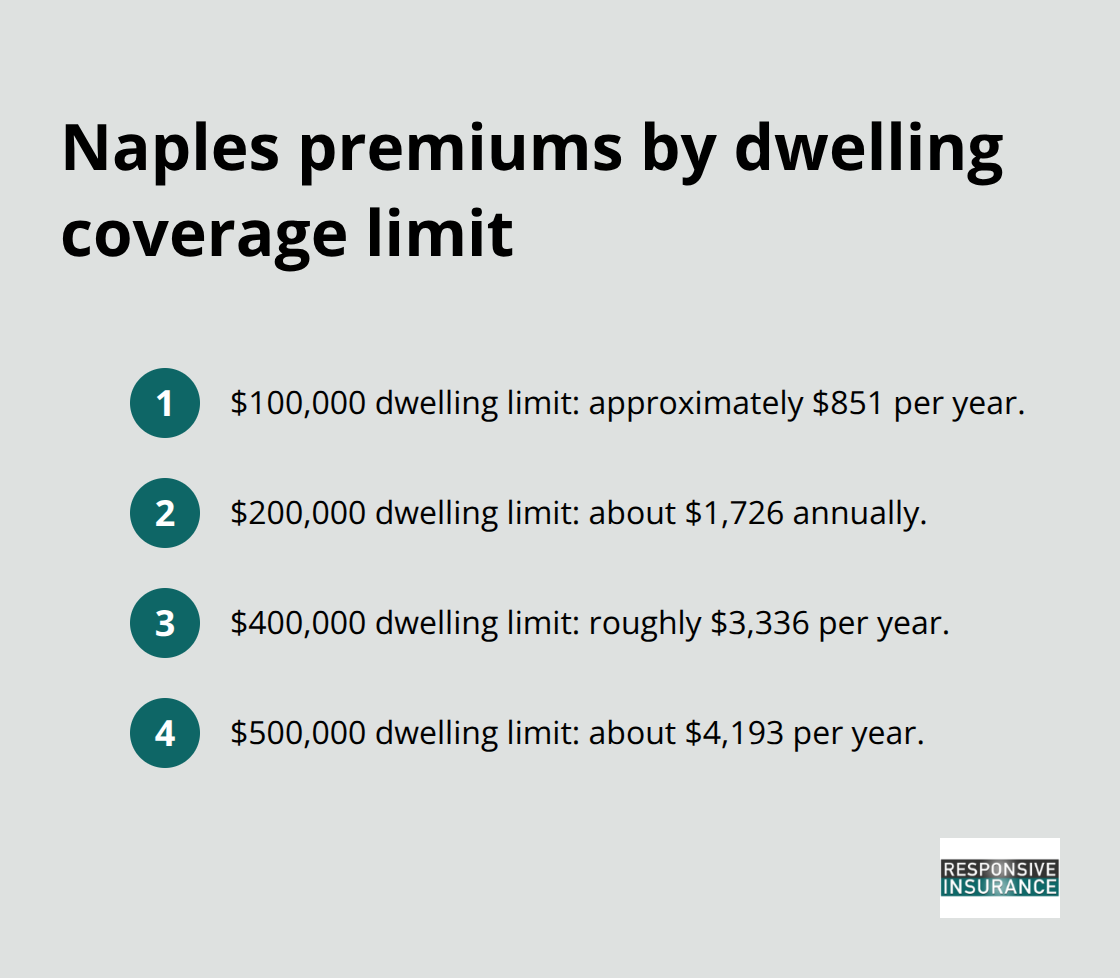

The dwelling coverage amount you select directly impacts your annual premium. In Naples, a $100,000 dwelling limit runs approximately $851 per year, while $200,000 costs about $1,726 annually. Jump to $400,000 and you’re paying roughly $3,336 per year, and $500,000 reaches about $4,193 per year. These figures matter because underinsuring your home creates real financial risk if you need to rebuild.

Additional Coverage Types That Protect You

Personal property coverage protects your belongings inside the home, loss of use coverage pays for temporary housing and living expenses while repairs happen, and personal liability protects you if someone is injured on your property and sues. In Naples, homes built after 2001 generally cost less to insure than older homes, and living in a gated community can lower your premiums compared to non-gated neighborhoods. Your home’s replacement cost varies based on interior materials and flooring choices, so working with an agent who assesses your specific home’s value produces more accurate quotes than relying on online calculators. Understanding these coverage types helps you make informed decisions about what protection level fits your situation and budget.

Getting Your Naples Home Insurance Quotes Right

Prepare Your Home Information Before Requesting Quotes

Gathering the right information before requesting quotes saves time and produces more accurate premium estimates. Start with your home’s basic details: the year it was built, square footage, number of stories, roof type and age, and construction materials. Insurers in Naples care deeply about roof age because even roofs under 20 years old can trigger higher rates or limited coverage. Next, document your home’s protective features: impact-resistant windows and doors, security systems, smoke detectors, and any wind mitigation improvements like roof tie-downs or reinforced garage doors. These upgrades can reduce your premium by 20 to 30 percent on top of already-reduced 2026 rates.

Have your mortgage information ready, including your lender’s name and loan amount, because this affects your required coverage limits. Gather your claims history from the past five years, including dates, claim amounts, and what was covered. Your credit score also matters significantly in Naples, as insurers use it to calculate rates. If you have poor credit, Security First Insurance becomes your cheapest option at around $604 per year in Naples, followed by Tower Hill at roughly $1,120 annually. Finally, work with an agent who can assess your specific interior materials and finishes rather than relying on generic online estimates to determine your home’s replacement cost.

Request Quotes from Multiple Carriers

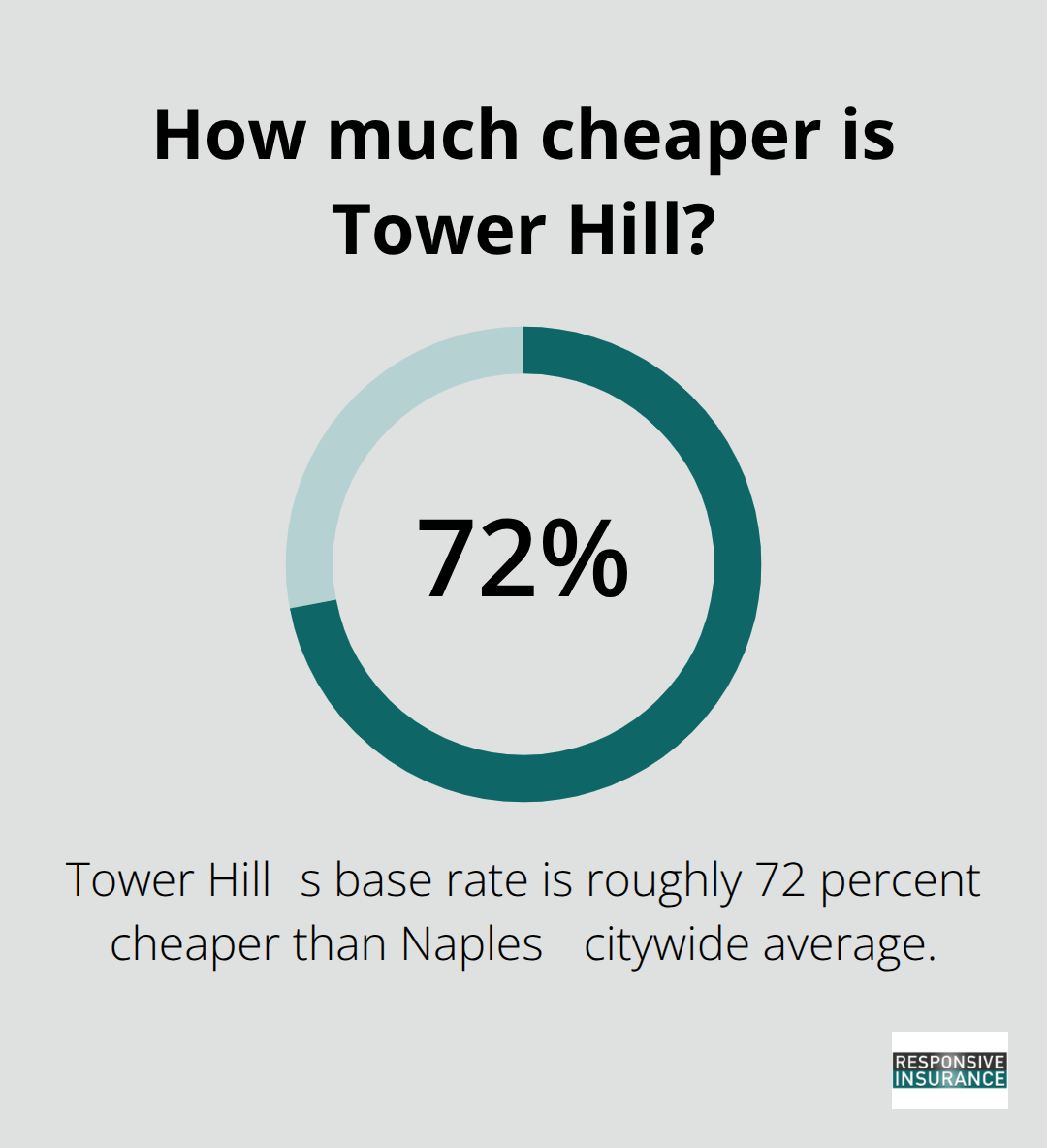

Once you have this information prepared, request quotes from at least three different carriers rather than settling for a single option. The 2026 market shift in Florida brought 17 new insurers into the state, giving Naples homeowners genuine competition that didn’t exist two years ago. State Farm averages around $2,016 annually in Naples with a 4.8 out of 5 customer rating and an A++ financial strength rating from AM Best. Tower Hill delivers much lower base rates at approximately $709 per year, roughly 72 percent cheaper than Naples’ citywide average, though it carries a B rating from AM Best.

Universal Property offers multiple add-ons including private flood coverage up to $5 million and covers homes up to 70 years old, averaging around $3,202 per year in Naples. Citizens Property Insurance, which acts as Florida’s high-risk option, costs about $6,281 annually and should be your last resort since it’s generally used when private carriers decline you.

Examine Coverage Details Beyond the Premium

When comparing quotes, look beyond the annual premium and examine what wind and flood coverage each policy includes or excludes. Many Naples policies exclude wind in high-risk coastal areas, meaning you’ll need separate windstorm insurance. Ask each carrier specifically about their flood endorsement options and private flood insurance limits before deciding. If you’re with Citizens now, have a licensed broker verify whether private-market offers beat your current rate, because the depopulation shift means better options likely exist for your situation. As you evaluate these options and narrow your choices, the next step involves understanding which specific rate factors most heavily influence what each carrier quotes you.

What Really Drives Your Insurance Rate in Naples

Home Age and Roof Condition Shape Your Premiums

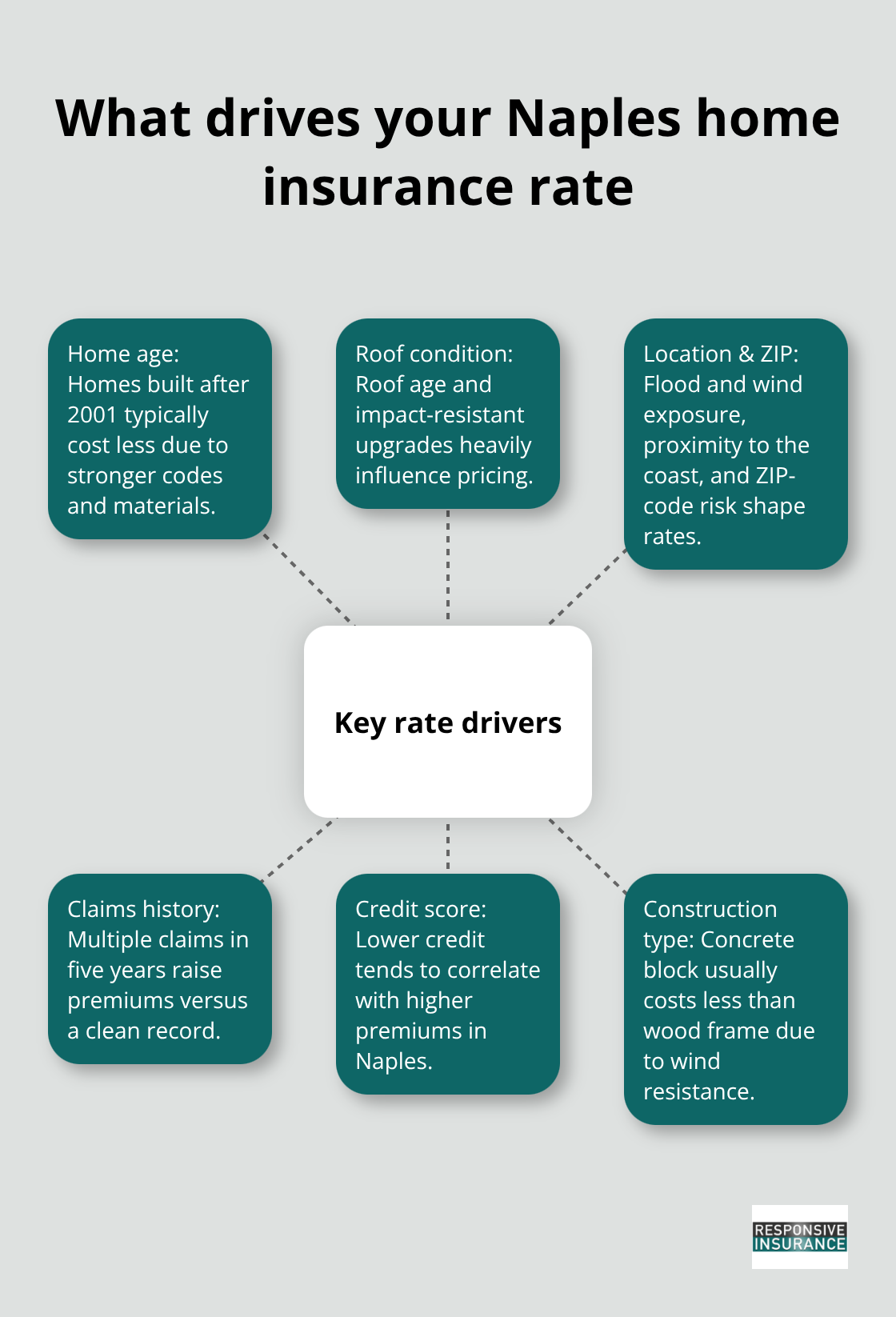

Your home’s age and roof condition are the two biggest factors insurers scrutinize in Naples, and they deserve your immediate attention. Homes built after 2001 cost significantly less to insure than older homes because newer construction meets current building codes and uses modern materials that withstand Florida’s weather better. A 50-year-old home will cost you substantially more than a 25-year-old home, all else equal. Your roof age matters even more than your home’s overall age because insurers know that roofs deteriorate and fail, leading to water damage claims that are expensive to settle.

Even roofs under 20 years old can trigger higher rates or limited coverage options, which is why you should document your roof’s installation date before requesting quotes. If you’ve recently replaced your roof with impact-resistant materials, that upgrade can reduce your premium by 20 to 30 percent on top of the already-reduced 2026 rates Florida is experiencing. Older roofs approaching or exceeding 20 years of age will face coverage restrictions or premium penalties, making roof replacement one of the smartest investments you can make before shopping for insurance. Construction type also influences rates, with concrete block homes costing less to insure than wood frame construction because concrete withstands wind and impact better.

Location and ZIP Code Determine Your Risk Profile

Your location within Naples determines your flood and wind exposure, which directly impacts what you’ll pay annually. ZIP code matters more than most homeowners realize, with rates varying significantly even within Naples neighborhoods. The 34109 ZIP code averages around $2,434 annually while nearby 34102 averages $2,582, a difference of roughly $150 per year driven entirely by location-based risk. Living in a gated community lowers your premiums compared to non-gated neighborhoods because gated properties typically have better security and lower theft claims.

Homes near the coast face higher premiums because wind and flood risks are genuinely greater, and insurers price accordingly. Your specific address tells insurers whether you sit in a flood zone, how close you are to the ocean, and what historical storm damage patterns affect your area. This location-based pricing reflects real differences in claim frequency and severity across Naples neighborhoods.

Claims History and Credit Score Impact Your Rate

Your claims history over the past five years directly affects your rate, with multiple claims signaling higher risk to insurers. A homeowner with three claims in five years will pay substantially more than someone with a clean claims history, even if those claims were legitimate and covered. Your credit score also matters significantly in Naples because insurers use it as a predictor of claim likelihood and payment behavior.

Poor credit can increase your rate by hundreds of dollars annually, which is why Security First Insurance emerges as the cheapest option for Naples homeowners with poor credit at around $604 per year, compared to Tower Hill at roughly $1,120 annually for the same situation. If you have poor credit, focus on improving it before your policy renews because even modest credit improvements can reduce your premium meaningfully when combined with 2026’s competitive market.

Final Thoughts

Finding the right Florida home insurance quotes requires you to understand your home’s specific characteristics, prepare accurate information before requesting quotes, and evaluate coverage options that match your actual risk exposure in Naples. The 2026 market shift has created genuine competition among insurers, giving you leverage to negotiate better rates or switch to carriers that offer superior coverage at lower costs. Your roof age, home construction type, location within Naples, and claims history are the factors that most heavily influence what you’ll pay annually.

Request quotes from at least three different carriers rather than accepting the first offer you receive, and compare not just the premium but the specific wind and flood coverage each policy includes (since many Naples policies exclude wind in high-risk areas). A recent roof replacement or wind mitigation upgrades can reduce your premium by 20 to 30 percent, making these investments worthwhile before you shop for quotes. If you’re currently with Citizens Property Insurance, verify whether private-market options now beat your rate, because the depopulation shift means better alternatives likely exist for your situation.

Working with a local agent who understands Naples’ specific risks produces better outcomes than relying on online calculators alone. At Responsive Insurance, Inc., we work with multiple A-rated insurance companies to compare coverage and find the best fit for your needs, providing the knowledgeable advocacy that helps families in Southwest Florida make confident insurance decisions. Contact us today to discuss your Florida home insurance quotes and discover what coverage truly fits your home and budget.