How to Find Affordable Flood Insurance Florida Rates

Flood insurance in Florida isn’t optional-it’s a financial necessity. Most homeowners in Naples face significant flood risk, and understanding how to secure affordable flood insurance Florida rates can save thousands annually.

We at Responsive Insurance, Inc. know that navigating your options feels overwhelming. This guide breaks down exactly what impacts your premiums and how to lower them.

What Determines Your Flood Insurance Premium in Naples

Your Flood Zone Designation Sets the Foundation

Your flood zone designation is the single biggest driver of your premium, and it’s not negotiable. FEMA’s updated 2024 Flood Insurance Rate Maps for Naples reflect your property’s actual flood risk based on historical data, proximity to water, and elevation. Properties in Zone AE or VE-areas with a 1% annual chance of flooding-face mandatory flood insurance if you have a federally backed mortgage, and your rates reflect that higher risk. The City of Naples participated in the National Flood Insurance Program and updated its maps for the first time since 2012, which means many homeowners saw their risk classifications change. If your property moved from a lower-risk zone to a higher one, your premium increased accordingly.

Check your exact flood zone immediately using the City of Naples interactive flood map tool or contact the City Floodplain Coordinator at 239-213-5039 to confirm your designation. This single step prevents overpaying for coverage you don’t need or underpaying when you do.

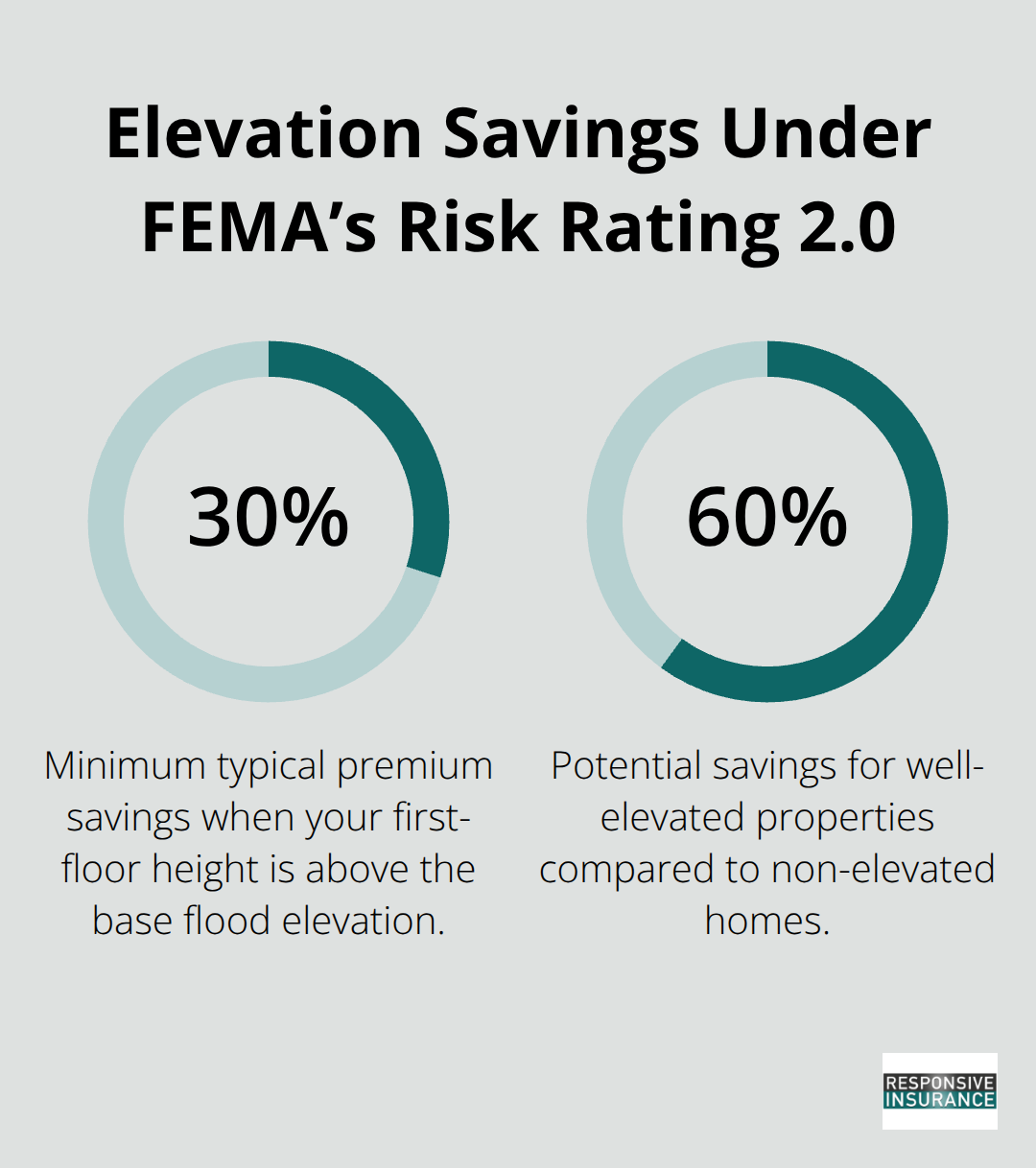

How Elevation Affects Your Rate

Your property’s elevation relative to the base flood elevation matters far more than most homeowners realize. An Elevation Certificate-a document showing your first-floor height compared to the base flood elevation in your zone-can help reduce premiums under FEMA’s Risk Rating 2.0 system. Properties elevated above the base flood elevation save 30-60% compared to non-elevated properties, which uses property-specific data including first-floor height, precise distance to water sources, rebuild cost, and flood history.

This means two nearly identical homes on the same street can have dramatically different premiums based solely on elevation.

If you’ve never obtained an Elevation Certificate, hire a surveyor to prepare one. The cost typically ranges from $300 to $600 but pays for itself through premium reductions within a year or two.

Prior Flood Claims and Mitigation Measures

Historical flood claims on your property directly influence your rate. FEMA’s system tracks whether your home has flooded before, and prior claims result in higher premiums. You can counteract this by implementing flood mitigation measures like raising utilities, installing certified flood vents, or raising the structure itself. These improvements qualify you for significant discounts from insurers and demonstrate to underwriters that you actively reduce risk.

The next section explores how comparing multiple providers and understanding coverage options helps you secure the best rates for your specific situation.

How to Compare Flood Insurance and Cut Your Costs

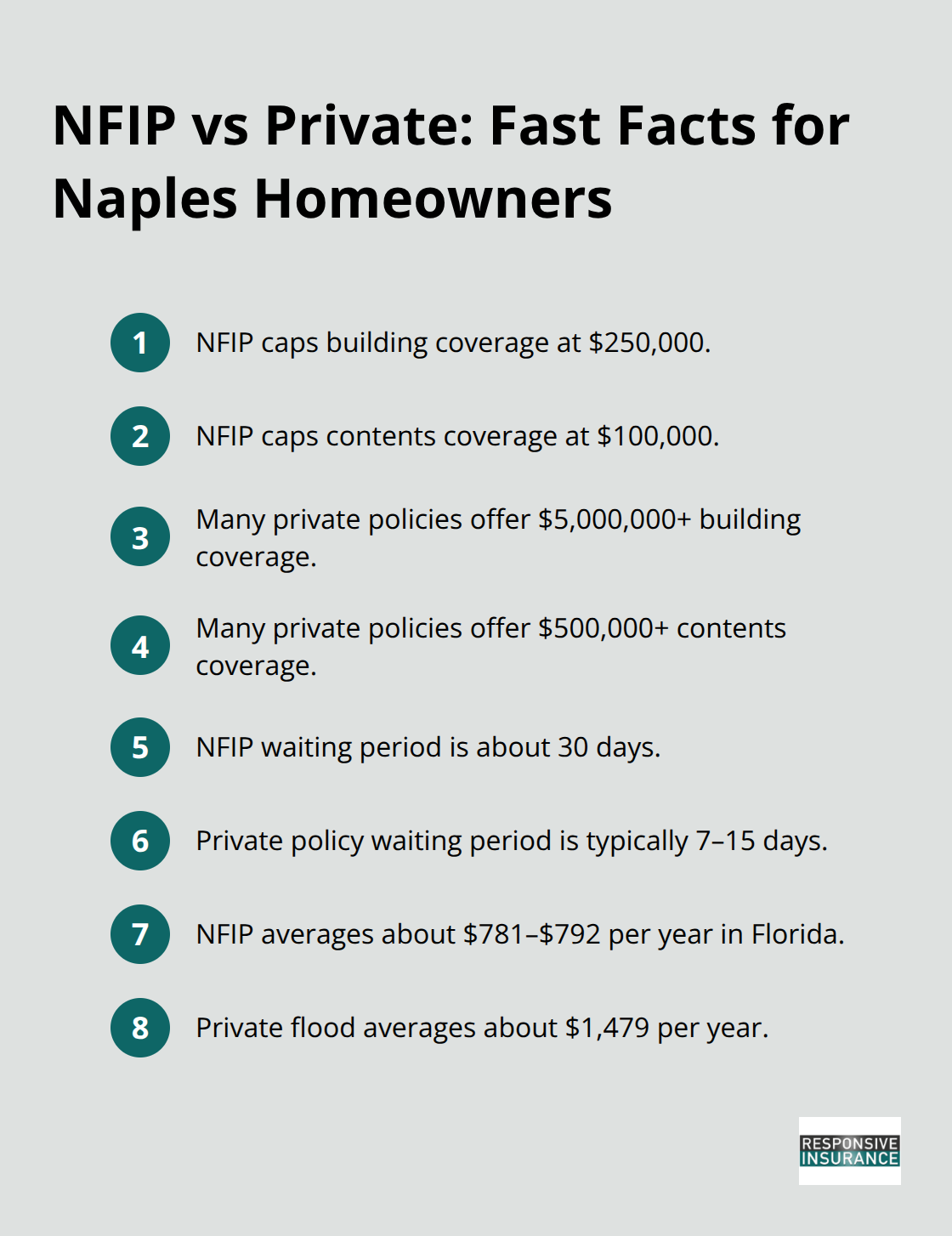

Getting multiple quotes is non-negotiable if you want affordable flood insurance in Naples. The National Flood Insurance Program, delivered through 47 private insurance companies plus NFIP Direct, means you have genuine options, and rates vary significantly between carriers for identical properties. Florida homeowners typically pay around $781–$792 annually through NFIP, while private flood insurance averages about $1,479 per year, but this average masks huge variation based on your specific risk profile. A property in a lower-risk zone might find private coverage cheaper than NFIP, while a coastal home in Zone VE will likely pay less through the federal program.

Getting Your First Quote

Start with a free quote through the NFIP Quote Tool, which provides a personalized estimate based on your address and property details. Then contact local agents representing private carriers to compare their rates side-by-side. When you share your NFIP quote with an agent, they can help you evaluate total costs including deductibles, coverage limits, and waiting periods. NFIP policies take roughly 30 days to activate, while private policies often go into effect within 7–15 days-a difference that matters if you’re buying before hurricane season or a loan closing.

Mitigation Improvements That Lower Premiums

Flood mitigation measures reduce your premiums far more than most homeowners expect. Elevating your home, installing certified flood vents, or raising utilities and mechanical systems qualifies you for substantial discounts from both NFIP and private carriers. An Elevation Certificate alone can save hundreds annually if your property sits above the base flood elevation.

Beyond elevation, flood-proofing steps like sealing walls, installing backflow preventers, or raising the first floor all demonstrate active risk reduction that insurers reward with lower rates. These improvements typically cost between $1,000 and $25,000 depending on scope, but the premium reductions often recoup the investment within five to ten years. Contact the City of Naples Floodplain Coordinator at 239-213-5039 or rdorta@naplesgov.com to discuss which improvements qualify for discounts in your specific flood zone before you invest.

Bundling and Community Discounts

Bundling flood insurance with your homeowners policy yields additional discounts and simplifies administration with a single agent and renewal date. Some insurers offer 10–15% reductions when you combine flood and homeowners coverage, effectively lowering your total insurance cost. Florida Citizens Property Insurance is phasing in flood requirements, with all Citizens homeowners expected to have flood coverage by January 1, 2027, making this bundling strategy increasingly relevant for policyholders in that program. If your community participates in the NFIP Community Rating System, better floodplain management may qualify you for premium discounts through your local jurisdiction. The City of Naples holds a CRS Rating Class 5, which can provide discounts on NFIP premiums for qualifying properties. Contact your flood insurance agent or company to confirm whether your property qualifies for these community-level discounts.

Understanding your options across NFIP and private carriers sets the stage for the next critical decision: determining which program actually works best for your specific situation and risk profile.

NFIP or Private Flood Insurance

Coverage Limits: Where the Programs Diverge Most

The National Flood Insurance Program and private flood insurance offer fundamentally different protection ceilings. NFIP, administered by FEMA and delivered through 47 private insurance companies plus NFIP Direct, caps building coverage at $250,000 and contents coverage at $100,000 for residential properties. Private carriers commonly offer $5,000,000 or more for building coverage and $500,000 or more for contents, with customizable terms that let you tailor protection to your home’s replacement cost. For Naples homeowners, this difference determines whether adequate protection exists at all. A waterfront property worth $2 million cannot be adequately protected under NFIP’s building limit, making private flood insurance necessary regardless of cost. Conversely, a property in a lower-risk zone outside the Special Flood Hazard Area might find NFIP’s lower premiums far more attractive than private options.

Coverage Gaps That Matter in Practice

Coverage exclusions separate the programs just as dramatically as limits do. NFIP policies typically exclude Additional Living Expenses, meaning if a flood forces you from your home, the program won’t cover hotel stays, meals, or temporary housing costs. Many private flood policies include ALE coverage and other endorsements that NFIP doesn’t offer. NFIP also provides limited or no coverage for basements, which creates a dangerous protection gap in Naples where many homes have finished basements vulnerable to flooding. Private carriers often cover basements with higher deductibles or specific endorsements, giving you control over that exposure. These gaps force you to choose between accepting unprotected assets or purchasing supplemental coverage that increases your total cost.

Activation Speed and Timing Considerations

Waiting periods differ significantly between the programs and affect your ability to obtain timely protection. NFIP requires approximately 30 days before coverage activates, while private policies typically go into effect within 7 to 15 days. If you purchase before hurricane season or coordinate with a loan closing, that speed difference determines whether you have protection when you need it. The 30-day NFIP waiting period means you must plan ahead rather than react to weather forecasts or lender requirements at the last moment.

Matching Your Property to the Right Program

The choice between NFIP and private flood insurance isn’t about picking the cheaper option-it’s about matching your property’s actual risk profile to the right carrier and coverage structure. Contact the City of Naples Floodplain Coordinator at rdorta@naplesgov.com or 239-213-5039 to understand your specific flood zone, then use that information to request quotes from both NFIP carriers and private insurers. Comparing actual quotes side-by-side reveals which program delivers real affordability for your situation rather than assuming one is universally cheaper. Your flood zone, property value, and coverage needs determine which program makes financial sense for your home.

Final Thoughts

Finding affordable flood insurance Florida rates requires three concrete actions: verify your exact flood zone, compare quotes from multiple carriers, and invest in mitigation improvements that lower your premiums. Your flood zone designation determines whether you face mandatory coverage and sets your baseline rate, so confirming it through the City of Naples interactive map or the Floodplain Coordinator eliminates guesswork. An Elevation Certificate or flood mitigation measures like raising utilities or installing certified flood vents can reduce your annual premium by hundreds of dollars, making these investments pay for themselves quickly.

Local insurance agents understand Naples flood zones and know which carriers offer the best rates for your risk profile. They compare deductibles, waiting periods, and exclusions across multiple carriers simultaneously, saving you hours of research and preventing costly coverage mistakes. They also track community discounts through the NFIP Community Rating System and identify bundling opportunities with your homeowners policy that lower your total insurance cost.

Contact Responsive Insurance, Inc. to discuss your flood zone, property elevation, and mitigation options so we can match you with the right carrier and coverage structure for your Naples home. Our team provides the local expertise and carrier relationships to secure genuine affordability without leaving gaps in your protection.

![Florida Home Insurance Quotes [2026 Guide]](https://responsiveinsurance.com/wp-content/uploads/emplibot/Florida-Home-Insurance-Quotes-_2026-Guide__1770848603-80x80.jpeg)