Landlord Insurance Florida Cost Breakdown

Owning rental property in Florida comes with significant expenses, and landlord insurance is one of the biggest. The cost of landlord insurance in Florida varies dramatically based on your property type, location, and coverage choices.

At Responsive Insurance, Inc., we’ve helped countless landlords understand where their premiums come from and how to reduce them. This guide breaks down the real numbers so you can make informed decisions about your coverage.

What Drives Your Landlord Insurance Costs

Location and Property Value Set Your Baseline

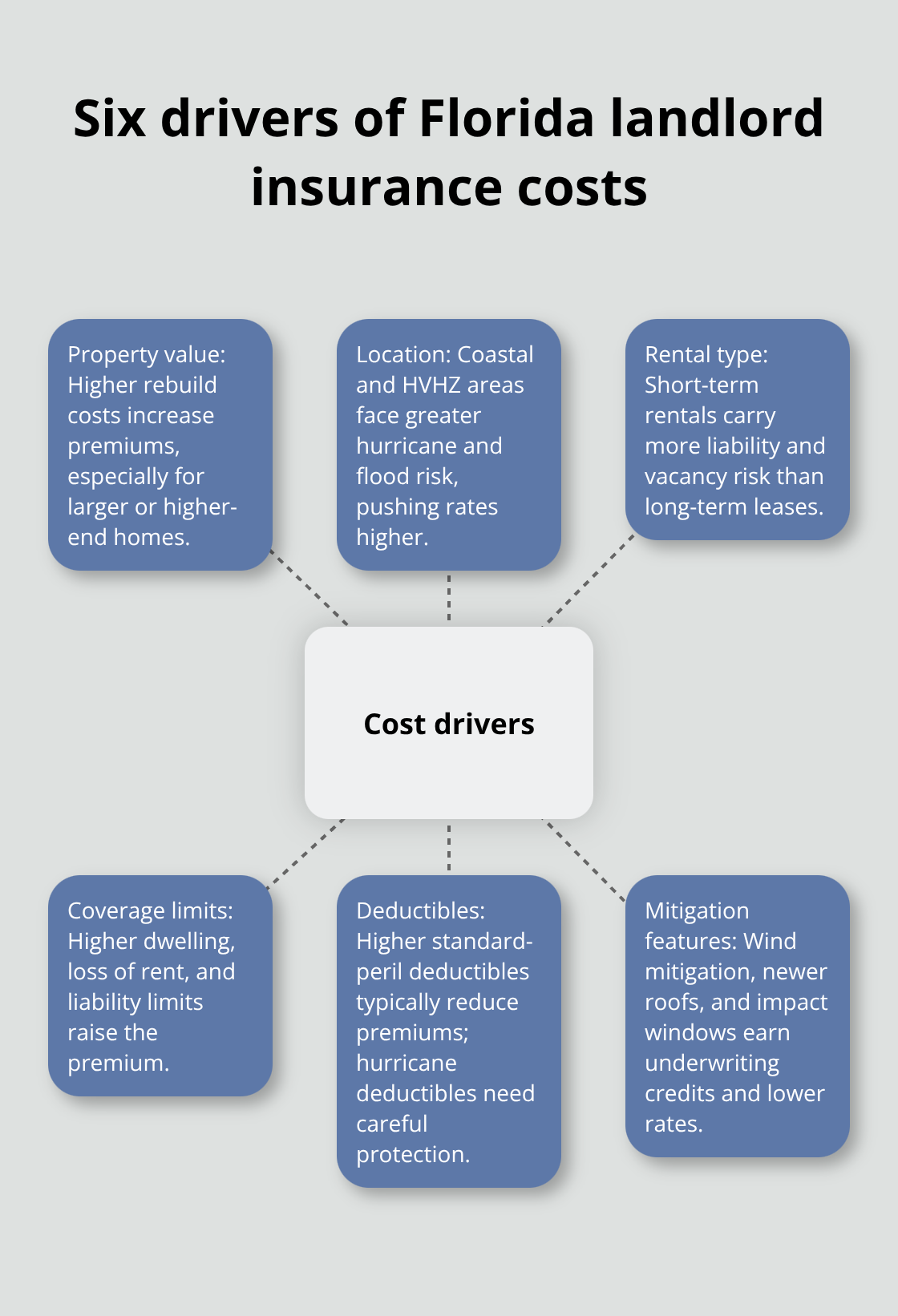

Your landlord insurance premium in Florida isn’t arbitrary. It reflects six concrete factors that insurers measure and price into every quote. Property value and location sit at the top of the list because they determine your replacement cost and exposure to natural disasters. A single-family home worth $400,000 in Tampa will cost significantly less to insure than an identical home in Miami, where hurricane and flood risk are substantially higher. Miami landlords pay around $10,357 annually according to recent rate data, while Orlando properties typically run $1,000 to $3,000 per year, and Tallahassee inland properties average around $1,130. The difference isn’t just weather exposure either. Proximity to the coast, designation in a high-velocity hurricane zone, flood zone classification, and even distance to fire hydrants all factor into your rate.

Property age and construction type matter too. A well-maintained 10-year-old home with a newer roof will underwrite at a lower premium than a 30-year-old property with original materials, because older properties carry higher claim frequency.

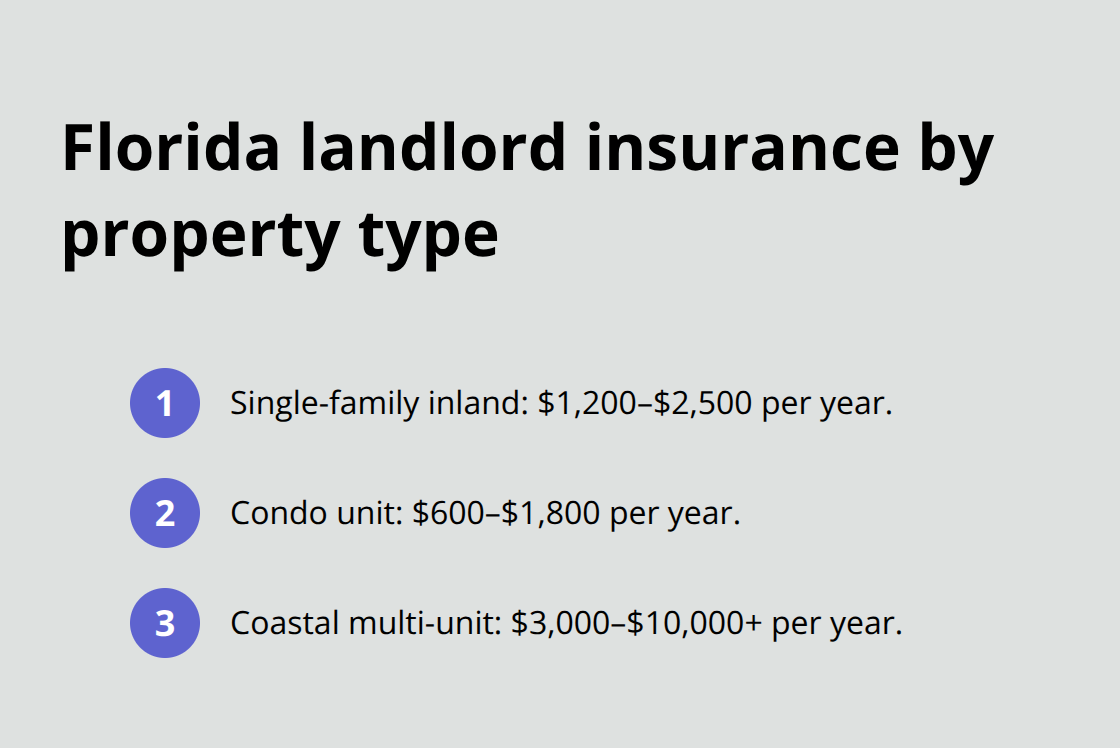

Property Type and Rental Structure Impact Rates

Rental property type shapes costs significantly. A single-family inland rental typically costs $1,200 to $2,500 annually, while a condo unit runs $600 to $1,800, but a coastal multi-unit building can exceed $10,000 per year. Short-term rentals like Airbnb or VRBO properties command higher premiums than long-term leases because tenant turnover increases liability exposure and vacancy risk. Loss of rent coverage keeps your cash flow steady, helping you cover mortgage payments, taxes, and maintenance without tapping into reserves.

Coverage Choices and Mitigation Features Control Costs

Your coverage decisions directly control what you pay. Increasing your deductible from $500 to $2,500 on non-catastrophic claims can meaningfully reduce premiums while you maintain adequate hurricane and flood limits. Wind mitigation features make a measurable difference too. A certified wind mitigation inspection qualifying you for credits can lower your annual premium by hundreds of dollars. Roof-to-wall straps, secondary water barriers, and impact-rated windows aren’t just safety upgrades; they’re premium reduction strategies that underwriters actively reward with rate reductions. Understanding these three cost drivers positions you to evaluate quotes accurately and identify where you can reduce expenses without sacrificing protection.

Average Landlord Insurance Rates in Florida

Cost Breakdown by Property Type

Florida landlord insurance costs split dramatically by property type and location, and understanding these real numbers helps you budget accurately. Single-family inland rentals run $1,200 to $2,500 annually according to industry rate data, making them the most affordable option for most landlords. Condo units cost less because they typically have smaller replacement values, ranging from $600 to $1,800 per year. Multi-unit coastal buildings jump to $3,000 to $10,000 or higher annually due to concentrated hurricane and flood exposure.

Short-term rentals like Airbnb and VRBO properties cost substantially more than long-term leases because insurers view tenant turnover and higher occupancy rates as increased liability risk. If you own a short-term rental in Naples or another coastal area, expect to pay 30 to 50 percent more than comparable long-term rental rates. The type of structure matters as much as how you rent it. A manufactured home carries different underwriting criteria than a traditional stick-built home, and pools or detached garages add another 10 to 15 percent to your premium because they expand your liability exposure.

Regional Price Variations Across Florida

Geography within Florida creates price variations that dwarf national averages. Miami properties average around $10,357 annually because the city sits in a high-velocity hurricane zone with significant flood risk and elevated property values. Orlando inland properties typically cost $1,000 to $3,000 yearly, reflecting moderate hurricane exposure without coastal flood designation. Tallahassee properties average around $1,130 annually because inland northern Florida faces substantially lower weather risk than coastal regions.

Naples sits between these extremes, with premiums generally tracking with coastal Florida rates due to hurricane and storm surge exposure. Roof age, wind mitigation features, and claims history can shift your quote by hundreds of dollars in either direction, which means two similar properties in the same ZIP code might have dramatically different costs based on maintenance and risk management choices.

How Florida Rates Compare Nationally

In 2025, annual premiums typically range from $2,100 to $4,000, though some landlords pay as little as $700 or as much as $8,300+, depending on property type and location. Compared to national averages, Florida costs run 40 to 60 percent above the national median, making location selection and property hardening critical for expense management. This premium reflects the state’s concentrated exposure to hurricanes, flooding, and coastal storms that other regions simply don’t face at the same intensity.

Understanding these regional and property-type variations positions you to identify which cost-reduction strategies will have the most impact on your specific situation. The next section reveals concrete steps you can take to lower your premiums without sacrificing the protection your investment requires.

How to Lower Your Landlord Insurance Premiums

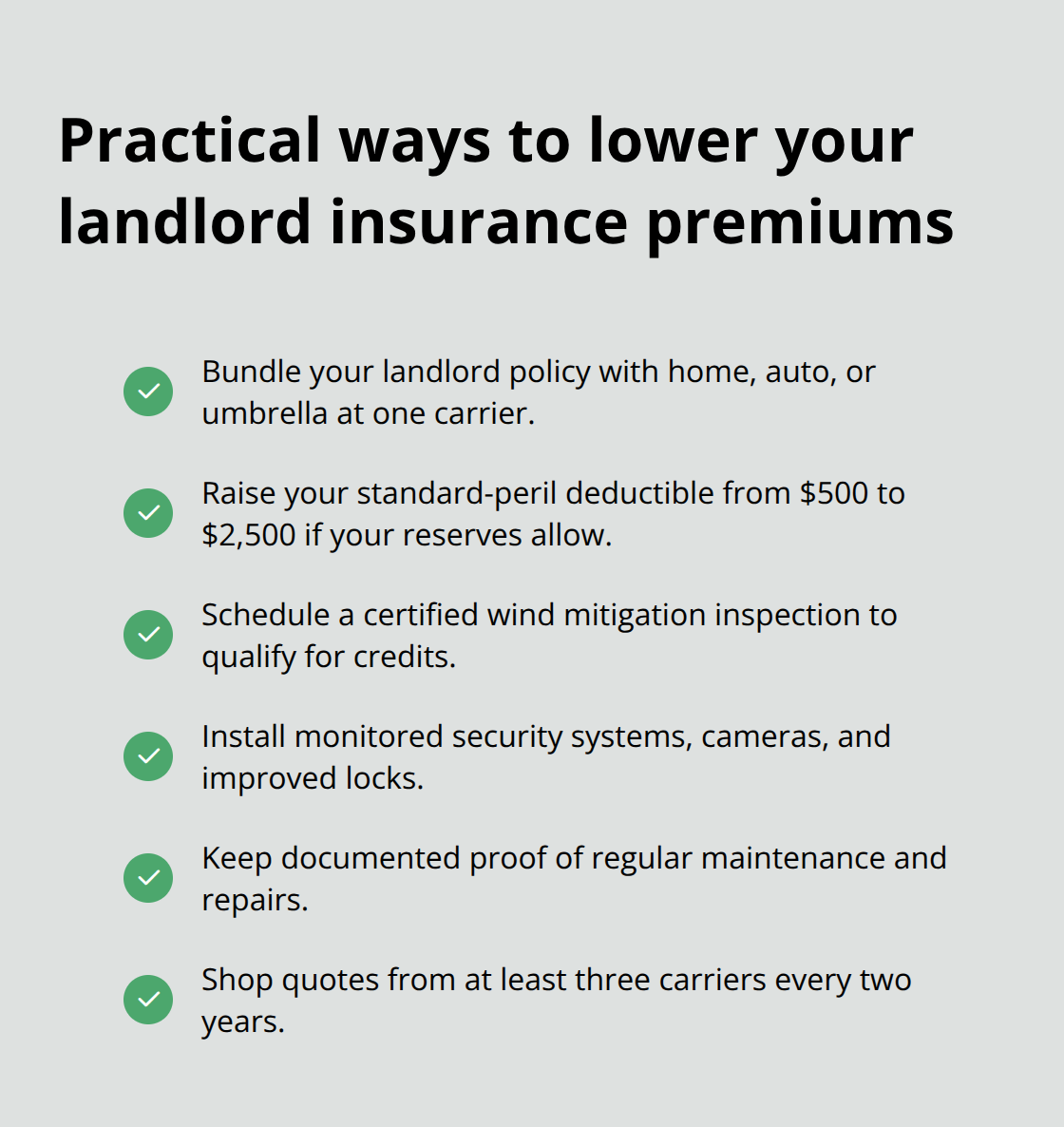

Bundle Policies and Raise Your Deductible

Reducing your landlord insurance premium requires specific, measurable actions rather than hoping for discounts. The most effective approach combines two distinct strategies that compound when deployed together. Bundling your landlord policy with other insurance you already carry at the same company typically saves 10 to 20 percent on your overall costs. If you insure your personal home, auto, or umbrella liability at one carrier, moving your rental property there often triggers a multi-policy discount that applies across all your accounts. Simultaneously, raising your deductible from $500 to $2,500 on standard perils reduces your annual premium by 15 to 25 percent because you accept more out-of-pocket responsibility for smaller claims.

This strategy works particularly well if you maintain an emergency fund covering three to six months of repairs, which most serious landlords should maintain anyway. The key is distinguishing between catastrophic coverage you cannot afford to lose-your hurricane deductible, flood coverage, and liability limits-and standard claim deductibles where higher retentions make economic sense.

Invest in Property Hardening and Maintenance Documentation

Property hardening investments deliver measurable returns that insurers actively reward with rate reductions. A certified wind mitigation inspection (which costs $200 to $400) qualifies you for credits that typically save $300 to $600 annually, paying for itself in one year. Roof-to-wall straps, secondary water barriers, and impact-rated windows reduce your replacement cost after a storm while simultaneously lowering your premium while they remain in place. Installing security features like alarm systems, surveillance cameras, and improved locks reduces liability and theft risk, lowering rates by 5 to 15 percent depending on your insurer.

Maintaining documented proof of regular maintenance-roof inspections, HVAC servicing, plumbing checks-demonstrates lower claim frequency to underwriters and improves renewal terms. These records transform your property from a statistical risk into a well-managed asset that carriers want to insure.

Shop Multiple Carriers Every Two Years

Shopping quotes from at least three different carriers every two years prevents you from overpaying through inertia. Insurance companies reward new customers with lower rates while existing customers often face gradual increases, so switching carriers every two or three years can save 20 to 40 percent compared to staying with one insurer. Kin offers online quotes for short-term and long-term rentals in high-risk Florida areas. American Modern covers properties other insurers reject. Security First typically prices 15 to 25 percent below average for Florida landlord policies.

As an independent insurance agency based in Naples, Florida, Responsive Insurance, Inc. works with multiple A-rated carriers to compare options and identify which company offers the best combination of price and coverage for your specific property, location, and risk profile.

Final Thoughts

Florida landlord insurance costs reflect real risk exposure, and understanding where your premium comes from puts you in control of your expenses. The six cost drivers we covered-property value, location, rental type, coverage limits, deductibles, and mitigation features-account for nearly every dollar you pay. Single-family inland rentals run $1,200 to $2,500 annually, while coastal multi-unit buildings exceed $10,000, and Miami properties average $10,357 due to concentrated hurricane and flood risk.

Reducing your landlord insurance Florida cost requires action, not wishful thinking. Bundling policies saves 10 to 20 percent immediately, while raising your deductible from $500 to $2,500 cuts premiums by 15 to 25 percent. A certified wind mitigation inspection pays for itself within one year through rate reductions, and shopping three carriers every two years prevents you from overpaying through inertia.

The most effective approach combines multiple strategies simultaneously-invest in property hardening, maintain documentation of regular maintenance, increase your deductible on standard perils while protecting catastrophic coverage, and compare quotes from carriers that specialize in Florida rental properties. We at Responsive Insurance, Inc. work with multiple A-rated carriers to compare coverage options and identify which company offers the best combination of price and protection for your specific property and location. Contact us today to discuss your rental property insurance needs and discover how much you can save.

![What Does Landlord Insurance Cover? [A Complete Guide]](https://responsiveinsurance.com/wp-content/uploads/emplibot/What-Does-Landlord-Insurance-Cover_-_A-Complete-Guide__1766873387-80x80.jpeg)