![What Does Landlord Insurance Cover? [A Complete Guide]](https://responsiveinsurance.com/wp-content/uploads/emplibot/What-Does-Landlord-Insurance-Cover_-_A-Complete-Guide__1766873387-1030x589.jpeg)

What Does Landlord Insurance Cover? [A Complete Guide]

Owning rental property in Naples comes with significant financial responsibility. You need protection that goes beyond standard homeowners coverage, which is why understanding what landlord insurance covers is essential for protecting your investment.

At Responsive Insurance, Inc., we help property owners navigate the specific risks that come with renting out homes or apartments. The right policy can mean the difference between a manageable loss and financial hardship.

What Landlord Insurance Actually Is

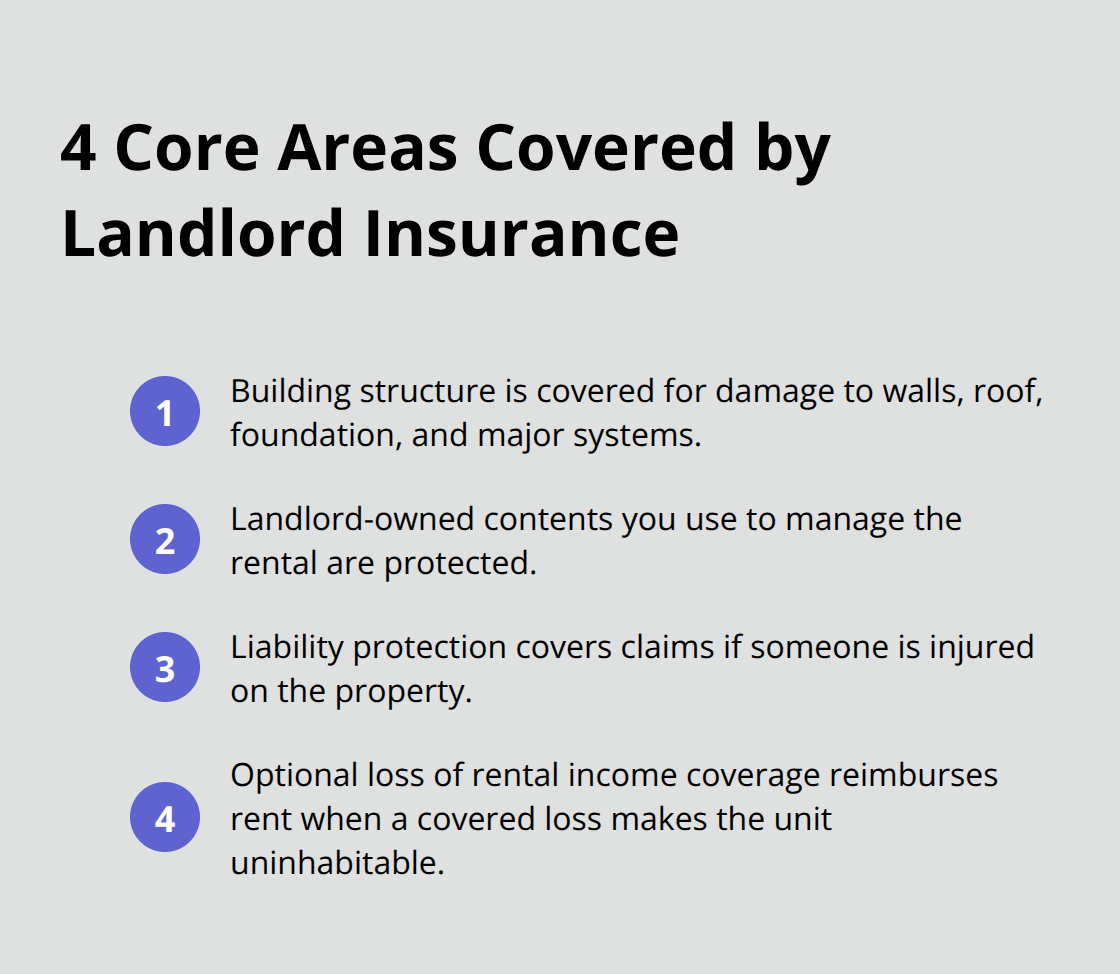

Landlord insurance is a specialized policy built specifically for rental properties, not a simple variation of homeowners coverage. It protects your building structure, covers liability claims if someone gets injured on your property, and reimburses lost rental income when a covered event makes the unit uninhabitable. The Insurance Information Institute confirms that a typical landlord policy covers four core areas: the building structure, landlord-owned contents you use to manage the rental, liability protection, and optional coverage for loss of rental income. This matters because Naples rental properties face distinct risks-from hurricane damage to tenant-related liability-that standard homeowners policies either ignore or actively exclude.

How Landlord and Homeowners Policies Differ

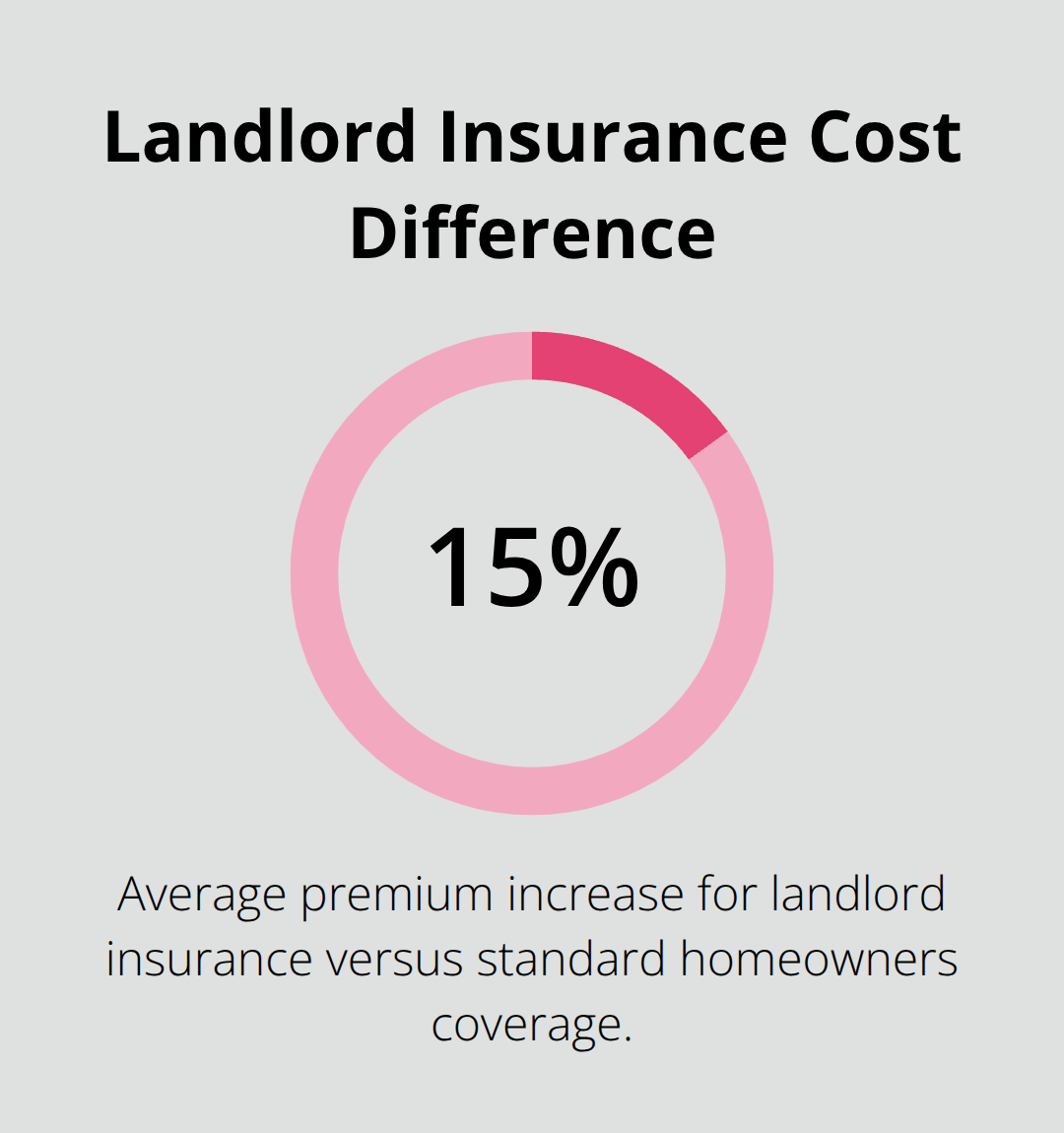

A homeowners policy assumes you live in the property and own all the contents inside. It does not account for the financial loss when a tenant cannot pay rent due to fire damage, nor does it protect you against liability claims specific to operating a rental business. According to Insurance.com data, landlord insurance costs roughly 15 percent more than standard homeowners coverage, averaging around $1,481 per year compared to $1,288 for homeowners. That premium difference reflects the actual added risk you carry as a landlord.

Why Your Homeowners Policy Won’t Work

Your existing homeowners policy explicitly excludes rental income loss and often limits liability coverage for business-related activities. If your property becomes unlivable after a covered loss, a homeowners policy leaves you with no compensation for the rent you cannot collect during repairs. Mortgage lenders typically require landlords to carry landlord-specific coverage with minimum protection levels, which means your current homeowner policy likely violates your loan terms if you rent out the property.

Florida’s Unique Liability Exposure

Florida’s Residential Landlord and Tenant Act imposes specific maintenance duties-functioning smoke detectors, structural repairs, safe common areas, and code compliance-that create distinct liability exposure beyond what homeowners insurance addresses. A tenant injured by a maintenance violation can pursue claims that your homeowners insurer may deny because the injury stems from a rental operation rather than personal occupancy. These statutory obligations transform your liability risk profile and demand coverage that homeowners policies simply do not provide.

Understanding these gaps sets the stage for what landlord insurance actually covers and how it protects your Naples investment from the specific perils you face as a property owner.

What Your Landlord Policy Actually Protects

Building Structure and Property Coverage

A landlord policy covers three distinct layers of protection that homeowners insurance ignores entirely. The building structure itself-walls, roof, foundation, plumbing, electrical systems, and fixtures you own-receives coverage under most DP-3 policies, which is the standard form for rental properties. This includes damage from fire, wind, hail, theft, and vandalism. Landlord-owned appliances and furnishings you provide to the tenant, like a refrigerator or washer-dryer, fall under landlord contents coverage, but the tenant’s personal belongings do not.

Liability Protection Against Injury Claims

The Insurance Information Institute notes that liability protection typically ranges from $300,000 to $1,000,000 in coverage limits, protecting you against bodily injury claims if someone gets hurt on your property due to a maintenance violation or unsafe condition. This matters in Naples because Florida’s Residential Landlord and Tenant Act requires you to maintain functioning smoke detectors, structural integrity, and safe common areas-failures that trigger liability claims when tenants or visitors suffer injury. A tenant injured by a maintenance violation can pursue claims that your homeowners insurer may deny because the injury stems from a rental operation rather than personal occupancy.

Loss of Rental Income During Repairs

Loss of rental income coverage reimburses you for rent you cannot collect when a covered peril makes the unit uninhabitable, but only during the repair period. If a fire damages the kitchen and the unit becomes unlivable, this coverage compensates for lost rent while repairs happen, protecting your cash flow during the downtime. The critical distinction: this coverage does not apply to tenant defaults, evictions, or normal vacancies-only to situations where a covered loss renders the property temporarily unusable.

Calculating Adequate Rental Loss Coverage

Many Naples landlords underestimate their rental loss needs and select limits below their actual monthly rent, which leaves income gaps during claims. Your rental loss coverage should equal your gross monthly rent multiplied by the estimated repair timeline; if you rent a property for $2,500 monthly and repairs typically take three months, you need at least $7,500 in rental loss coverage. Standard policies exclude flood damage entirely, meaning a hurricane-driven storm surge or heavy rainfall flooding creates zero coverage unless you purchase separate flood insurance from the National Flood Insurance Program or a private flood insurer-a critical gap for coastal Naples properties.

This flood exclusion reveals a major blind spot in standard landlord policies that affects nearly every Naples investor. Understanding what your policy leaves unprotected becomes the next essential step in building comprehensive coverage for your rental investment.

What Your Landlord Policy Leaves Unprotected

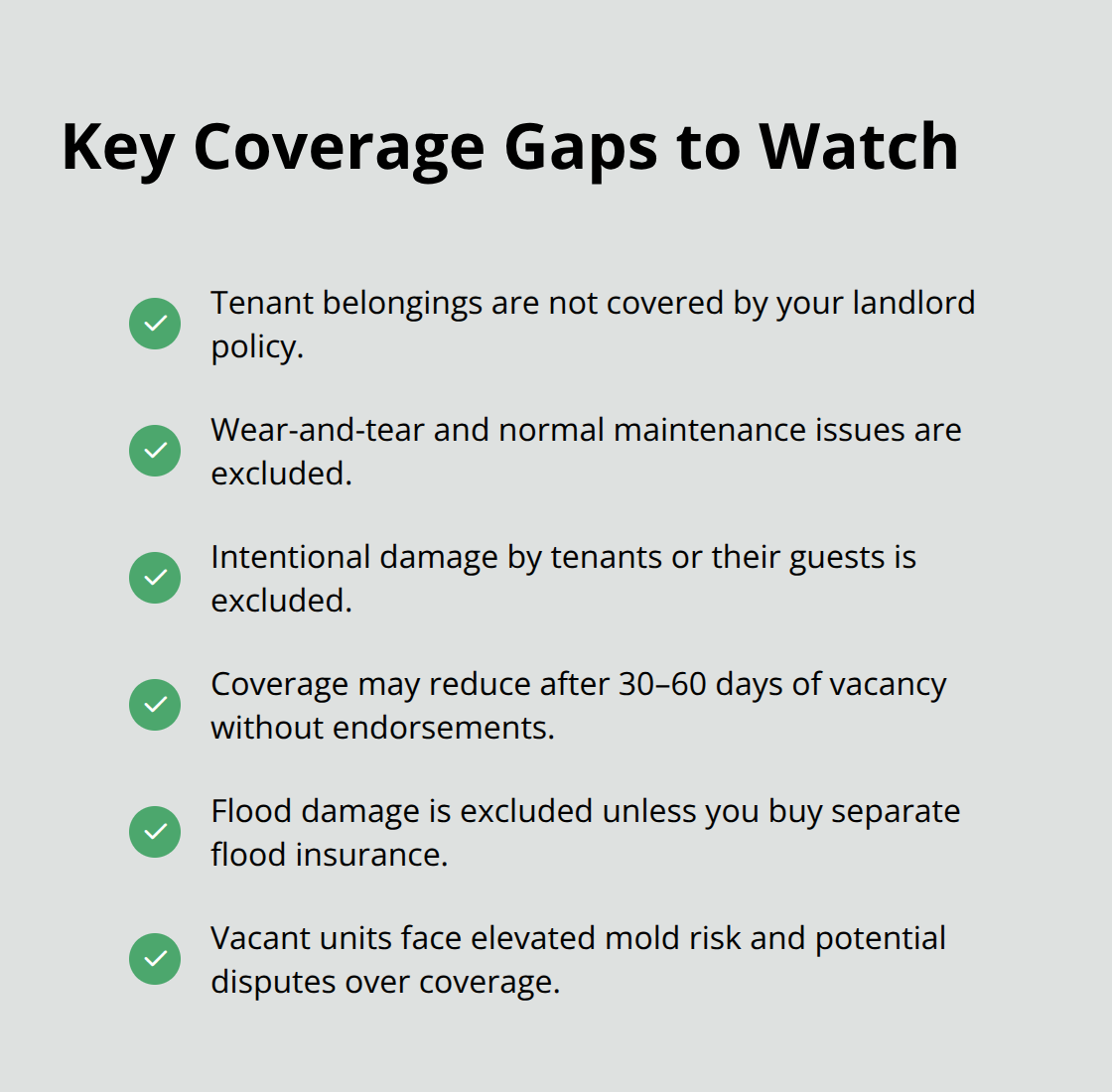

Tenant Belongings Fall Outside Your Coverage

Your landlord insurance protects the building and your liability exposure, but it creates significant coverage gaps that catch many Naples property owners off guard. Tenant belongings sit entirely outside your policy, meaning if a fire destroys a tenant’s furniture, electronics, or clothing, your insurance covers zero of that loss. Tenants’ personal property is not covered by landlord insurance, which is precisely why you should require renters insurance as a lease condition. A tenant’s renters policy costs roughly $20 monthly and covers their belongings plus provides liability protection if they accidentally damage your property or injure someone on the premises. Without this requirement, you absorb liability risk for injuries caused by tenant negligence while your policy excludes their possessions entirely.

Wear-and-Tear and Intentional Damage Exclusions

Wear-and-tear damage, normal maintenance failures, and intentional destruction fall outside coverage. If a tenant damages walls, flooring, or fixtures through normal use, that damage belongs to the tenant’s security deposit dispute, not your insurance claim. Intentional damage caused by the tenant or anyone acting with their permission creates a coverage void because policies exclude losses from criminal acts or deliberate property destruction. These exclusions protect insurers from covering losses that tenants or their guests cause through negligence or malice.

Vacant Property Coverage Gaps

Vacant property exclusions represent another critical gap that affects Naples investors holding properties between tenants or undergoing renovations. Many policies reduce or exclude certain protections when a property sits vacant for extended periods, sometimes as short as 30 to 60 days of non-occupancy. This matters because standard landlord policies assume someone occupies the unit, which reduces the risk of theft, vandalism, or water damage from burst pipes going unnoticed. If your property remains empty while you search for tenants or complete upgrades, you may lose coverage for theft, vandalism, or water damage unless you specifically request extended vacancy coverage or purchase a separate vacant property endorsement.

Flood Damage and Mold Risk in Vacant Units

The National Flood Insurance Program excludes flood damage entirely from standard policies, but this exclusion hits differently for vacant properties where water intrusion from broken pipes or roof leaks might go undetected for weeks. Florida’s humid climate creates additional mold risk in vacant units where moisture accumulates without active climate control or occupancy monitoring. Mold claims are notoriously contentious in Florida insurance disputes, and vacant properties amplify this risk because mold develops faster in unoccupied spaces and insurers often dispute whether the damage qualifies as a sudden, accidental loss or results from inadequate maintenance and moisture control.

Final Thoughts

Landlord insurance protects your Naples rental investment by covering building damage, liability claims, and lost rental income during repairs. The coverage gaps we discussed-tenant belongings, wear-and-tear, vacant property exclusions, and flood damage-demand your attention when you select a policy. What does landlord insurance cover ultimately depends on your specific policy terms, so you must verify both what your coverage includes and what you must address separately through additional endorsements or policies.

Building adequate coverage starts with calculating your actual needs based on your property’s monthly rent and realistic repair timelines. If you own multiple properties or anticipate short-term rentals like Airbnb, you should confirm your policy covers those scenarios. You also need to require renters insurance from tenants to fill the personal property gap, reduce your liability exposure, and consider flood insurance immediately if your property sits in a coastal area or flood zone (since standard policies exclude this peril entirely).

Contact Responsive Insurance, Inc. for a quote and discuss your property details, rental income, and coverage concerns with our team. We compare coverage options from multiple A-rated insurance companies to find the best fit for your specific situation and understand the local risks that affect your investment decisions. The right landlord policy costs roughly 15 percent more than homeowners coverage but delivers protection that homeowners insurance simply cannot provide.