How to Get Rental Property Insurance Quotes Fast

Getting rental property insurance quotes doesn’t have to be time-consuming. We at Responsive Insurance, Inc. know that landlords in Naples need fast, straightforward answers about coverage options and pricing.

This guide walks you through exactly what information to gather, where to request quotes, and how to compare them side-by-side. You’ll have the details you need to protect your investment without wasting hours on the process.

What Information Landlords Need to Gather

Before you request quotes, collect your property details and rental history. Underwriters assess risk accurately only when they have specifics about your building. For properties in Naples, prepare your address, property type (single-family home, multi-unit building, condo unit), square footage, year built, and roof age. If your roof exceeds 20 years old, carriers will scrutinize it closely-some require replacement or detailed inspection reports. Underwriters also want to know the number of units, current rent per unit, and whether tenants stay long-term or short-term rental coverage like Airbnb guests. Short-term rentals face different underwriting standards and may require specialized coverage, so disclose your rental model upfront from the start.

Your Loss History Shapes Your Quote

Carriers require three to five years of loss history before issuing quotes. This includes any claims you filed on the property, previous damage incidents, or liability claims. Request your loss runs from your current insurer or agent-these documents show underwriters that you manage the property responsibly or reveal patterns that increase risk. If you filed multiple water damage claims, underwriters will ask about your maintenance practices and may require proof of plumbing updates. Properties with no loss history quote faster and often receive better rates. Additionally, provide details about your current coverage if you already have a policy. Include your dwelling limits, liability limits, deductibles, and any gaps you identified. If your current homeowner policy explicitly excludes rental use, mention this immediately-it means you carry insufficient coverage and need proper landlord insurance.

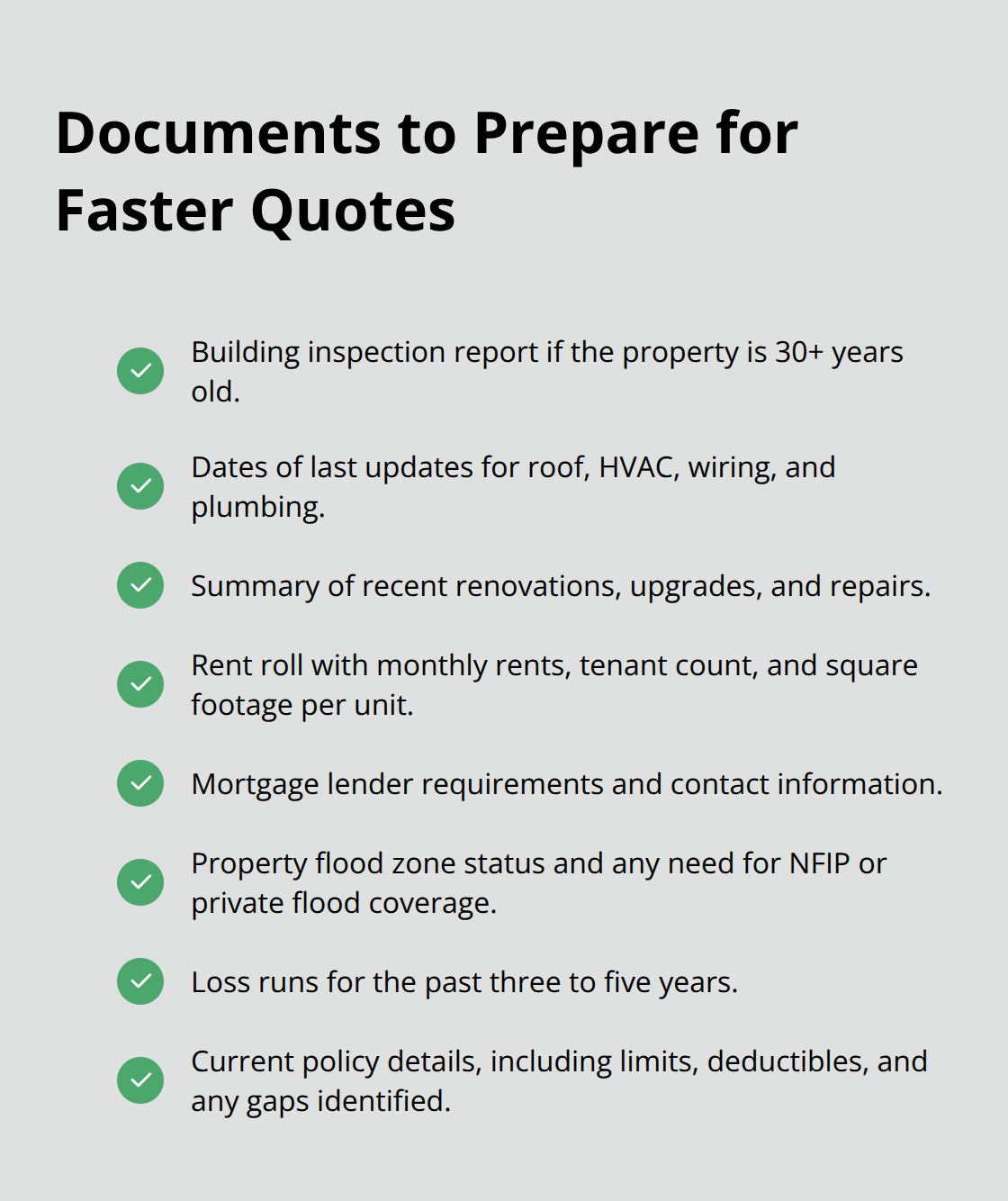

Documentation That Eliminates Delays

Prepare an up-to-date building inspection report if your property exceeds 30 years old. Underwriters will ask when your roof, HVAC, wiring, and plumbing were last updated anyway, so an inspection report eliminates back-and-forth delays. Include information about any recent renovations, upgrades, or repairs.

For multi-unit properties, a rent roll showing monthly rents, tenant count, and square footage per unit saves time and improves accuracy. Have your mortgage lender information available-lenders often require specific coverage minimums and may mandate loss of rental income coverage. Know your property’s flood zone status before requesting quotes. Florida properties in flood-prone areas need separate flood insurance through the National Flood Insurance Program or private carriers, and this affects your overall coverage strategy and timeline.

Moving Forward With Your Quote Request

Organize these documents before contacting agents. A complete file dramatically reduces the quote turnaround time and positions you to move quickly through the next phase-finding the right agencies and platforms to request your quotes.

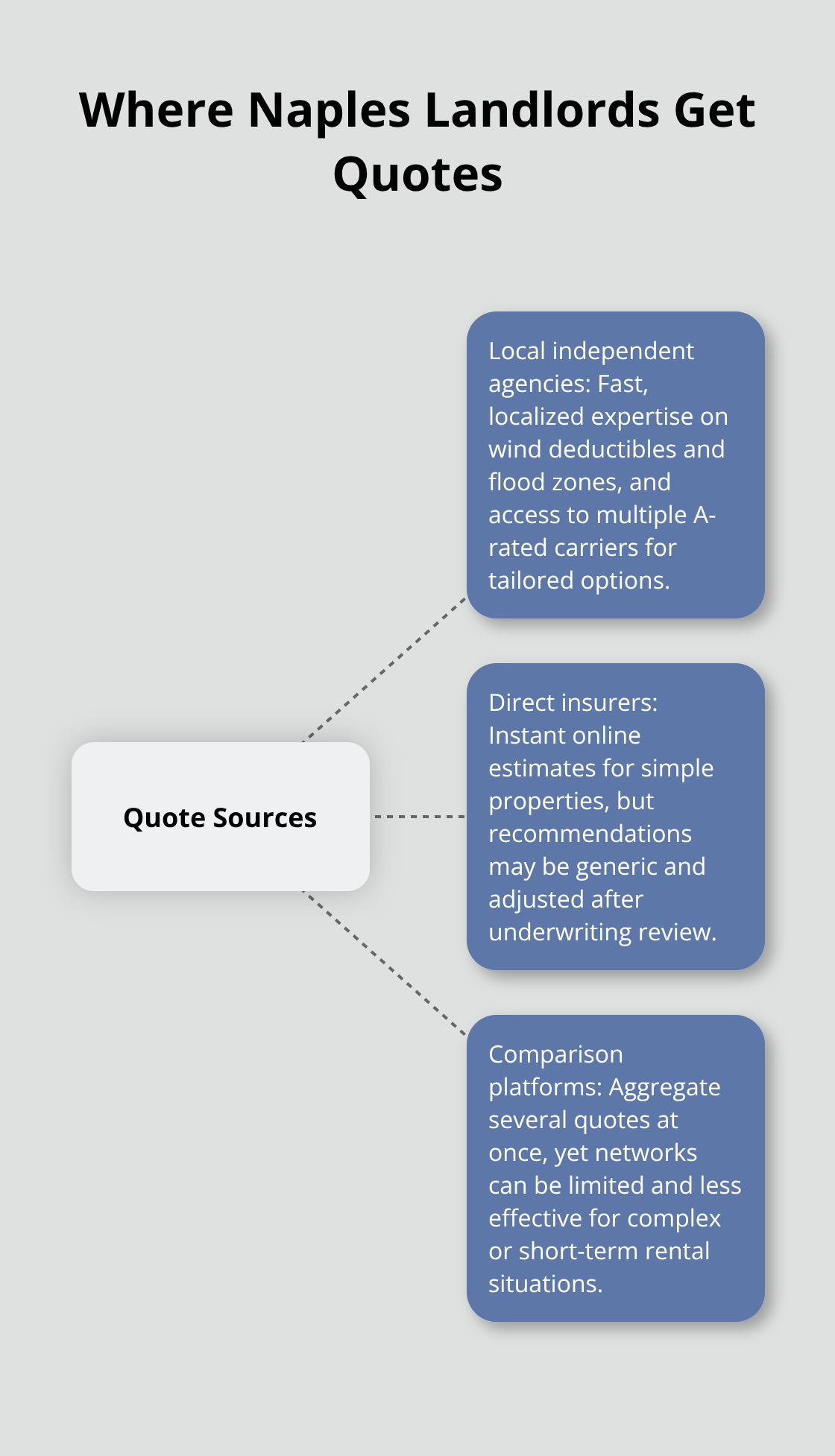

Where to Get Quotes

Local Independent Agencies Offer Speed and Local Expertise

Independent insurance agencies in Naples provide the fastest path to accurate quotes because local agents understand Florida’s specific risks and lender requirements. When you contact a local independent agency, you speak directly with someone who knows Naples properties, wind deductibles, flood zones, and which carriers move quickly on habitational underwriting. Local agents answer questions about your specific property within minutes rather than waiting for online form submissions to route through a national system. They ask targeted questions about your roof age, loss history, and rental model upfront, then submit your information to underwriters who specialize in landlord coverage. This approach typically produces quotes within 30 minutes to a few hours for straightforward properties, though more complex multi-unit buildings or properties with loss history may take one to two business days. Independent agencies work with multiple A-rated insurance companies, which means they compare coverage options and pricing across several carriers rather than locking you into one company’s rates.

Direct Insurance Company Websites Work Best for Simple Properties

National carriers like State Farm or Allstate offer online quote tools where you enter property details and receive instant estimates. This method works best only if you know exactly what coverage you need and your property is straightforward with no loss history. The advantage is speed and convenience-you complete the process on your own schedule without speaking to an agent. The disadvantage is that you’ll likely receive generic coverage recommendations rather than tailored advice for Naples’ hurricane exposure, flood risk, or your specific rental model. Direct company websites often come with disclaimers that underwriting may adjust pricing after a more detailed review, so the initial quote may not reflect your final rate.

Online Comparison Platforms Aggregate Multiple Quotes

Online comparison platforms aggregate quotes from multiple insurers simultaneously, allowing you to view side-by-side pricing and coverage in one place. However, these platforms typically work with a limited network of carriers and may miss specialized landlord insurers who offer competitive rates in Florida. You’ll still answer detailed questions about your property, and the quotes come with the same underwriting caveats as direct company websites.

For Naples landlords with complex properties, loss history, or short-term rental situations, this approach often produces less useful quotes because the platform’s algorithm cannot account for local nuances that affect pricing and availability.

Comparing Your Options

Each channel has trade-offs. Direct websites and comparison platforms offer convenience but sacrifice personalization. Local independent agencies require a phone call or office visit but deliver quotes tailored to your property’s unique risk profile and Florida’s specific insurance landscape. The choice depends on your property’s complexity and how much guidance you need. Once you’ve selected where to request quotes, the next step involves understanding what to look for when comparing the quotes you receive.

Tips for Comparing Quotes and Choosing Coverage

You now have quotes in hand, but comparing them requires more than glancing at the annual premium. Insurance companies quote identical properties differently because they weight risk factors uniquely, and Naples landlords must understand exactly what coverage differences drive price variations.

Extract and Compare Dwelling Limits

Start with the dwelling limit from each quote-this is your property’s replacement cost protection. If one insurer quotes a $400,000 dwelling limit while another quotes $350,000 for the same property, the higher quote may reflect more accurate replacement costs, not overpricing. Florida properties built before 2000 often need higher dwelling limits due to construction cost inflation and code upgrades required after damage.

Evaluate Liability Protection and Deductibles

Next, examine liability limits across quotes. Most carriers offer $300,000 or $1,000,000 in liability protection. For Naples properties, $300,000 represents the minimum lenders typically require, but $1,000,000 provides substantially better asset protection if a tenant or visitor sues you-the extra premium usually costs only $100–$200 annually. Deductibles vary significantly and directly impact your out-of-pocket costs after a claim. A $2,500 deductible saves premium compared to $1,000, but after a water damage claim in a rental unit, you’ll pay the difference yourself. For Florida properties facing frequent weather events, evaluate whether the quoted deductible applies to all perils or only wind and hail. Some carriers impose separate hurricane deductibles of 5–10% of the dwelling limit, meaning on a $400,000 home, you’d pay $20,000–$40,000 out of pocket before coverage applies. This detail alone can make or break a quote’s true value.

Identify Coverage Gaps and Exclusions

Loss of rental income coverage appears on some quotes but not others-this is a critical gap to catch. If a covered disaster damages your rental property, this coverage replaces your lost monthly income so you can still pay your bills during repairs. Without it, you still owe your mortgage while earning zero rent, depleting your reserves rapidly. Carriers quote this coverage at different limits and may exclude it entirely from basic policies. Compare whether each quote includes water damage, vandalism, and liability for tenant injuries, as these protections vary by carrier and significantly affect your actual coverage. Review the quote documents for exclusions or limitations-some policies exclude mold damage unless caused by a covered peril, others limit water backup coverage, and a few exclude short-term rentals entirely.

Assess Agent Responsiveness and Discount Opportunities

Call the agent issuing each quote and ask directly about wind exclusions, flood requirements, and whether the policy covers Airbnb or VRBO properties if applicable. The agent’s responsiveness during the quote process predicts how they’ll handle claims. If obtaining clarification takes days or requires multiple follow-ups, that carrier’s claims support will likely frustrate you when you need it most. Local independent agencies in Naples typically answer clarification questions within hours, while national carriers may route inquiries through call centers that lack property-specific knowledge. Finally, ask about discounts explicitly-bundling homeowners and rental coverage, installing security systems, or maintaining a loss-free history can reduce premiums by 10–25%, but carriers don’t always volunteer these savings unless prompted.

Final Thoughts

Getting rental property insurance quotes fast requires preparation and selecting the right source. You now understand what information underwriters need, where to request quotes, and how to compare coverage without overpaying or missing critical gaps. Local independent agencies in Naples deliver the fastest path forward because agents know Florida’s wind deductibles, flood zones, and which carriers move quickly on habitational underwriting-they answer your questions directly rather than routing inquiries through national call centers.

We at Responsive Insurance, Inc. work with multiple carriers to compare your rental property insurance quotes and tailor coverage to your property’s unique risk profile. Our team responds promptly to your questions and guides you through the entire process so you can protect your investment without unnecessary delays. Start by organizing your documents today-property details, loss history, building inspection reports, and rent rolls-then contact a local agent tomorrow.

The difference between a rushed decision and an informed choice comes down to having complete information ready when you request your quotes. Your rental property deserves coverage that matches its actual risks, and the fastest way to find it is working with someone who knows Naples properties inside and out.

![Home Insurance for Older Homes in Florida [What to Know]](https://responsiveinsurance.com/wp-content/uploads/emplibot/Home-Insurance-for-Older-Homes-in-Florida-_What-to-Know__1766268849-80x80.jpeg)

![What Does Landlord Insurance Cover? [A Complete Guide]](https://responsiveinsurance.com/wp-content/uploads/emplibot/What-Does-Landlord-Insurance-Cover_-_A-Complete-Guide__1766873387-80x80.jpeg)