![Home Insurance for Older Homes in Florida [What to Know]](https://responsiveinsurance.com/wp-content/uploads/emplibot/Home-Insurance-for-Older-Homes-in-Florida-_What-to-Know__1766268849-1030x589.jpeg)

Home Insurance for Older Homes in Florida [What to Know]

Older homes in Florida face unique insurance challenges that newer properties simply don’t encounter. Insurers charge more for aging houses because of structural vulnerabilities, outdated building codes, and higher replacement costs.

At Responsive Insurance, Inc., we help Naples homeowners navigate home insurance for older homes in Florida and find coverage that actually fits their needs. This guide breaks down why premiums are higher, what coverage options work best, and how to reduce your costs.

Why Older Homes Cost More to Insure

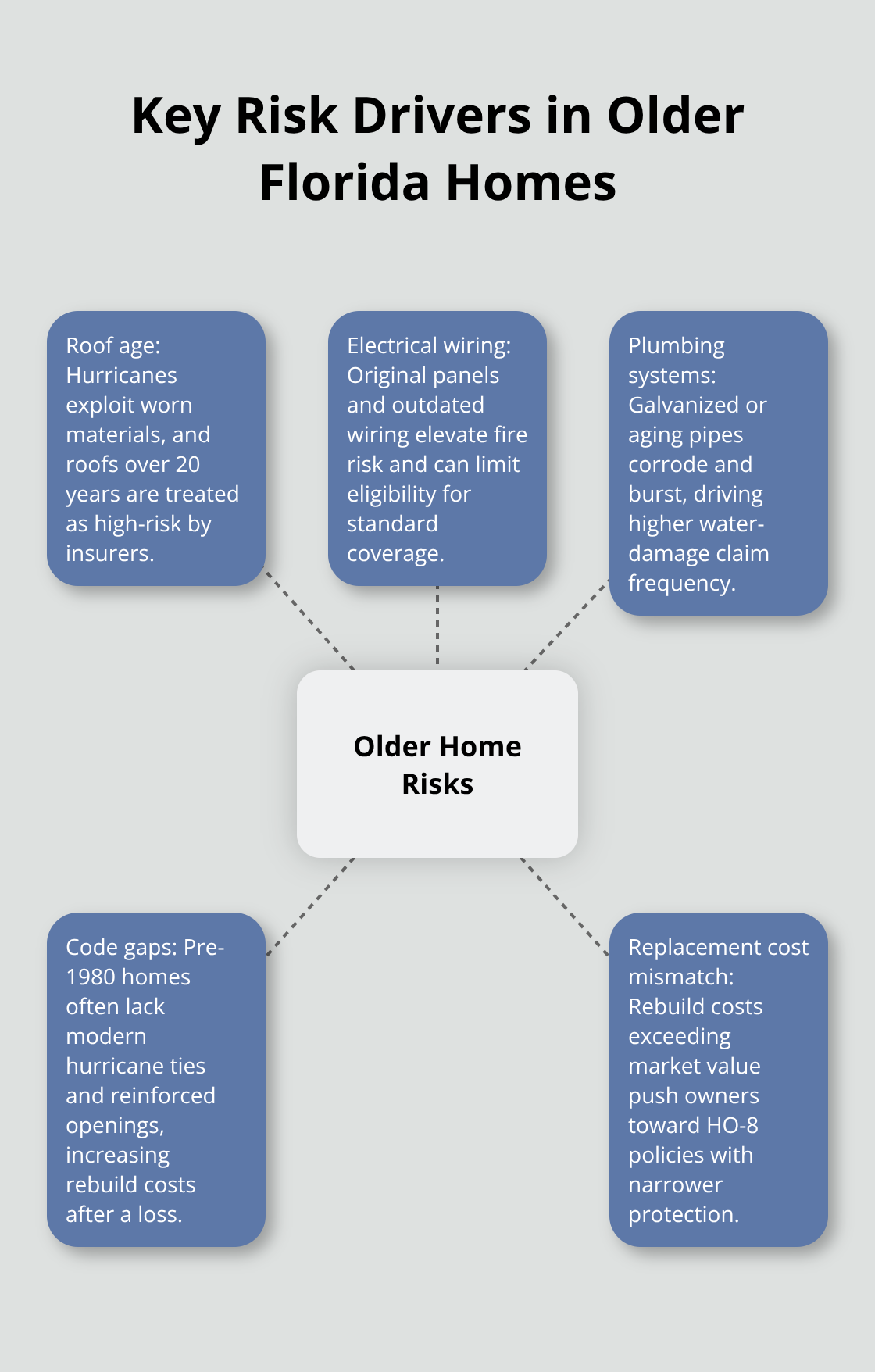

Insurers charge significantly higher premiums for homes built before 1980 in Florida because the risk profile is fundamentally different. Homes constructed 40+ years ago often contain original electrical wiring, plumbing, and roofing systems that fail at higher rates than modern equivalents. A home with knob-and-tube wiring or outdated galvanized pipes presents measurable fire and water damage risks that insurers quantify through claims data. When insurers review your property, they’re not being cautious-they’re pricing based on actual failure rates from thousands of similar homes. The National Association of Insurance Commissioners reports that water damage and theft represent the largest homeowners insurance loss categories, and older plumbing systems are primary culprits.

Your 50-year-old copper or galvanized pipes are statistically more likely to burst or leak than PVC installed in 2010, and insurers know this from decades of claims history.

Roofing Age and Hurricane Vulnerability

Roofing age creates the most immediate pricing impact. Florida insurers scrutinize roof condition because hurricane-force winds exploit weaknesses in aging materials. A roof installed in 2000 is approaching the end of its lifespan, and many insurers won’t issue standard homeowners coverage without a recent roof inspection or replacement. The “30-year roof” label on shingles refers to material lifespan, not an insurance guarantee-insurers treat roofs over 20 years old as high-risk. Your Naples home’s roof age directly affects your premium because wind damage claims spike dramatically on older roofing systems.

Electrical and Plumbing System Risks

Electrical systems matter equally to roofing. Homes with original wiring present fire risks that modern code requirements eliminated. If your Naples home still has the original electrical panel from 1975, you’re looking at either upgrading before qualifying for standard coverage or accepting higher premiums on a limited policy. Outdated plumbing creates similar pressure-galvanized pipes corrode from the inside, and burst pipes flood homes faster than most other perils. Insurers factor these failure rates into every quote for older properties.

Building Code Compliance Gaps

Modern Florida building codes require stronger hurricane ties, better insulation, and reinforced openings that homes built decades ago lack. When your older home sustains damage and needs rebuilding, current code requires upgrades that cost substantially more than simply replacing what was damaged. Insurers account for this through higher premiums or by offering HO-8 policies with lower coverage limits instead of standard HO-3 protection.

The Replacement Cost Problem

The math here is brutal. Suppose your 1970s Naples home has a current market value of $400,000 but would cost $550,000 to fully rebuild with modern materials and current code compliance. Insurers flag this scenario because it creates moral hazard-you’d receive more in insurance proceeds than the home’s market value. This mismatch forces insurers to offer HO-8 policies instead of standard HO-3 coverage. HO-8 policies cover fewer perils, cap dwelling coverage lower, and cost less upfront but leave you exposed if a hurricane or major fire strikes. Alternatively, you upgrade critical systems before applying for standard coverage. Replacing outdated wiring, plumbing, or roofing reduces your premium immediately because you’ve eliminated the primary risk factors that triggered the higher rate in the first place. Understanding these cost drivers helps you decide whether to invest in upgrades or explore specialized policies designed specifically for aging Florida properties.

Coverage Options Designed for Older Florida Homes

Florida insurers have stopped pretending that one-size-fits-all homeowners policies work for aging properties. The reality is that specialized programs now dominate coverage for homes built before 1980, and Naples homeowners need to understand the practical differences before shopping.

HO-8 Policies and Their Limitations

HO-8 policies, designed explicitly for older homes where rebuild cost exceeds market value, cover fewer perils than standard HO-3 policies but cost significantly less upfront. An HO-8 typically excludes coverage for vandalism, malicious mischief, and sometimes water damage unless you add it separately. If your Naples home would cost $600,000 to rebuild but has a market value of $450,000, insurers will push you toward HO-8 because they won’t issue standard coverage on that mismatch. The trade-off is lower premiums in exchange for narrower protection.

Specialized Programs for Older Owner-Occupied Homes

Integrity Select, offered by American Integrity Insurance, targets older owner-occupied Florida homes valued between $150,000 and $3,000,000 (depending on county) and provides robust protection without the common exclusions found in standard policies. This matters because you receive broader coverage than HO-8 while still qualifying as an older-home owner. American Integrity also offers Additional Living Expense coverage if a storm displaces you, belongings protection for personal items, and specialized home computer coverage. You pay more than HO-8 but receive actual protection rather than gaps.

Replacement Cost vs. Actual Cash Value

Replacement cost coverage on dwelling and other structures ensures you’re not left covering a large portion of the expenses out of pocket. If your roof burns in a fire, replacement cost reimburses you for new shingles, not depreciated ones. Actual Cash Value reduces that payout by factoring in age and wear, which severely underfunds repairs on older homes. For Naples homeowners, replacement cost is non-negotiable because depreciation on a 50-year-old home creates unmanageable gaps between what you receive and what repairs actually cost.

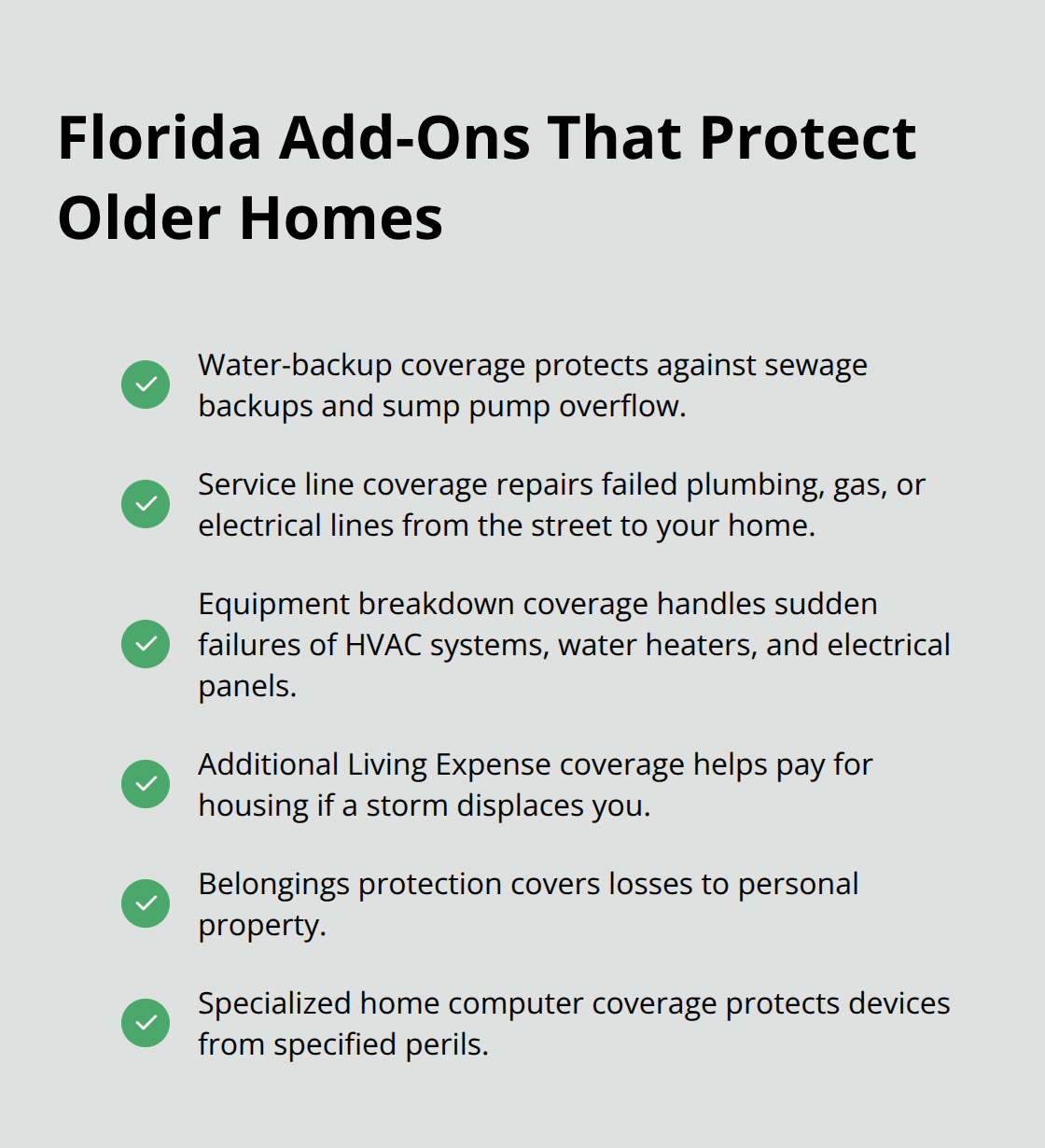

Florida-Specific Add-On Protections

Florida-specific risks demand additional protections that standard policies underinsure. Water-backup coverage protects against sewage backups and sump pump overflow, common issues in older homes with aging drainage systems and outdated plumbing. Service line coverage protects essential lines like plumbing, gas, and electrical service running from the street to your home, which fail frequently in aging properties. Equipment breakdown coverage handles sudden mechanical failures in HVAC systems, water heaters, and electrical panels that older homes accumulate. These add-ons cost $100 to $300 annually but prevent catastrophic out-of-pocket expenses when systems fail. Once you select the right policy type and coverage layers, the next step involves identifying which home improvements actually reduce your premiums and which ones simply improve your home’s value without affecting insurance costs.

How to Lower Your Premiums on an Older Home

Upgrade Critical Systems to Eliminate Risk Factors

Replacing your home’s critical systems delivers the fastest premium reduction because you eliminate the exact risk factors that triggered higher rates in the first place. Roof replacement qualifies for premium reductions because you’ve removed a major vulnerability in hurricane-prone Florida. Electrical upgrades matter equally-replacing knob-and-tube or cloth-wrapped wiring with modern code-compliant systems eliminates fire risk that insurers quantify through claims data. If your Naples home has the original 1970s electrical panel, replacing it costs $3,000 to $5,000 but recovers that investment through lower premiums within five to eight years.

Water heater replacement, HVAC system upgrades, and plumbing updates follow the same principle: you reduce measurable risk, and insurers respond with lower quotes. Installing a security system qualifies for additional discounts on some policies, typically saving 5 to 10 percent on dwelling coverage. Get quotes before and after any major upgrade so you can quantify exactly what the improvement saves on your annual premium-this prevents overspending on renovations that don’t affect insurance costs.

Compare Rates Across Multiple Carriers

Older-home rates vary dramatically between insurers because each carrier weights roof age or building materials differently. One carrier might quote $2,400 annually for your 1975 Naples home while another quotes $1,800 for identical coverage. Integrity Select, offered by American Integrity Insurance, often provides better rates than standard HO-3 policies on older owner-occupied homes valued between $150,000 and $3,000,000 (depending on county), making it worth comparing against traditional carriers.

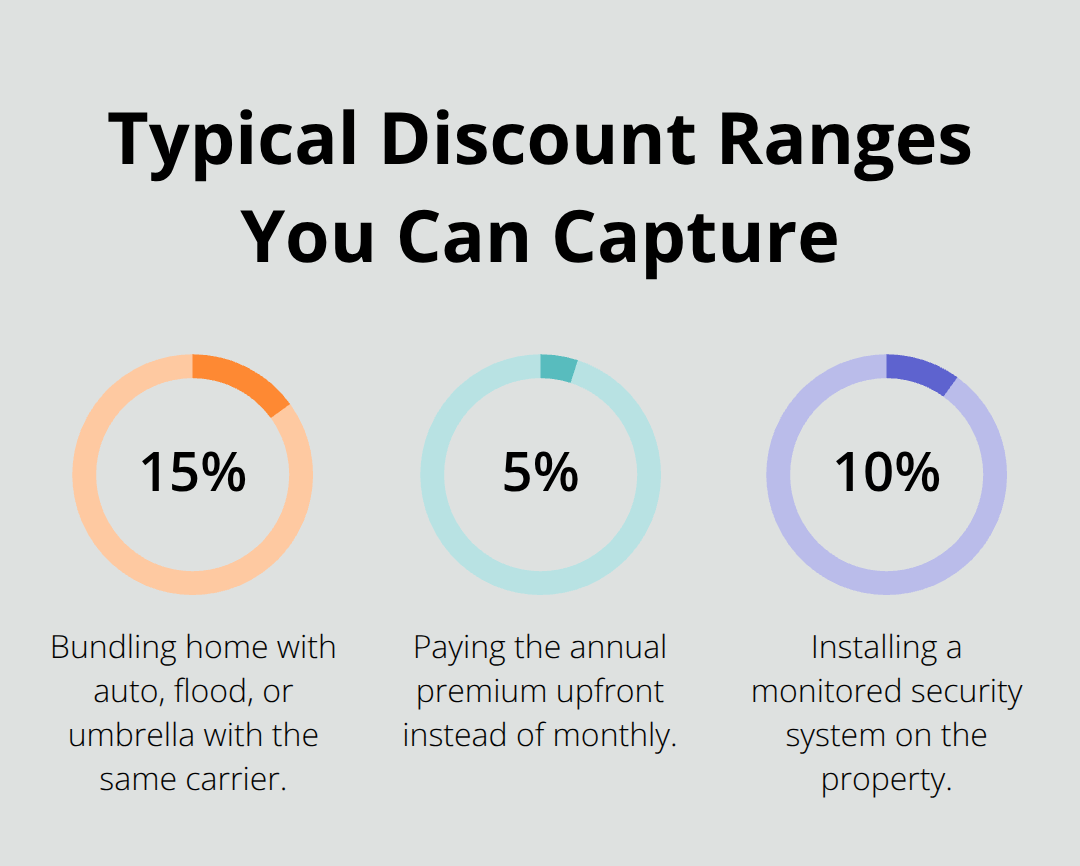

Stack Discounts Through Bundling and Payment Options

Bundling your homeowners policy with auto insurance, flood coverage, or umbrella liability typically saves 10 to 20 percent on your total premium because insurers reward customer loyalty. If you maintain auto and home coverage with the same carrier, expect 10 to 15 percent combined savings. Some insurers offer additional discounts for paying your annual premium upfront rather than monthly, which can save another 3 to 5 percent. Autopay enrollment sometimes triggers small discounts as well.

The math compounds quickly-a $2,000 annual homeowners premium with a 15 percent bundling discount plus 5 percent for paying annually saves you $400 without requiring any home improvements. As an independent agency based in Naples, Responsive Insurance, Inc. compares rates from multiple A-rated carriers to identify which combination delivers the lowest total cost while maintaining the coverage your older home actually needs.

Final Thoughts

Insuring an older home in Florida requires you to accept three realities: your property costs more to insure because of measurable structural and system risks, specialized policies exist that address these risks without leaving coverage gaps, and strategic upgrades combined with smart shopping reduce your premiums. You’ll choose between HO-8 policies with lower premiums but narrower protection, or specialized programs like Integrity Select that provide broader coverage for older owner-occupied homes. Replacement cost coverage on dwelling and other structures becomes non-negotiable because depreciation on aging properties creates dangerous gaps between what you receive and what repairs actually cost.

Reducing your premium happens through two parallel strategies: upgrade critical systems that insurers specifically penalize (roof replacement, electrical modernization, and plumbing updates deliver measurable rate reductions), and compare rates across multiple carriers because older-home pricing varies dramatically between insurers. Bundling your homeowners policy with auto or flood coverage, then paying annually, stacks discounts that compound into substantial savings without requiring any home improvements. Adding Florida-specific protections like water-backup coverage and service line coverage prevents catastrophic expenses when systems fail.

Finding the right coverage for home insurance for older homes in Florida demands more than an online quote tool-you need someone who understands how different carriers treat aging properties, which upgrades actually affect your premium, and which coverage combinations protect your specific situation. Responsive Insurance, Inc. is an independent agency based in Naples that compares coverage and rates from multiple A-rated carriers to identify the best fit for your older home. Contact us to discuss your property’s specific needs and get quotes that reflect the actual protection available for your situation.