Naples Flood Policy: Understanding Your Coverage Options

Living in Naples means accepting that flooding is a real threat to your home and finances. A Naples flood policy isn’t optional-it’s a practical necessity that protects what matters most.

Standard homeowners insurance won’t cover flood damage, leaving you exposed to devastating losses. At Responsive Insurance, Inc., we help residents understand their coverage options so they can make informed decisions about protecting their property.

Why Flood Insurance Matters in Naples

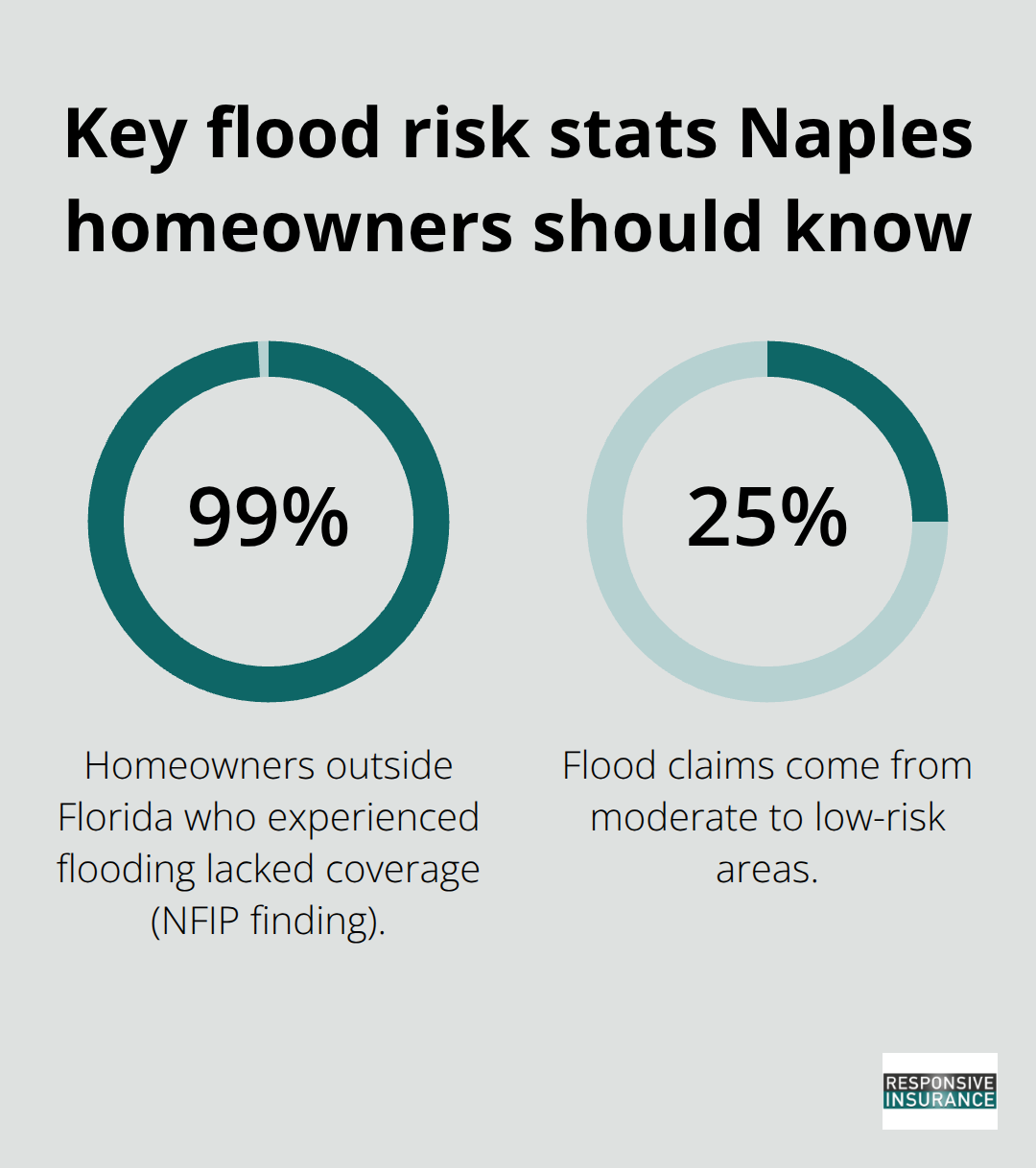

Florida experiences more frequent flooding than any other state, and Naples sits directly in the crosshairs. The National Flood Insurance Program reports that roughly 99% of homeowners outside of Florida who sustained flooding are not covered, yet up to 25% of flood claims come from people in moderate to low-risk areas. This gap exists because most people assume their standard homeowners policy covers water damage-it doesn’t. Your homeowners insurance protects against wind, theft, and fire, but flood damage falls into a completely separate category that requires its own dedicated policy. In Naples, where storm surge, heavy rainfall, and rising tides create constant exposure, this distinction becomes the difference between recovering quickly after a flood or facing financial devastation. Flooding ranks as the costliest natural disaster in the United States, according to FEMA, and without flood insurance, you’ll pay out of pocket unless a presidential disaster declaration is issued (something that happens in fewer than half of flooding events).

The Real Cost of Going Uninsured

A single flood event destroys the structural integrity of your home, ruins appliances, damages flooring, and destroys personal belongings. Flood insurance covers building damage like walls, ceilings, floors, and stairs, plus household appliances and utilities. It also covers debris cleanup costs that homeowners often overlook-expenses that can easily reach tens of thousands of dollars. Without coverage, you pay for every penny of restoration yourself. Government aid does not arrive automatically; it only appears after a presidential disaster declaration, leaving most flood victims to fund their own recovery. The average flood insurance premium runs about $53 per month, making comprehensive protection affordable compared to the potential loss.

What Naples Residents Can Access

Naples participates in the National Flood Insurance Program, meaning all residents can qualify for NFIP coverage. The 2024 Flood Insurance Rate Maps now in effect provide updated risk data that affects your premium and eligibility. If your property sits in a Special Flood Hazard Area, your mortgage lender will require flood insurance-you won’t have a choice. Even outside high-risk zones, purchasing a policy protects against the unexpected. Private flood markets in Florida also offer alternatives to NFIP policies, with some options providing excess coverage that exceeds federal limits (potentially saving money for lower-risk properties through preferred risk rates).

Finding Coverage That Fits Your Property

Your next step involves assessing your property’s specific flood risk zone and comparing available options. An Elevation Certificate, prepared by a licensed surveyor, helps determine your exact flood risk and premium level if your home sits in a Special Flood Hazard Area. Multiple insurance companies offer flood policies in Naples, each with different rates and coverage limits. Working with an independent insurance agency gives you access to multiple A-rated carriers, allowing you to compare quotes and find the best fit for your property’s risk profile and budget.

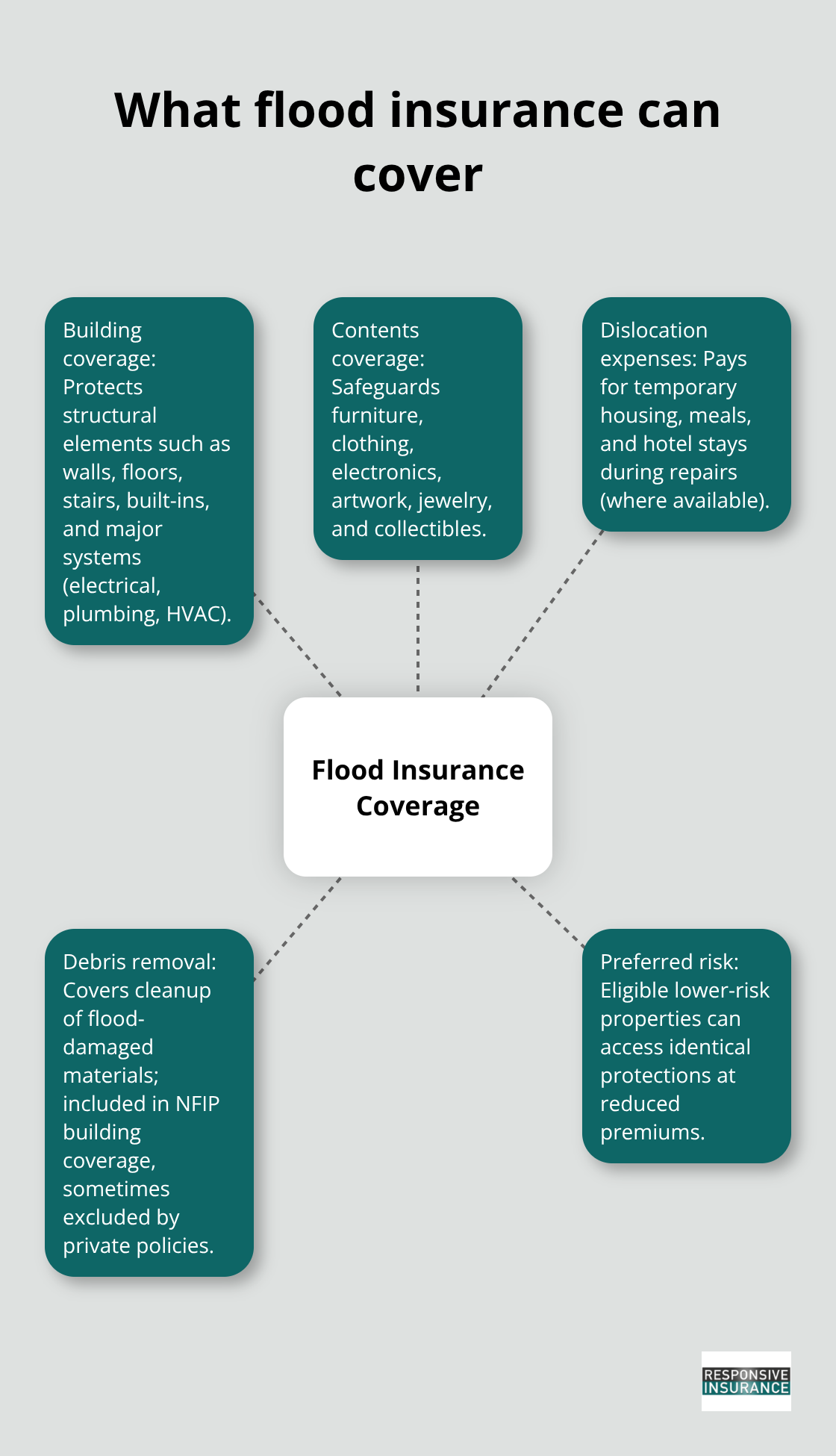

What Does Flood Insurance Actually Cover

Building Coverage Protects Your Home’s Structure

NFIP building coverage protects the structure itself, including walls, ceilings, floors, stairs, built-in appliances, electrical and plumbing systems, and HVAC equipment. The program covers up to $250,000 for single-family homes, which sounds substantial until you price actual structural repairs. A foundation replacement or complete roof restoration easily exceeds $100,000, so understanding your home’s replacement cost matters significantly. This gap between federal limits and real-world repair expenses explains why many Naples homeowners explore private flood insurance options that exceed NFIP maximums.

Contents Coverage Protects Your Belongings

Contents coverage operates separately and protects personal belongings inside your home-furniture, clothing, electronics, artwork, jewelry, and collectibles. NFIP limits contents coverage to $100,000, which many Naples homeowners find inadequate given the cost of replacing a lifetime of possessions. Private flood insurance markets in Florida have expanded specifically because homeowners need protection beyond these federal caps. A high-value home or property with substantial personal collections requires excess flood coverage that private policies can provide.

Additional Endorsements Expand Your Protection

Dislocation expenses coverage pays for temporary housing, meals, and hotel stays while your home undergoes repairs-critical support that prevents financial strain during recovery. Debris removal coverage handles the substantial costs of cleaning up flood-damaged materials, expenses that NFIP building coverage includes but private policies sometimes exclude.

Property owners in lower-risk zones qualify for preferred risk policies offering the same protections at substantially reduced premiums, sometimes 40-60% below standard rates.

Naples Residents Receive Special Rate Discounts

Naples qualifies as a CRS Class 5 community, meaning residents receive up to a 25% discount on standard NFIP policies through the Community Rating System, a program that rewards communities implementing floodplain management measures. This discount applies automatically to eligible properties, reducing your annual premium without sacrificing coverage. An independent flood insurance agent can help identify which coverage combination matches your property’s actual replacement cost and financial situation rather than federal limits that may fall short of reality. Understanding these options positions you to make informed decisions about the specific protection your Naples home requires.

Selecting the Right Flood Policy for Your Naples Home

Identify Your Property’s Flood Zone

Start with the City of Naples interactive flood map tool or contact the City Floodplain Coordinator at 239-213-5039 to determine your property’s flood zone. Your zone designation directly impacts your premium and coverage requirements. Properties in Special Flood Hazard Areas pay higher rates than those in moderate or low-risk zones, sometimes dramatically so.

If your home sits in Zone AE, AH, or VE, your mortgage lender will require flood insurance, and you’ll need an Elevation Certificate prepared by a licensed surveyor to receive an accurate quote. This document measures your home’s elevation relative to the Base Flood Elevation and determines your exact premium tier. Properties in Zone X or outside mapped flood areas qualify for preferred risk policies, which can cost 40–60% less than standard NFIP rates while providing identical coverage.

Calculate Your True Replacement Cost

Once you know your zone, calculate your home’s actual replacement cost rather than relying on the federal limit of $250,000 for building coverage. Real structural repairs in Southwest Florida routinely exceed $150,000 to $200,000, meaning NFIP maximums often fall short. Contents coverage limits of $100,000 similarly underestimate the value of furnishings, electronics, and personal items in most homes. This gap between federal caps and reality explains why private flood insurance markets in Florida have grown substantially over the past five years. Private policies can provide excess coverage that protects against the true cost of recovery, and for lower-risk properties, preferred risk private policies sometimes undercut NFIP premiums while offering higher limits.

Compare Quotes from Multiple Carriers

Obtain quotes from multiple carriers before committing to coverage. NFIP offers a free quote tool through FloodSmart.gov that takes minutes to complete, and you can share that quote with an independent insurance agent who can access private market options. An independent agency compares NFIP and private flood policies side by side so you see the actual cost difference between federal coverage and excess protection. The 30-day waiting period between policy purchase and coverage activation means you cannot delay-securing a quote today protects you before storm season intensifies.

Factor in Community Discounts and Your Budget

Preferred risk properties in CRS Class 5 communities like Naples receive automatic 25% discounts on NFIP policies, reducing the average monthly premium of roughly $53 even further for qualifying homes. Your final decision should weigh the premium cost against your home’s actual replacement value, your mortgage lender’s requirements, and your financial capacity to absorb uninsured losses. A $100 annual difference in premiums becomes insignificant if flood damage leaves you $75,000 short of recovery funds.

Final Thoughts

Protecting your Naples home from flood damage requires action, not hope. A Naples flood policy stands between financial recovery and catastrophic loss, yet most homeowners delay until storm season arrives. Standard homeowners insurance leaves you exposed, government aid appears only after presidential disaster declarations, and out-of-pocket recovery costs can exceed $100,000 or more.

Start by identifying your flood zone through the City of Naples interactive map tool or by calling the City Floodplain Coordinator at 239-213-5039. Calculate your home’s true replacement cost rather than accepting federal limits that often fall short of real repair expenses. Properties in lower-risk zones qualify for preferred risk policies that cost 40–60% less while providing identical coverage, and Naples residents automatically receive up to a 25% CRS discount on NFIP policies.

The 30-day waiting period between purchase and coverage activation means you cannot wait for a storm forecast to buy protection. Contact Responsive Insurance, Inc. to access multiple A-rated carriers and compare your actual options for coverage that matches your property’s specific risk profile and budget.