Naples Commercial Property Insurance: Protecting Your Business Real Estate

Your business property in Naples faces real risks-from hurricanes and flooding to theft and break-ins. Without proper coverage, a single incident could threaten your entire operation.

Naples commercial property insurance protects your building, equipment, and income when disaster strikes. We at Responsive Insurance, Inc. help local business owners understand what coverage they actually need and how to avoid paying for protection they don’t.

What Your Commercial Property Insurance Actually Covers

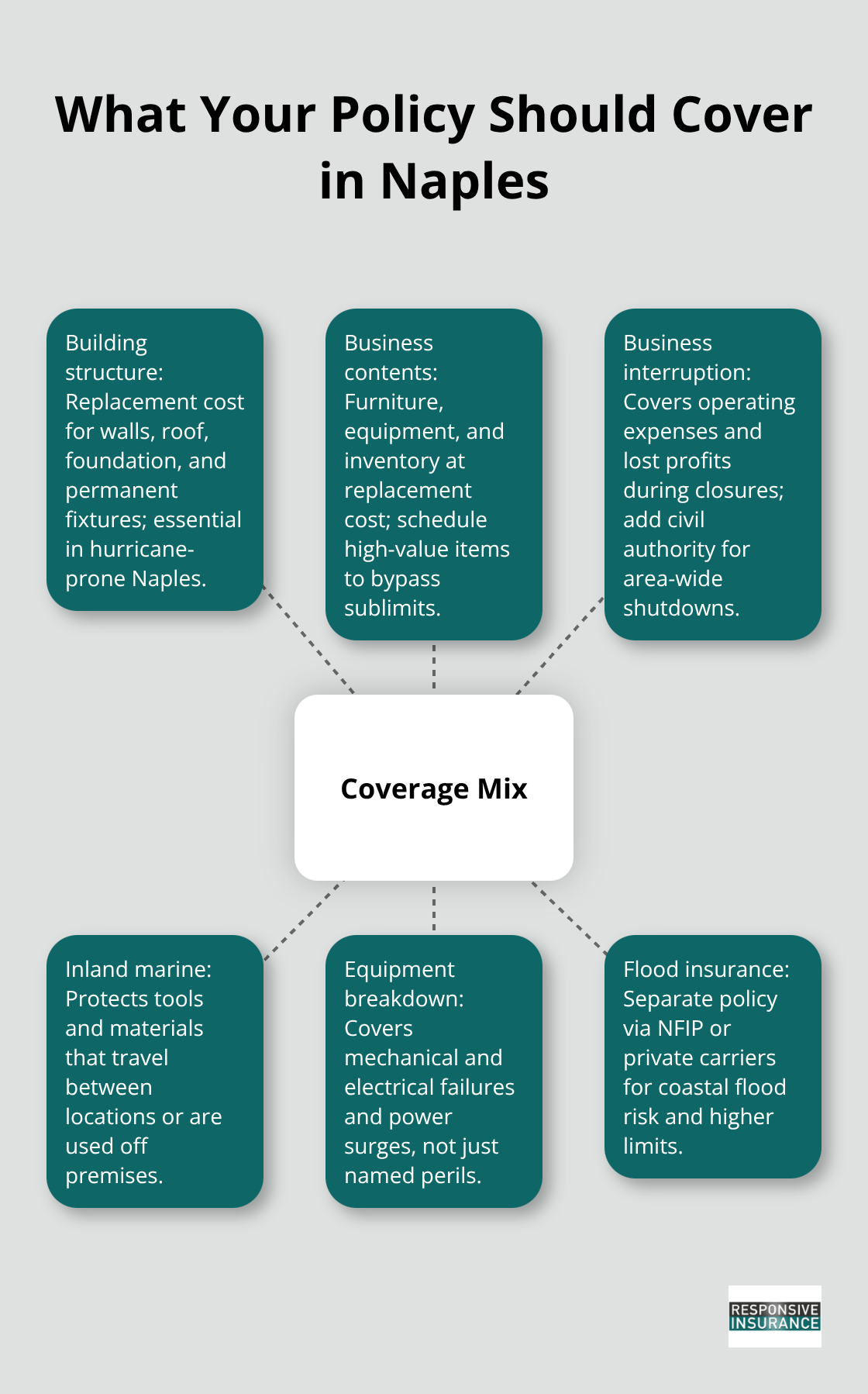

Your commercial property insurance policy protects three distinct areas of your business, and understanding each one matters when you set coverage limits. The building structure itself-walls, roof, foundation, and permanent fixtures like built-in cabinets or HVAC systems-forms the foundation of your coverage. In Naples, where hurricane and windstorm risk is constant, this structural protection is non-negotiable. You’ll want replacement cost coverage rather than actual cash value, since construction costs in Southwest Florida continue climbing. A third-party appraisal of your building gives you a far more accurate replacement figure than generic online estimators, which often undervalue commercial properties in our area.

Your Business Contents Need Separate Protection

Most Business Owner Policies leave a dangerous gap when it comes to what sits inside your building. Furniture, equipment, inventory, and tools typically aren’t fully covered under a standard BOP, which focuses mainly on the structure itself. If a fire destroys $50,000 worth of inventory or a break-in takes your expensive equipment, a basic BOP may leave you significantly underinsured. Commercial property insurance fills this gap by covering your interior assets at replacement cost. For businesses with high-value equipment, you can schedule those specific items to prevent sublimits from capping your recovery. Off-site equipment also needs attention-if your tools or materials regularly leave the premises or travel between locations, an inland marine policy extends coverage beyond your main location.

Income Protection When Disaster Stops Operations

Business interruption coverage covers operating expenses and lost income for a set period of time incurred by a company that closes or is unable to operate normally as a result of physical damage. This matters more than many Naples business owners realize. If a windstorm damages your building and you close for three months, business income coverage pays your rent, utilities, payroll, and lost profits during that period. Civil authority coverage goes further (you receive compensation when government authorities restrict access to your area after a disaster)-you get paid for lost income even if your building wasn’t directly damaged. Most businesses benefit from having both physical asset coverage and income protection working together in a coordinated policy.

Choosing Between Basic and Comprehensive Coverage

A standard BOP covers the building’s structure against perils like weather events and losses such as robbery, but it leaves interior contents exposed. Commercial property insurance fills these gaps with customizable protection for furniture, equipment, lost inventory, landscaping, outdoor signs, and damage to the property of others. You avoid paying for unnecessary coverage while you ensure critical assets receive full protection. The policy adapts as your asset profile changes with business growth or relocation, and you can adjust limits and deductibles to balance premiums with your risk tolerance.

Understanding what each coverage type protects sets the stage for the next critical decision: evaluating your specific property value and determining which additional endorsements your Naples business actually needs.

Why Your Naples Business Needs Commercial Property Insurance

Hurricane Season Brings Real Financial Exposure

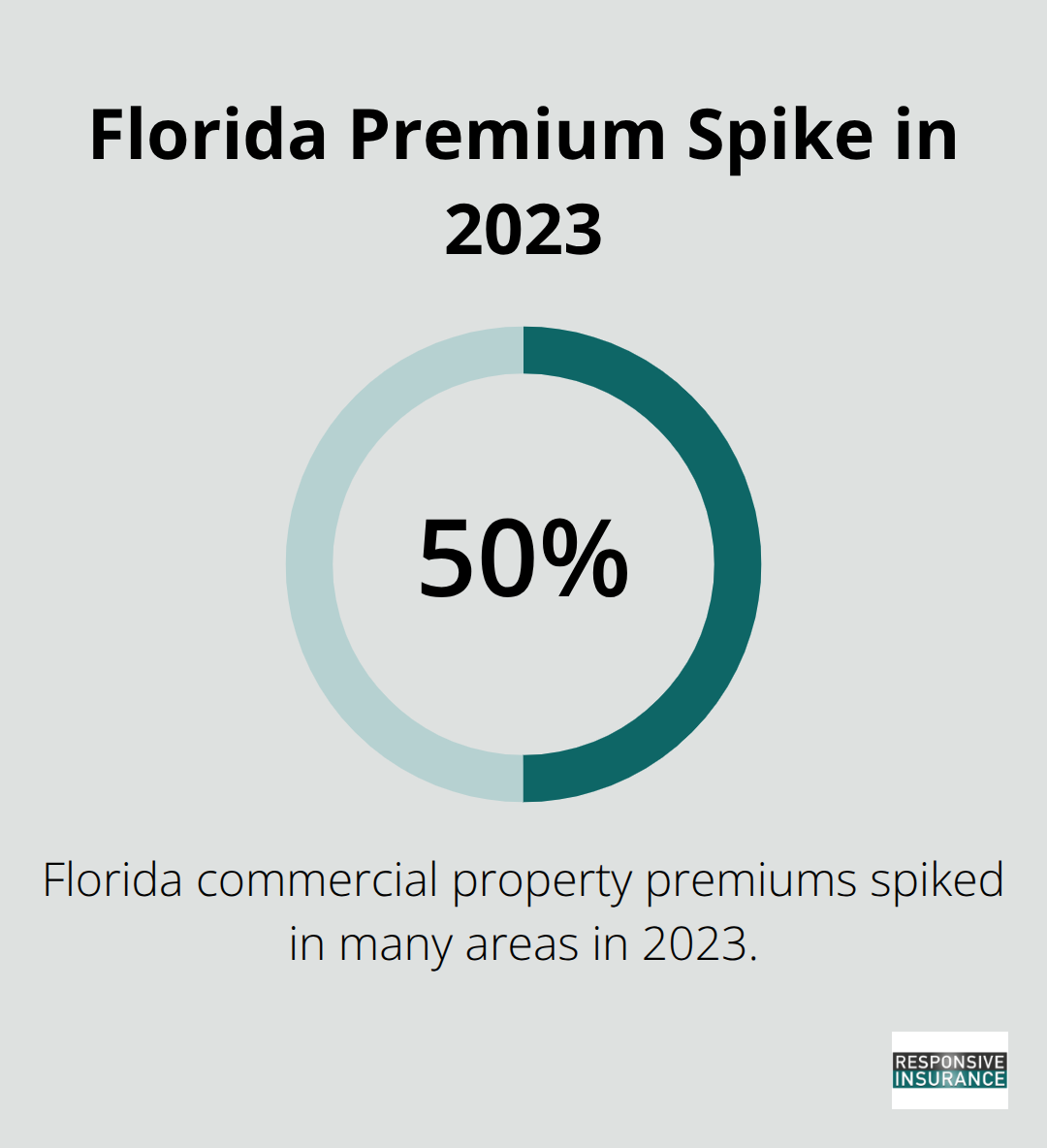

Southwest Florida’s exposure to natural disasters makes commercial property insurance non-negotiable for any business owner in Naples. Hurricane season runs from June through November, and the National Hurricane Center data shows that major hurricanes strike Florida roughly every few years. When a hurricane or tropical storm hits, wind damage alone can cost tens of thousands of dollars to repair a commercial building, and that’s before accounting for water intrusion, inventory loss, or the months of lost income while repairs happen. In 2023, Florida commercial property premiums spiked up to 50 percent in many areas, reflecting the genuine financial exposure that insurers face and that you face without coverage.

Theft and Vandalism Threaten Your Bottom Line

Beyond weather, theft and vandalism plague Naples businesses at a steady rate. A break-in that takes equipment or inventory can wipe out months of profit, especially for retail operations or service businesses that depend on specialized tools. Commercial property insurance protects your assets against these losses, allowing you to recover without depleting cash reserves or taking on debt.

Your Lender and Landlord Require Coverage

Your landlord or lender won’t let you ignore this risk. If you lease your space or financed your building with a mortgage, your lease agreement or loan documents almost certainly require you to carry commercial property insurance. Lenders view uninsured property as unacceptable collateral, and landlords protect their investment by making insurance mandatory in the lease. Skipping coverage to save money puts you in direct violation of those obligations and leaves you personally liable if something happens.

Building a Recovery Strategy That Works

A comprehensive property insurance approach with both building coverage and business interruption protection helps you recover fast after a disaster instead of struggling through months of downtime and financial strain. When you work with an independent agent to build your policy, you gain access to multiple carriers and options rather than being locked into one company’s offerings. Different insurers price windstorm risk, flood exposure, and equipment breakdown differently, so shopping around can save you thousands annually. The key is moving beyond the bare minimum and ensuring your replacement cost limits actually match what it would cost to rebuild or restock in today’s market, not what your property cost five years ago.

Now that you understand why commercial property insurance matters in Naples, the next step involves assessing your actual property value and determining which coverage options fit your specific business needs.

How to Choose the Right Commercial Property Coverage

Find Your Actual Replacement Cost

Naples business owners who recover quickly after a loss separate themselves by calculating replacement cost accurately from the start. Online property estimators and rough calculations based on your purchase price five years ago will fail you when you actually need to rebuild. Construction costs in Southwest Florida have climbed steadily, and what your building cost to construct then bears little resemblance to what it costs today. A third-party appraisal from a local appraiser who understands Naples commercial real estate provides a defensible, accurate figure that insurers will accept and that actually reflects current replacement expenses. This single step prevents the painful scenario where you receive an insurance check that covers only 70 percent of what reconstruction actually costs.

Obtain this appraisal before you shop for coverage, not after, so you can request quotes based on realistic numbers. For business contents, itemize your furniture, equipment, and inventory rather than guessing at totals. If you operate a retail business with $75,000 in stock, document that figure. If you have specialized equipment worth $40,000, list it separately. This inventory becomes the foundation for setting coverage limits that actually protect you. High-value items warrant scheduling on your policy, which removes sublimits and guarantees full replacement value for those specific assets.

Equipment that leaves your location regularly or travels between job sites needs inland marine coverage, which extends protection beyond your primary address. Many Naples business owners overlook this gap and discover too late that off-site equipment lacks coverage under their standard policy.

Select Coverage Extensions That Match Your Exposure

Equipment breakdown coverage protects against losses from mechanical failure, electrical breakdown, and power surges that damage machinery and systems your business depends on daily. If your HVAC system fails or a power surge destroys your computer servers, this coverage pays for repairs or replacement without waiting for a weather event or other covered peril. For Naples businesses, this matters more than it does in regions with stable power supplies.

Sewer and drain backup coverage addresses a real gap in standard policies, since most exclude water damage from backed-up sewers or drains. Heavy rains and flooding in Southwest Florida make this endorsement practical protection rather than unnecessary add-on. Civil authority coverage compensates you for lost income when government authorities restrict access to your area after a disaster, even if your building sustained no direct damage. If a hurricane damages neighboring properties and authorities close the street for weeks, this coverage pays your operating expenses and lost profits.

Flood coverage deserves separate attention because standard commercial property policies exclude it entirely. The National Flood Insurance Program offers coverage if your property qualifies, but private flood insurance through carriers often provides broader terms and higher limits. Review your flood risk using FEMA flood maps and local drainage patterns rather than assuming you’re safe because your building sits on slightly higher ground. Coastal properties in Naples face genuine flood exposure that standard policies ignore completely.

Compare Multiple Carriers to Reveal Real Price Differences

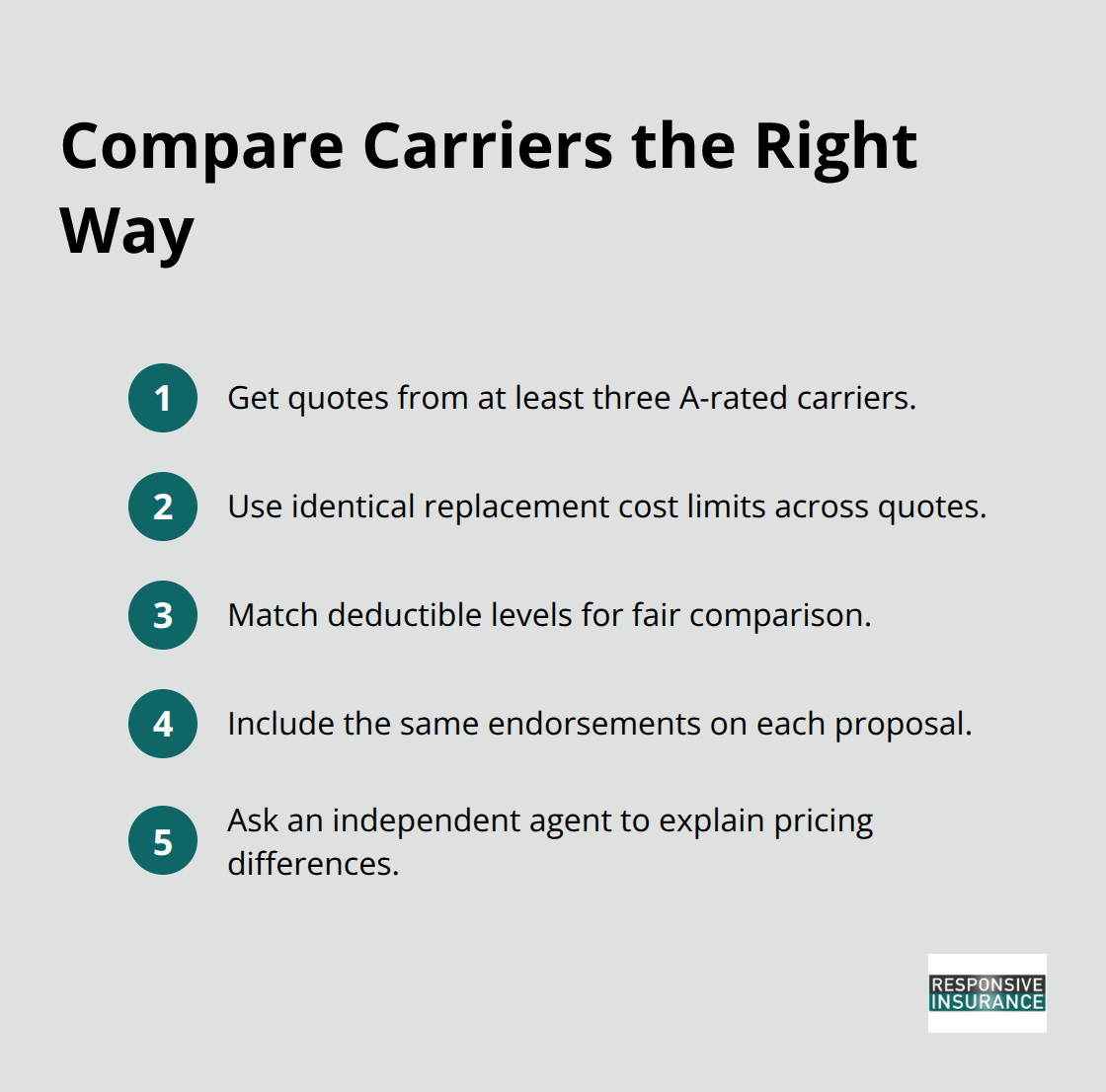

An independent agent gives you access to multiple A-rated carriers rather than locking you into one company’s pricing and underwriting standards. Different insurers price windstorm exposure, flood risk, and equipment breakdown coverage differently based on their own claims experience and risk appetite. One carrier might charge $2,400 annually for your coverage while another quotes $1,800 for nearly identical limits. That $600 annual difference compounds over five or ten years into thousands of dollars saved or wasted.

Request quotes from at least three different carriers on the same coverage specifications so you compare apples to apples. Specify the same replacement cost limits, the same deductible levels, and the same endorsements across all quotes. This transparency reveals whether price differences reflect real underwriting variations or simply different premium structures.

An agent who represents multiple carriers can explain why one insurer charges more for windstorm coverage or why another applies a lower rate for equipment breakdown. These conversations matter because they help you understand your actual risk profile through an insurer’s eyes.

Some carriers specialize in Naples coastal properties and price that exposure competitively, while others treat Southwest Florida as high-risk territory and charge accordingly. An agent who knows local market dynamics saves you money while ensuring your coverage actually fits your business.

Final Thoughts

Protecting your Naples business property requires moving beyond basic coverage and building a strategy that reflects what your assets cost to replace today. Start with a third-party appraisal of your building and an itemized list of your business contents and equipment-these concrete numbers become the foundation for requesting quotes from multiple carriers. An independent agent who represents multiple A-rated insurers can explain how different companies price windstorm exposure, flood risk, and equipment breakdown for your specific property.

Naples commercial property insurance isn’t a checkbox item or a cost to minimize; it’s the financial foundation that lets you rebuild without depleting savings or taking on debt when disaster strikes. The difference between underinsurance and adequate coverage often amounts to tens of thousands of dollars when you actually file a claim. Your building structure, interior contents, and operating income all deserve protection that matches your real exposure.

We at Responsive Insurance, Inc. work with Naples business owners to compare coverage options and find policies that fit your needs rather than leaving gaps or paying for unnecessary protection. Contact us to discuss your property value, review your current coverage, and get quotes from carriers that understand Southwest Florida’s unique risks.