Short Term Rental Liability Florida: Protecting Hosts And Listings

Short-term rental liability in Florida is a real concern for hosts who want to protect their investment. Guest injuries, property damage claims, and legal disputes are happening more frequently in the vacation rental market.

At Responsive Insurance, Inc., we’ve seen firsthand how quickly a single incident can threaten a host’s financial security. This guide walks you through the liability risks you face, the coverage options available, and the regulations you need to follow.

What Liability Risks Should Florida Rental Hosts Actually Worry About

Guest Injuries Create Immediate Financial Threats

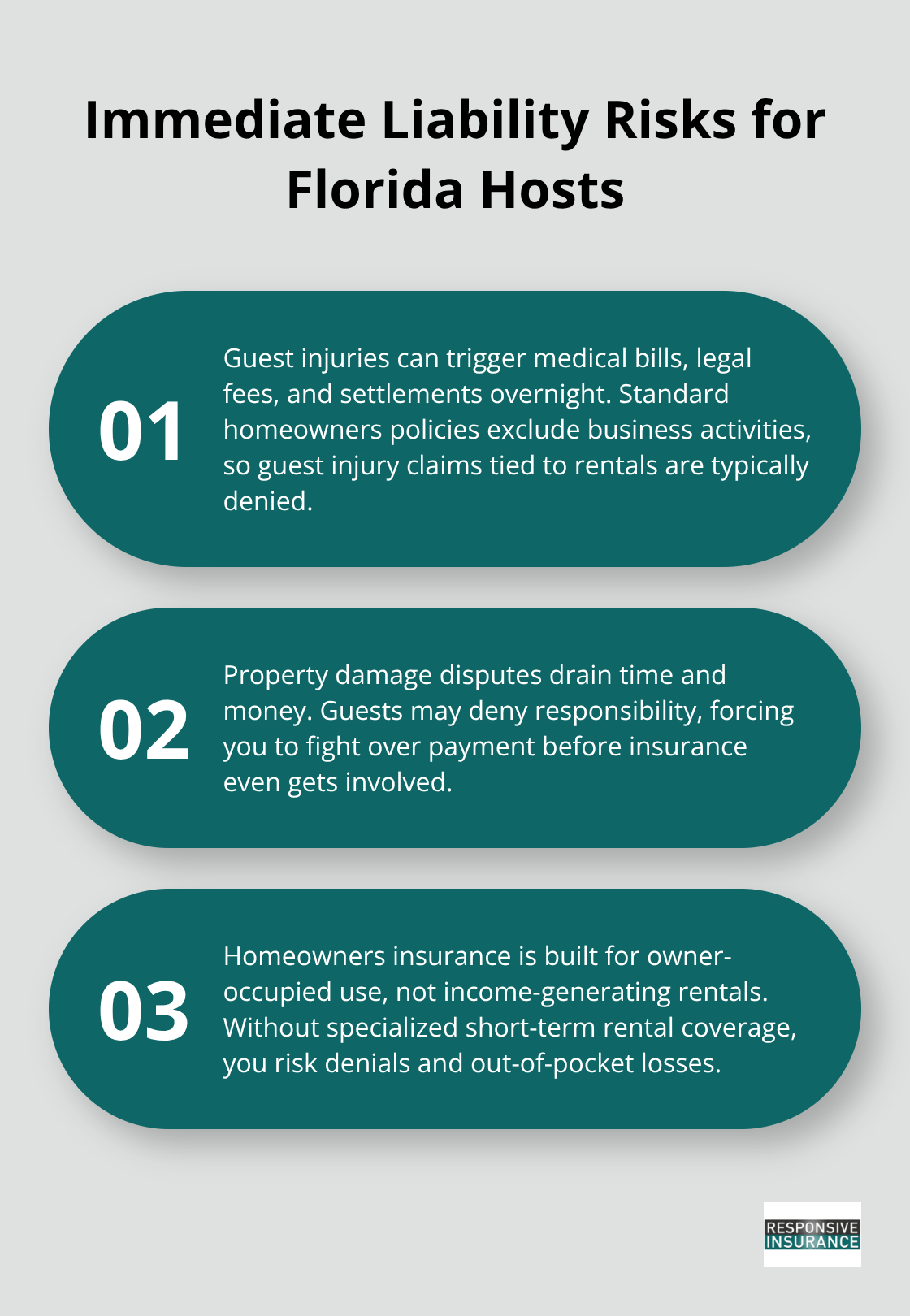

Guest injuries represent the most immediate financial threat to Florida short-term rental hosts. A visitor slips on your pool deck, falls down stairs, or suffers an injury during their stay, and suddenly you face medical bills, legal fees, and potential lawsuit settlements. Standard homeowners policies explicitly exclude business activities, meaning your regular home insurance will deny the claim outright if a guest is injured while renting your property.

Property damage claims follow the same pattern. Guests damage furniture, break appliances, punch holes in walls, or cause plumbing disasters that cost thousands to repair. What makes this worse is that guests often dispute liability, claiming the damage existed before arrival or that they bear no responsibility. You’ll spend money fighting over who pays before insurance even enters the picture.

Host Negligence and Legal Responsibility

Host negligence adds another layer of financial exposure. Florida courts hold property owners to a duty of care standard, meaning you’re legally responsible for maintaining safe conditions. If a guest discovers a loose railing, faulty electrical outlet, or broken step that causes injury, you can be held liable even if you weren’t directly negligent.

The plaintiff’s attorney will argue you should have inspected the property, fixed hazards, and disclosed known dangers. This is why documentation matters tremendously. Hosts who maintain dated photo records of property conditions before each guest arrival have significantly stronger legal defenses than those without evidence.

Litigation Trends and Off-Property Exposure

Litigation in the vacation rental market has accelerated noticeably. Guests are more willing to pursue legal action when injured, and plaintiff attorneys actively solicit short-term rental cases because they know hosts often lack proper insurance coverage.

Your liability exposure extends beyond your property boundaries too. If a guest causes damage at an off-site location while using amenities you provided (kayaks, bicycles, or other equipment), you could face claims. The cost of defending even a frivolous lawsuit in Florida ranges from ten thousand to fifty thousand dollars in legal fees before any settlement or judgment.

Without specialized short-term rental liability coverage, these costs come directly from your personal assets. This reality makes the difference between standard homeowners insurance and dedicated short-term rental policies critical for protecting your rental business and personal finances. Understanding what coverage options actually exist for Florida hosts requires examining how standard policies fail and what specialized alternatives provide.

Why Your Homeowners Policy Won’t Cover Your Rental Business

The Business Activity Exclusion Blocks All Guest-Related Claims

Your standard homeowners policy covers owner-occupied residences, not income-generating rental operations. The moment you accept payment from guests, your policy’s business activity exclusion activates, and coverage disappears. Insurance companies classify short-term rental hosting as a commercial enterprise, fundamentally different from a primary residence. This distinction matters enormously because guest-related claims-injuries, property damage, liability disputes-fall squarely into the business category your homeowners policy explicitly rejects.

When a guest slips on your pool deck and files a claim, your insurer will deny it. When guests cause damage, you’ll receive a denial letter. Misrepresenting your rental activity to avoid this reality creates worse problems: claim denials, immediate policy cancellation, and significantly higher premiums when you try to obtain coverage elsewhere.

Platform Protections Provide Inadequate Backup Coverage

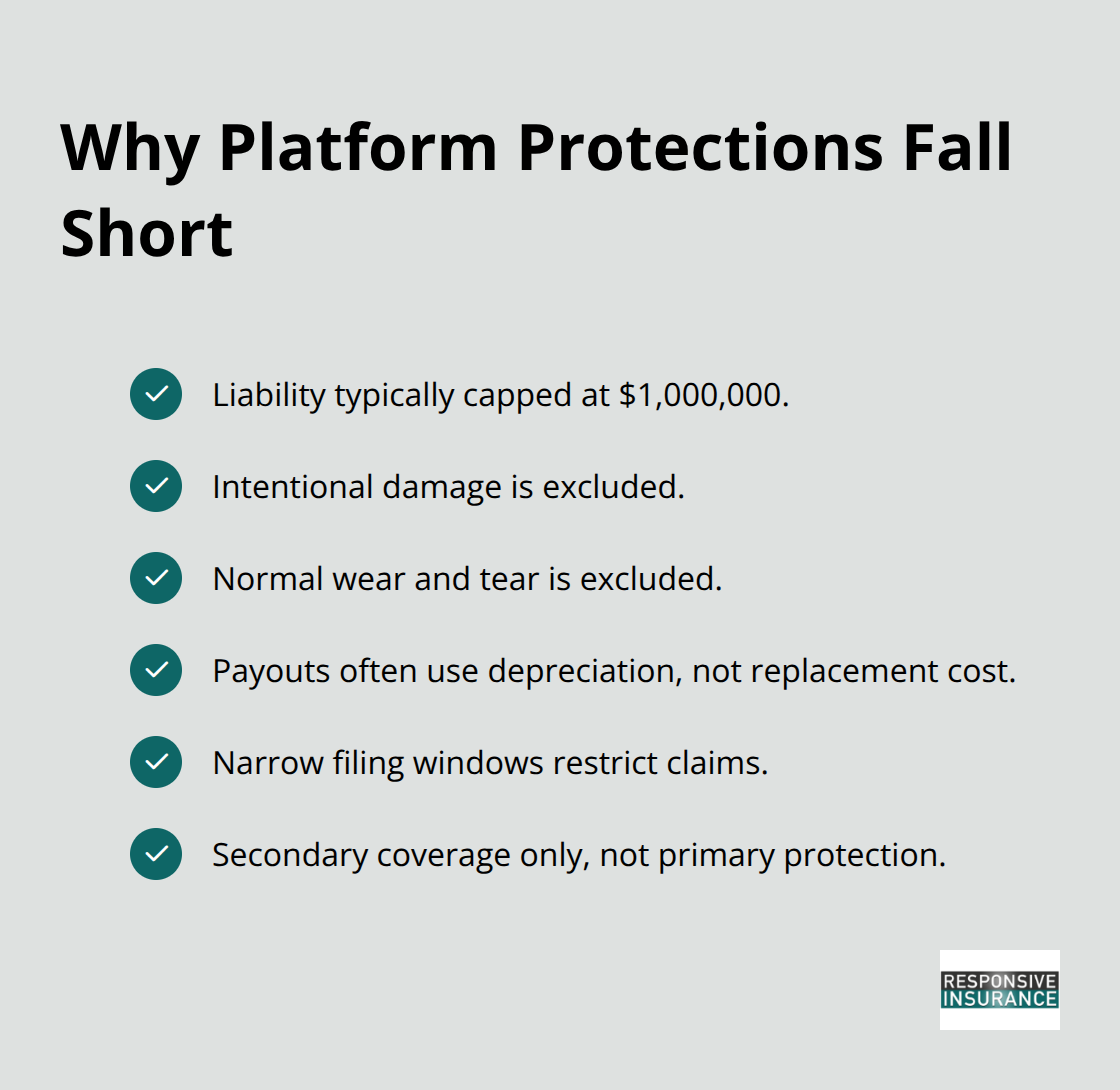

Platform protections from Airbnb and Vrbo offer minimal backup. These protections typically cap liability at one million dollars, exclude intentional damage and normal wear-and-tear, apply depreciation rather than replacement cost value, and contain narrow filing windows. They function as secondary coverage only, not primary protection. You cannot rely on them as your main defense against guest-related financial losses.

Specialized Short-Term Rental Policies Close Critical Coverage Gaps

Specialized short-term rental insurance policies eliminate these gaps entirely. These policies cover property damage from guest actions, provide commercial general liability starting at one million dollars or higher, protect your business revenue if a covered incident makes the property uninhabitable, and cover amenities you provide like kayaks, bicycles, or hot tubs. Florida hosts specifically benefit from endorsements for bed bug and pest infestation liability, squatter protection if guests refuse to leave, and pet liability with no breed restrictions.

Understanding Costs and Finding the Right Coverage

Costs vary significantly based on location, property value, construction type, rental frequency, and amenities. Independent agencies work with multiple carriers to find policies matching your specific risk profile and property characteristics, helping you avoid overpaying for unnecessary coverage or leaving dangerous gaps in protection.

The difference between standard homeowners insurance and dedicated rental coverage directly determines whether a guest injury or property damage claim financially devastates you or gets handled by your insurer as intended. With proper coverage in place, you can focus on running your rental business rather than worrying about catastrophic liability exposure. Understanding what specific coverage options exist for Florida hosts requires examining the different types of policies available and how they address the unique risks of short-term rental operations.

Florida’s Short-Term Rental Rules You Cannot Ignore

Registration Requirements in Collier County

Florida hosts operating in Collier County face specific registration requirements that carry real penalties for non-compliance. If you rent your property for stays under 30 consecutive days more than three times per calendar year, you must register with Collier County under Ordinance 2021-45, effective January 3, 2022. The registration process happens online through the GMD Public Portal, and you’ll need to obtain a DBPR vacation rental license before accepting guests. Failure to register results in fines up to $500 per violation per day, which compounds quickly if enforcement discovers an unregistered listing. Properties in Naples, Marco Island, and Everglades City operate under different municipal rules, so verify your property’s status through the Trim Notices on the Collier County Property Appraiser website.

Advertising and Registration Number Requirements

Once registered, your Collier County Rental Registration Number must appear in all advertising across print, radio, video, online platforms, social media, and sharing economy sites like Airbnb and Vrbo. This requirement is not optional-missing your registration number from listings violates the ordinance. You’ll also need to designate a Responsible Party available 24/7 by phone to address law enforcement actions or code violations, and this person must appear onsite within one business day of notification. If ownership changes or your Designated Responsible Party changes, notify the county within ten business days or face additional violations.

Tax Obligations and Property Maintenance Standards

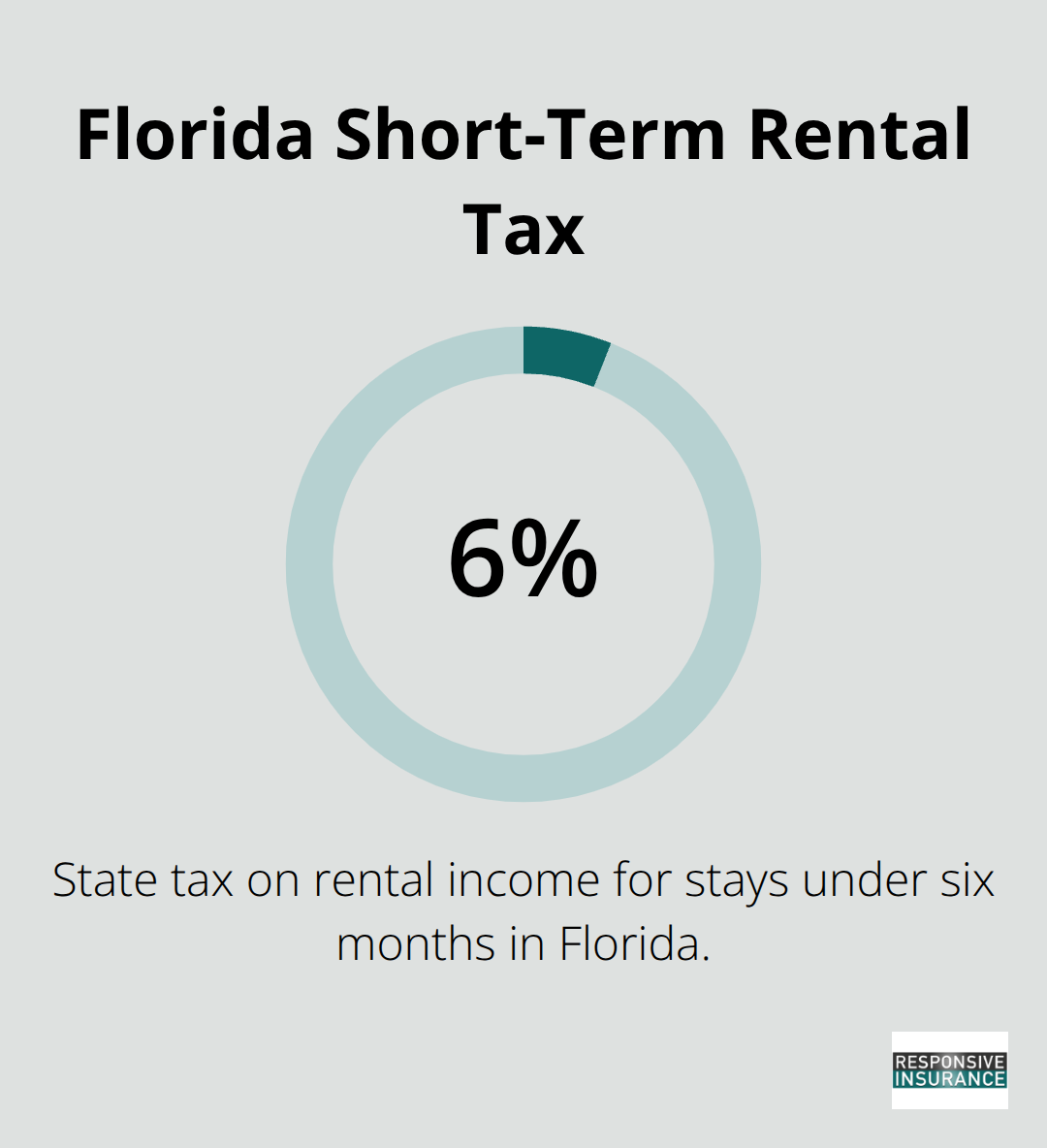

Florida imposes a 6% tax on rental income for stays under six months, per Florida statute F.S. 125.0104(3)(a) and F.S. Chapter 212. You’re responsible for collecting and remitting this tax, and the county tracks compliance through your registration. Property maintenance standards fall under Collier County Code Ordinance No. 2010-02, meaning your rental must meet current building codes, fire prevention codes, and occupancy limits-violations trigger enforcement action separate from your rental registration status.

Homeowners Association Restrictions and Insurance Implications

Homeowners association rules may further restrict short-term rentals or prohibit them entirely, so review your HOA documents before listing. Some associations require approval, limit rental days per year, or mandate specific insurance coverage levels. These regulatory layers create separate liability exposure that insurance must address. An independent insurance agency can help you verify that your homeowners insurance meets both county ordinances and HOA requirements, preventing gaps that could void protection when claims occur. Many hosts overlook these compliance requirements, assuming registration alone satisfies obligations, but enforcement actions and HOA violations create financial consequences that proper insurance coverage must protect against.

Final Thoughts

Short-term rental liability in Florida demands immediate action from every host who accepts guests. Your homeowners policy will deny claims tied to rental activities, platform protections leave dangerous gaps, and fines for regulatory violations reach five hundred dollars per violation per day. A specialized short-term rental policy covers guest-caused property damage, commercial general liability starting at one million dollars, loss of rental income when covered events make your property uninhabitable, and Florida-specific endorsements for bed bugs, squatters, and pet liability that address the actual risks you face.

Compliance with Collier County registration requirements, tax obligations, and property maintenance standards protects you from enforcement action and separate liability exposure. Your Designated Responsible Party must remain available twenty-four hours daily, your registration number must appear across all advertising platforms, and you must maintain property conditions that meet current building codes and fire prevention standards. These regulatory layers create financial consequences that proper insurance coverage must address alongside guest-related claims.

Three concrete steps protect your rental business immediately. First, obtain quotes from multiple carriers through an independent agency that understands Florida’s short-term rental environment and can compare coverage options matching your specific property characteristics. Second, verify that your coverage meets both county ordinances and any homeowners association restrictions specific to your property. Third, implement risk management practices like documenting property conditions with time-stamped photos before each guest arrival, maintaining clear house rules with digital guest acknowledgment, and keeping a comprehensive welcome book with emergency contacts and safety instructions. We at Responsive Insurance, Inc. work with multiple A-rated insurance companies to help Naples hosts find short-term rental insurance that closes protection gaps without overpaying for unnecessary coverage.