Commercial Vehicle Insurance Florida Guide

Running a business with vehicles in Florida means understanding your insurance obligations. Commercial vehicle insurance in Florida protects your assets, covers liability claims, and keeps your operation compliant with state law.

At Responsive Insurance, Inc., we help Naples business owners navigate coverage options that match their specific needs. This guide walks you through what’s required, what it costs, and how to select the right policy for your fleet.

What Your Commercial Vehicle Insurance Actually Covers

Liability Coverage: Your Legal Obligation

Commercial vehicle insurance in Florida protects three critical areas of your business operations. Liability coverage pays for injuries and property damage you cause to others, and Florida law mandates this protection. Florida requires minimum liability coverage, though specific amounts depend on your vehicle type and weight classification. However, this minimum falls short for most businesses. If one of your drivers injures someone seriously, a single medical bill can easily exceed $50,000. Property damage claims from hitting another vehicle or structure accumulate rapidly too.

Try carrying at least $100,000 in bodily injury coverage and $50,000 in property damage coverage, especially if you operate multiple vehicles or travel high-traffic routes in Naples. Higher limits protect your business assets when accidents happen. The difference in premium cost between minimum and recommended coverage is often smaller than the financial exposure you face with inadequate limits.

Collision and Comprehensive: Protecting Your Fleet

Collision and comprehensive coverage protects your own vehicles from accidents and non-accident damage. Collision covers damage from crashes with other vehicles or objects. Comprehensive covers theft, weather damage, vandalism, and natural disasters like the hurricanes Florida experiences regularly. Given Florida’s hurricane season and theft rates, comprehensive coverage is not optional for most Naples businesses.

Your deductible typically ranges from $500 to $1,000, and choosing a higher deductible lowers your premium but increases your out-of-pocket costs after a claim. This trade-off requires honest assessment of your cash flow and risk tolerance. Most businesses find that a $750 or $1,000 deductible balances affordability with reasonable protection.

Uninsured and Underinsured Motorist Coverage: The Overlooked Protection

Uninsured and underinsured motorist coverage is the protection most Florida business owners overlook, yet it shields you when another driver lacks adequate insurance. The Hartford reports that not all commercial drivers carry sufficient coverage, meaning you could face significant losses if hit by an underinsured operator. This coverage applies to your vehicle damage and medical expenses your liability insurance won’t cover.

Florida has about 3 million small businesses according to the U.S. Small Business Administration, and many operate with minimal insurance. Carrying UM/UIM coverage separates responsible operators from those taking unnecessary financial risks. Your agent can explain which coverages apply to hired vehicles your employees rent or non-owned vehicles they use for business, since these situations require specific endorsements to your policy.

Understanding these three coverage pillars positions you to make informed decisions about your fleet protection. The next section examines what Florida law actually requires and how much you should expect to pay for adequate coverage.

Florida Commercial Vehicle Insurance Requirements and Costs

State Minimum Coverage Requirements

Florida law mandates minimum commercial auto insurance of Personal Injury Protection (PIP) and Property Damage Liability (PDL) for all business vehicles. These minimums prove dangerously low for operating a profitable business. A single serious injury claim easily exceeds these minimum thresholds in medical costs alone, leaving your business exposed to devastating liability. The U.S. Small Business Administration reports Florida has about 3 million small businesses, and many operate at these inadequate minimum levels, gambling with their assets.

For-hire passenger transport vehicles like taxis and limousines face much stricter requirements: $125,000 per person and $250,000 per incident in bodily injury liability, plus $50,000 in property damage liability. Your specific vehicle weight and classification determine your exact minimums, so verify requirements with your agent before assuming the basic limits apply to your fleet.

Factors That Affect Your Premiums

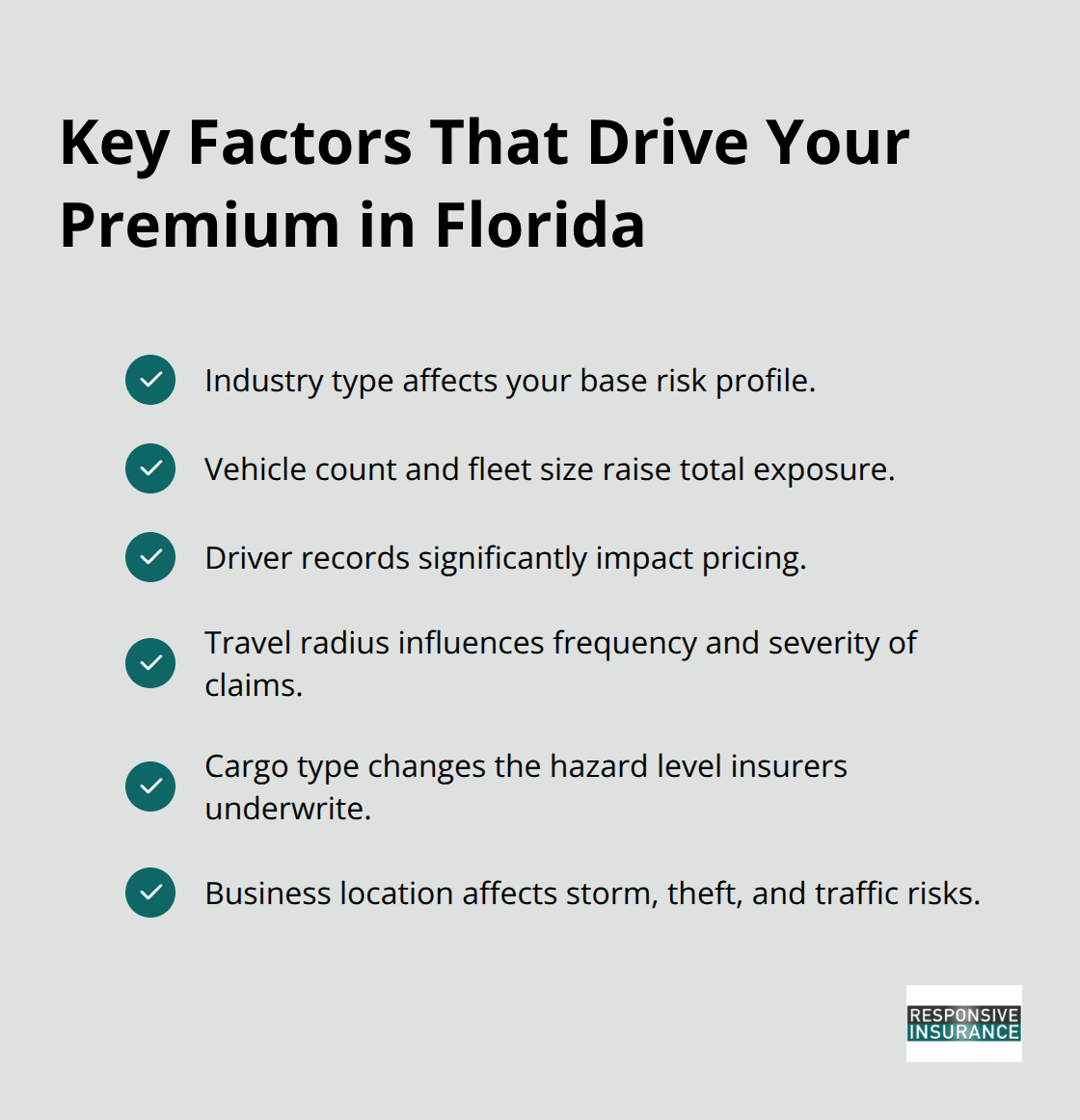

Premium costs for Florida commercial auto insurance average between $250 and $1,370 monthly depending on your risk profile, according to Insurify data. Weather exposure drives higher premiums here compared to other states, as hurricanes and tropical storms increase both claim frequency and severity. The Hartford reports that industry type, vehicle count, driver records, travel radius, cargo type, and location all heavily influence what you pay.

A delivery business operating five vans throughout Naples pays dramatically more than a consulting firm with one company car. Your drivers’ records matter significantly too-a single at-fault accident or traffic violation can increase premiums by 20 to 40 percent. Choosing higher deductibles like $1,000 instead of $500 reduces your monthly cost but means larger out-of-pocket expenses after claims. Most Naples businesses find the sweet spot at $750 deductibles, balancing affordability with manageable financial exposure.

Average Costs for Different Business Types

When obtaining quotes, gather complete information on every vehicle, every driver, typical weekly hours, and your specific business operations so insurers can calculate accurate pricing. Comparing quotes from multiple carriers often reveals 30 to 50 percent price variations for identical coverage, making the effort to shop around financially worthwhile. Your deductible choice, fleet size, and industry classification create substantial cost differences across providers.

The Hartford notes that industry-specific coverage options (for beauty shops, consulting, photography, retail, technology, and restaurants) allow you to tailor protection to your business. These customized approaches typically cost less than broad, one-size-fits-all policies because insurers adjust pricing to match your actual operational risks. Getting multiple quotes takes time but protects your bottom line significantly.

Moving Forward With Your Coverage Decision

Understanding Florida’s minimum requirements and the factors that shape your premiums positions you to make smart coverage choices. The next section walks you through assessing your specific business needs and comparing policies across multiple insurers to find the right fit for your operation.

Selecting the Right Policy for Your Naples Business

Organize Your Fleet and Operations Information

Start your policy search with honest answers about your fleet and operations before comparing quotes. Calculate exactly how many vehicles you operate, list every driver who will use them, and document your typical weekly driving hours and routes. A delivery business running five vans across Naples daily faces entirely different risks than a consulting firm with one vehicle parked most days. Your insurance agent needs this operational clarity to quote accurately-vague descriptions lead to either overpriced coverage or dangerous gaps when claims arise.

The Hartford emphasizes that industry type, vehicle weight classifications, driver records, and travel radius heavily shape premiums, meaning precision in your initial assessment saves thousands annually. Gather this information before contacting insurers so you can provide consistent details across all quotes.

Compare Quotes From Multiple Carriers

Contact three to five insurers for quotes rather than settling on the first option. Insurify data shows that premium variations of 30 to 50 percent exist for identical coverage across different carriers, making comparison shopping financially essential. When gathering quotes, ensure each insurer prices the same vehicles, drivers, deductibles, and coverage limits so you’re comparing apples to apples.

Request quotes with multiple deductible and limit combinations so you see the actual cost differences rather than guessing. This approach reveals which carriers offer the best value for your specific operational profile and helps you avoid overpaying for unnecessary coverage. Get insurance quotes from an independent agency that can shop multiple carriers for you.

Select Your Deductible and Coverage Limits

Your deductible selection directly impacts both your monthly cost and out-of-pocket expenses after an accident, requiring deliberate choice rather than default acceptance. A $500 deductible costs more monthly than $1,000 but means smaller repair bills when claims occur. Most Naples businesses operating tight cash flows find that $750 deductibles balance affordability with manageable financial exposure.

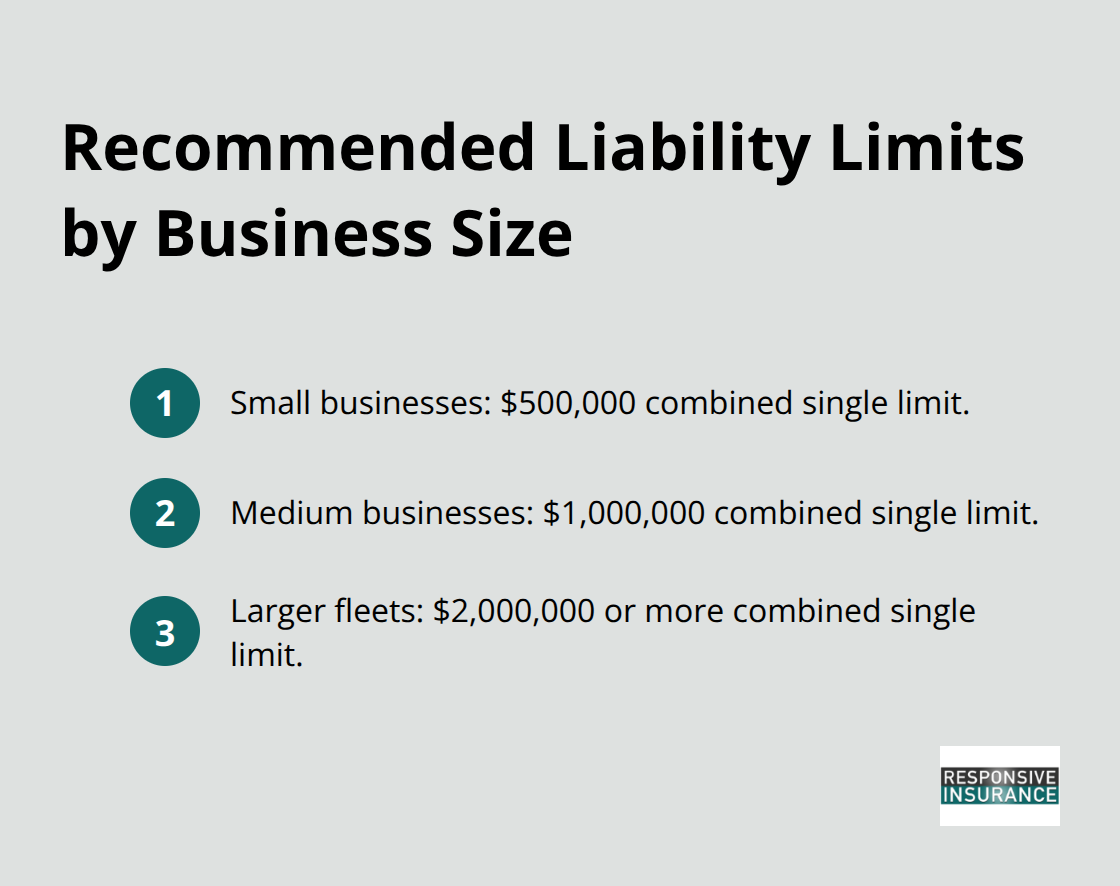

Higher liability limits deserve serious consideration even though Florida’s minimums are dangerously low. Recommended coverage varies by business size: small businesses typically need $500,000 in combined single limits, medium businesses $1,000,000, and larger fleets $2,000,000 or more. The difference in premium cost between minimum and recommended coverage is often smaller than the financial exposure you face with inadequate limits.

Tailor Coverage to Your Specific Business Risks

Don’t automatically add every optional coverage; instead, discuss your specific operational risks with your insurance agent. A construction company hauling materials needs different protections than a service business using passenger vehicles. Your agent can explain which coverages apply to hired vehicles your employees rent or non-owned vehicles they use for business, since these situations require specific endorsements to your policy.

The Hartford notes that industry-specific coverage options (for beauty shops, consulting, photography, retail, technology, and restaurants) allow you to tailor protection to your business. These customized approaches typically cost less than broad, one-size-fits-all policies because insurers adjust pricing to match your actual operational risks. Getting multiple quotes takes time but protects your bottom line significantly.

Final Thoughts

Commercial vehicle insurance in Florida protects your business from financial devastation when accidents happen. Florida’s minimum coverage limits prove dangerously inadequate for most operations, as a single serious injury claim or property damage incident can exceed these minimums within hours and leave your assets exposed. Higher liability limits cost far less than the financial exposure you face without them, and your deductible choice directly impacts both your monthly premium and out-of-pocket costs after claims.

Finding the right commercial vehicle insurance Florida policy requires gathering accurate information about your fleet and operations before contacting insurers. Premium variations of 30 to 50 percent exist across carriers for identical coverage, making comparison shopping financially essential. Contact three to five insurers with consistent details about your vehicles, drivers, and business operations so you can compare apples to apples and request quotes with multiple deductible and limit combinations to see actual cost differences.

Gather your fleet information today and request quotes from multiple carriers this week. We at Responsive Insurance, Inc. help Naples business owners navigate coverage options that match their specific needs, and as an independent insurance agency, we work with multiple A-rated insurance companies to compare coverage and find the best fit for your business. Contact us for a personalized quote and let our team guide you toward the right protection for your operation.