Flood Insurance for Contents Only Coverage Guide

Renters and condo owners in Naples face unique flood risks, yet many overlook a straightforward protection: flood insurance for contents only. This coverage shields your belongings-furniture, electronics, clothing-without covering the building itself, making it affordable and practical for those who don’t own their homes.

At Responsive Insurance, Inc., we’ve helped countless residents understand why contents-only policies matter in Southwest Florida. This guide walks you through coverage limits, what’s protected, and how to file claims when water damage strikes.

Understanding Contents Only Flood Insurance

What Contents Only Coverage Actually Protects

Contents only flood insurance covers your personal belongings inside a building but not the structure itself. This means furniture, electronics, clothing, curtains, washers and dryers, microwaves, and carpet installed over wood floors receive protection when floodwaters damage them. According to FEMA and the National Flood Insurance Program, contents coverage extends up to $100,000 for renters and condo owners, which covers most household possessions for typical residents in Naples. High-value items like original artwork and furs carry a $2,500 sub-limit, so you need to know what sits in your home and whether standard limits work for you. The key point: contents coverage protects only what’s inside the dwelling, not the building’s foundation, walls, electrical systems, plumbing, or built-in appliances. Many renters assume their landlord’s building policy covers their belongings, but it doesn’t. Your landlord insures the structure; you must insure your stuff.

Why Renters and Ground-Floor Condo Owners Face Real Risk

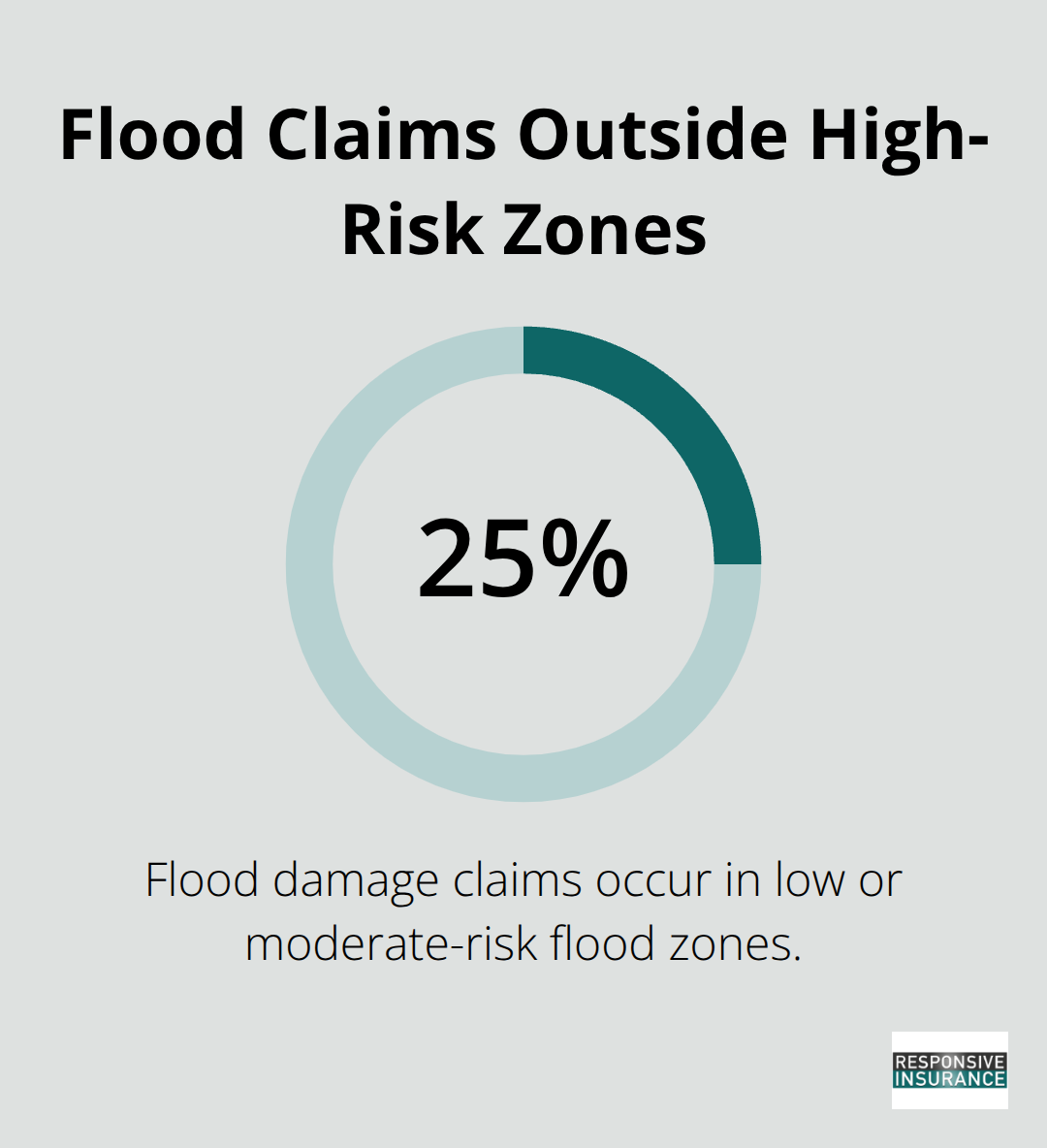

About 25 percent of flood damage claims occur in low or moderate-risk flood zones, not just in the high-hazard areas everyone talks about. This statistic from FEMA data shows that renters and condo owners outside mandatory insurance zones still experience significant water damage. Ground-floor condo owners face particular vulnerability because even if the condo association carries building coverage, that policy covers only the structure, not your personal property inside your unit.

You remain exposed unless you purchase contents coverage separately. In Naples, typical annual costs for contents only policies range from $450 to $1,500 depending on your flood zone and coverage limits, making it far more affordable than replacing furniture, electronics, and clothing out of pocket after a flood event.

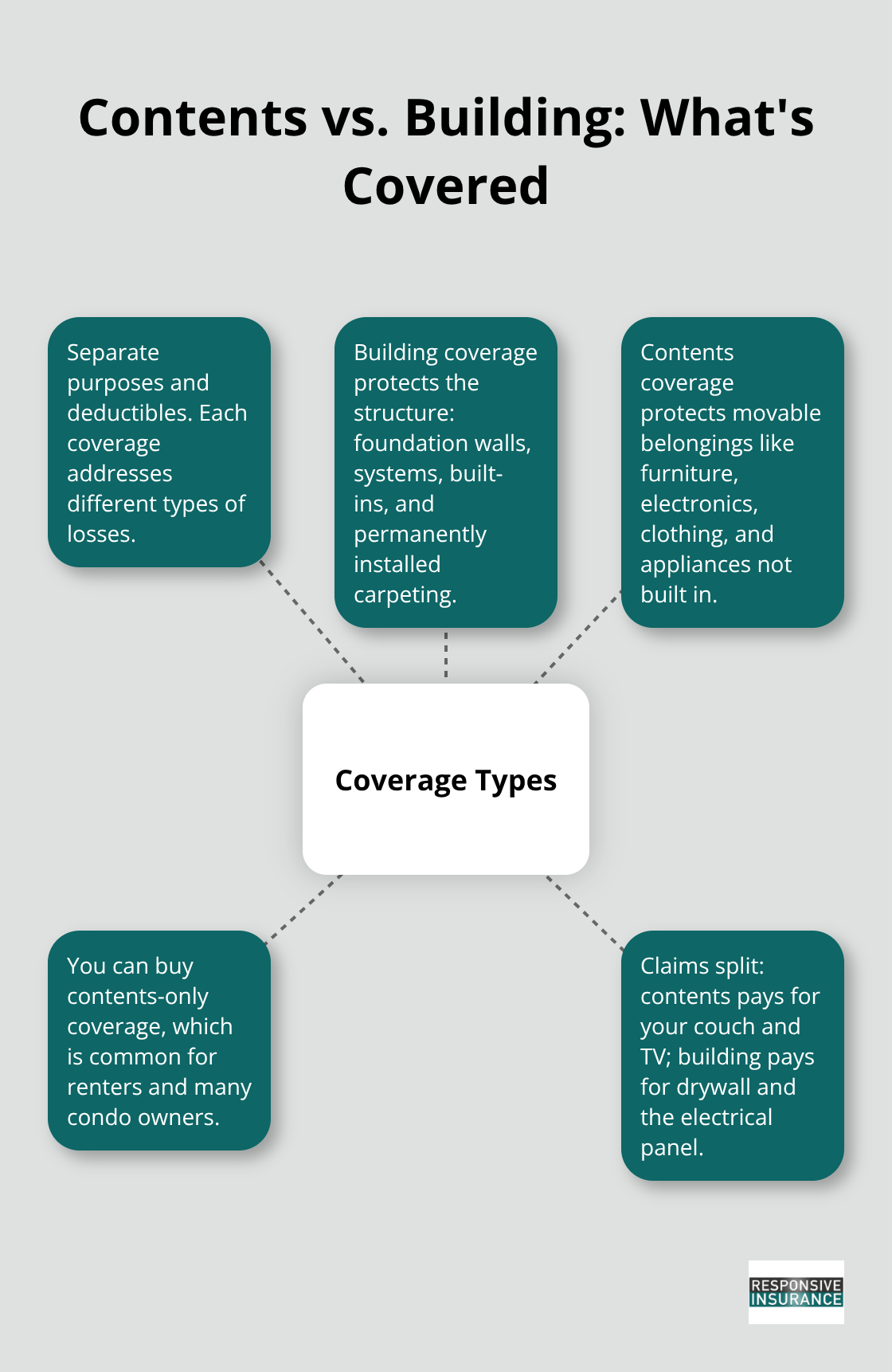

How Contents Coverage Differs from Building Protection

Contents and building coverage serve completely different purposes and have separate deductibles. Building coverage protects the structure itself, including foundation walls, electrical and plumbing systems, furnaces, water heaters, built-in appliances, and permanently installed carpeting. Contents coverage protects movable items. You can purchase contents only without building coverage, which is exactly what renters and many condo owners do.

The distinction matters for claims: if water damage ruins your couch and shorts out your television, contents coverage pays. If that same flood compromises your apartment’s drywall and electrical panel, building coverage (which your landlord or condo association should carry) handles it. Understanding this separation prevents you from assuming you’re covered when you’re not.

What Happens When You Don’t Have Contents Coverage

Without contents coverage, you absorb the full cost of replacing your belongings after a flood. A single flood event can destroy thousands of dollars in personal property-furniture, clothing, electronics, and household items that you’ve accumulated over years. Federal disaster aid does not arrive automatically; it typically comes only after a presidential disaster declaration, and when it does arrive, it often takes the form of an interest-bearing loan rather than a grant. This means you’d owe money back to the government while also replacing everything you lost. Contents coverage eliminates this financial burden and provides peace of mind that your belongings have protection. The next section covers coverage limits in detail and explains how much protection you actually need for your situation.

Coverage Limits and What They Mean

Calculate Your Actual Coverage Needs

Contents coverage limits under the National Flood Insurance Program max out at $100,000 for renters and condo owners according to FEMA guidelines. That ceiling sounds substantial until you inventory your apartment or condo unit. A living room sofa costs $1,500 to $3,000 new. A bedroom set runs $2,000 to $5,000. Electronics like televisions, computers, and kitchen appliances add another $3,000 to $8,000 depending on what you own. Clothing, shoes, and accessories for a household of two people total $5,000 to $10,000 easily. Most renters and ground-floor condo owners in Naples stay comfortably within the $100,000 limit, but you need to verify this applies to your situation.

The way coverage limits work is straightforward: NFIP sets the maximum, and your actual limit depends on what you choose to purchase and what your property warrants. Your flood zone and the replacement cost of your belongings determine your specific quote, not some arbitrary formula. In Southwest Florida, typical contents-only policies run between $450 and $1,500 annually, and that premium reflects both your risk zone and your chosen coverage limit. Higher limits cost more, but they provide fuller protection.

Avoid the Guessing Game

The critical mistake renters make is guessing their coverage needs instead of calculating them. Walk through your apartment or condo and estimate replacement costs for furniture, appliances, electronics, and clothing. If that total approaches $80,000 or more, you’re near the $100,000 maximum and should purchase the full limit available. This exercise takes an afternoon and prevents serious underinsurance later.

Understand Sub-Limits on High-Value Items

Certain items within your contents coverage carry sub-limits that cap protection below your overall policy limit. Original artwork and furs max out at $2,500 each under NFIP contents policies, meaning a painting worth $8,000 or a fur coat worth $6,000 receives only partial reimbursement. Jewelry, watches, and similar valuables also face caps that may fall short of actual replacement cost.

If you own high-value items in these categories, standard contents coverage leaves you underprotected. Private flood insurance carriers in Naples sometimes offer more generous sub-limits on valuables and higher overall limits than NFIP, which matters if your belongings include collectibles, fine art, or expensive jewelry. Before purchasing contents coverage, identify whether you own items that trigger sub-limits. If you do, calculate whether the $2,500 cap covers your loss or whether you need supplemental protection.

Most renters and condo owners with standard household possessions never hit these sub-limits, but the ones who do often discover the gap too late during a claim. Ask your agent directly about sub-limits when quoting coverage, and request clarification on exactly which items fall under reduced limits. That conversation takes five minutes and prevents thousands of dollars in unpleasant surprises after a flood damages your belongings. Once you understand your coverage limits and sub-limits, the next step involves knowing exactly what happens when water damage strikes and you need to file a claim.

Filing a Flood Claim for Water Damage

Document Damage Immediately After Floodwaters Recede

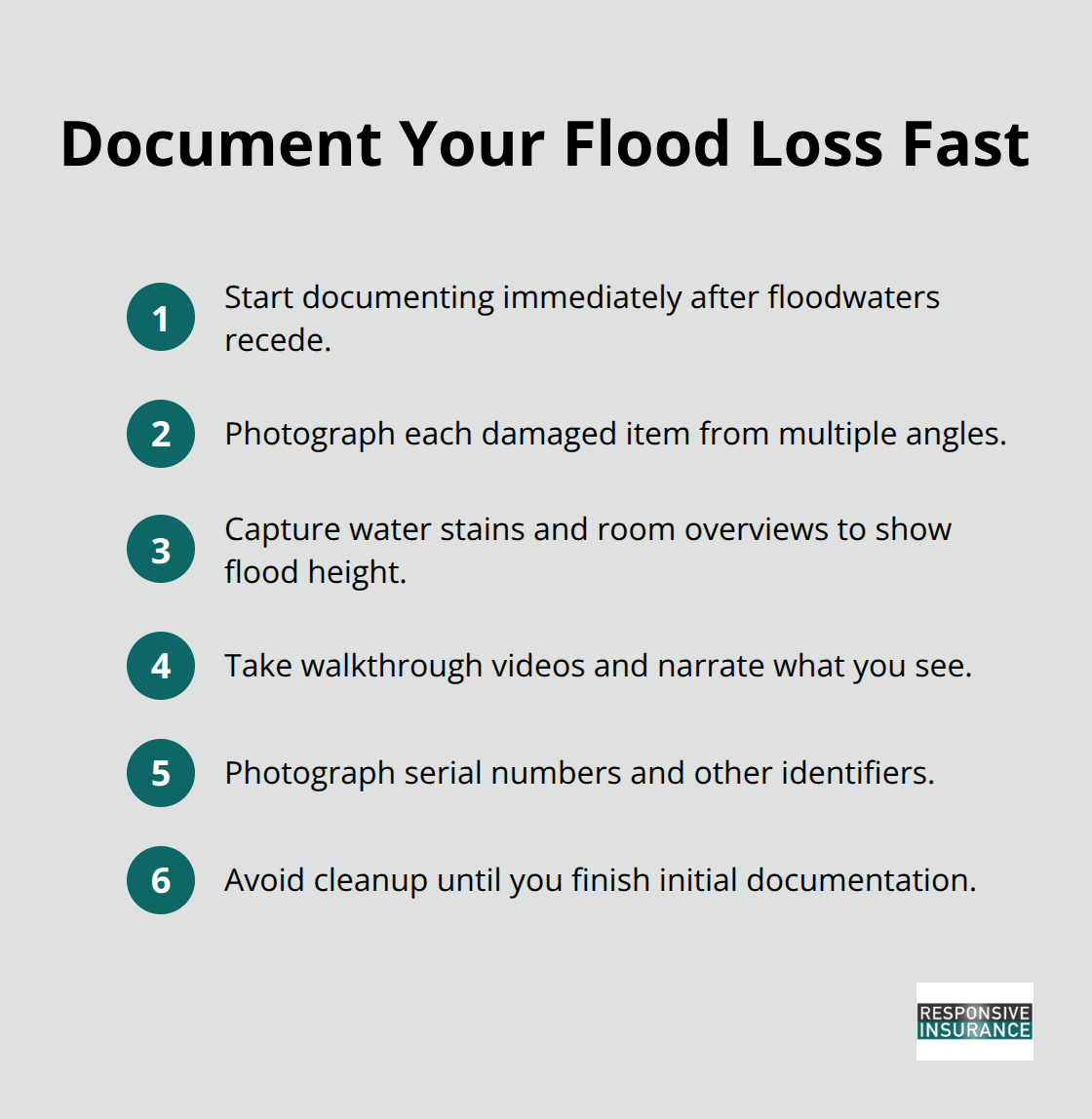

Filing a flood claim without proper documentation is like showing up to court without evidence. FEMA and the National Flood Insurance Program require specific proof before they’ll cut a check, and the difference between a paid claim and a denied one often comes down to what you photographed and what records you kept. Start documenting damage immediately after floodwaters recede, before you touch anything or begin cleanup.

Photograph every damaged item from multiple angles, capturing both the item itself and water stains on walls or furniture that show flood height. Take videos walking through your apartment or condo unit, narrating what you see and pointing out damage. For electronics, furniture, and appliances, photograph serial numbers and any identifying information visible on the items.

Collect Receipts and Create a Detailed Inventory

Collect receipts, credit card statements, or bank records showing when you purchased major items; if you lack original receipts, bank statements showing the purchase often satisfy NFIP requirements. Create a detailed written inventory listing every damaged item, its approximate purchase date, original cost, and current condition. Include measurements for furniture and dimensions for rooms to help substantiate replacement costs. High-value items like artwork, jewelry, or collectibles require extra attention; photograph these items before damage occurs if possible, and keep appraisals or valuations on file. FEMA requires prompt, written notice of flood-related damage submitted to your insurance agent or directly to your insurer. Vague claims without supporting photos or receipts get denied regularly, so treat documentation as your primary responsibility during the immediate aftermath.

Understand the Claims Timeline and Adjuster Process

The claims timeline under NFIP typically runs 30 to 60 days from submission to payment, though complex claims involving multiple damaged items or disputes over replacement costs can stretch longer. After you file, an adjuster contacts you within a few days to schedule an inspection; cooperate fully with that inspection and provide access to damaged items. Most adjusters complete inspections within two weeks, then send their assessment to NFIP for approval.

Know Why NFIP Denies Claims

Denials happen when documentation fails to support your claim, when you misrepresent the cause of damage, or when items fall outside coverage scope. Water damage from a backed-up sewer during heavy rain gets covered; water damage from a sewer backup caused by clogs in your line does not. Damage to items stored in basements may face coverage questions depending on specific policy language. Temporary housing costs, business interruption, and mold remediation fall outside standard contents coverage, so claims for those expenses get rejected. The most common denial reason FEMA sees involves inadequate proof of loss, meaning the policyholder simply didn’t provide enough photos, receipts, or documentation to verify the claim amount. Over-document rather than under-document to avoid this outcome.

Appeal a Denied Claim Through FEMA’s Advocate Office

If FEMA denies your claim, you have the right to appeal; contact the FEMA Office of the Flood Insurance Advocate if you believe the denial was incorrect or if you’re having trouble navigating the appeals process. That office exists specifically to help policyholders with complex NFIP issues and disputes.

Final Thoughts

Contents only flood insurance protects what matters most when water damage strikes your Naples home. Your furniture, electronics, clothing, and household items represent years of accumulation and financial investment that you cannot replace without proper coverage. About 25 percent of flood damage claims occur in low or moderate-risk zones, meaning renters and ground-floor condo owners outside mandatory insurance areas still face real exposure to devastating losses.

A single flood event destroys thousands in personal property, yet federal disaster aid does not arrive automatically and comes as a loan you must repay. Flood insurance for contents only eliminates this financial burden by covering your belongings up to $100,000 under NFIP guidelines, with annual premiums typically ranging from $450 to $1,500 in Naples depending on your flood zone. Your landlord’s building policy covers the structure, not your stuff, and your condo association’s policy protects the building, not your unit’s contents-you must purchase coverage yourself.

Start protecting your belongings today by calculating your actual coverage needs and contacting an insurance agent for a personalized quote. Responsive Insurance, Inc. helps Naples residents understand their flood insurance options and find coverage that fits their situation. Reach out to us to discuss your contents only flood insurance needs and get protected before the next storm arrives.