![Hurricane Insurance Florida [Everything You Need to Know]](https://responsiveinsurance.com/wp-content/uploads/emplibot/Hurricane-Insurance-Florida-_Everything-You-Need-to-Know__1769898428-1030x589.jpeg)

Hurricane Insurance Florida [Everything You Need to Know]

Hurricane season in Florida isn’t a question of if a storm will hit-it’s when. Between 1851 and 2023, Florida experienced 120 hurricanes, making it the most hurricane-prone state in the nation.

At Responsive Insurance, Inc., we know that understanding hurricane insurance Florida options can feel overwhelming. This guide walks you through what coverage actually protects your home, how to compare policies, and what happens when you need to file a claim.

Why Florida’s Hurricane Risk Keeps Climbing

Florida’s Exposure and Recent Storm Impact

Florida’s position on the Atlantic and Gulf coasts makes it a hurricane magnet, but the real threat has intensified in recent decades. Approximately 500 tropical and subtropical cyclones have affected Florida since 1851, with more storms hitting Florida than any other U.S. state. Since 2000, the state has experienced a sharper uptick in major hurricanes, with storms like Hurricane Ian in 2022 causing an estimated $112.9 billion in damage across Florida alone. The National Hurricane Center tracks that the Atlantic hurricane season officially runs from June through November, with August and September representing the most active months.

What makes this timing critical is that many homeowners delay purchasing or reviewing their hurricane coverage until late summer, sometimes after insurers have already stopped writing new policies or raised rates significantly in response to seasonal risk assessments.

How Ocean Temperatures Shift Storm Behavior

Climate patterns are shifting the calculus further. Warmer ocean temperatures fuel stronger storms, and research from NOAA indicates that hurricanes intensify faster than they did decades ago, giving residents less warning time to prepare and respond. This acceleration means homeowners face compressed decision windows when it comes to securing adequate coverage before a season turns active.

Why Coastal Areas Pay More for Coverage

Coastal and high-risk areas like Naples, Miami, and Tampa face substantially higher insurance premiums than inland cities such as Gainesville or Ocala because of their direct exposure to storm surge and wind damage. Naples specifically sits in Hurricane Surge Evacuation Zones A through E, which reflect actual surge risk rather than storm category alone-your address determines which zone applies to you, and understanding your zone is essential for both evacuation planning and insurance decisions.

The Cost Reality for High-Risk Properties

The practical reality is that homeowners in these zones pay roughly two to three times more for coverage than those inland, and premiums continue climbing as rebuild costs and insurer losses mount. This trend means waiting to secure coverage or shopping for the lowest quote without verifying what’s actually protected puts your property at genuine financial risk when a storm arrives. Understanding what your policy actually covers-and what gaps exist-becomes the next critical step in protecting your home.

What Your Hurricane Insurance Actually Covers

Wind Coverage Falls Short of Real Hurricane Damage

Standard homeowners insurance in Florida covers limited wind damage, but here’s the hard truth: it does not cover the full scope of hurricane destruction. Wind coverage typically applies to structural damage from high winds, but many policies exclude or severely limit protection for wind-driven water intrusion, which is where most hurricane damage actually occurs. Water enters through wind-damaged roofs, broken windows, or compromised walls-a gray area that standard policies often deny or underpay. Hurricane Ian’s $112.9 billion in damage came largely from water intrusion and flooding, not pure wind force, which illustrates why this distinction matters enormously.

Understanding Your Deductible and Out-of-Pocket Costs

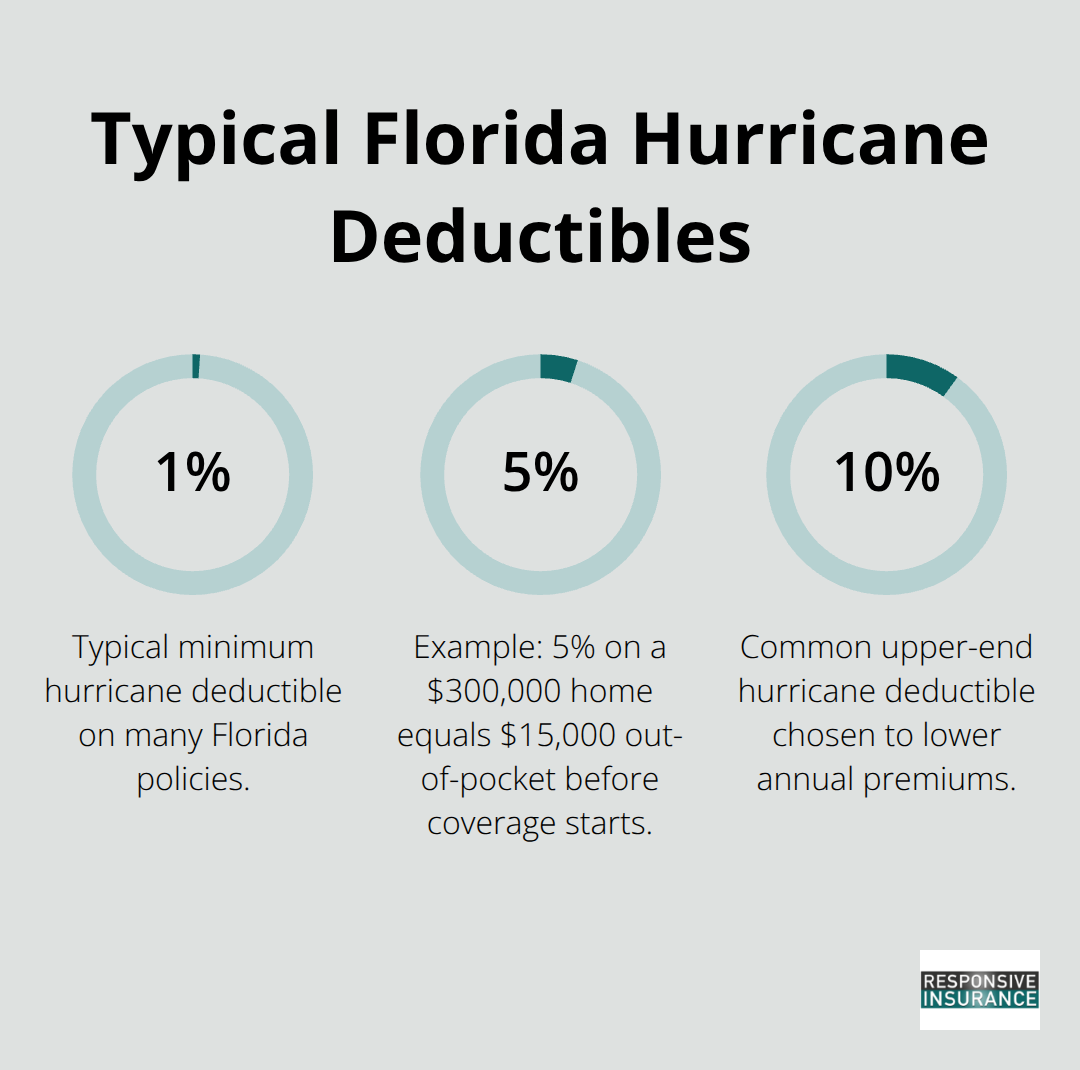

Florida homeowners insurance averages around $2,000 to $6,000 annually, but that price tag does not guarantee comprehensive hurricane protection without careful policy review. Wind or hurricane deductibles typically range from 1% to 10% of your dwelling coverage amount, meaning a homeowner with a $300,000 home and a 5% deductible faces a $15,000 out-of-pocket cost before insurance pays anything. This deductible applies per hurricane event, not annually, so a second storm in the same season means you pay it again. The financial exposure compounds quickly when you factor in what standard policies actually exclude.

Flood Insurance Requires a Completely Separate Policy

Flood insurance, which covers damage from storm surge, heavy rainfall, and standing water, is sold as a completely separate policy and is not included in standard homeowners coverage at all. National Flood Insurance Program flood policies in Florida average around $700 annually, but high-risk coastal zones pay substantially more-sometimes exceeding $2,000 per year depending on elevation and flood zone designation. Naples residents in Hurricane Surge Evacuation Zones A and B face the steepest flood insurance costs because storm surge risk directly correlates to premium calculations.

Without flood coverage, a single hurricane can leave homeowners facing tens of thousands of dollars in uninsured water damage, which is why flood insurance is genuinely non-negotiable in Florida, not optional.

Additional Coverage Options Require Active Selection

Beyond basic wind and flood coverage, additional options exist but require active selection during policy setup. Replacement cost coverage for contents allows you to rebuild your possessions at current prices rather than depreciated value-essential because post-hurricane material and labor costs spike dramatically. Additional living expenses coverage pays for hotel, meals, and temporary housing if your home becomes uninhabitable, a cost that can reach thousands of dollars monthly during extended recovery periods. Loss of rental income coverage protects investment property owners when tenants cannot occupy storm-damaged units. Many insurers now reduce or eliminate these ancillary coverages, forcing homeowners to purchase supplemental extreme weather policies separately if they want full protection.

Verifying Your Coverage Before Hurricane Season Arrives

This fragmentation of coverage means you cannot assume one policy handles everything. You must verify wind coverage exists, confirm flood insurance is active and current, check expiration dates on all policies, and understand your specific deductible amounts. Coastal properties should seriously consider extra hurricane coverage beyond the minimum because standard policies leave significant gaps.

The next step involves comparing what different carriers actually offer and understanding how to select the right limits and deductibles for your specific situation and budget.

How to Choose the Right Hurricane Insurance

Calculate Your True Replacement Cost

Choosing the right hurricane insurance hinges on one principle: your coverage must reflect what it actually costs to rebuild your home, not what you paid for it. Start with your dwelling’s replacement cost, which means the current expense to reconstruct it from the foundation up using today’s labor and material prices, not your home’s market value. After Hurricane Ian, Florida rebuild costs jumped significantly, with contractors charging premium rates for labor and materials. A $300,000 home may cost $380,000 to $420,000 to rebuild fully, which means insuring it for only $300,000 leaves you financially exposed. Request a professional replacement cost estimate from your insurance agent or a local contractor familiar with post-hurricane recovery in Southwest Florida; this figure becomes your baseline for dwelling coverage.

Match Your Deductible to Your Emergency Savings

Once you know your replacement cost, you can then layer in appropriate deductible levels. A 5% hurricane deductible on a $300,000 home means $15,000 out-of-pocket per storm event, but jumping to 10% cuts that to $30,000 while reducing your annual premium substantially. The right choice depends entirely on your emergency savings and risk tolerance. If you have $25,000 in liquid savings, a 5% deductible makes sense. If you have less, a higher deductible becomes risky because you may lack funds to cover repairs while waiting for insurance payment. Flood insurance deductibles typically range from $500 to $5,000, with higher deductibles lowering premiums; coastal properties in Naples should avoid the temptation to select $5,000 deductibles simply to save money, because a single hurricane surge event can cause $50,000 to $150,000 in flood damage, making that small premium savings irrelevant against catastrophic exposure.

Work with Local Agents Who Know Your Market

Working with a local agent who understands Naples-specific risks and has relationships with multiple insurers matters far more than shopping online for the lowest quote. National carriers continue pulling out of Florida, concentrating policies among regional and state-run insurers that may offer limited options or higher rates. An independent agent can access multiple A-rated companies simultaneously, compare actual coverage terms beyond just premium prices, and explain how different policies handle wind-driven water intrusion, which standard policies frequently dispute. When a hurricane hits and you file a claim, having an agent who knows local adjusters, understands Florida insurance law, and can advocate on your behalf becomes invaluable.

Handle Claims Promptly and Thoroughly

If your claim is denied or underpaid, specialized legal support exists; firms handle hurricane claim disputes on contingency, meaning no upfront cost, and many recover substantial additional payments for homeowners. Document all damage immediately after a storm with detailed photos and video, retain every receipt for cleanup and temporary repairs, and contact your insurer within 48 hours to initiate the claim process. Do not delay filing because Florida statutes establish strict timelines for claim submission. Provide your agent or adjuster with complete documentation rather than waiting for them to request it, as this speeds settlement and demonstrates you took reasonable steps to prevent further damage.

Final Thoughts

Hurricane insurance in Florida protects your home only when you act before a storm arrives. Florida experiences more hurricanes than any other state, your standard homeowners policy leaves massive gaps in coverage, and flood damage alone costs tens of thousands of dollars without separate flood insurance. A $300,000 home with a 5% hurricane deductible means you pay $15,000 out-of-pocket before insurance covers anything, assuming your policy actually includes wind protection and you purchased flood coverage separately.

Three actions separate homeowners who recover quickly from those facing financial devastation. Calculate your home’s actual replacement cost using current labor and material prices, not your purchase price or market value. Layer in appropriate wind and flood coverage with deductibles you can afford to pay if a storm hits this season, and verify your policies are active before June arrives, because waiting until August means higher rates and potentially no availability.

We at Responsive Insurance, Inc. work with multiple A-rated insurance companies to compare hurricane insurance Florida options and find coverage that fits your property and budget. As an independent agency based in Naples, we understand the specific risks facing Southwest Florida homeowners and explain what your policies actually cover before a hurricane tests them. Contact us to review your current coverage or get quotes for comprehensive hurricane protection tailored to your home and situation.