Landlord Insurance for Short Term Rentals Explained

Short-term rental owners face a critical gap in protection that standard homeowners policies simply don’t address. Your guests, your property, and your income all need specialized coverage that goes beyond what traditional insurance offers.

At Responsive Insurance, Inc., we’ve helped Naples property owners understand why landlord insurance for short-term rentals isn’t optional-it’s essential. This guide walks you through your coverage options and how to select the right policy for your business.

Why Your Homeowners Policy Won’t Protect Your Short-Term Rental

Standard Policies Exclude Business Activity

Standard homeowners insurance explicitly excludes coverage for active business use, and short-term rental activity falls squarely into that category. When you rent your property to guests for days or weeks at a time, you’ve crossed from personal residential use into commercial operation. Most insurers will either deny claims outright or cancel your policy entirely if they discover you’re running a short-term rental without proper coverage. This isn’t a gray area-it’s a hard line that insurers enforce consistently.

If a guest injures themselves on your property or causes damage, your homeowners policy will refuse to pay. Your mortgage lender likely requires you to maintain continuous insurance, so losing coverage creates a serious legal and financial problem. Naples property owners often assume their existing homeowners policy provides adequate protection, but that assumption can cost thousands of dollars in uninsured losses.

What Short-Term Rental Insurance Actually Covers

Landlord insurance designed for short-term rentals addresses the specific risks you face when strangers occupy your property. These policies include liability protection starting at $1 million for guest injuries, property damage coverage using replacement-cost valuation for your furnishings and structure, and loss of rental income protection if a covered event makes your property uninhabitable.

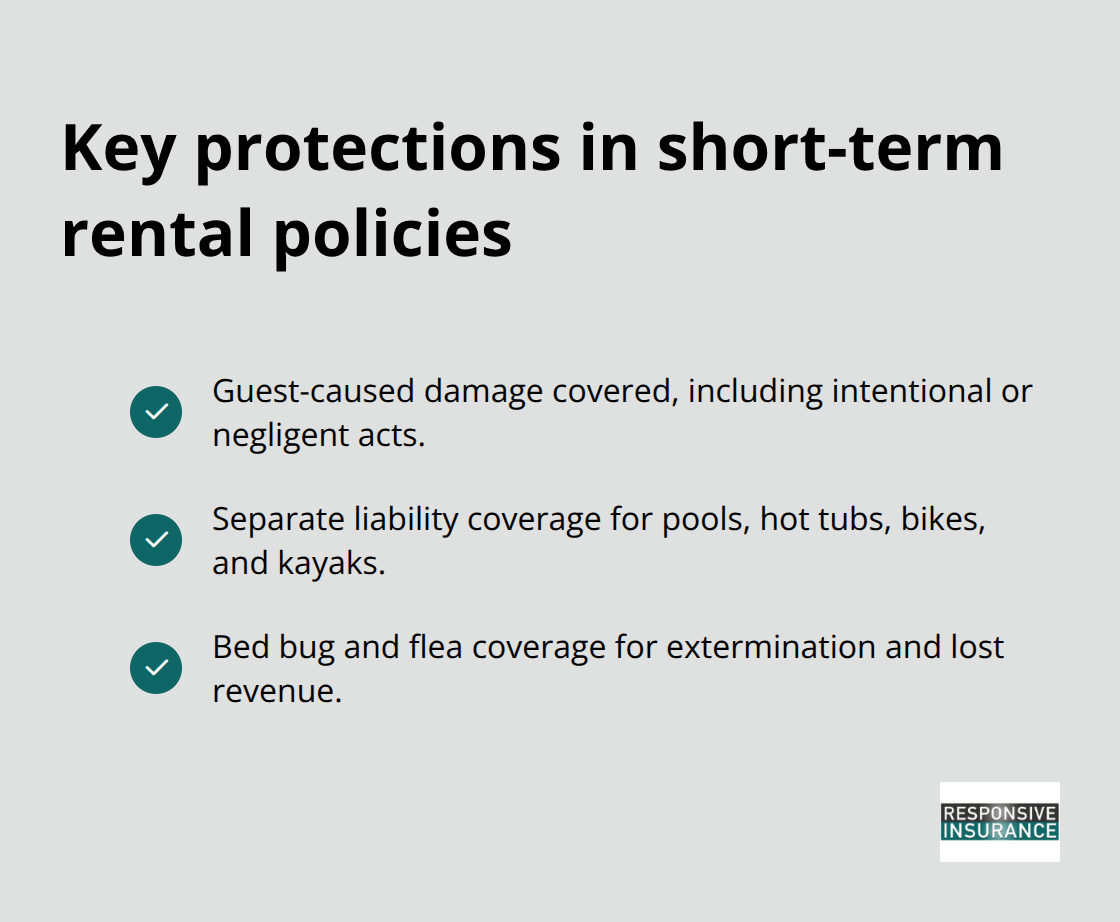

Guest-caused damage receives explicit coverage under short-term rental policies, whether that damage is intentional or negligent-a protection that standard policies refuse. Amenities like pools, hot tubs, bikes, and kayaks receive separate liability coverage, closing gaps that would leave you exposed if a guest is injured using these features. Bed bug and flea protection is increasingly common, covering both extermination costs and lost revenue from canceled bookings.

These aren’t theoretical add-ons; they’re practical protections addressing real risks that short-term rental operators encounter regularly. The annual cost typically ranges from $2,000 to $3,000 for an average-sized home in Florida, substantially higher than homeowners insurance but justified by the commercial-level exposure you’re accepting.

Long-Term Rental Policies Don’t Fit Your Business Model

Landlord policies designed for long-term rentals assume tenant occupancy lasting six months or longer, creating coverage structures misaligned with short-term rental operations. These policies often impose occupancy restrictions or require properties to remain rented continuously, which contradicts the vacant periods that characterize seasonal short-term rental businesses. They typically don’t cover loss of income during vacancy, yet your property will sit empty between bookings.

Guest damage coverage is limited or absent because long-term policies assume a single tenant household rather than dozens of different guests cycling through annually. If you rely on a long-term landlord policy for short-term rental activity, you’ll discover coverage gaps exactly when you need protection most. The distinction matters legally-using the wrong policy type gives insurers grounds to deny claims and potentially cancel coverage.

Finding Coverage Aligned With Your Rental Model

Short-term rental insurance policies account for the realities of your business model. They accommodate vacant periods without penalty, cover multiple guests throughout the year, and protect your income when circumstances force you to stop accepting bookings. The coverage structure reflects how you actually operate your property rather than forcing you into a mold designed for different rental scenarios.

When you compare policies, look for those that explicitly address short-term rental activity and include the protections we’ve outlined. The right policy transforms your liability exposure from a financial threat into a manageable business cost. Your next step involves understanding which specific coverage options matter most for your property and rental situation.

What Your Short-Term Rental Insurance Actually Protects

Liability Coverage: Your First Line of Defense

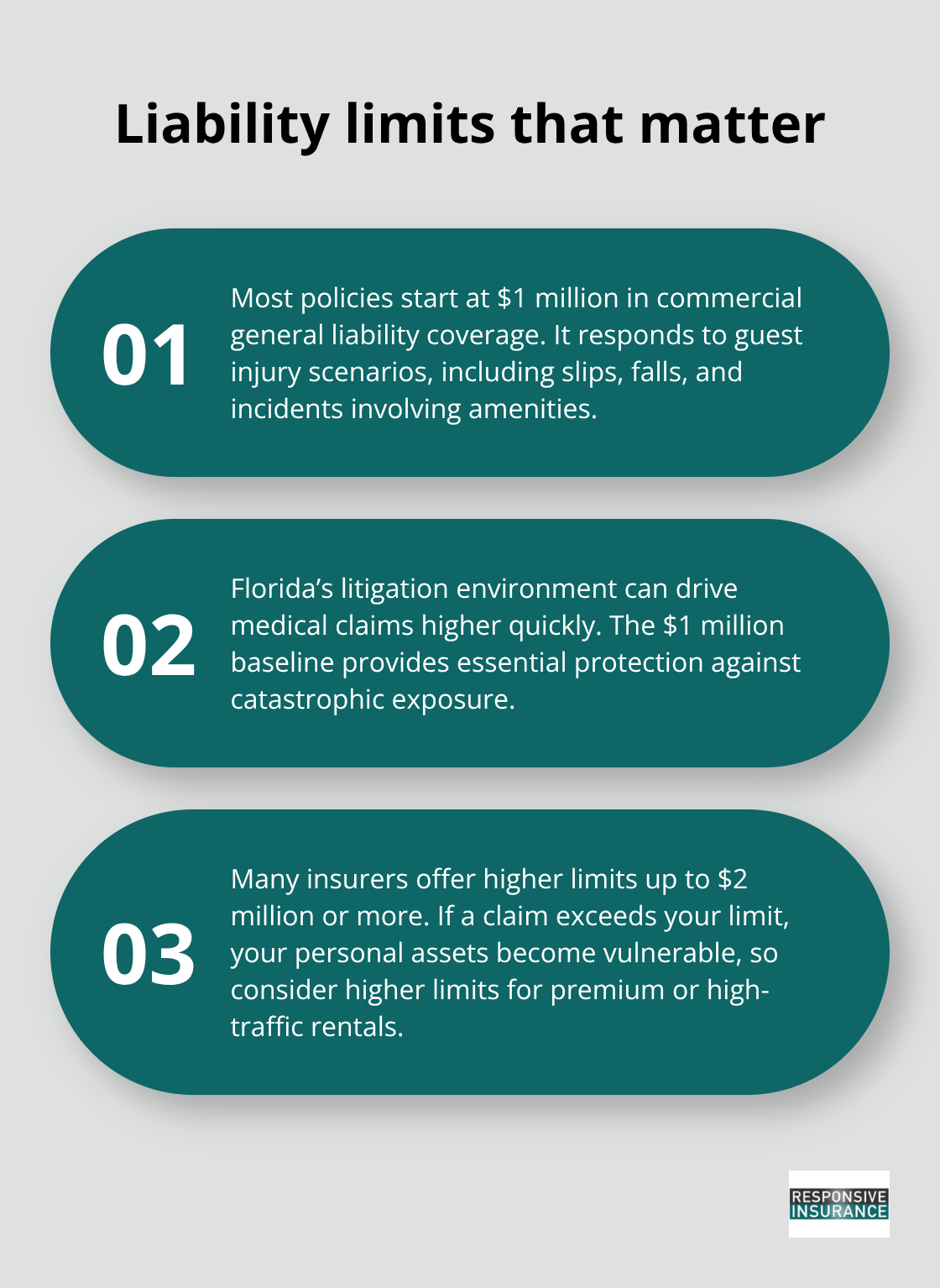

Liability protection forms the foundation of any short-term rental policy, and the numbers matter significantly. Most policies start at $1 million in commercial general liability coverage, which protects you when a guest suffers an injury on your property or causes damage to neighboring properties. A guest slips on your pool deck, falls down stairs, or injures themselves on amenities like hot tubs and kayaks-this coverage responds to those claims. Florida’s litigation environment means medical claims escalate quickly, so the $1 million baseline provides essential protection against catastrophic exposure.

Some insurers offer higher limits up to $2 million or more, and Naples property owners with premium properties or high-traffic rentals should seriously consider upgrading beyond the standard $1 million threshold. If a guest’s injury claim exceeds your liability limit, your personal assets become vulnerable, making adequate limits a non-negotiable business decision rather than an optional upgrade.

Amenities Liability and Property Coverage

Amenities liability deserves specific attention because it covers liability from guest use of pools, bikes, golf carts, and water equipment-risks that standard homeowners policies explicitly exclude. This protection addresses a genuine exposure gap that many property owners overlook until an incident occurs.

Property damage coverage under short-term rental policies uses replacement-cost valuation, meaning your furnishings, appliances, and structural improvements are covered at what it costs to replace them today, not their depreciated value. This matters enormously when guests damage high-end furnishings or appliances that depreciate slowly. Guest-caused damage receives explicit coverage under short-term rental policies whether intentional or negligent, addressing the reality that guests sometimes damage property significantly.

Income Protection and Additional Coverages

Loss of rental income protection reimburses your lost bookings when a covered loss like fire, wind, or water damage makes your property temporarily uninhabitable. Florida’s hurricane season creates genuine exposure here-a covered loss could eliminate weeks or months of rental income while repairs proceed. This coverage keeps your business financially stable during recovery periods.

Theft and vandalism coverage protects against guest theft of your belongings and property damage from intentional destruction. Bed bug and flea protection, increasingly standard in quality policies, covers extermination costs plus lost revenue from canceled bookings-a practical protection addressing a genuine problem in the hospitality industry. When you evaluate policies, verify which perils are covered and what the per-claim limits are, because some insurers impose sub-limits on specific coverages like guest theft or amenities damage that could leave you underprotected on high-value items.

Understanding these coverage components positions you to make informed decisions about which policy features align with your property’s specific risks and your rental operation’s financial needs.

Selecting the Right Policy for Your Property

Document Your Rental Operation

Start by writing down exactly how your property operates. Record your average occupancy rate, typical guest turnover, seasonal patterns, and which amenities you offer. A property rented 200 days annually with a pool and hot tub faces different exposures than a seasonal rental without amenities. Your rental model directly determines which coverages matter most and what limits you actually need. Properties in high-traffic areas near downtown Naples or on popular booking platforms attract more guests and higher liability exposure than quieter locations. If you manage multiple properties, each one’s risk profile differs based on location, construction type, and how guests use the space. This information becomes your baseline for comparing policies accurately rather than shopping based on price alone.

Request Detailed Quotes and Compare Coverage

Request detailed quotes from at least three insurers and require them to specify coverage limits, deductibles, and exclusions in writing. Don’t accept vague summaries-demand clarity on whether guest-caused damage is covered, what the liability limit is for amenities like your pool, and whether loss of income coverage includes vacant periods. Proper Insurance offers coverage for short-term rentals, including property, revenue and liability protection with unmatched coverage for guests. Farmers Insurance offers nationwide availability with claim forgiveness after five years of claims-free history, though you’ll want to confirm their specific limits match your property’s value. CBIZ specializes in rental properties with customizable replacement-cost coverage, while Allstate’s Host Advantage targets owners renting one or two rooms with locally based agents who understand Florida’s specific risks. When comparing quotes, note that annual costs typically range from $2,000 to $3,000 for average-sized homes, but premium properties in high-value areas or those with extensive amenities will cost significantly more. The cheapest quote rarely represents the best value-a $1,500 policy with $500,000 liability limits and guest-damage exclusions creates far more risk than a $2,800 policy with $1 million liability and comprehensive guest-damage coverage.

Evaluate Deductibles and Out-of-Pocket Costs

Your deductible directly impacts both your premium and your financial exposure when claims occur. A $1,000 deductible costs less monthly but requires you to absorb that amount from each claim. If a guest causes $2,500 in furniture damage, you pay $1,000 and insurance covers $1,500. If you experience multiple claims annually, that $1,000 deductible multiplies your out-of-pocket costs quickly. Higher deductibles like $2,500 or $5,000 reduce your premium but only work if you have sufficient cash reserves to cover them when incidents happen. Florida’s claim frequency for water damage, weather events, and guest-related incidents means you should realistically expect at least one claim every few years. Calculate whether saving $200 annually on premiums makes sense if you’ll pay $2,000 from pocket when that water damage claim arrives.

Identify Coverage Gaps Before You Commit

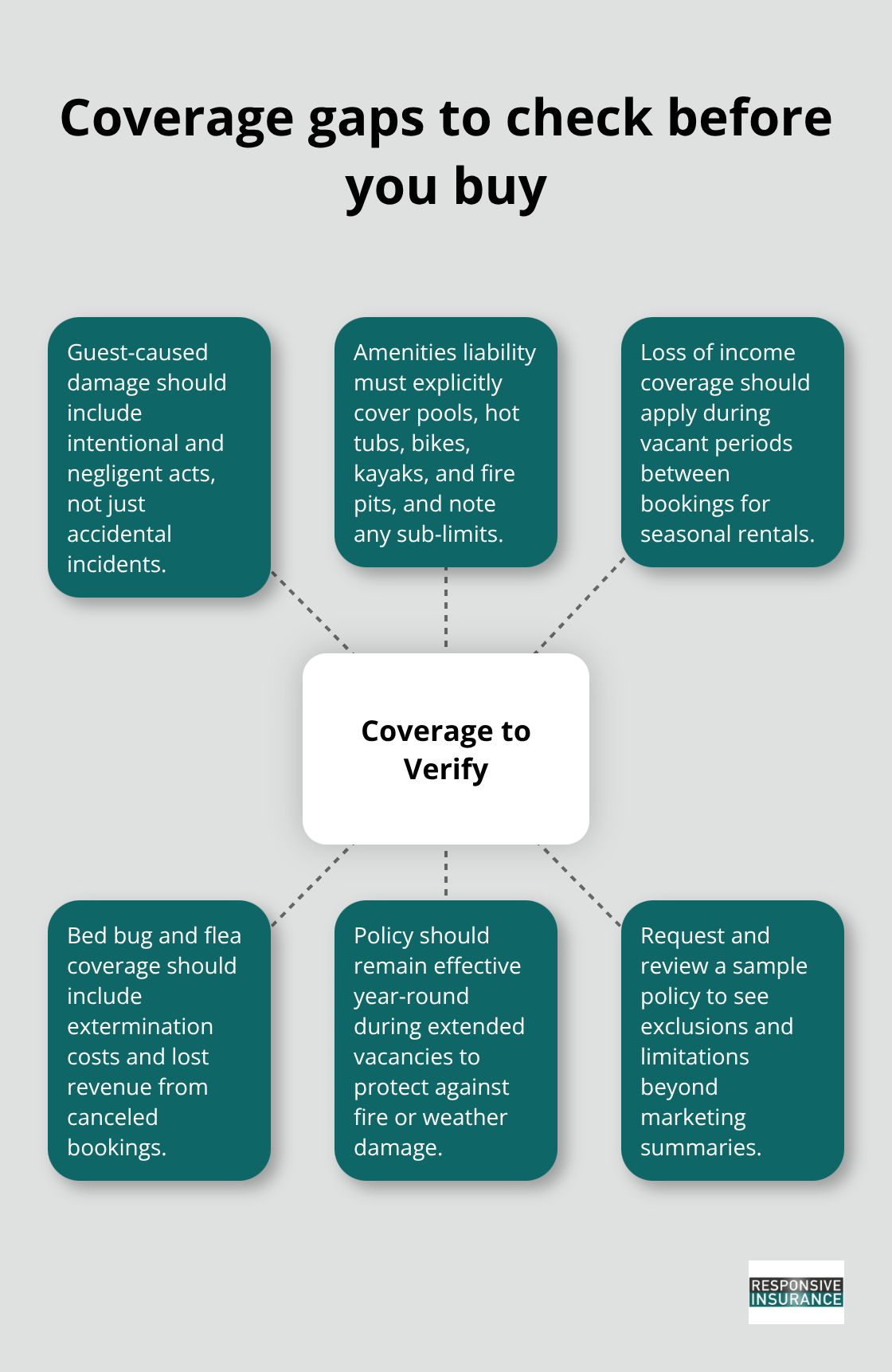

Read the policy’s specific coverage sections rather than relying on marketing materials. Confirm that guest-caused damage covers both intentional and negligent damage, not just accidental incidents. Verify whether your amenities-pools, hot tubs, bikes, kayaks, fire pits-receive explicit liability coverage or carry sub-limits that might leave you underprotected.

Check whether loss of income coverage applies during vacant periods when no guests occupy the property, since seasonal rentals naturally have gaps between bookings. Ask whether bed bug and flea coverage includes both extermination costs and lost revenue from canceled bookings, or if it only covers one component. Confirm that the policy remains effective year-round even during extended vacancies, protecting against fires or weather damage when the property sits empty. Request a sample policy document before committing, not just a quote summary, because the actual policy language reveals exclusions and limitations that marketing materials omit. An independent agency in Naples works with multiple A-rated carriers to compare these specifics across policies, helping property owners identify which coverage actually matches their operation rather than which policy offers the lowest initial quote.

Final Thoughts

Short-term rental insurance forms the operational foundation that separates successful rental businesses from owners facing financial devastation after a single incident. Your property, your guests, and your income all depend on having landlord insurance for short-term rentals in place before you accept your first booking. The coverage gaps in standard homeowners policies aren’t minor oversights-they’re complete exclusions that leave you personally liable for guest injuries, property damage, and lost income.

Request detailed quotes from multiple insurers and demand specifics about liability limits, guest-damage coverage, amenities protection, and income coverage during vacant periods. Read the actual policy documents and identify coverage gaps before you commit, because the difference between a comprehensive policy and one with significant exclusions becomes painfully obvious when you file a claim. Don’t settle for vague marketing language or the lowest price-focus instead on which policy actually protects your financial interests.

Responsive Insurance, Inc. works with multiple A-rated insurance companies to compare coverage options and find the best fit for your specific rental operation. Our independent agency based in Naples provides professional expertise about which coverages matter for your property, what limits protect your financial interests, and how to structure your deductibles based on your cash reserves. The investment in proper landlord insurance for short-term rentals pays dividends through peace of mind and financial protection.

![Florida Car Insurance Requirements [2025 Update]](https://responsiveinsurance.com/wp-content/uploads/emplibot/Florida-Car-Insurance-Requirements-_2025-Update__1768083205-80x80.jpeg)