How to Find Cheap Car Insurance in Florida

Car insurance in Florida costs more than the national average, and Naples drivers face some of the highest premiums in the state. Finding cheap car insurance in Florida requires understanding what drives up your rates and knowing which discounts actually work.

At Responsive Insurance, Inc., we help drivers cut through the confusion and find real savings. This guide walks you through the factors affecting your premiums, proven strategies to lower them, and mistakes to avoid.

What Drives Up Your Car Insurance Costs in Florida

Florida’s insurance market punishes drivers in ways most states don’t. Your rates depend on factors you can control and several you cannot. Understanding the difference helps you focus your energy on real savings rather than chasing myths about cheap coverage.

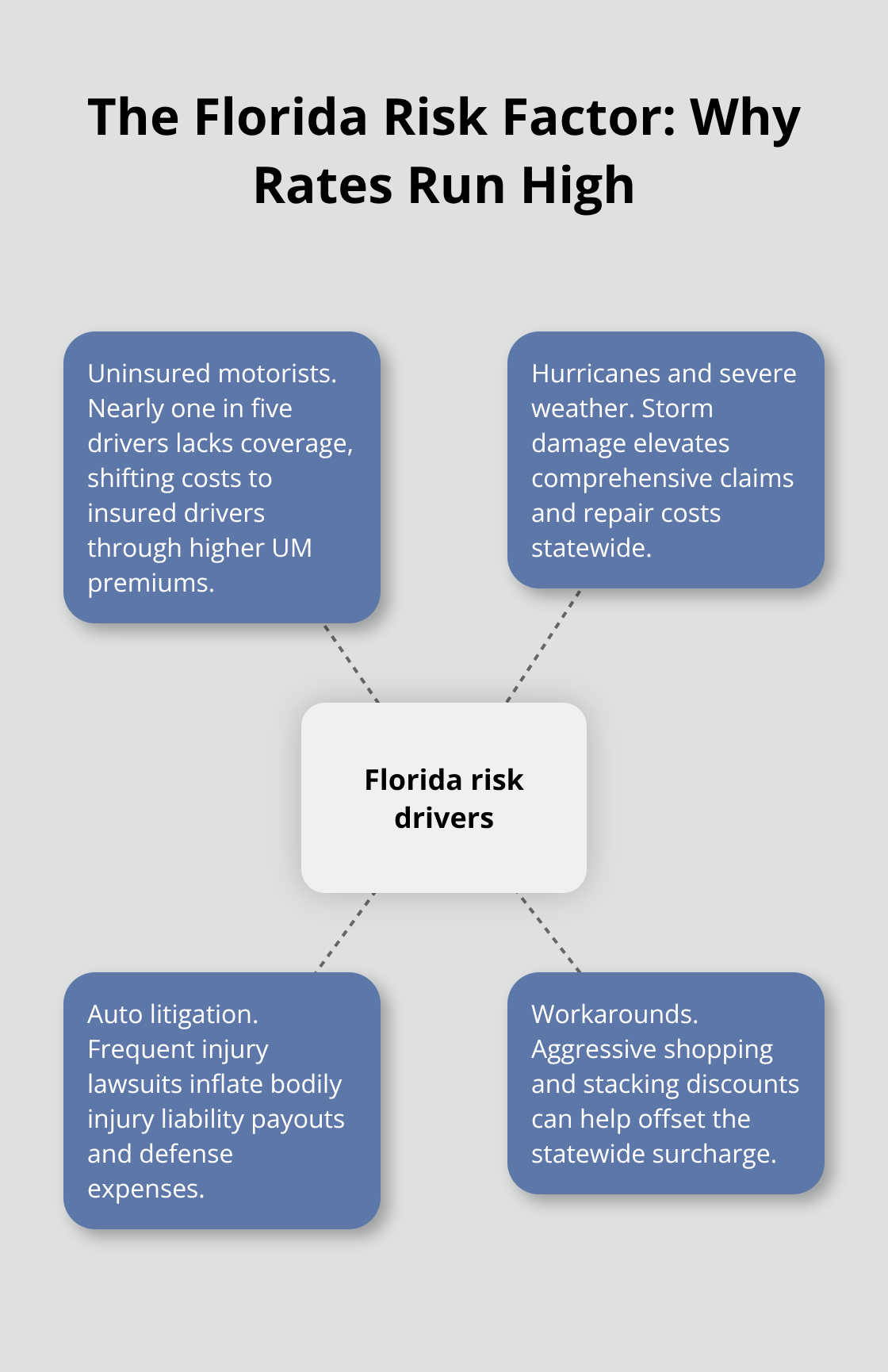

The Florida Risk Factor

Florida consistently ranks among the most expensive states for car insurance, and Naples drivers pay a premium for living here. According to Insurify data from January 2026, the average full-coverage premium in Naples runs about $165 per month, compared to the national average of roughly $137 per month. That gap exists because Florida has structural problems that push costs upward across the board.

The state has an uninsured motorist rate of just under 20 percent, meaning one in five drivers on the road carries no insurance at all. Hurricanes and severe weather drive up comprehensive claim costs. Auto litigation is rampant, with personal injury claims inflating bodily injury liability expenses. These factors affect every driver’s rates, regardless of how clean their record is.

You cannot eliminate this Florida surcharge, but you can work around it through aggressive shopping and stacking discounts that offset the baseline cost increase.

How Your Driving History Shapes Your Premium

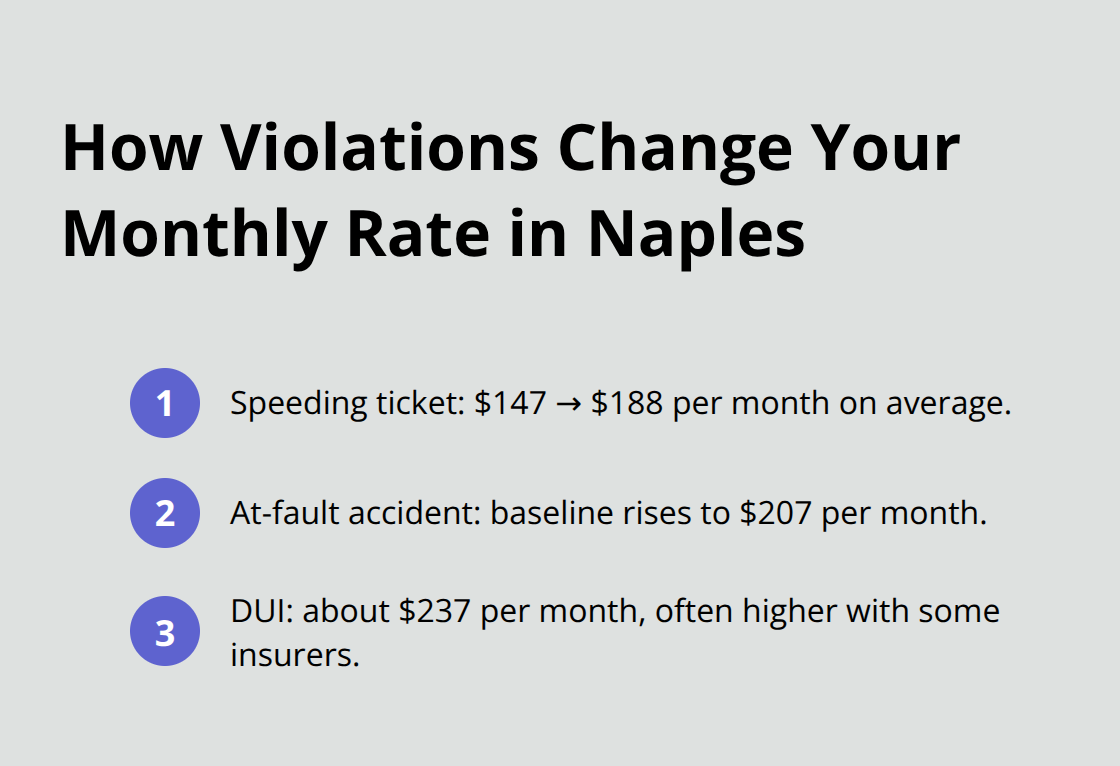

Your record shapes your premium more directly than almost anything else. A single speeding ticket in Naples raises your average rate from $147 per month to $188 per month, according to Insurify data. An at-fault accident pushes that same baseline to $207 per month. A DUI is far worse, jumping your rate to approximately $237 per month in Naples alone, with some insurers charging substantially more.

These increases stick around for three years, so a bad decision compounds across dozens of premium payments. Credit history also matters heavily in Florida. Insurify’s data shows drivers with excellent credit pay roughly $231 per month while those with poor credit face $411 per month for identical coverage in Naples. That $180 monthly gap is why improving your credit score before shopping for insurance makes financial sense.

Vehicle Choice and Insurance Costs

Your vehicle selection directly affects what you pay each month. A Tesla Model Y in Florida averages $407 per month for full coverage, while a Toyota Camry runs $324 per month according to regional data. Luxury vehicles and sports cars trigger higher rates because repair costs and theft risk are elevated. Safer, lower-value vehicles cost less to insure, which matters especially for teen drivers who already face astronomical premiums.

The type of vehicle you drive influences not just your base rate but also your eligibility for certain discounts and your long-term insurance costs. When you shop for a new car, consider the insurance implications alongside the purchase price. This decision affects your budget far beyond the initial transaction and shapes what you’ll pay for coverage over the vehicle’s lifetime. Understanding these cost drivers positions you to make smarter choices about which discounts actually work and which strategies will cut your premiums most effectively.

How to Cut Your Premiums Without Cutting Coverage

Bundle Multiple Policies for Maximum Savings

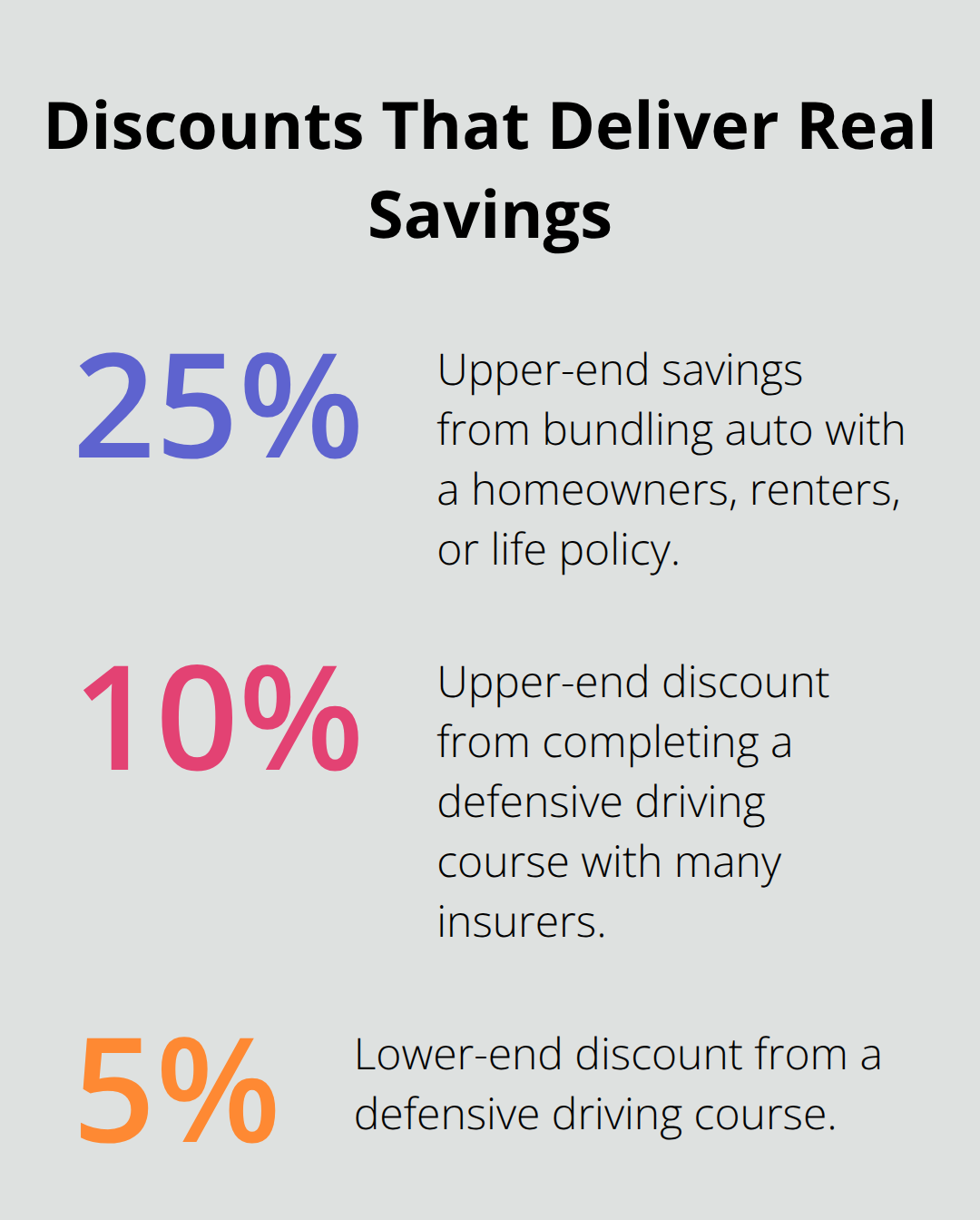

Bundling auto insurance with homeowners, renters, or life policies remains the single most effective way to lower your monthly payments in Naples. State Farm, Progressive, and Allstate all offer meaningful discounts for multi-policy customers, with bundling typically saving drivers between 10 and 25 percent on their auto premium alone. If you own a home or rent an apartment, bundling makes financial sense immediately.

According to Insurify data from January 2026, a Naples driver paying $165 per month for full-coverage auto insurance could save $16 to $41 monthly just by bundling with a homeowners policy. Over a year, that amounts to $192 to $492 in pure savings without changing your coverage limits or accepting higher deductibles. The math is straightforward: if your home insurance costs $1,200 annually, bundling might reduce that to $1,080 while simultaneously lowering your auto premium. Shop bundled rates explicitly when you request quotes, because some insurers hide these savings unless you ask. Many drivers miss this savings opportunity simply because they never request a combined quote.

Raise Your Deductible Strategically

Increasing your deductible from $500 to $1,000 cuts your monthly premium by roughly 10 to 15 percent, according to industry data. In Naples, that translates to $16 to $25 monthly savings on full-coverage policies. This strategy works best if you have emergency savings set aside for the higher out-of-pocket cost after an accident. Drivers without financial cushion should not raise deductibles beyond their comfort level.

Claim Discounts You Actually Qualify For

Low-mileage discounts apply if you drive fewer than 10,000 to 12,000 miles annually and can provide proof through your odometer or telematics app. Completing a defensive driving course through organizations like the American Safety Council or National Safety Council qualifies you for discounts ranging from 5 to 10 percent with most major insurers. These courses take four to eight hours online and cost between $25 and $50, making them cost-effective if your insurer offers the corresponding discount.

Teen drivers in Naples benefit substantially from good-student discounts, typically receiving 10 to 15 percent reductions when they maintain a 3.0 GPA or higher. Stacking multiple discounts compounds savings significantly-a Naples driver combining bundling, a higher deductible, a defensive driving discount, and a low-mileage discount could reduce their $165 monthly baseline to roughly $120 or less depending on their specific insurer and coverage selections.

These savings strategies work only if you actively pursue them. The next section covers the mistakes that undo all this progress and leave drivers paying far more than they should.

Common Mistakes That Drive Up Insurance Costs

Most Naples drivers commit the same costly error: they accept their current insurer’s renewal rate without requesting competing quotes. According to The Zebra, customers who shop quotes save an average of $440 per year, yet roughly 60 percent of drivers never compare rates after their initial purchase. This single mistake erases all the savings strategies discussed in the previous section. A driver who bundles policies, raises their deductible, and completes a defensive driving course might save $45 monthly through those actions, but if they fail to shop around, they could be overpaying by $100 or more monthly compared to competitors. The math is brutal: your diligence in claiming discounts becomes irrelevant if you remain with an overpriced insurer. Insurify data from January 2026 shows that State Farm and Mile Auto consistently offer the lowest full-coverage rates in Naples at around $107 and $148 monthly respectively, while other carriers charge $164 or higher for identical coverage. Shopping takes roughly 20 minutes across three to five major insurers, yet this single action typically yields more savings than any discount strategy combined. Your annual renewal notice signals the time to request fresh quotes immediately, not your permission to pay the same rate again.

Why Annual Reviews Prevent Rate Creep

Insurance companies raise rates annually, and most drivers simply accept these increases without question. Your rate from last year rarely stays flat this year, and your coverage from two years ago may no longer match your actual needs. Life changes require coverage adjustments: if you paid off your vehicle loan, you might eliminate collision coverage and save significantly. If you moved to a safer neighborhood or reduced your annual mileage, you qualify for discounts you couldn’t claim before. If your teen graduated high school and moved into their own apartment, removing them from your policy cuts your premium substantially. Failing to review coverage annually means you carry protection you no longer need while missing discounts you now qualify for. Teens in Naples average $285 monthly for full coverage, but moving them to their own policy after college graduation immediately eliminates that cost from your household premium. Similarly, bundling your auto policy with a newly purchased homeowners policy can cut both premiums by 10 to 25 percent, but only if you contact your insurer to restructure your coverage. Schedule a coverage review each time your policy renews, not just when something feels wrong.

The Silent Cost of Lapses

Letting your car insurance lapse, even briefly, carries penalties that extend years into your future. In Florida, driving without required coverage leads to license suspension and vehicle registration suspension for up to three years, with reinstatement costs between $150 and $500. Beyond legal consequences, lapsed coverage creates a permanent mark on your insurance history that insurers see forever. Drivers with any history of non-payment face higher rates across the industry and reduced access to standard-market carriers, forcing them into high-risk pools with premiums 30 to 50 percent above normal rates. A single 30-day lapse can cost you hundreds of dollars annually in elevated premiums for the next three to five years. If your financial situation becomes tight, contact your insurer immediately to discuss payment arrangements, reduced coverage options, or discount opportunities rather than letting your policy lapse. Many carriers offer month-to-month payment plans specifically to prevent lapses, and some provide hardship discounts during temporary financial difficulties. The cost of preventing a lapse is always lower than the cost of recovering from one.

Final Thoughts

Finding cheap car insurance in Florida requires three concrete actions: shop quotes from multiple carriers, claim every discount you qualify for, and review your coverage annually. Naples drivers who complete these steps typically save $440 or more yearly compared to those who accept renewal rates without question. The strategies outlined in this guide work only when you execute them consistently, and your shopping discipline determines your final premium far more than your driving record or vehicle type.

Working with an independent insurance agent simplifies this process significantly. Rather than requesting quotes individually from dozens of carriers, an agent accesses multiple A-rated insurers simultaneously and presents you with side-by-side comparisons tailored to your specific situation. At Responsive Insurance, Inc., our team works with multiple carriers to compare coverage options and identify the best fit for your needs, handling the quote requests and explaining coverage differences so you understand exactly what you pay for.

Request quotes this week from three to five insurers or speak with an independent agent who can access multiple carriers at once. Provide identical coverage information across all quotes so you can compare apples to apples, and ask explicitly about bundling discounts and low-mileage savings you might qualify for. Once you select a carrier, schedule a coverage review annually to ensure your protection matches your current needs and that you claim all available discounts.

![Florida Car Insurance Requirements [2025 Update]](https://responsiveinsurance.com/wp-content/uploads/emplibot/Florida-Car-Insurance-Requirements-_2025-Update__1768083205-80x80.jpeg)