How to Cancel Flood Insurance

Flood insurance can feel like an unnecessary expense once your risk situation changes. Whether you’ve moved to higher ground, paid off your mortgage, or reassessed your property’s flood risk, canceling your policy might make sense.

At Responsive Insurance, Inc., we help Naples residents understand when and how to cancel flood insurance without leaving themselves vulnerable. This guide walks you through the process step by step.

When Cancellation Actually Makes Sense

Canceling flood insurance requires more than a desire to save money. Federal law limits mid-term cancellations under the National Flood Insurance Program to specific qualifying events, such as selling your property. If your situation doesn’t match one of these, NFIP won’t process your cancellation request, and you’ll remain covered until renewal. This matters because if you later want flood coverage again, reinstatement rates can jump dramatically-you’ll lose any subsidized rates you currently enjoy and pay full risk rates instead. The financial penalty for canceling prematurely and then needing coverage again can easily exceed $1,000 over several years.

Property Remapping Changes Everything

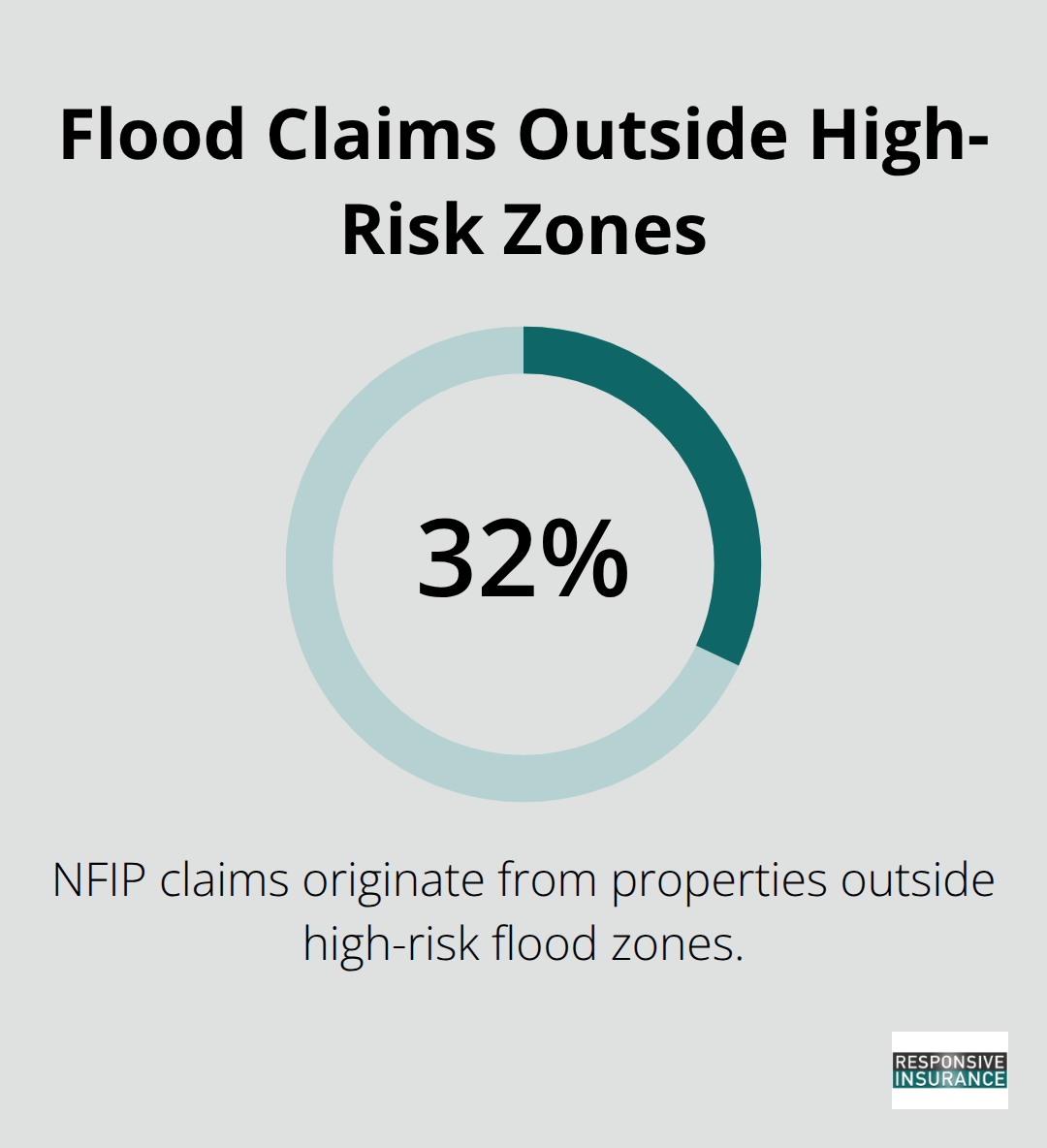

Your flood zone designation determines whether cancellation is even possible. When Collier County updated its Digital Flood Insurance Rate Maps, some Naples properties moved into lower-risk zones, while others shifted into higher-risk areas. Check your current flood zone designation using the Flood Map Service Center to confirm whether you’ve been remapped. If you’re now in Zone X-the lowest-risk category-you may have grounds to cancel, especially if your lender no longer requires coverage. However, don’t assume your lender will agree; some lenders maintain stricter requirements than federal law mandates. Contact your mortgage servicer directly before you submit any cancellation request. Properties outside mapped high-risk zones still carry real flood risk-about 32% of NFIP claims come from outside high-risk areas, according to NFIP data-so reassess your actual exposure even if legal requirements have changed.

Mortgage Payoff and Property Sales

Paying off your mortgage eliminates the lender’s requirement for flood insurance, but it doesn’t eliminate your flood risk. Many homeowners assume they can drop coverage once the mortgage disappears, then face catastrophic losses when water damage strikes. Average flood damages exceed $25,000, and that money comes directly from your pocket without insurance. If you sell your property, the transaction itself qualifies for cancellation, though your buyer will likely need their own flood policy if the property sits in a high-risk zone. Time this carefully-notify your insurance agent at least 30 days before the sale closes to avoid coverage gaps and ensure proper documentation for the lender or title company. For mortgage payoffs, the decision is purely yours, but we strongly recommend you keep coverage if your property has any flood history or sits near water features.

What Comes Next in Your Cancellation Journey

Once you’ve confirmed that your situation qualifies for cancellation, the actual process involves several specific steps that protect both you and your lender.

The Cancellation Process

Canceling your NFIP policy requires you to gather specific documents and follow an exact sequence. Your current flood insurance policy holds the information you need-pull out the declarations page and read it carefully. This page shows your policy number, coverage limits, deductible, and renewal date. The declarations page also lists any special endorsements or riders you’ve purchased, such as additional living expenses coverage. Understanding what you currently have protects you from accidentally losing coverage you may want to keep. Many Naples homeowners discover after cancellation that they’ve had optional coverages they forgot about, then regret dropping them once flood season arrives.

Confirm Your Cancellation Qualifies

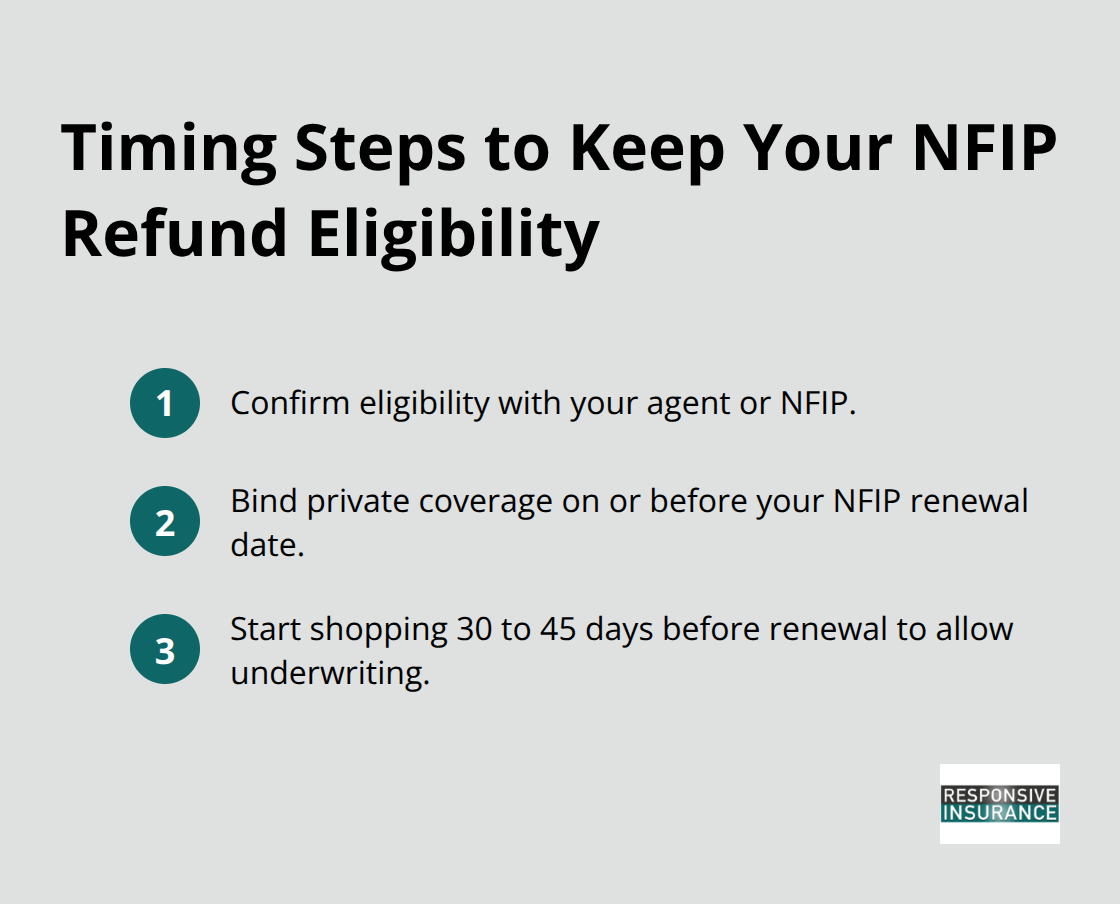

Call your insurance agent or the NFIP directly at 1-888-CALL-FLOOD to confirm your cancellation qualifies under federal rules. Don’t assume your situation meets the criteria-agents handle this regularly and can spot problems you might miss. If you’re switching to private flood insurance, time this conversation carefully. Your private policy must bind and become effective on or before your NFIP renewal date to qualify for a refund. Missing this deadline by even one day means forfeiting your refund entirely. Start shopping for private coverage 30 to 45 days before your renewal date to ensure adequate time for underwriting and binding.

Submit Your Cancellation Request in Writing

Once your agent confirms cancellation is legitimate, submit your request in writing. Email works, but request a read receipt so you have proof of delivery. Include your policy number, the effective cancellation date, and the reason for cancellation. If you’re selling the property, include the closing date and buyer’s name if available. If you’re moving to private coverage, include the effective date of your new policy. The NFIP processes written cancellations faster than phone requests and creates a paper trail for your records.

Understand Your Refund Timeline and Eligibility

After you submit your cancellation, expect your policy to terminate on the date you specified, though some delays occur during hurricane season when processing times increase. You’ll receive a cancellation confirmation letter within 7 to 10 business days, along with details about any refund. If you paid your premium in full and cancel mid-term, NFIP calculates a refund based on the unused portion of your policy, though the calculation varies depending on your cancellation reason. For property sales or remapping into lower-risk zones, refunds are straightforward. For other qualifying events, contact NFIP to confirm your refund eligibility before submitting your cancellation.

Once NFIP processes your cancellation and you receive your confirmation letter, the next critical step involves what you do with your coverage gap-whether you’re moving to private flood insurance or accepting the risk yourself.

What Happens After Cancellation

Your NFIP cancellation unfolds over days and weeks, with specific timelines you must track and refunds that depend on precise conditions. NFIP processes cancellations within 7 to 10 business days under normal circumstances, though hurricane season can stretch this to two weeks or longer. Your policy terminates on the effective date you specified in your cancellation request, not the date NFIP receives it. This distinction matters enormously if you’re switching to private flood coverage.

Timing Your Private Policy Binding

Your private policy must become effective on or before your NFIP renewal date to qualify for a refund under FEMA Reason Code 26. If your NFIP renewal falls on January 1 and your private policy binds on January 1, you receive a refund. If that private policy doesn’t bind until February 1, NFIP keeps the entire year’s premium with no refund. One-day timing differences determine thousands of dollars in your pocket or theirs. Start coordinating with your private insurer at least 45 days before your NFIP renewal to ensure the binding date aligns perfectly.

Understanding Your Refund Calculation

Your refund calculation depends entirely on your cancellation reason. NFIP refunds the unused portion of your premium only if you qualify under specific circumstances: selling your property, being remapped into a lower-risk zone, paying off a federally backed mortgage, or holding duplicate coverage. Mid-term cancellations for cost savings alone produce zero refund. You’ll receive a cancellation confirmation letter that details your refund amount, the calculation method, and the processing timeline.

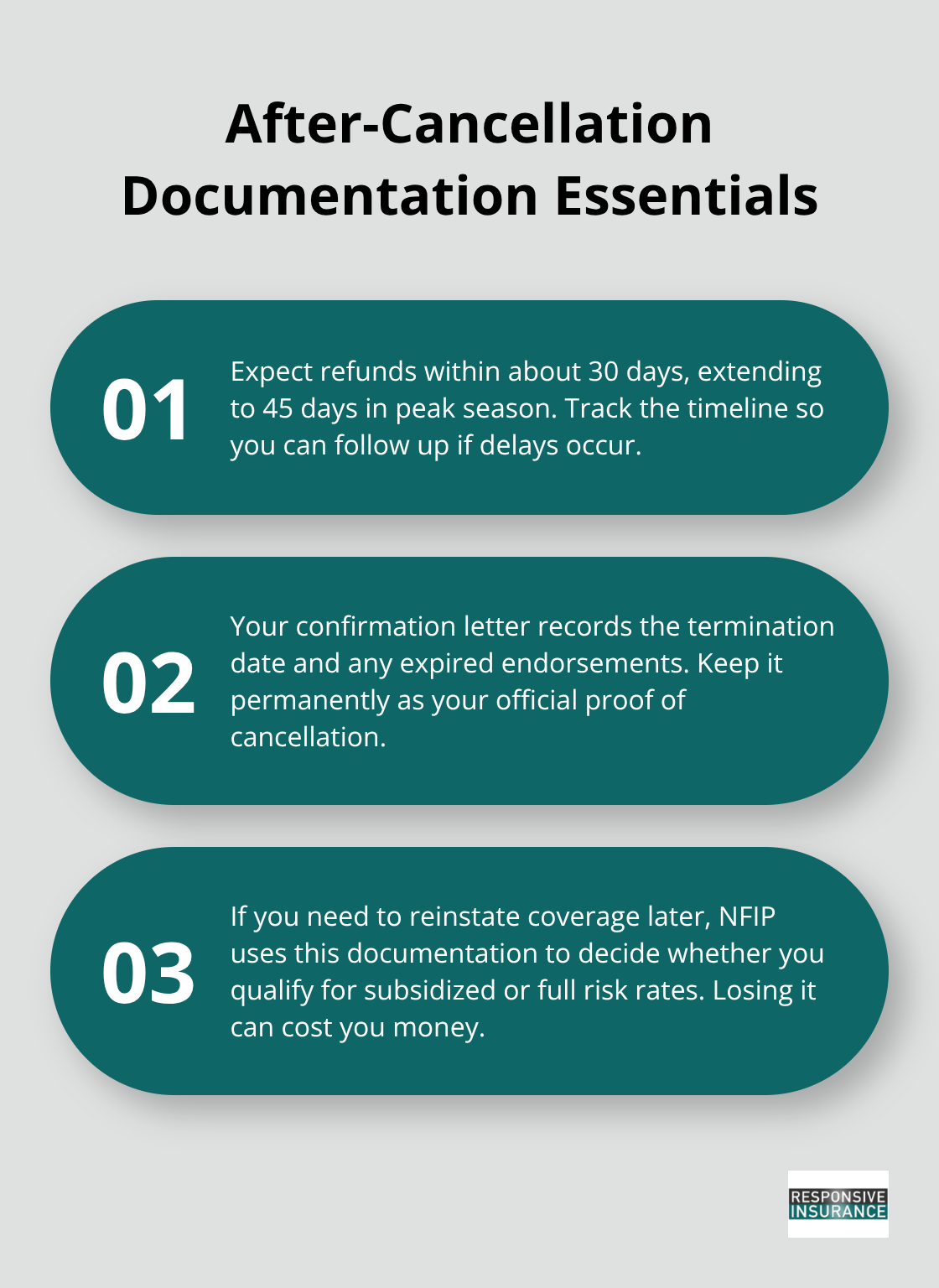

Processing Timelines and Documentation

Refunds typically arrive within 30 days of cancellation, though some delays extend to 45 days during peak season. The confirmation letter also documents your policy termination date and any special endorsements that expired. Keep this letter permanently. If you ever need to reinstate flood coverage, NFIP uses this documentation to determine whether you qualify for subsidized rates or must pay full risk rates. Losing this letter complicates reinstatement and costs you money.

Store it with your other important documents, not in a file you’ll discard next year.

Final Thoughts

Canceling flood insurance requires careful planning and precise timing-the process involves confirming your situation qualifies under federal rules, coordinating with your lender, and understanding the financial consequences of your decision. About 32% of NFIP claims come from properties outside high-risk flood zones, which means your flood risk exists regardless of your zone designation. Many Naples homeowners regret canceling too quickly, only to face devastating losses when water damage strikes unexpectedly.

Before you finalize how to cancel flood insurance, honestly assess whether your property truly sits in a low-risk area and whether you can absorb potential flood losses out of pocket. Average flood damages exceed $25,000-that’s money you’ll pay directly if you’re uninsured. If you’ve been remapped into Zone X, paid off your mortgage, or are switching to private flood coverage, binding your new policy on or before your NFIP renewal date is the only way to secure a refund, so start shopping 30 to 45 days before renewal.

We at Responsive Insurance, Inc. help Naples residents navigate these decisions with clarity and confidence. Contact us to discuss your specific situation and explore flood insurance options that fit your needs and budget-our team provides the guidance you need to make informed decisions for your property and financial security.