What Options Are There When Choosing Flood Insurance?

Living in Naples, FL means understanding your flood risk isn’t optional-it’s essential. Standard homeowners insurance won’t protect you when water damage strikes, leaving a significant gap in your coverage.

At Responsive Insurance, Inc., we know that when choosing flood insurance, you have real options beyond what most people realize. This guide walks you through the National Flood Insurance Program, private alternatives, and additional protections that fit your specific situation.

Why Flood Risk in Naples Demands Immediate Attention

Southwest Florida’s Multi-Directional Flood Threat

Southwest Florida’s geography creates flooding from multiple directions simultaneously. Heavy rainfall overwhelms drainage systems, storm surge pushes inland from the Gulf of Mexico, and rising groundwater tables threaten even properties far from visible water bodies. FEMA’s flood maps categorize this area into distinct zones based on flood frequency and severity, with the highest-risk zones designated as Special Flood Hazard Areas where the annual chance of flooding reaches 1% or higher. Your property’s flood zone directly determines whether your mortgage lender requires flood insurance and influences your premium costs significantly.

The Critical Gap in Standard Homeowners Coverage

Standard homeowners insurance explicitly excludes flood damage, a gap that catches most homeowners off guard. Water damage from burst pipes or roof leaks receives coverage, but water flowing across your land or rising through your foundation does not. This distinction matters enormously: water represents the leading cause of home losses in the United States, yet the vast majority of homeowners policies leave this exposure completely unprotected. In Naples, where tropical storms and heavy rainfall occur regularly, this exclusion represents a dangerous blind spot in your protection.

Determining Your Property’s Actual Risk Level

Your specific flood risk extends far beyond general assumptions about your neighborhood. Start with FEMA’s Flood Map Service Center, which provides free, detailed information about your exact risk level. Properties in high-risk zones face mandatory flood insurance requirements if you carry a federally backed mortgage, but moderate and low-risk properties face different considerations entirely.

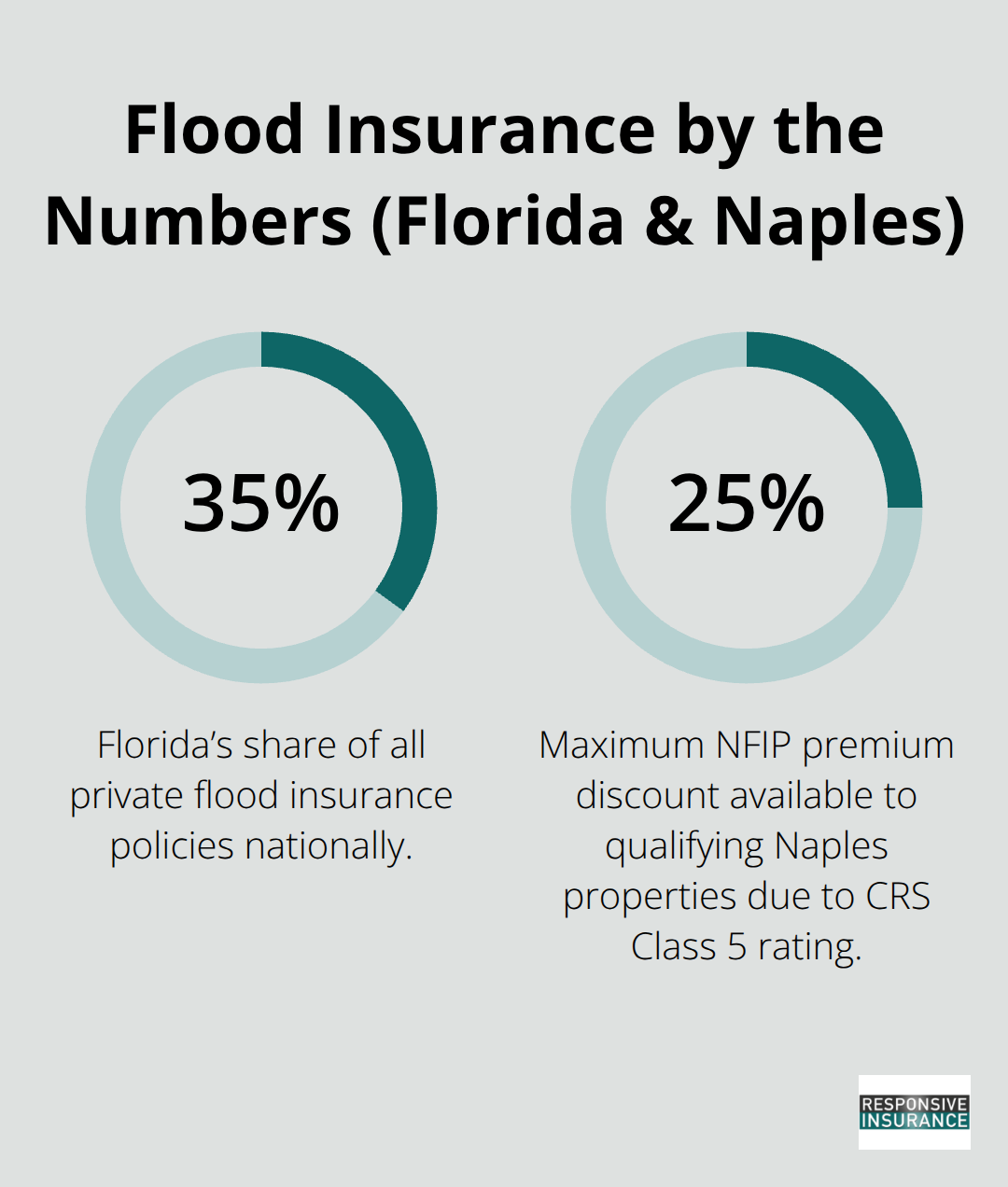

Even if flood insurance isn’t mandatory for your situation, the City of Naples participates in the National Flood Insurance Program and offers a Class 5 Community Rating System designation, which provides up to a 25% discount on standard NFIP policies for qualifying properties. Your elevation relative to the base flood elevation, the age of your home, and documented mitigation improvements like engineered vents or flood-resistant materials all affect your actual risk profile and available premium discounts. Properties built after the year 2000 with proper elevation certificates often qualify for substantial savings that properties built earlier cannot access.

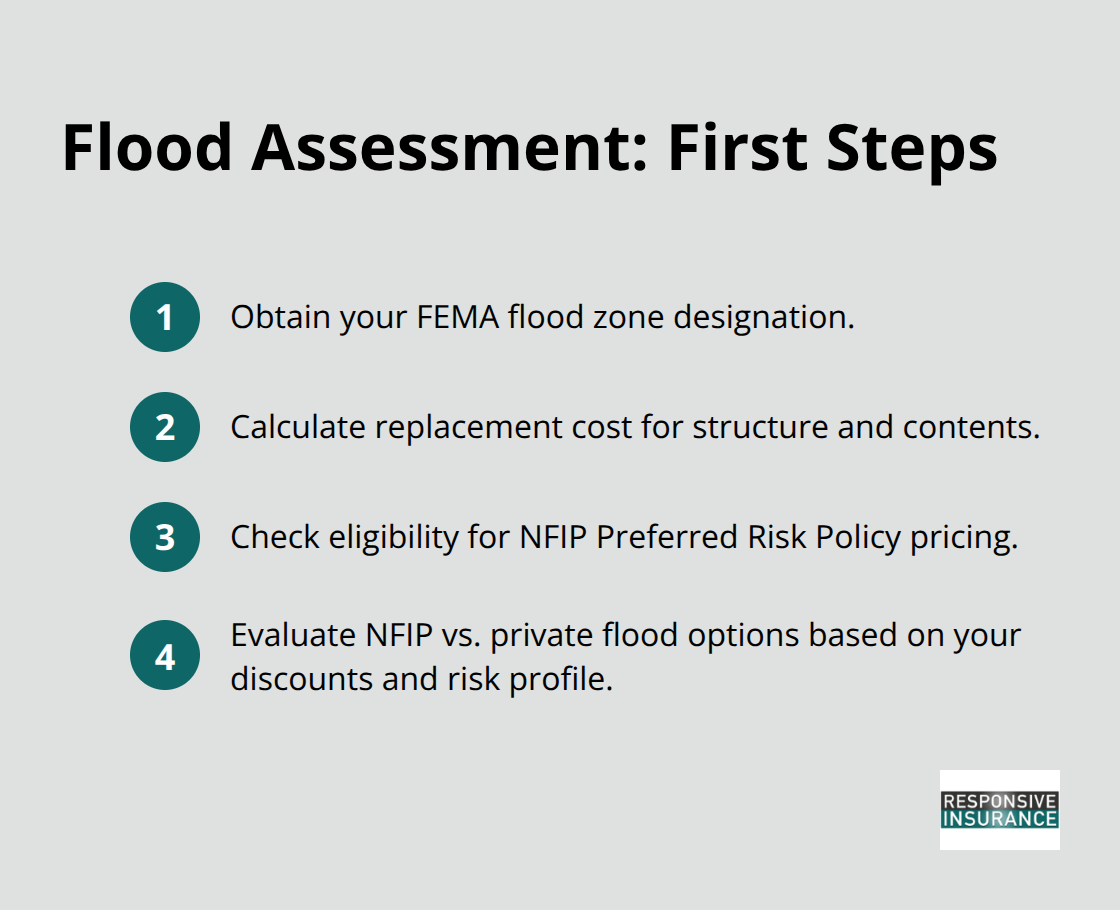

Taking Action on Your Flood Assessment

The practical steps here are straightforward: obtain your flood zone designation, calculate your replacement cost for both structure and contents, and understand whether your property qualifies for Preferred Risk Policy pricing through NFIP, which offers substantially lower rates for lower-risk properties in the same zone. Once you understand your risk profile and available discounts, you’ll be positioned to evaluate the two primary flood insurance pathways available to Naples homeowners.

Your Flood Insurance Choices

NFIP Coverage Limits and How They Fall Short

The National Flood Insurance Program remains the foundation of flood protection for most Naples homeowners, but private flood insurance has grown substantially in Florida over the past decade. Florida now holds approximately 35% of all private flood insurance policies nationally, making it the largest private flood market in the United States with over 600,000 privately insured properties. This expansion happened for a reason: NFIP has structural limitations that don’t work for every property, particularly those with higher values or specific protection needs.

The NFIP caps dwelling coverage at $250,000 for single-family homes and contents coverage at $100,000, using actual cash value for contents rather than replacement cost. These limits work fine for modest properties but fall dramatically short for homes worth $500,000 or more.

NFIP policies typically cost around $700 annually in high-risk areas, though your actual premium depends heavily on your flood zone and elevation relative to the base flood elevation.

Private Flood Insurance Offers Higher Limits and Better Contents Protection

Private flood carriers in Florida offer dwelling limits up to $10 million, with replacement-cost contents coverage that actually pays what you need to replace items, not their depreciated value. In moderate-risk Zone X areas, private flood premiums run 20 to 35% cheaper than NFIP, typically $350 to $600 annually versus NFIP’s $500 to $800. However, in high-risk zones like AE or VE, pricing becomes less predictable and can sometimes exceed NFIP costs depending on your specific property characteristics and elevation.

Private carriers also include loss-of-use coverage that NFIP generally excludes, meaning they cover your hotel stays, meals, and temporary housing if you face displacement from flooding. NFIP offers dislocation expense coverage as an add-on, but private policies typically bundle this protection as standard. The waiting period matters significantly: NFIP imposes a mandatory 30-day waiting period before coverage begins, while private carriers typically require only 10 to 14 days and can sometimes issue same-day bindings. This speed advantage proves critical if you’re closing on a home purchase or need immediate protection.

Elevation Improvements and Mitigation Credits Make a Real Difference

Private flood policies respond better to elevation improvements and mitigation investments than NFIP does. An elevation certificate showing your home sits 3 feet above the base flood elevation can generate 20 to 60% premium discounts with private carriers, compared to 10 to 70% with NFIP depending on how many feet above elevation your property sits. Engineered vents, flood-resistant materials, and backflow prevention devices all qualify for credits that reduce your premium substantially.

Market Stability and the Layering Strategy

The trade-off with private flood involves market stability and lender acceptance. NFIP guarantees renewal of your policy year after year, while private carriers can non-renew or exit markets entirely after major storms. Federal law requires that lenders accept private flood policies meeting specific criteria under the Biggert-Waters Act, but this doesn’t eliminate the stability concern. Many Naples homeowners solve this through layering: they purchase NFIP as their base policy for stability and federal protection, then add private excess coverage on top to reach higher total limits. This approach costs less than purchasing full limits through NFIP alone while preserving the certainty that your base coverage will always renew.

Matching Your Property Type to the Right Coverage Option

Properties built after 2000 with proper elevation documentation almost always qualify for better private pricing than NFIP. Older properties without elevation certificates, properties with repetitive loss histories, or those in the highest-risk coastal zones often find NFIP remains their most practical option regardless of cost. The comparison requires examining your specific property details: your elevation relative to base flood elevation, your home’s construction date, whether you have an elevation certificate, and your total replacement cost for both structure and contents. Once you understand which option fits your property’s profile, you can evaluate the additional protections that work alongside your primary flood coverage to address gaps that standard flood policies leave unprotected.

Closing the Gaps Your Flood Policy Leaves Open

Basement Improvements and the Coverage Void

Standard flood insurance covers your dwelling structure and personal property inside the home, but significant exposures remain unprotected. Basement improvements represent one critical gap. NFIP policies exclude finished basements, meaning your basement walls, flooring, insulation, and built-in fixtures receive no coverage even though these improvements can cost $30,000 to $75,000 to restore. Private flood carriers handle basements differently depending on the specific policy, but most still exclude or severely limit basement coverage unless you purchase it as an explicit add-on. If your Naples home includes a finished basement with flooring, drywall, electrical systems, or HVAC equipment, you need to verify whether your chosen policy covers these items and at what percentage. Many homeowners discover too late that their basement improvements fall into a coverage void, leaving them responsible for tens of thousands in restoration costs. Excess flood insurance purchased above your primary policy can sometimes address this gap, though you’ll need to confirm the excess policy actually covers basement contents that your primary policy excludes.

Personal Property and Replacement Cost Gaps

Personal property coverage under flood insurance applies only to items inside your home, leaving outdoor structures, pools, and landscaping completely unprotected. NFIP contents coverage maxes out at $100,000 with actual cash value, meaning your furniture, electronics, artwork, and clothing receive depreciated values rather than replacement costs. A five-year-old television worth $1,500 new might receive only $600 in actual cash value, forcing you to absorb the difference. Private flood policies typically offer replacement-cost contents instead, paying what you actually need to replace items, not their worn-out value. This difference matters enormously for households with substantial personal property.

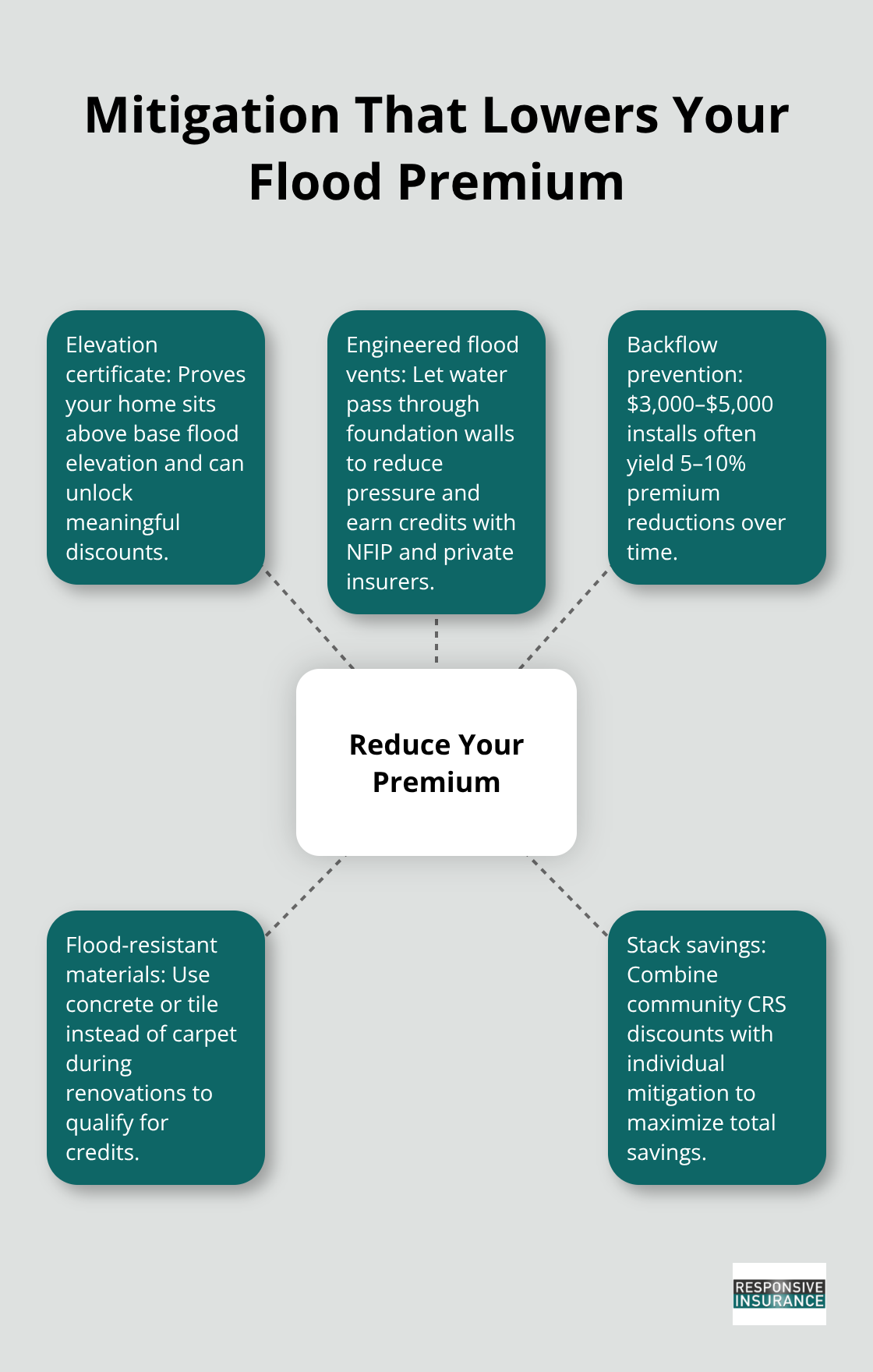

Elevation Certificates and Premium Reductions

Mitigation investments directly reduce your premiums across both NFIP and private options, making them worth pursuing before you finalize your coverage. An elevation certificate documents that your home sits above the base flood elevation and generates meaningful discounts with private carriers. This single improvement often pays for itself within a few years through premium savings alone.

Additional Mitigation Measures That Lower Costs

Engineered flood vents allow water to flow through your foundation rather than building pressure against it and qualify for meaningful credits with both NFIP and private insurers. Backflow prevention devices installed on your sewer lines cost $3,000 to $5,000 but typically generate 5 to 10 percent premium reductions that recover the investment within five to ten years. Flood-resistant materials used during renovations, such as concrete or tile flooring instead of carpet, also qualify for credits, though these become practical only when you’re already planning renovation work.

The City of Naples CRS Class 5 rating already provides up to 25 percent discounts on NFIP policies for participating properties, but individual mitigation measures stack on top of this community-wide discount, meaning your actual savings can exceed 40 percent if you combine elevation improvements with other upgrades and verify that your specific policy reflects all available credits.

Final Thoughts

NFIP provides stability and federal backing with coverage limits capped at $250,000 for dwellings and $100,000 for contents, using actual cash value that depreciates your belongings. Private flood carriers offer higher limits reaching $10 million, replacement-cost contents that pay full replacement prices, and loss-of-use coverage for temporary housing. The cost comparison depends entirely on your property’s elevation, construction date, and flood zone, with private options running 20 to 35 percent cheaper in moderate-risk areas but potentially more expensive in high-risk coastal zones.

Your specific situation determines which option makes sense when choosing flood insurance. Properties built after 2000 with elevation certificates almost always qualify for better private pricing, while older homes without elevation documentation, properties with repetitive loss histories, or those in the highest-risk zones typically find NFIP more practical. Many Naples homeowners solve this through layering-NFIP as their base coverage for guaranteed renewal, then private excess policies on top to reach higher total limits at lower overall cost.

Start by obtaining your flood zone designation from FEMA’s Flood Map Service Center and calculate your actual replacement cost for both structure and contents. Verify whether your property qualifies for the City of Naples CRS Class 5 discount, which provides up to 25 percent savings on NFIP policies, and contact Responsive Insurance, Inc. to compare flood coverage options and find the best fit for your Naples property.