Professional Liability Insurance Florida Guide

One mistake in your professional practice can cost thousands in legal fees and damage your reputation with clients. Professional liability insurance in Florida protects you from these financial and reputational risks.

At Responsive Insurance, Inc., we help Florida professionals understand what coverage they actually need and how to find the right policy for their business.

What Professional Liability Insurance Actually Covers

Professional liability insurance, also called Errors and Omissions or E&O insurance, protects your business when a client claims you made a mistake, gave bad advice, or failed to deliver what you promised. Unlike general liability insurance, which covers bodily injury and property damage, professional liability specifically addresses claims of negligence in the services or advice you provide. If a client sues because they lost money due to your error, misrepresentation, or breach of professional duty, this coverage pays for your legal defense, court costs, settlements, and judgments.

What You’ll Actually Pay

Solo practitioners in Florida typically pay between $1,200 and $3,000 annually for professional liability coverage, while small firms with two to five professionals usually face premiums in the $3,500 to $10,000 range. Your industry, claims history, and coverage limits you select heavily influence the cost. Real estate agents, consultants, accountants, engineers, attorneys, and IT professionals face the highest exposure to negligence claims, making this coverage non-negotiable for their operations. Attorneys handling real estate transactions, personal injury, or securities work face particularly high premiums because these practice areas generate more claims.

Immigration lawyers and criminal defense attorneys typically see lower premiums due to fewer claims. Geographic location also affects your rate: attorneys practicing in Miami-Dade or Broward counties may pay slightly more than those in less litigious areas due to higher claims activity in those markets.

Who Actually Needs This Coverage

If your business provides services or advice rather than products, professional liability insurance matters for you. Many client contracts now require proof of professional liability insurance before they’ll hire you, making it a business requirement rather than optional protection. If you’ve had even one prior claim, expect your premiums to increase significantly, which is why risk management practices matter from day one.

The Hidden Problem: Shrinking Limits

A critical detail most professionals miss: your policy limits shrink as you use them. When your insurer pays for legal defense costs, those payments reduce the amount available to settle or pay a judgment. A $1 million policy doesn’t guarantee $1 million in protection if half goes to lawyers before trial. This is why many Florida professionals choose higher limits like $1 million per claim and $3 million aggregate. Extended litigation drains reserves quickly, sometimes lasting two to three years. Working with an independent agent who understands Florida’s claims environment helps you select limits that actually match your exposure rather than guessing at numbers.

Moving Forward With the Right Coverage

The right professional liability policy protects your assets and reputation when claims arise. Understanding what coverage actually costs and what it covers positions you to make informed decisions about your protection needs.

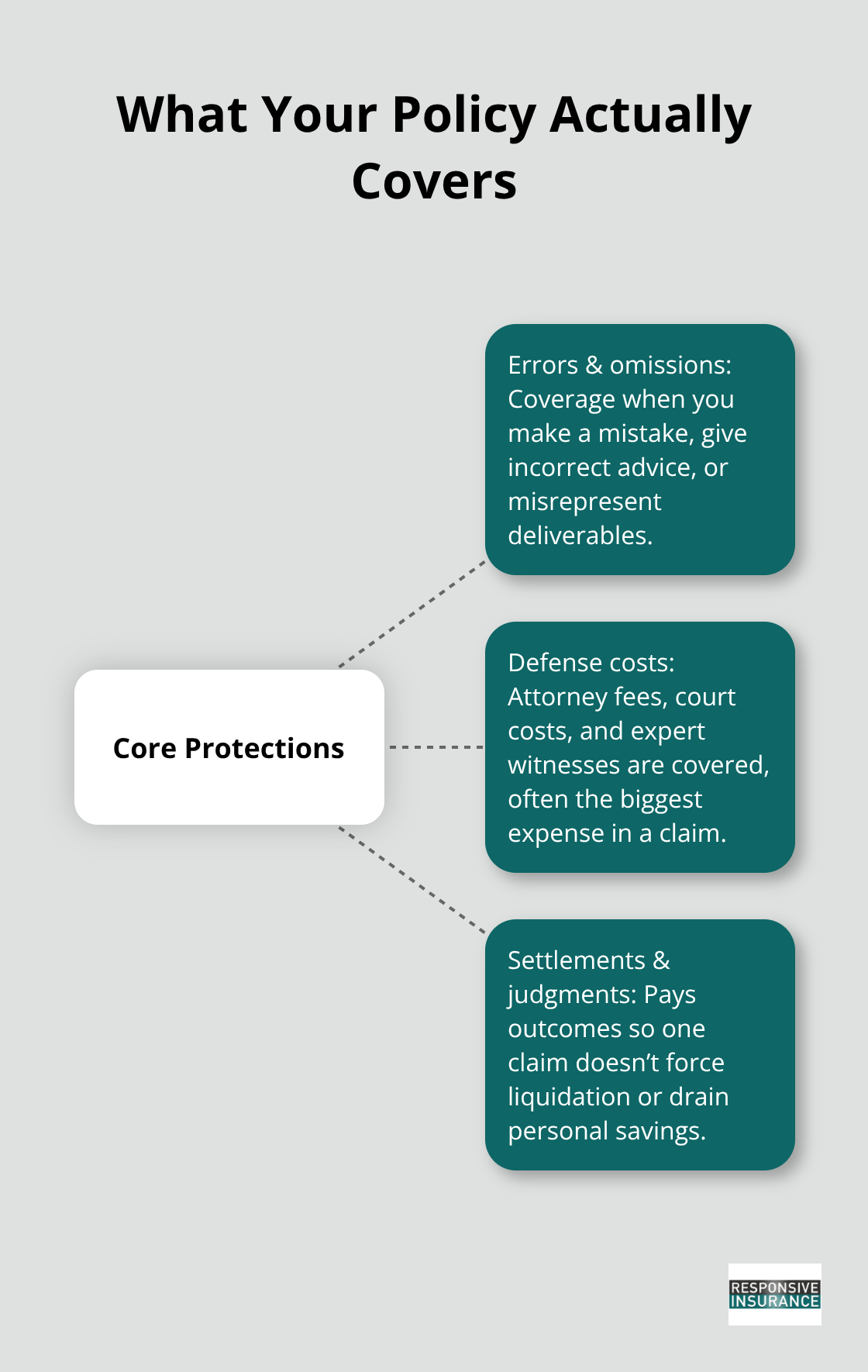

What Your Professional Liability Policy Actually Protects

When a client files a negligence claim against your business, your professional liability policy covers three critical areas that general liability simply won’t touch. First, errors and omissions coverage pays when you make a mistake in delivering your service, give incorrect professional advice, or misrepresent what you can deliver. If a client claims you failed to complete work properly or that your guidance cost them money, this coverage responds.

Second, your policy covers the full cost of defending yourself, including attorney fees, court costs, and expert witness expenses. This matters enormously because legal defense in Florida can easily exceed $50,000 before a case reaches trial, and extended litigation lasting two to three years drains resources rapidly. Third, the policy protects your reputation by covering settlements and judgments, which prevents a single claim from forcing you to liquidate business assets or personal savings. Without this protection, even an unfounded claim can devastate your finances simply through the cost of proving your innocence.

Defense Costs Consume Your Coverage Limits

The shrinking limits problem deserves your attention because it directly affects what protection you actually have. Suppose you carry a $1 million per claim limit. Your insurer defends you in a negligence lawsuit, spending $300,000 on legal fees before settlement. You now have only $700,000 remaining to cover the actual settlement or judgment. If the client wins and the court awards $800,000 in damages, you owe $100,000 out of pocket because your coverage limit got consumed by defense costs. Florida professionals who work in high-risk areas like real estate transactions, financial advising, or engineering should seriously consider limits of $1 million per claim with $3 million aggregate. An independent agent can review your specific exposure and recommend limits that account for both potential judgments and the legal costs required to defend them.

Client Relationships Suffer From Claims, Even Winning Ones

A professional liability claim damages your reputation even when you win. Clients talk, and word spreads that you’ve been sued, regardless of the outcome. Your policy addresses this by paying defense costs quietly without requiring you to drain business cash flow or take loans. When settlements happen, they’re typically confidential, limiting public knowledge of the dispute. This confidentiality protects your ability to attract new clients and retain existing ones. Many client contracts in Florida now require proof of professional liability insurance before they’ll engage your services, making coverage a prerequisite to getting hired rather than optional protection. Attorneys in Miami-Dade and Broward counties understand this reality particularly well, as high claims activity in those markets means clients expect proof of coverage as standard practice. Your next step involves assessing your actual business risks to determine what coverage limits and policy features match your specific exposure.

Finding the Right Coverage for Your Business

Match Your Exposure to Policy Limits

Selecting professional liability coverage requires matching your actual exposure to the right policy limits, deductibles, and endorsements rather than picking arbitrary numbers. Start by documenting what your business does and where claims typically arise. If you’re an accountant, tax errors and missed deadlines create the most exposure. If you’re a real estate consultant, transaction mishandling and misrepresentation of property conditions matter most. If you’re an IT consultant, data loss and system failures drive claims. This specific understanding of your risks shapes everything that follows.

Next, review your client contracts to see what coverage limits clients actually require before they’ll hire you. Many Florida businesses now demand minimum coverage of $1 million per claim with $3 million aggregate, meaning you need at least that much to win new business regardless of what you think you need. Compare this contractual requirement against your estimated exposure based on your typical project size and client financial losses. A consultant handling $50,000 projects faces different risk than one managing $500,000 engagements. Solo practitioners often underestimate their exposure because they think small practice size means small claims, but a single error can cost a client far more than your annual revenue.

Choose Deductibles That Fit Your Financial Position

Your deductible choice directly impacts your premium and out-of-pocket exposure. A $5,000 deductible costs significantly less than a $1,000 deductible, but it means you cover the first $5,000 of any claim before insurance kicks in. Florida professionals handling high-value transactions should try $1,000 or $2,500 deductibles because claims often involve large client losses where the difference between a $1,000 and $5,000 deductible matters less than the absolute protection you need.

Work With Agents Who Know Your Industry

Interview three independent agents in Naples who specialize in your specific profession because they understand local claims patterns and which insurers actually pay claims quickly. An agent serving Florida accountants knows which carriers respond fastest to audit-related claims, while an agent serving real estate professionals understands Miami-Dade claims activity differently than an agent in a quieter market. These specialists can compare quotes from multiple carriers to show you actual premium differences between $1 million/$3 million limits versus $2 million/$5 million limits in your specific industry. Request these comparisons in writing so you can see exact figures rather than estimates.

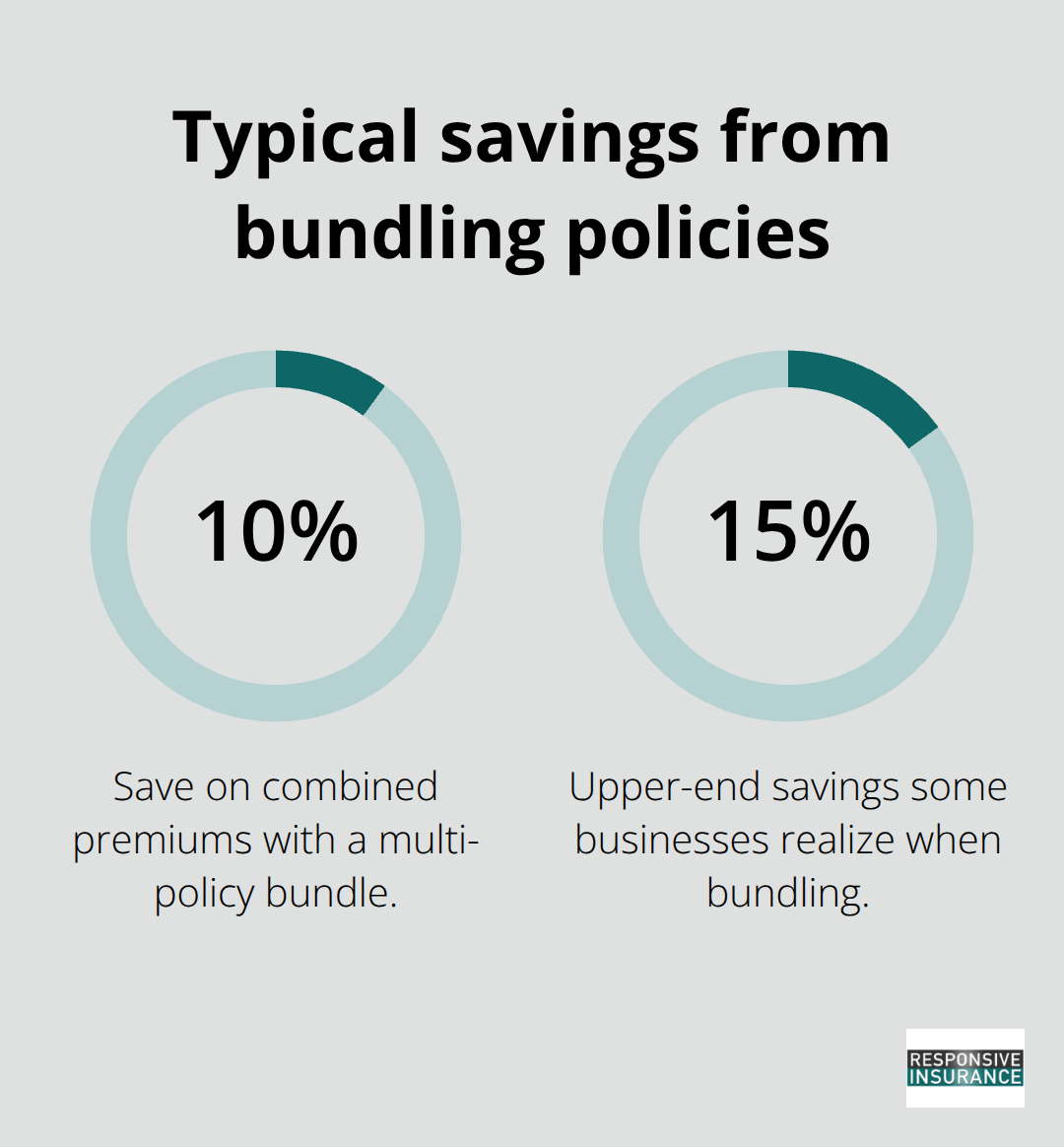

Bundle Policies to Lower Your Total Cost

Bundling professional liability with cyber liability and general liability typically saves 10 to 15 percent on combined premiums compared to buying each separately, so ask agents specifically what discount applies when you purchase multiple policies. An independent agent can show you how adding coverage for specific risks (like cyber incidents or contractual liability) strengthens your protection while potentially reducing your overall cost through bundling discounts.

Disclose Your Claims History Fully

Your claims history matters enormously: even one prior claim increases premiums substantially, which is why clean risk management practices from the start protect your long-term costs. If you’ve had claims, disclose them fully to agents because hiding history will result in coverage denial when you file a claim. This transparency allows agents to find carriers willing to work with your specific situation and price your coverage accurately.

Final Thoughts

Professional liability insurance in Florida protects your ability to operate your business and serve clients without constant financial fear. The coverage you select today determines whether a single negligence claim forces you to liquidate assets or whether your insurance handles the legal costs, settlements, and judgments that arise. Solo practitioners paying $1,200 to $3,000 annually and small firms investing $3,500 to $10,000 yearly gain protection that prevents catastrophic financial loss.

Start by documenting your actual business risks and reviewing client contracts to see what coverage they demand before hiring you. Most Florida professionals discover their clients require $1 million per claim with $3 million aggregate, which sets a baseline for your shopping process. Request written quotes from three independent agents who specialize in your profession because they understand local claims patterns and which carriers respond fastest when claims arise.

Contact Responsive Insurance, Inc. to discuss your professional liability insurance Florida needs and get quotes tailored to your specific practice. We compare coverage options from multiple A-rated insurance companies and find the policy that actually fits your needs and budget. We work with you to understand your exposure, match it to appropriate limits, and secure the protection your business requires.