Small Business Insurance Florida Options

Running a small business in Florida means protecting what you’ve built. Without the right coverage, a single lawsuit or property damage claim can threaten your entire operation.

At Responsive Insurance, Inc., we help Florida business owners understand which small business insurance policies actually matter for their situation. This guide walks you through the coverage types you need, why they’re important, and how to pick the right plan for your business.

Essential Coverage Types for Florida Businesses

General liability insurance protects your business when someone gets injured on your property or your operations damage their property. In Florida, this coverage is often mandatory if you lease commercial space or bid on contracts. Typical general liability premiums for small Florida businesses fall between $400 and $1,500 annually, depending on your industry and location. High-risk sectors like construction and food service pay significantly more than low-risk fields like consulting. The coverage pays for medical expenses, legal defense, and settlements, which means without it, you remain personally liable for these costs. Many Naples businesses skip this coverage thinking they’ll never need it, then face financial devastation when a customer slips on wet flooring or your equipment damages their property.

Property Coverage Protects What You Own

Commercial property insurance covers your building, equipment, inventory, and fixtures against fire, theft, weather damage, and vandalism. In Naples and surrounding areas, flood and hurricane damage represent the biggest threats to business assets. FEMA flood zones AE and VE cover significant portions of commercial areas in Collier County, making flood coverage essential rather than optional. Standard commercial property policies exclude flood damage, so you’ll need a separate flood policy if you’re in a high-risk zone. A contractor’s tools and equipment might be worth $15,000 to $50,000, and without tools and equipment coverage, theft or damage on job sites leaves you replacing everything from your pocket. Business interruption coverage, often added to property policies, reimburses lost income if a hurricane or fire forces you to close temporarily. This matters enormously in Florida, where hurricane season runs June through November and can shut down operations for weeks.

Commercial Auto Protects Your Fleet

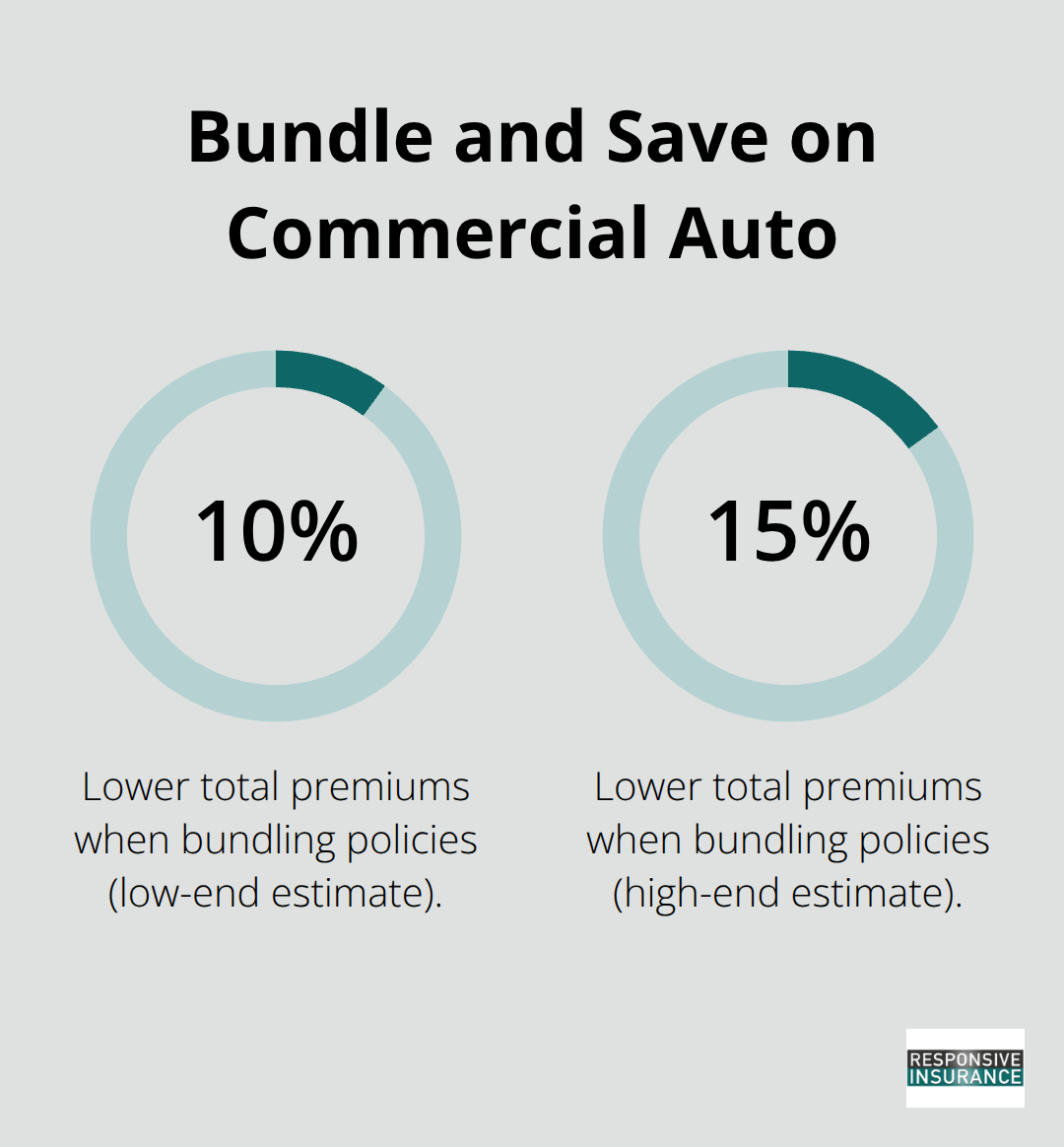

Commercial auto insurance covers company-owned vehicles used for business purposes, which personal auto policies explicitly exclude. If your employee causes an accident while making a business delivery, your personal auto insurance won’t cover the liability or vehicle damage. Florida businesses using vehicles for client visits, deliveries, or service calls need this coverage. Premiums vary widely based on vehicle type, driver records, and annual mileage, but expect $1,000 to $3,000 annually for a single commercial vehicle. Contractors with multiple work trucks or plumbers with service vans benefit significantly from commercial auto bundled with general liability and property coverage, which can reduce total premiums by 10 to 15 percent compared to purchasing policies separately. Understanding these three core coverages sets the foundation for evaluating additional protections your specific business may require.

Why Florida Businesses Can’t Afford to Skip Insurance

A single lawsuit in Florida costs a small business owner tens of thousands of dollars in legal fees alone, before any settlement or judgment. Construction companies, restaurants, and service providers face the highest exposure because their work directly impacts customers and their property. General liability claims in Florida average $5,000 to $50,000 depending on injury severity and property damage, according to industry claims data.

Without coverage, you write personal checks for medical bills, attorney fees, and court judgments. Landlords and clients won’t work with you without proof of insurance-most commercial leases and service contracts explicitly require general liability coverage with minimum limits of $1 million. Florida’s workers’ compensation law mandates coverage for any business with four or more employees, and violations result in fines starting at $500 per employee per day. Property damage claims from hurricanes, floods, and theft destroy businesses equally; a single hurricane can destroy $100,000 worth of inventory, equipment, or building improvements in minutes.

What Happens When You Get Sued

Defending a lawsuit costs money upfront, even if you win. Your business pays attorneys, expert witnesses, and court fees while your case moves through Florida’s court system, which typically takes 18 to 36 months for commercial disputes. General liability insurance covers these defense costs separately from your policy limits, meaning your insurer pays your attorney while your coverage limit remains intact for any judgment. Without this coverage, a customer’s slip-and-fall claim or a contractor’s property damage allegation forces you to liquidate business assets or take on personal debt just to afford legal representation. Product liability claims for food poisoning, allergic reactions, or equipment failure add another layer of financial risk that many small business owners underestimate until it’s too late. Professionals like accountants, consultants, and real estate agents need professional liability insurance specifically because their advice or services can cause financial harm to clients, and these claims frequently exceed $100,000 in damages.

Natural Disasters and Business Interruption

Florida experiences hurricane season annually from June through November, and the state averages one major hurricane every 2.5 years according to historical data. Property damage alone doesn’t tell the full story-business interruption is where most Florida owners face unexpected financial collapse. If a hurricane forces you to close for three weeks, your expenses continue while revenue stops completely. Business interruption coverage reimburses lost income during forced closures, covering payroll, rent, utilities, and loan payments while your business recovers. Flood damage represents the second-largest threat to Florida commercial properties, with claims frequently ranging from $25,000 to $250,000 depending on water depth and building contents. Standard property policies exclude flood entirely, so you need a separate flood insurance policy to protect against this specific peril. Commercial property insurance also covers equipment breakdown, which matters for businesses relying on refrigeration, HVAC systems, or specialized machinery (a broken walk-in cooler in a restaurant can cost $2,000 to $5,000 in emergency repairs plus lost food inventory).

Coverage Gaps That Expose Your Business

Many Florida business owners purchase general liability and property insurance, then stop there, leaving critical gaps in their protection. Workers’ compensation coverage protects your employees and your business from injury claims, yet some owners skip it thinking they can’t afford it. The cost of a single workplace injury claim-medical treatment, lost wages, and legal fees-typically exceeds annual workers’ compensation premiums by thousands of dollars. Commercial auto insurance represents another overlooked necessity; if your employee causes an accident while making a business delivery, your personal auto insurance won’t cover the liability or vehicle damage. Contractors with multiple work trucks or plumbers with service vans benefit significantly from commercial auto bundled with general liability and property coverage, which can reduce total premiums by 10 to 15 percent compared to purchasing policies separately. These gaps don’t disappear-they wait for the moment when a claim exposes them, and that’s when your business faces financial ruin. Understanding which coverage types your specific business needs sets the foundation for evaluating additional protections and selecting the right insurance partner to guide you through the process.

Choosing the Right Coverage for Your Business

Start by mapping your actual business operations, not an imaginary version of your business. Walk through a typical workday and identify every point where someone could get injured, your property could be damaged, or your operations could harm a customer. A restaurant owner should list slip-and-fall risks in the dining area, food contamination exposure, employee injuries in the kitchen, and inventory losses from equipment failure.

A contractor should account for injuries on job sites, property damage caused by their work, tools stolen from vehicles, and employee accidents. This exercise takes 30 minutes and reveals which coverage types matter most for your specific situation. Many Florida business owners purchase whatever their neighbor has, then discover critical gaps when a claim happens. Document your findings in writing so you can reference them when comparing quotes from insurance providers.

Gather Quotes from Multiple Providers

Shopping around isn’t optional if you want fair pricing. When you request quotes, provide the same business information to all providers so you’re comparing identical scenarios.

Specify your industry, number of employees, annual revenue, years in business, claims history, and the exact coverage limits you’re considering. Prices vary dramatically based on these details, and a quote based on incomplete information wastes your time. Request quotes from both national carriers and local independent agencies, which compare multiple A-rated companies to find options tailored to your business rather than pushing one-size-fits-all policies. Independent agencies in Naples typically have deeper knowledge of local risks like hurricane exposure and flood zones that affect your premiums and coverage needs.

Understand Policy Limits and Deductibles

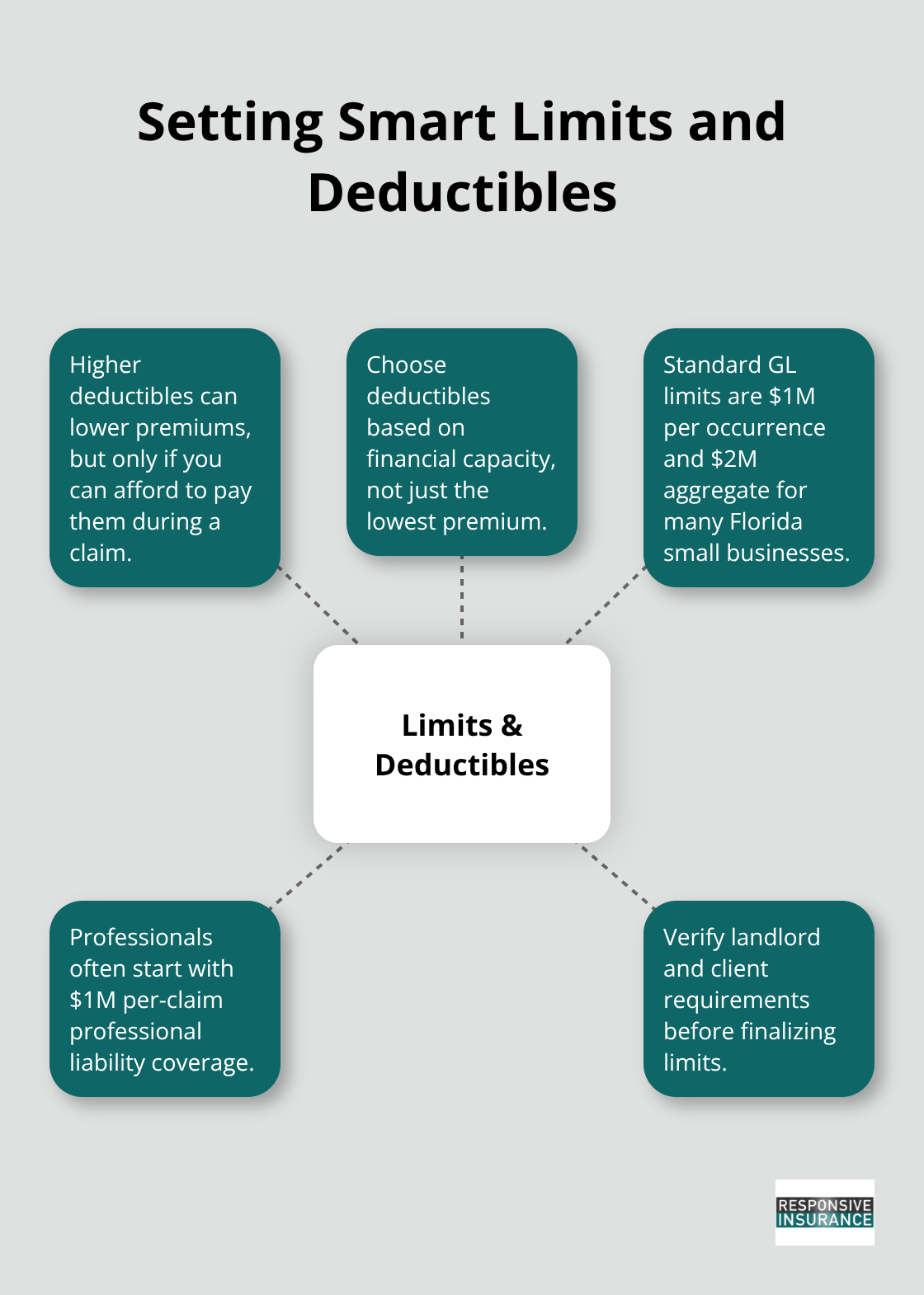

Policy limits determine the maximum amount your insurance pays for a claim, while deductibles determine how much you pay out of pocket before coverage kicks in. Higher deductibles lower your premiums, but only if you can actually afford to pay that amount when a claim occurs.

A contractor with $50,000 in liquid reserves can comfortably handle a $2,500 deductible and save $400 to $600 annually on premiums. A restaurant with $10,000 in emergency funds cannot afford a $5,000 deductible because a single claim would drain reserves needed for operations. Choose deductibles based on your financial capacity, not just the lowest premium option.

General liability limits of $1 million per occurrence and $2 million aggregate represent the industry standard for most Florida small businesses, though high-risk industries like construction often need higher limits. Professional liability policies for consultants and real estate agents typically start at $1 million per claim. Review what your landlord, clients, and contract partners actually require in writing before finalizing limits because buying inadequate coverage to save money creates exposure that a single lawsuit will reveal.

Final Thoughts

Small business insurance in Florida protects your legal liability, physical assets, and vehicles-the three pillars that keep your business solvent when claims happen. General liability, commercial property, and commercial auto insurance address the most common and costly risks you face, from slip-and-fall lawsuits to hurricane damage to vehicle accidents. A local insurance agent understands Florida’s specific risks in ways national call centers cannot, knowing which flood zones affect your location and how hurricane exposure impacts your premiums.

At Responsive Insurance, Inc., we work with multiple insurance companies to compare coverage and find the best fit for your small business insurance Florida needs. Our team provides timely and complete responses to your questions, acting as your advocate rather than just processing paperwork. We understand the Southwest Florida business environment and help you identify which coverages matter most for your specific operation.

Start by documenting your actual business risks, then request quotes from at least three providers using identical information. Review policy limits and deductibles based on your financial capacity, not just the lowest premium. Contact a local agent who can explain your options clearly and answer questions without jargon-your business took years to build, and protecting it with proper insurance takes only a few hours of planning and a phone call.