Homeowners Insurance Florida Condo Policies

Condo owners in Florida face unique insurance challenges that differ significantly from traditional homeowners. Your master policy covers the building’s structure, but you need separate coverage for your interior space and personal belongings.

At Responsive Insurance, Inc., we help Naples residents understand exactly what homeowners insurance Florida condo policies should include. The right coverage protects your investment without leaving gaps or paying for unnecessary protection.

Why Your Condo Insurance Differs from a Standard Homeowners Policy

Your master policy is not your personal insurance. The condo association’s master policy covers the building’s structural elements-the roof, walls, common hallways, elevators, and the original fixtures installed when your unit was built. It does not cover your personal belongings, interior improvements you’ve made, or liability if someone gets injured inside your unit. This gap exists by design under Florida law. The association’s responsibility ends at the boundary of your walls. Everything inside becomes your responsibility.

Most condo associations in Florida require owners to carry an HO-6 policy, and mortgage lenders almost always demand proof of coverage before approving a loan, even when a master policy exists. The average HO-6 condo insurance in Florida costs about $1,858 per year, though Naples residents typically pay closer to $2,570 annually due to hurricane exposure and higher property values.

What the Master Policy Actually Protects

The master policy covers common areas and the structural shell of the building, but deductibles matter significantly. When the association’s deductible applies to a loss affecting your unit, you may face a special assessment to cover your share of the deductible. This assessment can range from hundreds to thousands of dollars depending on the loss and your unit’s percentage of ownership.

Florida law requires associations to maintain replacement-cost coverage updated by independent appraisal at least every 36 months. However, some associations underfund their policies or choose higher deductibles to keep premiums lower. If hurricane damage exceeds the master policy limits, unit owners can be liable for reconstruction costs. This is why loss assessment coverage in your HO-6 policy is critical-it helps pay your portion of shortfalls.

How Your HO-6 Covers Interior Improvements

Your HO-6 covers dwelling improvements-flooring, wall treatments, built-in cabinets-that the association’s policy explicitly excludes. Without this coverage, you would personally fund repairs to these items after a loss. Dwelling coverage in your HO-6 typically ranges from $10,000 to $50,000 or higher, depending on your unit’s interior value and improvements.

Personal property coverage protects furniture, electronics, clothing, and appliances if they suffer damage, theft, or destruction. You should select replacement cost coverage rather than actual cash value-the difference can mean paying out-of-pocket for depreciation.

Liability and Special Risks in Naples

Liability coverage shields you if a guest is injured on your property and sues. Medical payments coverage pays for minor injuries without requiring a lawsuit. Consider liability limits of $100,000 as a baseline, but if you have significant assets in Naples, higher limits of $300,000 or $500,000 make sense.

Flood insurance requires separate attention because standard HO-6 policies exclude flood damage entirely. If your condo is in a flood zone, the association may carry flood coverage for common elements, but you need individual flood insurance for your unit’s interior and belongings. Private flood insurance or National Flood Insurance Program coverage both exist as options.

Wind and Hurricane Coverage Gaps

Wind and hail damage related to hurricanes is typically covered under the master policy for the building’s exterior, but windstorm policies may be necessary depending on your location and the association’s coverage structure. Naples experiences elevated hurricane risk, making adequate wind protection more than theoretical. Your HO-6 should include adequate loss assessment limits to handle potential special assessments from hurricane-related losses.

Condo owners in Naples who understand these layers of protection can now evaluate which coverage types matter most for their specific situation.

Coverage Types You Need in a Florida Condo Policy

Dwelling Coverage for Your Interior Improvements

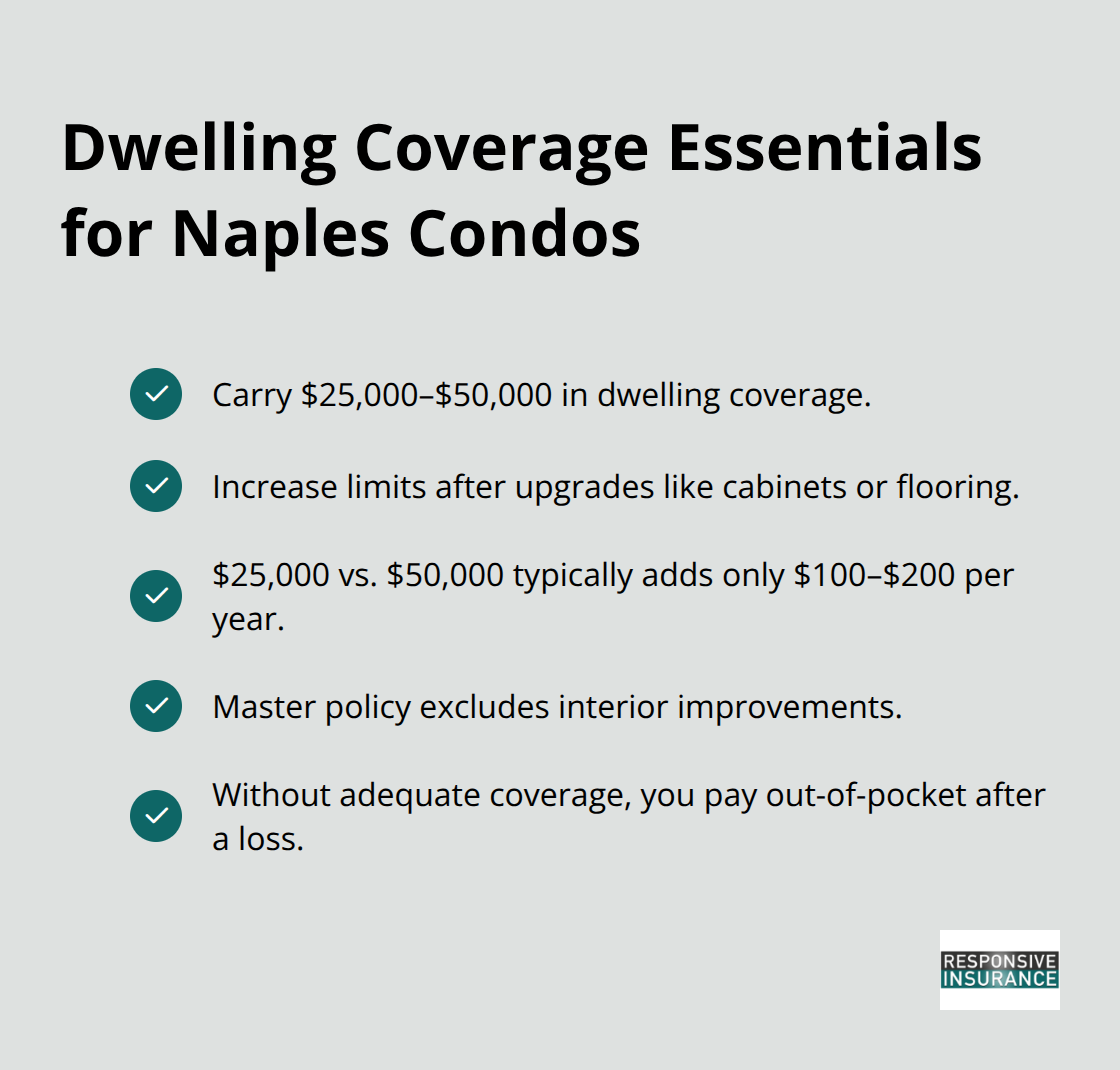

Dwelling coverage protects the interior structure of your unit that the master policy ignores. This includes flooring, wall coverings, built-in shelving, cabinets, countertops, and any fixtures you installed or upgraded. The master policy covers only what was originally installed when the building was constructed, so any improvements you made become your responsibility. Naples condo owners should carry dwelling coverage between $25,000 and $50,000 depending on unit size and renovation history. If you upgraded kitchen cabinets, installed new flooring, or added custom built-ins, higher limits are necessary. The cost difference between $25,000 and $50,000 in dwelling coverage typically amounts to $100 to $200 annually, making it inexpensive insurance against expensive repairs.

Many Naples residents underestimate this coverage because they assume the association’s policy includes interior improvements-it does not. After a hurricane or water damage event, you will pay out-of-pocket for these repairs without adequate dwelling coverage.

Personal Property Protection

Personal property coverage protects your belongings if damage, theft, or destruction occurs. Furniture, electronics, clothing, kitchen appliances, and entertainment systems all fall under personal property. You must choose between actual cash value and replacement cost coverage. Replacement cost coverage costs roughly 10 to 15 percent more but pays what you actually need to replace items today, not what they were worth when you bought them five years ago. In Naples, where hurricane damage and water intrusion are genuine risks, replacement cost coverage makes financial sense. Try setting your personal property limit high enough to cover your belongings-typically $30,000 to $75,000 for a furnished condo unit.

Liability and Medical Payments Coverage

Liability coverage protects you if a guest slips in your bathroom or your dog bites someone visiting your unit. A judgment against you could reach $50,000, $100,000, or higher depending on injury severity. Standard HO-6 policies include $100,000 in liability coverage, but if you own significant assets in Naples, increase this to $300,000 or $500,000. Medical payments coverage, usually $1,000 to $5,000, pays a guest’s minor medical expenses without requiring a lawsuit. This coverage prevents small injuries from becoming legal disputes.

Loss Assessment Coverage

Loss assessment coverage is often overlooked but critical-it reimburses you for special assessments the association levies if hurricane damage or a liability judgment exceeds the master policy limits. Without loss assessment coverage, you could face assessments of thousands of dollars. Purchase loss assessment limits of at least $25,000, preferably $50,000 or higher depending on your association’s financial health and deductible structure. This protection becomes especially important in Florida, where hurricane-related losses frequently exceed association policy limits and trigger special assessments to unit owners.

Florida-Specific Factors Affecting Condo Insurance Costs

Hurricane Exposure and Regional Price Gaps

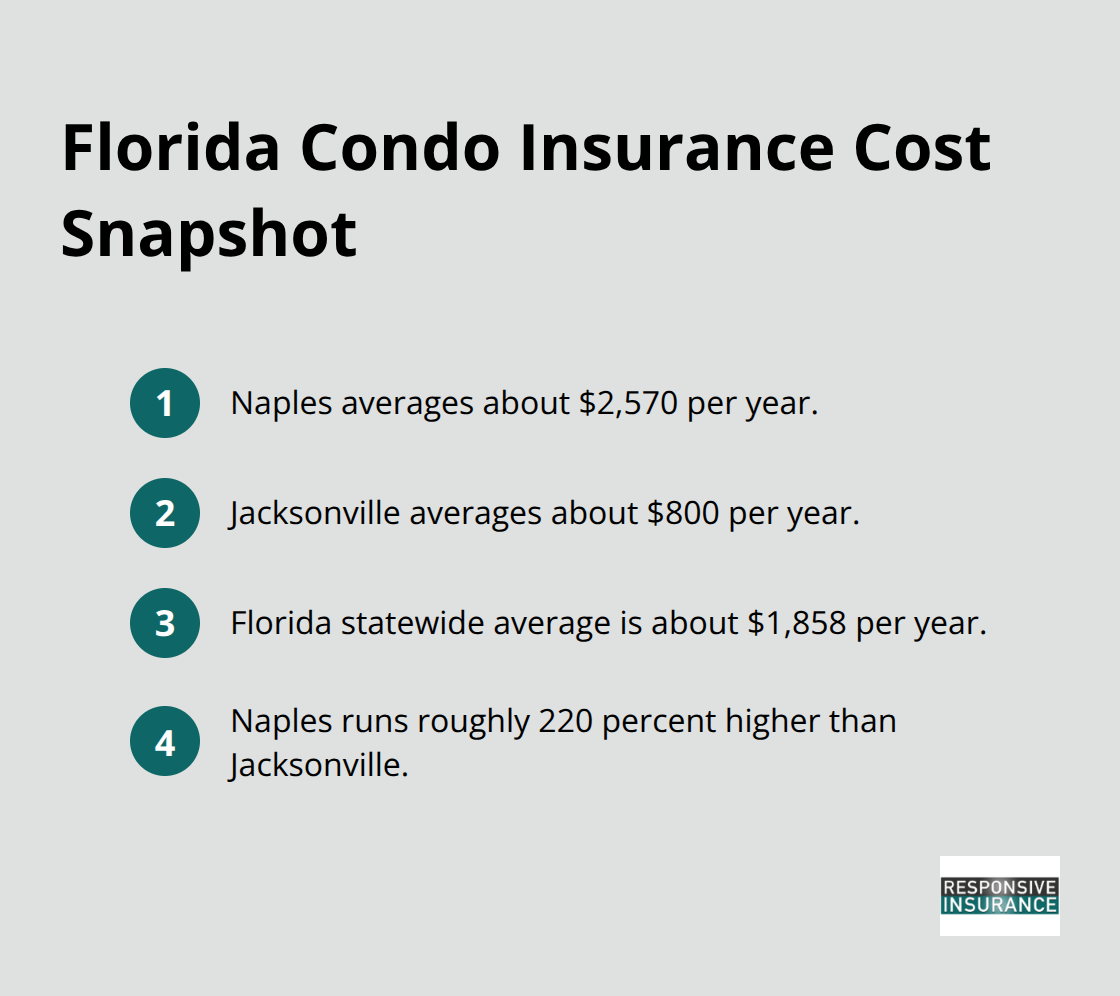

Hurricane exposure creates the largest price gap between Naples condo insurance and rates elsewhere in Florida. The average annual condo insurance cost in Naples reaches $2,570, compared to just $800 in Jacksonville and $1,858 statewide. This 220 percent difference reflects Naples’ position in Florida’s most active hurricane corridor. When a major hurricane strikes, insurers file massive claims across the region simultaneously, forcing carriers to raise rates or exit the market entirely. Florida has experienced significant insurer exits and insolvencies over the past five years, leaving fewer options for Naples condo owners and driving premiums higher as remaining carriers absorb more risk.

Your location within Naples matters significantly-ZIP codes like 34120 average around $2,500 annually while 34109 runs closer to $2,434, showing that even neighborhoods a few miles apart see meaningful rate variation based on coastal exposure and historical loss data.

Windstorm Deductibles and Special Assessments

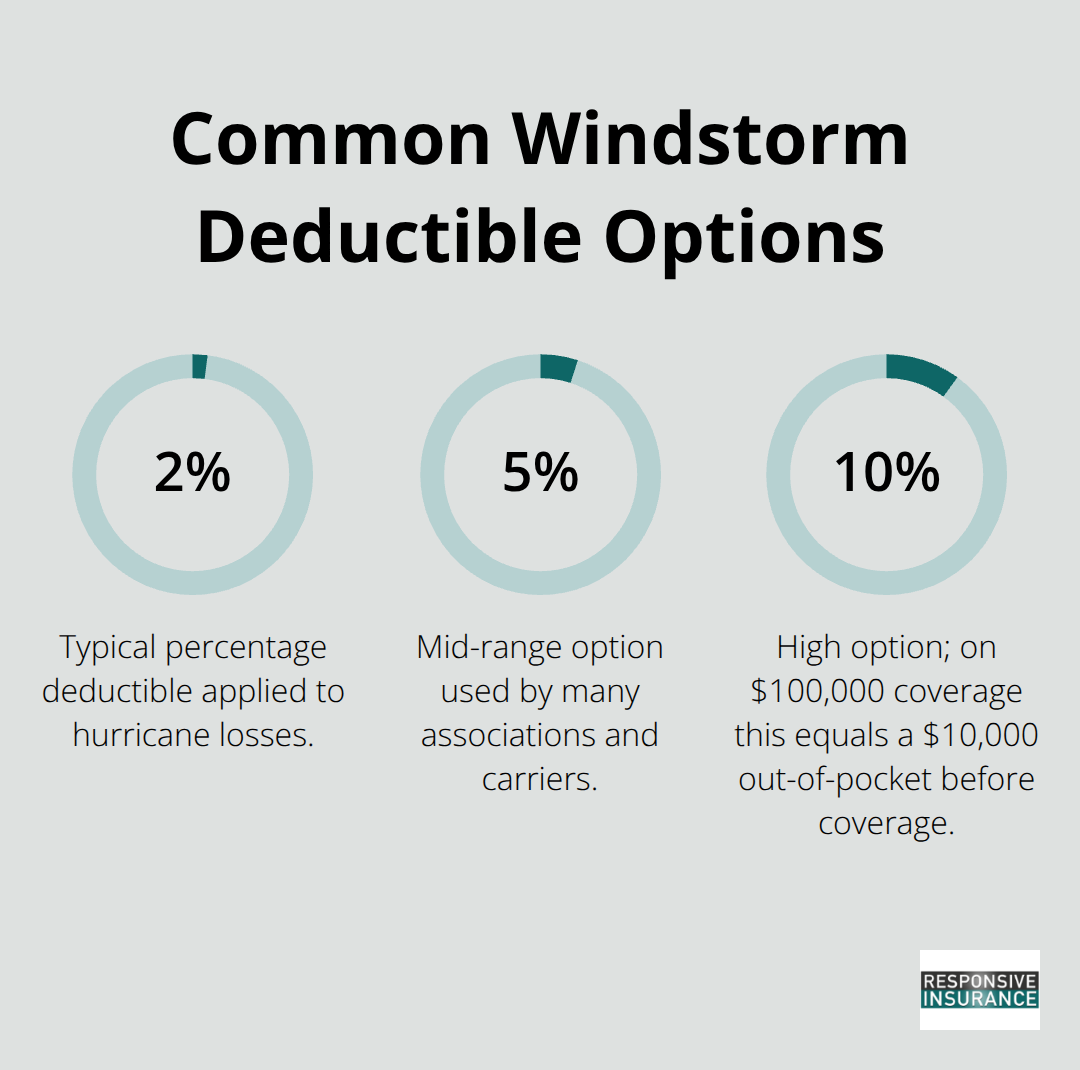

Windstorm deductibles compound the hurricane cost issue substantially. Unlike standard homeowners policies with fixed deductibles of $500 or $1,000, windstorm coverage often applies a percentage deductible-typically two, five, or ten percent of your dwelling coverage limit. On a unit with $100,000 in coverage, a ten percent windstorm deductible means you pay $10,000 out-of-pocket before insurance kicks in for hurricane damage.

This structure exists because insurers cannot absorb the massive concentrated losses from a single storm event.

The master policy’s deductible structure affects your personal costs even more directly. When a hurricane damages the building’s common areas, the association’s deductible applies first. If that deductible is $50,000 or higher and the association’s reserve funds are inadequate, the association levies a special assessment against unit owners to cover their share. You could face an unexpected bill for $5,000 to $15,000 depending on your ownership percentage and the loss severity. Loss assessment coverage in your HO-6 policy reimburses these assessments, making it essential in Naples where major hurricanes occur regularly enough to pose genuine financial risk.

Coastal Proximity and Flood Zone Premiums

Coastal proximity premiums reflect both wind exposure and water intrusion risk. Condos within one mile of the Gulf of Mexico see higher rates than those inland, and properties in flood zones face additional underwriting scrutiny. If your condo sits in a high-risk flood zone, standard HO-6 policies exclude flood damage entirely, forcing you to purchase separate flood insurance through the National Flood Insurance Program or private carriers. NFIP flood policies for condos in Naples typically cost $600 to $1,200 annually depending on zone designation and coverage limits, adding substantially to your total insurance expense.

Credit Scores and Claim History

Credit scores influence your rate more than many Naples residents realize. Condo owners with poor credit pay approximately 20 percent more for HO-6 coverage in Florida. If your credit score sits below 620, expect premiums near the higher end of regional ranges. Improving your credit score before shopping for condo insurance can save $300 to $500 annually. Claim history also determines pricing-if you filed three claims in the past five years, carriers view you as higher risk and charge accordingly.

Deductible Strategies to Lower Premiums

Selecting a higher deductible represents the most effective way to reduce premiums immediately. Moving from a $500 deductible to $1,000 typically saves Naples residents $1,000 or more annually, though this strategy only works if you maintain sufficient emergency savings to cover the higher out-of-pocket cost after a loss.

Final Thoughts

Condo insurance in Florida operates under fundamentally different rules than standard homeowners policies because your responsibility stops at your unit’s walls while the association manages everything beyond them. The master policy protects the building’s structure and common areas, but it leaves your interior improvements, personal belongings, and liability exposure entirely in your hands. This separation of responsibility means you cannot rely on the association’s coverage to protect your financial interests, so homeowners insurance Florida condo policies must fill these gaps with adequate dwelling coverage for your upgrades, personal property protection for your belongings, and liability limits that match your assets.

Naples residents face higher condo insurance costs than most Florida locations due to hurricane exposure and coastal risk, but you can reduce premiums through strategic choices. Increasing your deductible to $1,000 saves roughly $1,000 annually, while bundling condo and auto policies with the same carrier typically generates 10 to 15 percent discounts. Improving your credit score before shopping for quotes can lower rates by 20 percent or more, and comparing quotes from at least three carriers ensures you find competitive pricing rather than accepting the first offer.

Contact Responsive Insurance, Inc. to discuss your condo insurance needs and receive personalized quotes that reflect your unit’s value and your financial priorities. We help Naples residents navigate these decisions by comparing coverage options across multiple A-rated carriers and identifying the protection that matches your specific situation.