Flood Insurance Coverage Requirements Explained

Flooding is the most common natural disaster in Florida, affecting thousands of homeowners annually. Standard homeowners insurance won’t protect your property from flood damage, which is why understanding flood insurance coverage requirements is essential for Naples residents.

At Responsive Insurance, Inc., we help homeowners navigate these requirements and find the right protection for their specific situation.

Why Standard Homeowners Insurance Leaves You Unprotected from Floods

Standard homeowners insurance policies explicitly exclude flood damage, which is why this gap exists across nearly every residential policy sold in Florida. Insurance companies classify flooding as a separate peril requiring its own dedicated coverage. According to FEMA, an inch of floodwater can cause approximately $12,000 in damages to a home, yet most homeowners discover too late that their existing policy provides zero protection. This isn’t an oversight or a fine print technicality-it’s intentional policy design. Homeowners policies cover wind damage from hurricanes, but the moment water enters your home through rising water tables, storm surge, or excessive rainfall, your standard coverage ends.

The Coverage Gap Affects Everyone

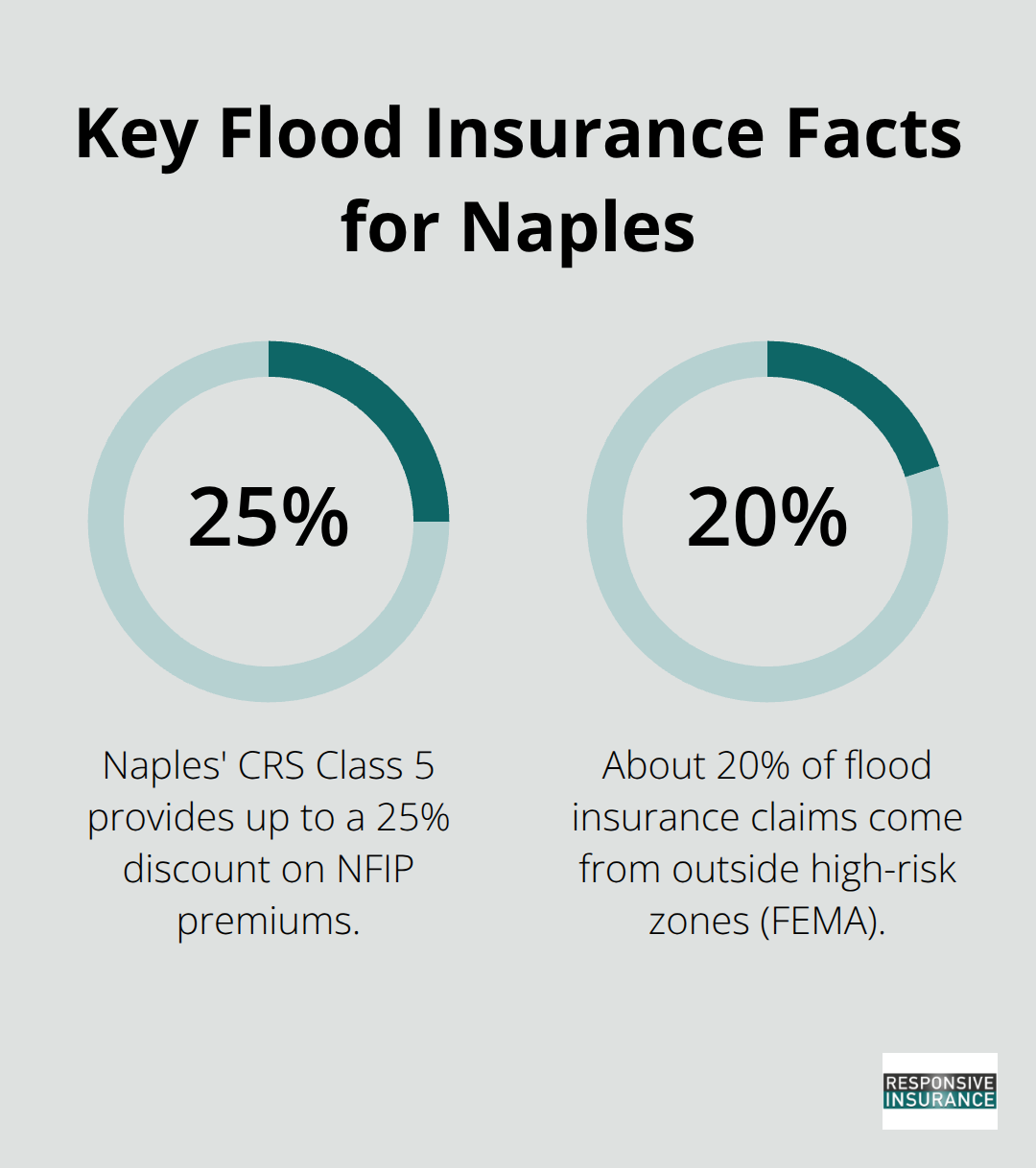

Naples residents in high-risk flood zones face mandatory flood insurance requirements if they carry federally backed mortgages, but even those in moderate-to-low-risk areas should recognize this protection gap. About 20% of flood insurance claims originate from properties outside high-risk zones, according to FEMA data, which means flood risk exists where many homeowners assume they’re safe. This statistic reveals a critical truth: flood damage strikes properties that most people consider protected.

Federal Mandate for Mortgaged Properties

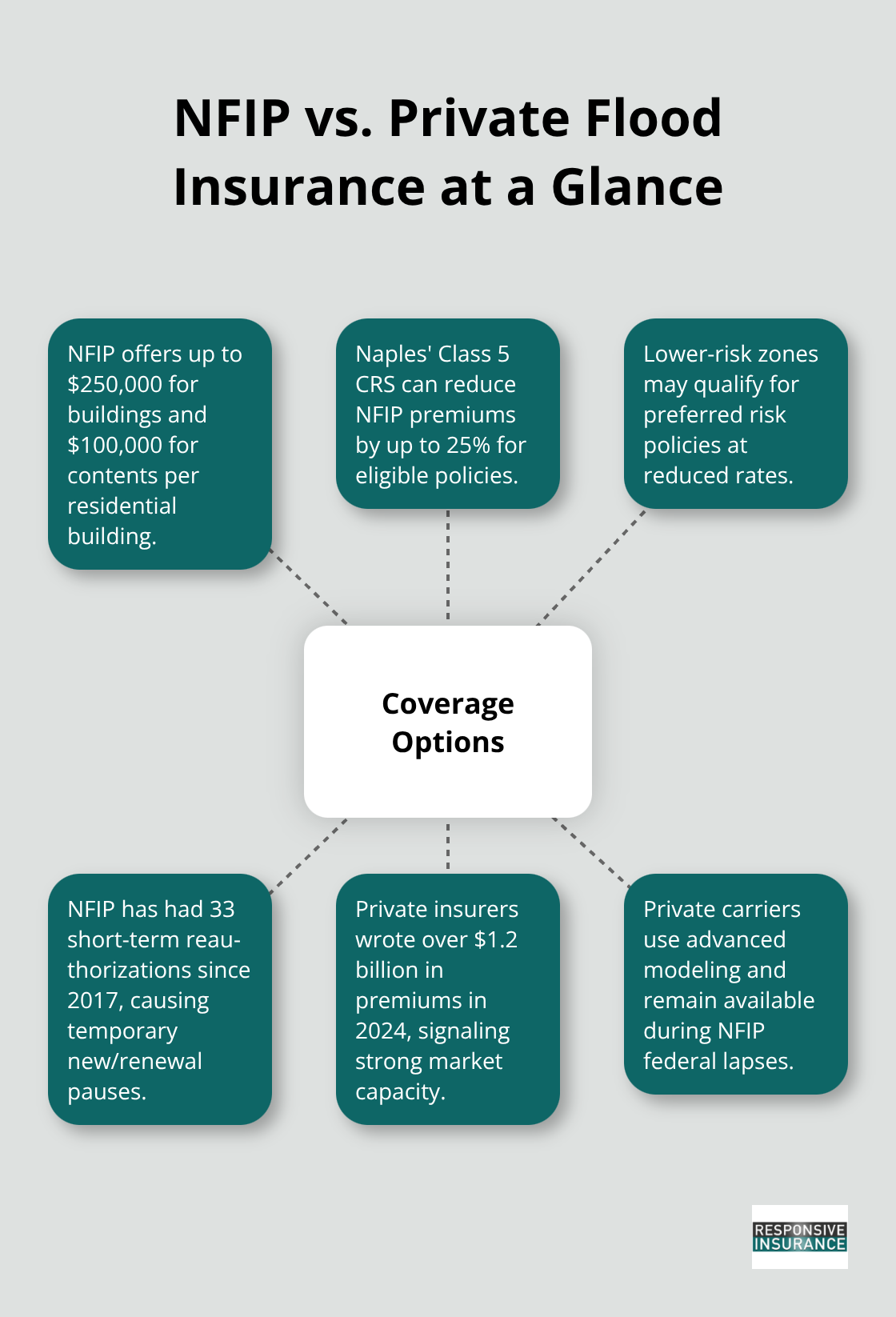

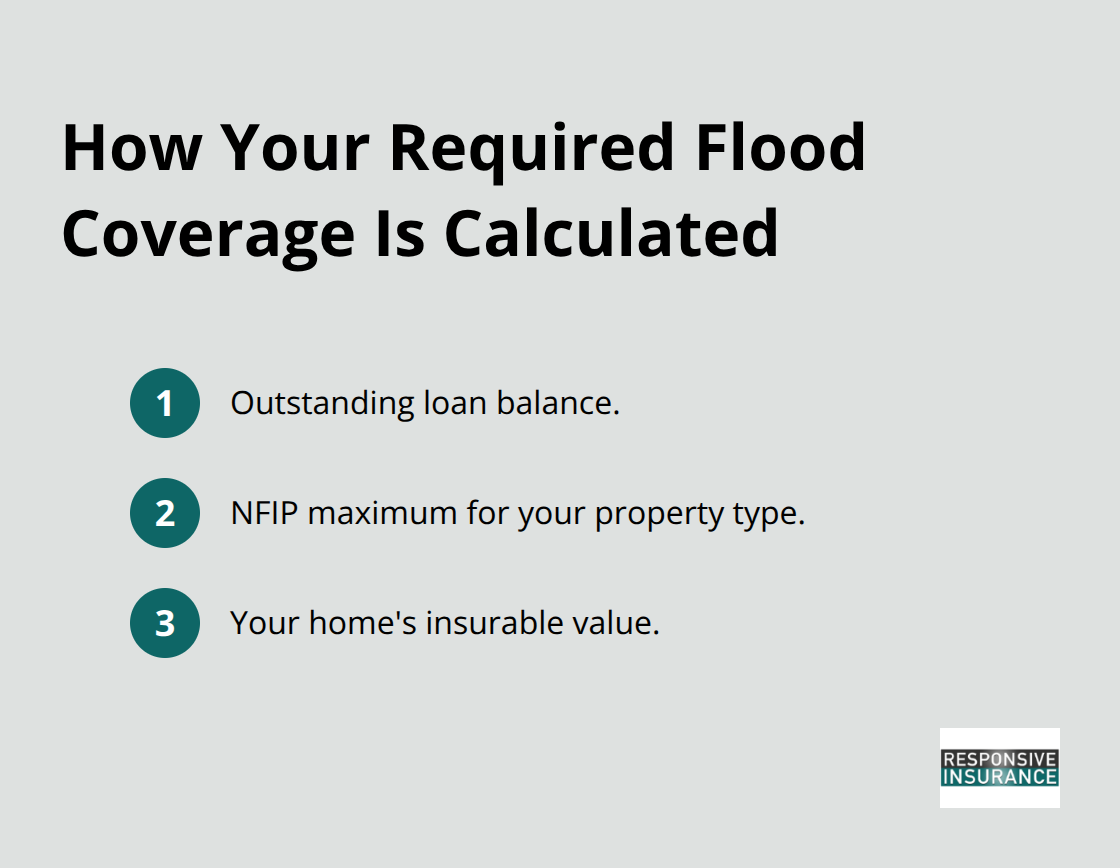

If your property sits in a Special Flood Hazard Area and you have a federally insured or regulated mortgage, the Flood Disaster Protection Act of 1973 mandates that you maintain flood insurance for the life of your loan. Lenders won’t approve your mortgage without proof of coverage, and servicers actively monitor compliance. The minimum required coverage equals the lesser of three factors: your outstanding loan balance, the maximum National Flood Insurance Program limits available for your property type, or your property’s insurable value. For residential structures, NFIP maxes out at $250,000 for the building and $100,000 for contents. If your coverage falls below the required minimum, your lender will force-place flood insurance at your expense, which typically costs significantly more than purchasing it yourself. This federal mandate exists because lenders recognize that uninsured flood losses could trigger loan defaults and destabilize the mortgage market.

Local Protections and Naples-Specific Considerations

Naples participates in the National Flood Insurance Program and maintains a Community Rating System classification of Class 5, which qualifies residents for up to a 25% discount on standard NFIP policies. This local participation means flood insurance is accessible to all Naples homeowners, but it doesn’t reduce the requirement-it simply makes compliant coverage more affordable. The city’s floodplain coordinator can provide detailed guidance on local elevation requirements and flood mitigation strategies, available at 239-213-5039.

Many Naples residents mistakenly believe that purchasing flood insurance is optional in lower-risk zones, but federal policy says otherwise if you have a mortgage in any mapped flood zone. Additionally, if your property has received federal disaster assistance for previous flood losses, you must maintain flood insurance to qualify for future federal aid.

Understanding Your Coverage Options

With federal requirements established and local discounts available, you now face a choice between the National Flood Insurance Program and private flood insurance alternatives. Each option offers distinct advantages depending on your property’s risk profile and coverage needs.

Your Coverage Options

The National Flood Insurance Program Dominates the Market

The National Flood Insurance Program administers over 4.7 million residential policies with $1.3 trillion in total coverage across more than 23,000 participating communities, making it the dominant flood insurance provider in the United States. NFIP offers standardized coverage limits: up to $250,000 for residential building structures and $100,000 for residential contents in a single family home. These limits apply per building, so if you own multiple structures on your property, each building receives its own separate limit. Contents coverage protects personal belongings including furniture, electronics, collectibles, clothing, and jewelry damaged by floodwater. NFIP policies also cover structural damage to walls, ceilings, floors, stairs, and flooring surfaces like wall-to-wall carpeting and tile.

Additional NFIP Protections and Local Advantages

Additional coverages available through NFIP include dislocation expenses such as temporary rent, hotel stays, and meal costs if you are displaced from your home during repairs. For properties in lower-risk flood zones, NFIP offers preferred risk policies at substantially reduced rates compared to standard policies. Naples residents benefit from the city’s Class 5 Community Rating System classification, which provides up to a 25% discount on NFIP premiums. However, NFIP has experienced 33 short-term reauthorizations since 2017 according to the Congressional Research Service, creating periodic coverage lapses that prevent new and renewal policies from being issued. During these lapses, existing policies remain honored, but the uncertainty creates compliance challenges for homeowners and lenders seeking continuous protection.

Private Flood Insurance Fills Market Gaps

Private flood insurance has emerged as a viable alternative, especially during NFIP gaps and for properties in moderate-to-low-risk zones where NFIP premiums may not reflect actual risk. Leading private flood insurers including AXA, Assurant, MS&AD, and Berkshire Hathaway collectively wrote over $1.2 billion in premiums in 2024, demonstrating significant market growth. Private insurers can price risk more accurately using advanced catastrophe modeling and property-specific factors, often resulting in lower premiums for lower-risk properties.

Private policies can also address coverage gaps where NFIP policies have sub-limits or restrictions. The private market provides continuity when NFIP is unavailable due to federal lapses, since private insurers are not dependent on congressional appropriations.

Making Your Coverage Decision

When you select between NFIP and private providers, evaluate your property’s flood risk, loan requirements, and budget constraints. If your lender requires coverage and you live in a participating NFIP community, NFIP’s standardized rates and 25% Naples discount often provide the most cost-effective solution. If NFIP is temporarily unavailable due to a federal lapse, or if your property sits outside the Special Flood Hazard Area but you want additional protection, private flood insurance fills that gap. The choice between these two options depends on your specific circumstances, and understanding both paths helps you move forward with confidence toward the coverage that actually protects your property and satisfies your lender’s requirements.

What’s Your Actual Flood Risk in Naples

Identify Your Flood Zone and What It Means

Start with FEMA’s flood map service to determine your property’s flood zone-whether your home sits in a Special Flood Hazard Area or moderate-to-low-risk zone. Naples residents access this tool online to identify their specific flood designation, and the results directly impact your insurance requirements and costs. Properties in high-risk zones face mandatory coverage if you have a federally backed mortgage, but the critical insight is that flood damage occurs in lower-risk areas too. About 20% of flood insurance claims originate from properties outside high-risk zones according to FEMA data, which means your flood risk may be higher than your zone designation suggests.

Calculate Your Property’s Insurable Value

Once you know your zone, calculate your property’s insurable value by determining what it would cost to rebuild your home from the ground up, excluding land value. This reconstruction cost value matters because NFIP coverage limits are set at $250,000 for residential structures and $100,000 for contents, and your required minimum coverage cannot exceed your insurable value. If your home’s reconstruction cost exceeds these NFIP limits, private flood insurance becomes necessary to close the gap between NFIP’s maximum and your actual replacement needs. Naples residents with homes valued above $350,000 frequently face this situation and need to evaluate private options to achieve adequate protection. Your lender will require coverage equal to the lesser of your outstanding loan balance, the NFIP maximum for your property type, or your home’s insurable value, so these three numbers determine exactly how much insurance you must carry. Document your home’s value with current appraisals, construction cost estimates, or hazard insurance valuations to support your coverage calculations and prevent disputes during claims.

Coverage Requirements for Renters and Business Owners

Renters should purchase renters flood insurance to protect personal belongings since landlord policies cover only the building structure, leaving your furniture, electronics, and clothing completely unprotected from flood damage. Business owners in Naples must evaluate whether their property sits in a mapped flood zone and whether their building contains multiple structures, since NFIP applies separate coverage limits per building. A warehouse with $475,000 in insurable value and a $1,000,000 outstanding loan, for example, requires only $475,000 in coverage because the insurable value is the controlling factor. Mixed-use properties demand careful classification since a building with a restaurant and apartments where the restaurant exceeds 50% of floor space is treated as nonresidential and subject to different NFIP maximums. All Naples property owners and renters should review their specific situation with a licensed agent rather than assuming standard coverage applies, because flood insurance requirements vary significantly based on property type, zone designation, and loan structure.

Final Thoughts

Flood insurance coverage requirements in Naples aren’t optional suggestions-they’re legal obligations backed by federal law and practical necessities that protect your financial security. If you carry a federally backed mortgage on a property in a Special Flood Hazard Area, you must maintain coverage for the life of your loan. An inch of floodwater causes approximately $12,000 in damages, and your standard homeowners policy won’t cover a single dollar of it.

Your path forward involves three concrete steps: determine your flood zone using FEMA’s flood map service and calculate your property’s insurable value, choose between the National Flood Insurance Program and private flood insurance based on your property type and budget, and purchase your policy well before hurricane season arrives (NFIP policies include a 30-day waiting period). The 25% Naples discount through the city’s Community Rating System classification makes NFIP an attractive option for many residents, while private insurers provide flexibility and often better rates for lower-risk properties. Property values change and loan balances decrease, so you should review your policy annually and after any significant home improvements that increase your property’s value.

We at Responsive Insurance, Inc. work with multiple A-rated insurance companies to compare flood insurance coverage requirements and find the solution that fits your Naples property and budget. Contact us to discuss your specific needs and move forward with protection that gives you genuine peace of mind.