Types of Flood Insurance You Need to Know

Flooding is the most common natural disaster in the United States, affecting homeowners across all regions. At Responsive Insurance, Inc., we know that understanding the different types of flood insurance available can feel overwhelming.

This guide breaks down your options so you can pick the coverage that actually protects your home and belongings in Southwest Florida.

What Standard Flood Insurance Actually Covers

Structure and Contents Protection Under NFIP

The National Flood Insurance Program covers direct physical damage from flooding, but most homeowners misunderstand what that means in practice. NFIP policies protect your home’s structure-including walls, electrical systems, plumbing, furnaces, water heaters, permanently installed carpet, and foundation walls-up to $250,000 for residential buildings. Contents coverage adds protection for furniture, clothing, electronics, and other belongings up to $100,000, though you purchase structure and contents as separate policies with separate deductibles. This matters financially: if both your home and possessions flood, you pay two deductibles instead of one, which could mean $2,500 or more out of pocket depending on your deductible choices.

Premium Costs and Naples Discounts

The average NFIP premium in Florida runs about $865 per year according to NerdWallet data, but Naples residents benefit significantly from the city’s Community Rating System Class 5 status, which qualifies you for up to a 25% discount on standard rates. That discount alone saves you roughly $200 annually compared to other Florida communities. FEMA’s Risk Rating 2.0 pricing system now evaluates your specific property’s flood frequency, distance to water, elevation, and rebuilding cost, so two homes on the same Naples street can have dramatically different rates depending on elevation and construction details.

The 30-Day Waiting Period and When It Matters

Your NFIP coverage does not activate until 30 days after you purchase the policy, which means purchasing flood insurance during hurricane season or after a storm warning is essentially pointless. The exceptions exist but are narrow: no waiting period applies if you purchase coverage as part of a mortgage transaction, and a one-day wait kicks in if FEMA redesignates your property into a high-risk zone within the past 12 months. Naples’ 2024 coastal flood map updates and the planned 2026 revisions mean some properties will shift flood zones, potentially triggering that one-day exception.

Deductible Options and Premium Trade-Offs

Deductible options typically range from $500 to $5,000, and choosing a higher deductible meaningfully lowers your annual premium-sometimes by 15% to 30%-but only if you can actually cover that deductible out of pocket when a flood hits. This trade-off between lower monthly costs and higher out-of-pocket expenses during a claim requires honest assessment of your financial situation. Understanding these NFIP basics positions you to evaluate whether standard coverage meets your needs or whether private flood insurance alternatives might offer better protection for your specific situation.

Should You Consider Private Flood Insurance

The Growth of Private Flood Insurance in Florida

Private flood insurance has grown substantially in Florida, now accounting for roughly 35% of the state’s flood market with over 600,000 privately insured properties according to Harbour Insurance data. This shift reflects a fundamental reality: NFIP policies have hard limits that leave many homeowners dangerously underinsured.

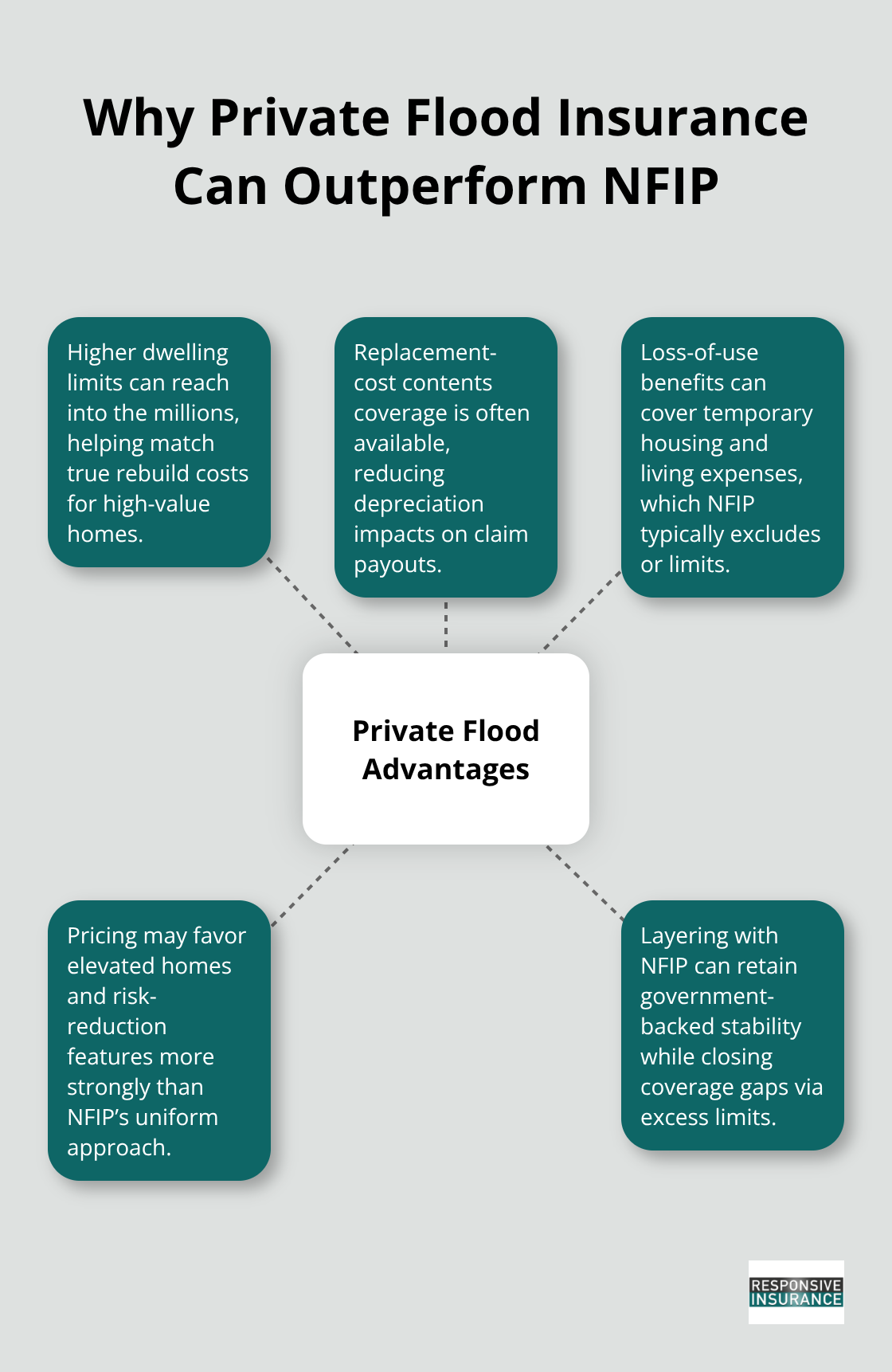

Where NFIP caps dwelling coverage at $250,000 and contents at $100,000, private flood carriers like Neptune Flood, Palomar, and Hiscox offer dwelling limits up to $10 million, replacement-cost contents coverage, and loss-of-use benefits that NFIP either excludes or severely limits. For Naples homeowners with properties valued above $400,000, this gap between NFIP limits and actual replacement costs creates real exposure.

How Private Carriers Price Coverage Differently

Private carriers price differently than NFIP. While NFIP uses Risk Rating 2.0 to evaluate flood frequency, distance to water, elevation, and rebuilding cost uniformly across all properties, private carriers employ proprietary underwriting models that often reward specific risk-reduction features more generously. An elevated home with a current elevation certificate typically qualifies for 15% to 70% premium discounts with private insurers, compared to NFIP’s more modest credits. For a single-family home elevated above the base flood elevation in a moderate-risk zone, private flood insurance frequently costs 10% to 30% less than NFIP annually, translating to $1,500 to $3,000 in long-term savings depending on your flood zone and property characteristics.

Which Properties Benefit Most from Private Coverage

The trade-off is that private flood works best for specific property types. Elevated homes built after 2000 in low-to-moderate risk zones represent ideal private flood candidates and typically see the strongest pricing advantages. Conversely, NFIP remains the better or only option for repetitive-loss properties, pre-1975 construction without elevation documentation, or homes in the highest-risk coastal zones where private carriers either decline or charge prohibitive rates. Many Naples agents recommend a layered approach: use NFIP as base coverage for federal stability and the 25% CRS discount, then add private excess coverage above NFIP limits for high-value homes. This strategy preserves NFIP’s government backing while closing the coverage gap on luxury properties.

Key Policy Details That Separate Quotes

When you compare quotes from private carriers, examine the deductible structure carefully-some use flat dollar deductibles while others use percentage deductibles that can exceed $10,000 on higher-value homes. Loss-of-use limits also vary dramatically; NFIP provides no loss-of-use coverage, but private policies range from $25,000 to $75,000 or more, covering temporary housing and living expenses during displacement. Contents valuation methods matter too: confirm whether replacement-cost value or actual-cash-value applies, since replacement-cost typically costs more but pays significantly more after a claim. These policy details directly affect what you actually recover after a flood, making side-by-side comparisons essential before you commit to any carrier.

Layering Coverage Beyond Standard Flood Insurance

How Excess Flood Insurance Fills Coverage Gaps

Excess flood insurance operates as a second layer sitting directly above your NFIP or primary private flood policy, activating only after your base coverage exhausts. This approach makes practical sense for Naples homeowners with properties valued significantly above NFIP’s $250,000 dwelling cap. If your home rebuilds for $600,000 but NFIP only covers $250,000, you face a $350,000 gap that excess flood insurance addresses. Private carriers like Neptune Flood and Palomar structure excess policies to pick up where NFIP ends, covering additional dwelling damage, higher contents limits, and extended loss-of-use benefits. The premium for excess coverage typically runs $500 to $2,000 annually depending on the additional limit you select, which represents genuine value when your actual exposure exceeds standard program caps. This layered strategy avoids forcing you into a choice between NFIP’s affordability and private insurance’s higher limits; instead, you gain both.

Understanding Umbrella Policies and Flood Protection

Umbrella policies function differently from excess flood coverage and deserve careful distinction. A standard homeowners umbrella provides general liability protection above your home and auto policies, covering lawsuit costs and damages from accidents on your property. Umbrella policies do not cover flood damage directly; they protect against personal liability claims. However, umbrella coverage becomes relevant when flood damage causes secondary liability exposure, such as a neighbor’s property damaged because your flooded foundation wall collapsed or debris from your home drifts onto adjacent lots. A $1 million umbrella policy costs roughly $150 to $300 annually through most Florida carriers and complements flood insurance rather than replacing it. Pairing umbrellas with comprehensive flood coverage makes sense because the two serve fundamentally different purposes.

Bundling Flood Insurance with Homeowners and Auto Policies

NFIP flood insurance cannot bundle with homeowners policies despite both covering your home; NFIP operates as a standalone purchase through participating agents. Private flood insurance occasionally bundles with homeowners coverage through certain carriers, yielding discounts of roughly 5% to 10%, though these savings prove modest compared to standard auto-home bundling discounts of 15% to 25%. The practical advantage of bundling with private carriers centers on administrative convenience and simplified claims handling rather than dramatic premium reduction. Naples homeowners with elevated properties in moderate-risk zones frequently benefit from comparing coverage and prices between private flood bundled with homeowners and NFIP plus separate private excess coverage. Your specific property characteristics determine which structure saves money.

Managing Deductibles Across Multiple Policies

Deductible coordination matters significantly when combining policies; if your homeowners policy carries a $1,000 deductible and you add NFIP with a $2,500 deductible, you could pay $3,500 out of pocket for damage affecting both coverage areas. Some private flood carriers allow you to select matching deductibles across policies, simplifying claims and reducing surprise out-of-pocket costs. Before finalizing any combined coverage arrangement, confirm with your agent exactly how deductibles apply during a multi-peril event affecting both home structure and contents, since this detail directly impacts your actual financial exposure when flooding occurs.

Final Thoughts

NFIP and private flood insurance serve fundamentally different purposes, and your property’s characteristics determine which option protects you best. NFIP offers government-backed stability and the 25% discount Naples residents receive through the city’s CRS Class 5 rating, while private flood insurance delivers higher coverage limits and better pricing for elevated homes in lower-risk zones. Excess flood coverage addresses gaps that standard policies leave exposed, particularly for high-value homes where NFIP’s $250,000 dwelling cap falls short of actual replacement costs.

Assess three factors to select the right types of flood insurance for your situation: your home’s actual replacement cost, your property’s elevation and flood zone designation, and your financial capacity to absorb out-of-pocket deductibles. A Naples home valued at $350,000 in a moderate-risk zone might benefit from private flood insurance alone, while a $600,000 coastal property likely needs NFIP plus excess coverage or a high-limit private policy. Properties in the highest-risk zones often have no private option and must rely on NFIP, making that government program essential despite its limitations.

Start by obtaining your elevation certificate and confirming your flood zone through FEMA’s mapping tools, then contact an independent agent who can quote both NFIP and private carriers for comparison. We at Responsive Insurance, Inc. work with multiple A-rated insurance companies to compare coverage options and find the best fit for your specific needs. Contact us today to discuss your flood insurance strategy and receive quotes tailored to your Southwest Florida property.