Should I Get Flood Insurance in Zone X?

Zone X properties in Naples, FL aren’t automatically safe from flooding. Many homeowners assume this FEMA designation means they’re protected, but the reality is more complex.

We at Responsive Insurance, Inc. help residents understand whether they should get flood insurance in Zone X. The answer depends on your specific location, property details, and risk factors that go beyond the standard flood zone map.

What Zone X Actually Means for Your Naples Home

FEMA’s Zone X Classification System

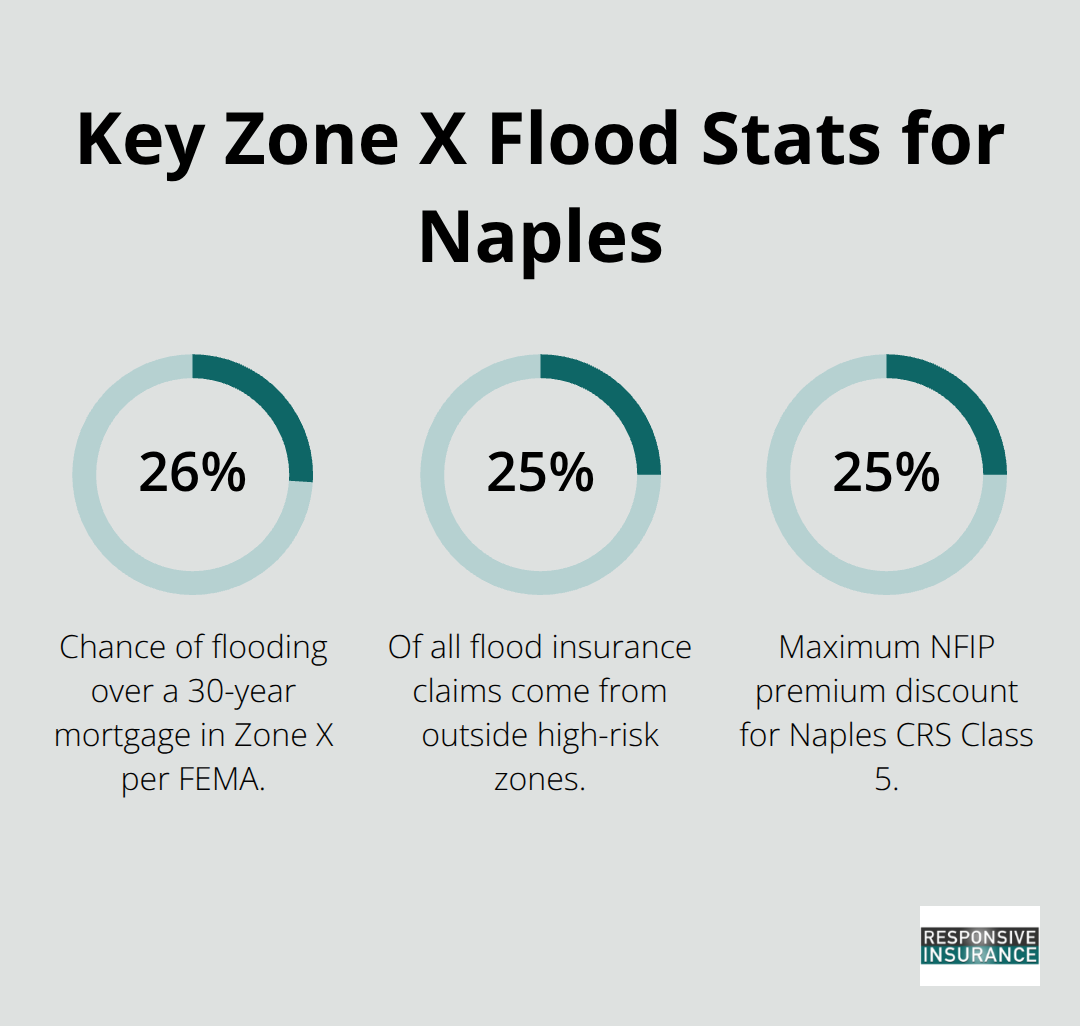

FEMA divides flood zones into categories based on statistical risk, and Zone X represents areas with lower flood probability compared to high-risk zones like AE or VE. Shaded Zone X carries a 0.2% to 1% annual flood risk, while unshaded Zone X falls below 0.2% annually. This translates to roughly a 26% chance of flooding over a 30-year mortgage period, according to FEMA data. The lower designation does not mean your property sits in a flood-proof location.

How the 2024 Maps Changed Your Risk Picture

The 2024 Flood Insurance Rate Maps now in effect for Naples provide more detailed hazard data than the 2012 maps they replaced, giving you a clearer picture of actual risk based on topography, drainage patterns, and historical events. You can check your specific zone through the City of Naples interactive flood map tool or FEMA’s Flood Map Service Center by entering your address. If the designation seems wrong, you can request a Letter of Map Amendment with FEMA to correct it, though this process requires documentation and professional assessment.

The Hidden Truth About Zone X Claims

A critical fact that many Naples homeowners miss is that roughly 25% of all flood insurance claims come from areas outside high-risk zones, meaning Zone X properties file a substantial portion of claims. Since 2000, Florida has experienced five federally declared flood disasters, and recent events like Hurricane Ian in 2022 and Hurricane Milton in 2024 caused widespread flooding across low-risk areas. Standard homeowners insurance explicitly excludes flood damage, so your existing policy provides zero protection regardless of your zone designation.

Affordable Coverage Options for Zone X Residents

The City of Naples participates in the National Flood Insurance Program and maintains a CRS Rating Class 5, which qualifies residents for up to 25% discounts on flood insurance premiums. The average flood insurance cost in Florida runs about $865 per year through NFIP, though Naples premiums typically range from roughly $1,498 to $1,508 annually depending on property specifics. For Zone X properties, NFIP Preferred Risk Policies start as low as around $39 per year for some homes, making coverage affordable even in lower-risk areas. Your specific location, property value, and coverage limits will determine your actual premium, so comparing quotes from multiple insurers reveals the true cost of protection for your situation.

When Flood Insurance Makes Sense for Zone X

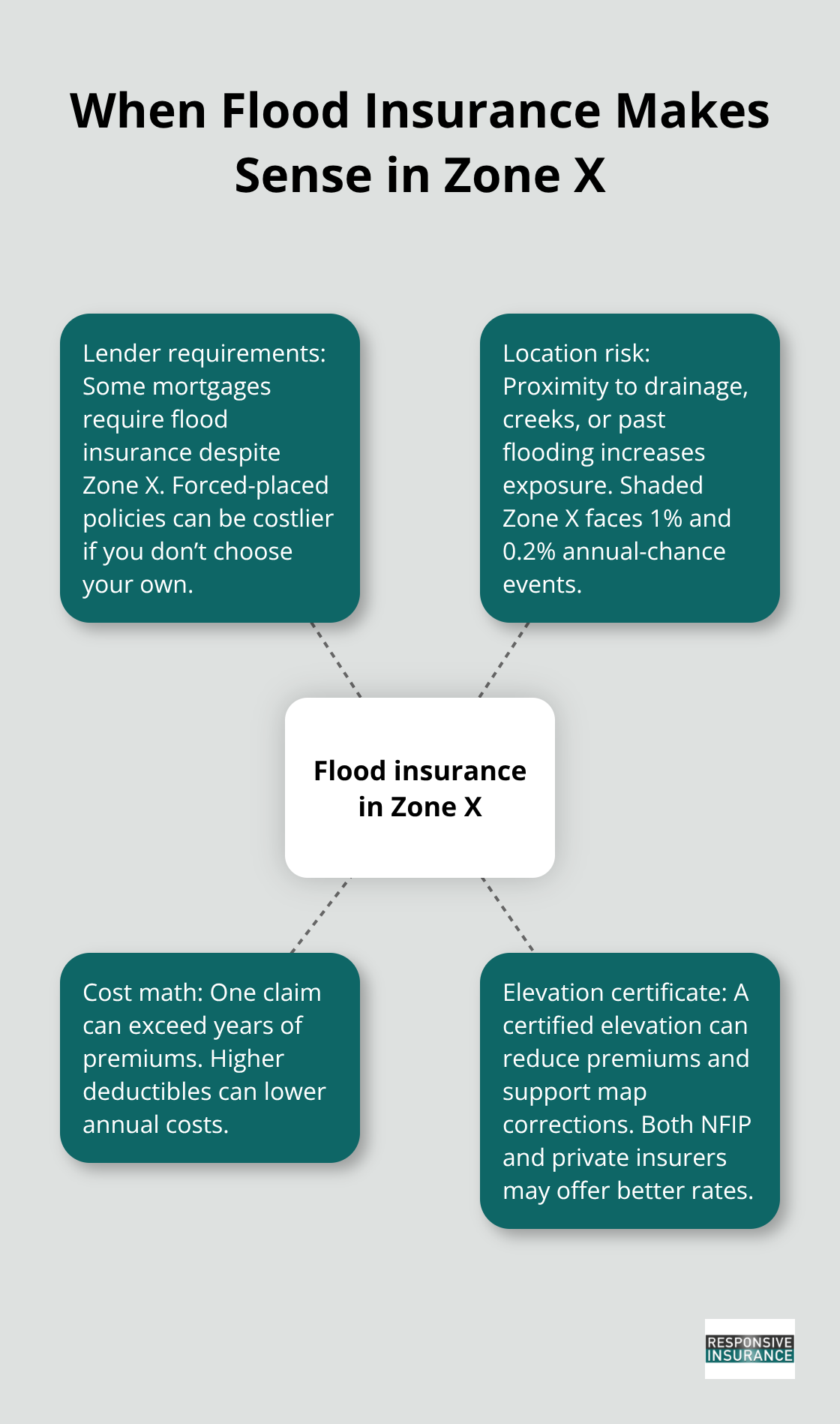

Lender Requirements Override Zone Designation

Your mortgage lender may require flood insurance regardless of your Zone X designation, particularly if your loan carries federal backing or FDIC insurance. Check your loan documents or contact your lender directly to confirm whether they mandate coverage-many lenders impose this requirement even for lower-risk zones to protect their financial interest. If your mortgage requires flood insurance, you have no choice. Lenders will force you into a policy and bill the premium to your escrow account at rates far higher than shopping independently.

Location Within Zone X Determines Real Risk

Your specific property location within Zone X determines whether insurance makes financial sense. Properties near drainage areas, within a quarter-mile of creeks or retention ponds, or in neighborhoods with historical flooding patterns face substantially higher risk than properties on elevated terrain. The City of Naples Floodplain Coordinator at 239-213-5039 can provide historical flood data for your specific address, showing whether your neighborhood experienced flooding during Hurricane Ian in 2022 or Hurricane Milton in 2024, both of which caused significant damage across supposedly low-risk areas. If your property sits in shaded Zone X rather than unshaded Zone X, FEMA calculations for flood probability in Zone X show exposure to both 1% annual-chance and 0.2% annual-chance flood events.

The Math Favors Coverage in Most Situations

One inch of floodwater causes thousands in damage, and just one claim would exceed years of premiums. NFIP Preferred Risk Policies for Zone X can cost as little as $39 annually for qualifying properties, while private insurers sometimes offer competitive rates with faster claims processing. Higher deductibles reduce your premium significantly, so choosing $5,000 or $10,000 deductibles instead of $1,000 works well if you have emergency savings to cover potential out-of-pocket costs after a flood event.

Elevation Certificates Lower Your Costs

An elevation certificate from a licensed engineer details your home’s lowest floor elevation and can significantly reduce your premium. This document proves invaluable if you later need to dispute your flood zone designation with FEMA. Properties with documented elevations often qualify for better rates across both NFIP and private options, making the upfront investment in professional assessment worthwhile.

Next Steps to Protect Your Property

Your Zone X designation does not eliminate flood risk, and the affordable coverage options available make protection accessible. Whether your lender requires it or your neighborhood’s history suggests it, the decision to obtain flood insurance protects your investment against events that standard homeowners policies explicitly exclude.

How to Evaluate Your Flood Risk and Get Coverage

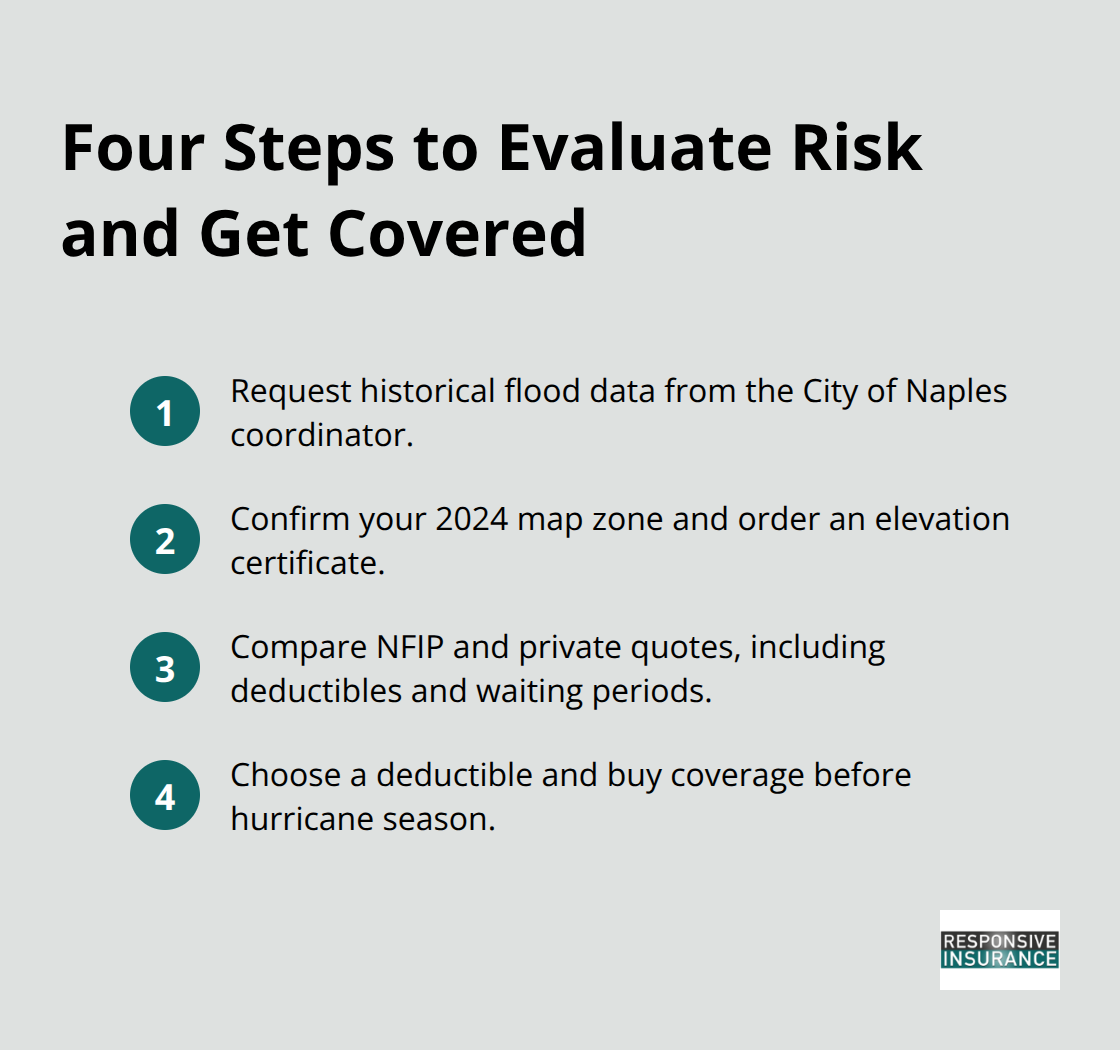

Request Historical Flood Data for Your Address

Contact the City of Naples Floodplain Coordinator at 239-213-5039 to request historical flood data for your specific address. This coordinator maintains records of flooding events in your neighborhood, including impacts from Hurricane Ian in 2022 and Hurricane Milton in 2024, and can tell you whether your street or block experienced damage during these storms. The coordinator provides concrete information about past events that affect your actual risk level, not just your zone designation.

Confirm Your Flood Zone and Obtain an Elevation Certificate

Request the 2024 Flood Insurance Rate Map for your property through FEMA’s Flood Map Service Center to confirm whether you sit in shaded Zone X (0.2% to 1% annual risk) or unshaded Zone X (below 0.2% annually), since the shaded designation carries higher actual exposure. If your property has ever been elevated or had structural work completed, hire a licensed engineer to obtain an elevation certificate. This document reduces premiums substantially and costs roughly $500 to $800. The certificate proves your home’s lowest floor elevation and qualifies you for better rates across both National Flood Insurance Program policies and private insurers.

Compare Quotes from Multiple Sources

Gather quotes from at least three sources before committing to any policy. Contact the NFIP directly at 1-888-CALL-FLOOD or visit FloodSmart to receive a Preferred Risk Policy quote if your property qualifies; these policies start around $39 annually for some Zone X homes. Request quotes from private flood insurers through the Florida Office of Insurance Regulation to compare higher coverage limits and potentially faster claims processing. Your insurance agent can help coordinate these quotes and explain the differences in deductibles, coverage limits for structure versus contents, and waiting periods-NFIP policies typically have a 30-day waiting period before coverage activates, while private insurers sometimes offer shorter windows.

Select Your Deductible and Purchase Your Policy

Choose your deductible strategically: a $1,000 deductible costs more in premium, but a $5,000 or $10,000 deductible cuts your annual cost significantly if you have emergency savings to cover that amount after a flood event. Once you select a policy, purchase it immediately rather than waiting for hurricane season, since that 30-day waiting period means coverage won’t be active if a storm arrives soon after purchase.

Final Thoughts

Zone X does not mean zero risk. Roughly 25% of all flood insurance claims come from areas outside high-risk zones, and recent hurricanes like Ian and Milton proved that lower-risk designations offer no protection against real flooding. Your FEMA zone classification reflects statistical probability, not actual safety, so the answer to “should I get flood insurance in Zone X” depends on your specific property location and lender requirements rather than your zone alone.

The math favors coverage for most homeowners. NFIP Preferred Risk Policies cost as little as $39 annually for qualifying Zone X properties, while one inch of floodwater causes thousands in damage. Standard homeowners insurance explicitly excludes flood damage, leaving you completely unprotected without a separate flood policy, and an elevation certificate reduces your premium further while higher deductibles make coverage affordable if you have emergency savings available.

Contact Responsive Insurance, Inc. to review your flood insurance needs and get a quote today. We help Naples residents evaluate their actual flood risk and find the right coverage that fits your situation. Whether your lender requires flood insurance or you want to protect your property against events that standard policies exclude, we provide guidance on your choices.