What is the Average Cost of Homeowners Insurance in Florida?

Homeowners insurance in Florida costs significantly more than in most states, and understanding why is the first step toward managing your premiums.

At Responsive Insurance, Inc., we help Naples residents navigate the unique challenges of insuring property in a high-risk hurricane zone. The average cost of homeowners insurance in Florida reflects real dangers-from coastal storms to rising replacement costs-but smart choices can lower what you pay.

What Really Drives Your Florida Insurance Bill

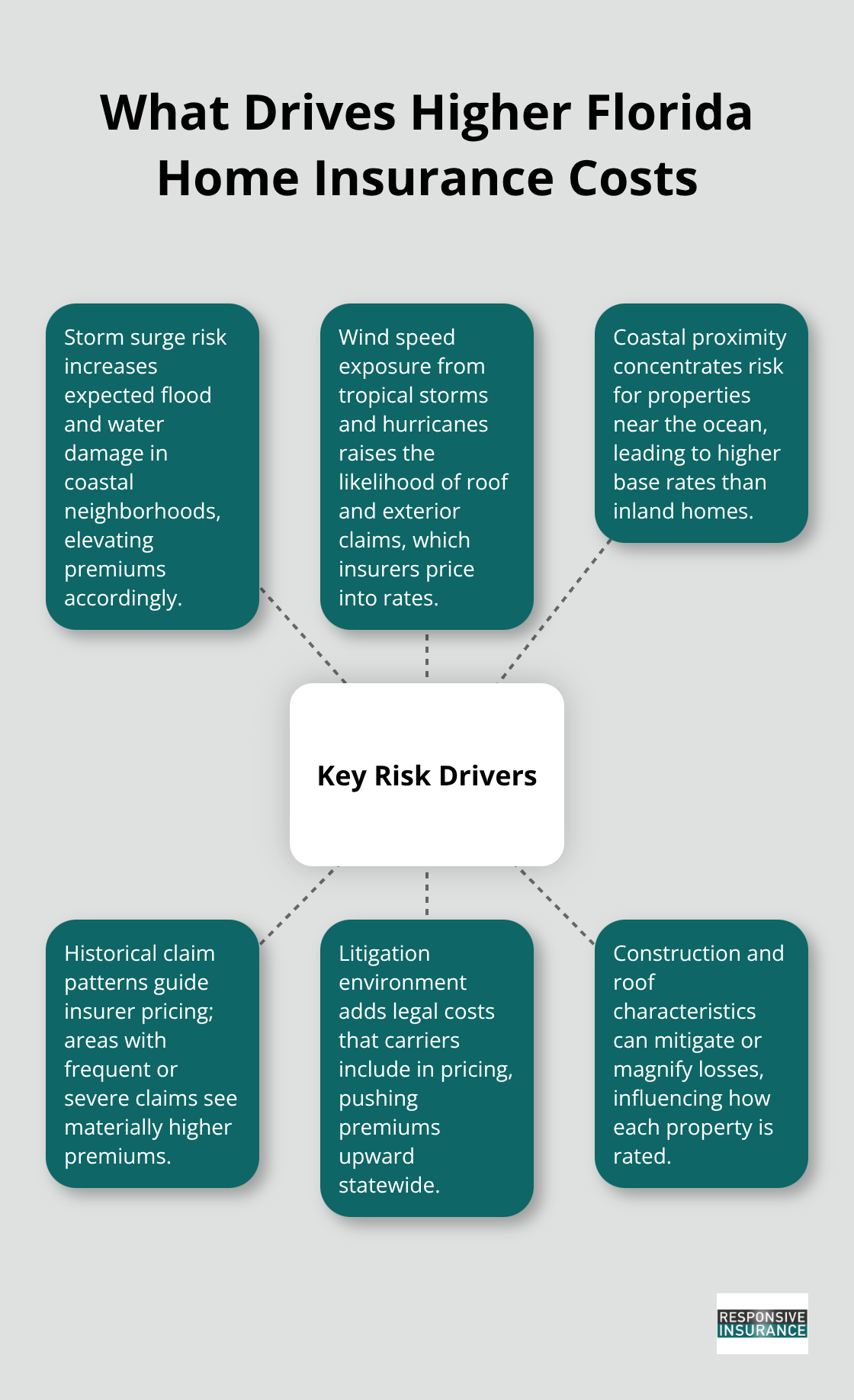

Location determines everything in Florida homeowners insurance, and coastal proximity matters far more than most people realize. If you live within a few miles of the ocean in Naples or similar coastal areas, your premiums reflect genuine hurricane and wind exposure that inland residents simply don’t face. Bankrate’s November 2025 data shows that for the same $300,000 home, West Palm Beach residents pay $8,618 annually while Fort Lauderdale homeowners pay $10,917-yet both cover identical dwelling values. The difference comes down to storm surge risk, wind speed exposure, and historical claim patterns.

A 2022 analysis by the Insurance Information Institute revealed that Florida accounts for just 9% of nationwide homeowners insurance claims but 79% of all lawsuits, driving costs higher across the board. This litigation environment affects your premium directly because insurers factor in legal expenses when pricing policies.

Home Age and Construction Quality Shape Your Rate

Older homes cost significantly more to insure because they often lack modern wind-resistant features and may have outdated roofing materials. Homes built after 2001 typically meet updated building codes designed to withstand hurricane-force winds, which can lower your premium compared to pre-2001 construction. Wind mitigation improvements like hurricane straps, hip roofs, and impact-resistant windows can reduce premiums by up to 40% for older homes according to industry data. Your roof’s age matters too-insurers often won’t cover homes with shingles older than 20 years or wood roofs beyond 15 years without significant rate increases. In Naples specifically, dwelling coverage costs escalate with home value: a $100,000 dwelling averages $851 annually, while a $500,000 dwelling averages $4,193 per year based on Policygenius data. Replacement cost directly influences what you’ll pay because insurers must account for material and labor expenses in your specific area, and those costs have risen substantially since construction material prices spiked in recent years.

Deductible Choices Create Real Savings

Your deductible decision produces the single largest premium difference available to you as a consumer. In Naples, choosing a $1,000 deductible instead of $500 cuts your annual premium by roughly $1,200-from about $3,271 to $2,046 annually. Hurricane deductibles work differently and often appear as a percentage of your home’s insured value rather than a flat amount; a 2% hurricane deductible on a $300,000 home means you pay $6,000 out-of-pocket before coverage applies. This structure exists because hurricane damage typically affects many policyholders simultaneously, and insurers need higher deductibles to manage catastrophic loss exposure. Coverage limits also directly impact your cost, so understanding what you actually need versus what you’re paying for prevents wasting money on unnecessary protection.

Flood Insurance Requires Separate Coverage

Flood insurance, which isn’t included in standard homeowners policies, requires a separate decision-and in flood-prone areas of Naples where FEMA designates high-risk zones, this becomes mandatory if you have a mortgage. The National Flood Insurance Program (NFIP) offers one option, while private insurers provide another. Some carriers like Universal Property offer private flood endorsements up to $5 million, giving you alternatives beyond the federal program. Your location within Naples matters significantly; properties in designated flood zones face higher premiums or coverage restrictions. As an independent agency, Responsive Insurance, Inc. works with multiple A-rated insurance companies to help you compare flood coverage options and find the right fit for your property’s specific risk profile. Understanding your flood risk through FEMA maps and supplementary tools like First Street Foundation helps you make informed decisions about this essential coverage. The cost of separate flood insurance varies dramatically based on your exact flood zone designation, so obtaining quotes from multiple providers reveals the true expense before you commit to a policy.

What You’ll Actually Pay for Homeowners Insurance in Florida

Florida’s Statewide Average and Regional Reality

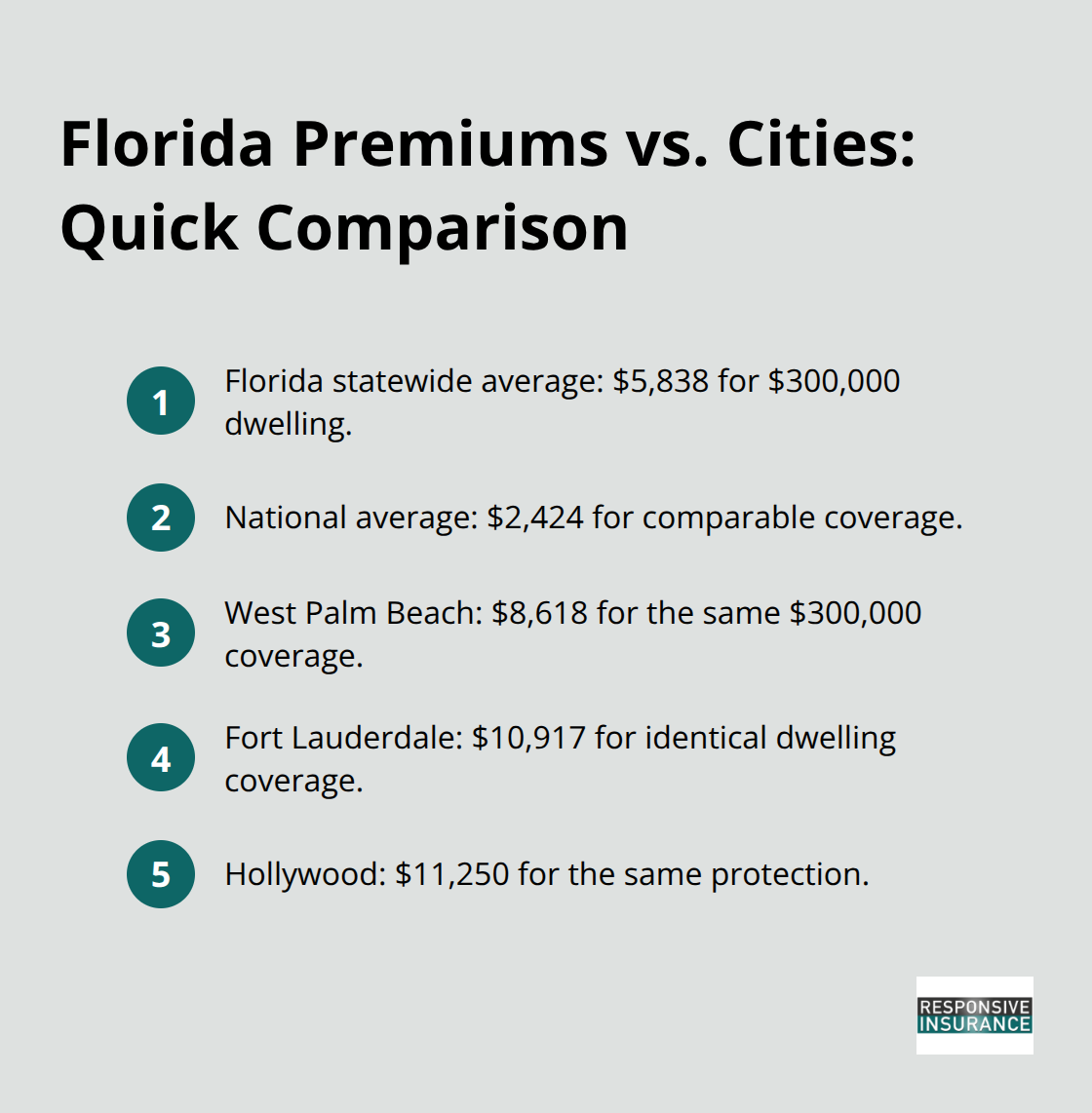

Florida’s statewide average for homeowners insurance reaches $5,838 annually for a $300,000 home, but this number masks enormous regional variation that directly affects what you pay. The $5,838 average runs roughly $3,414 higher than the national average of $2,424, making Florida one of the most expensive states for coverage. However, statewide averages reveal almost nothing about your actual cost because geography within Florida creates dramatic price swings. West Palm Beach homeowners pay $8,618 annually for identical $300,000 dwelling coverage, while Fort Lauderdale reaches $10,917 and Hollywood climbs to $11,250 for the same protection.

These aren’t minor variations-they represent fundamental differences in how insurers price risk based on coastal exposure, historical claims, and storm surge vulnerability.

How Distance from the Coast Transforms Your Premium

Moving inland changes everything: Ocala residents might pay around $1,865 annually for comparable coverage, illustrating that distance from the coast creates 400% to 500% premium differences for the same dwelling value. Naples specifically averages about $2,502 annually, which sits roughly 9% above Florida’s statewide average but remains significantly lower than coastal cities like Fort Lauderdale or Hollywood. Within Naples itself, ZIP code matters-the difference between the cheapest inspected ZIP code at $2,434 and the most expensive at $2,582 shows that even within a single city, your exact location influences your rate. This variation reflects how insurers assess wind exposure, flood risk, and historical storm damage patterns across specific neighborhoods.

Florida Versus the Nation: Why the Gap Exists

The national average of approximately $2,424 annually means Florida premiums run 140% higher overall, with coastal Florida cities running 300% to 450% above the national average. This gap exists because Florida accounts for 9% of nationwide homeowners insurance claims but generates 79% of all homeowners insurance lawsuits, which directly inflates costs across the state. Coastal areas like Fort Lauderdale and Hollywood don’t just face higher risk-they face higher litigation costs that insurers pass directly to policyholders. States like Louisiana average around $6,354, Oklahoma around $5,444, and Texas around $4,456 for the same coverage, all significantly cheaper than Florida’s coastal cities despite their own hurricane exposure. The difference comes down to claim volume and litigation patterns rather than risk alone.

Your Actual Quote Depends on Specific Property Details

For Naples residents, understanding that your $2,502 average falls between the national average and Florida’s most expensive coastal cities provides context, but your actual quote depends entirely on your specific property’s flood zone, roof age, home construction date, and distance from the ocean. Shopping quotes across multiple carriers reveals price differences of $1,000 to $3,000 annually for identical coverage in the same ZIP code, making comparison shopping the single most effective way to manage your costs regardless of regional averages. As an independent agency, Responsive Insurance, Inc. works with multiple A-rated insurance companies to help you compare quotes and find the best fit for your property’s specific risk profile. Your next step involves obtaining quotes from several carriers to see where your home actually falls within these ranges.

How to Cut Your Naples Homeowners Insurance Costs

Combine Policies for Immediate Savings

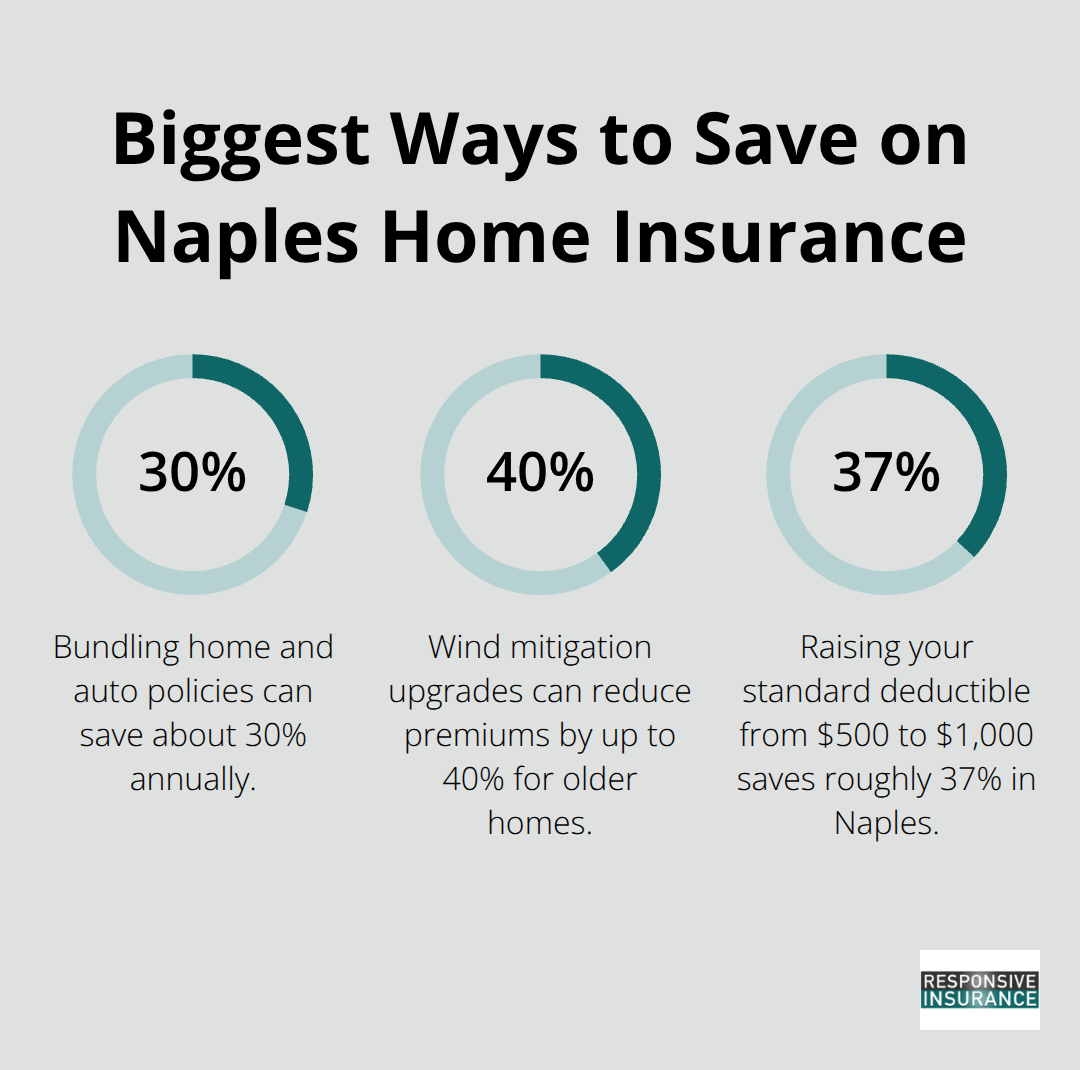

Consolidating your homeowners and auto policies with the same insurer produces immediate savings that most Naples residents overlook. Policy consolidation can save you as much as 30% each year, which on a $2,502 average Naples homeowners policy translates to substantial annual savings. If you currently pay separate homeowners and auto premiums across different carriers, moving to one insurer can save you $300 to $800 per year depending on your auto coverage level. This single decision often represents the fastest path to lower costs without sacrificing coverage.

Invest in Wind Mitigation for Maximum Savings

In coastal Florida, wind mitigation improvements deliver the most substantial savings because they directly address your region’s primary risk. Adding hurricane shutters, reinforcing garage doors, upgrading to impact-resistant windows, or installing hurricane straps can reduce premiums by up to 40% for older homes according to industry data. These aren’t cosmetic upgrades-they’re structural improvements that demonstrably reduce wind damage claims, and insurers reward them with meaningful discounts. Roof age matters enormously in Naples because wind exposure makes your roof your most vulnerable asset; if your roof approaches 20 years old, replacing it before your insurance renewal can lower your premium by 20% to 30%. Some carriers like Universal Property will insure homes with roofs up to 20 years old, while others impose stricter limits, so shopping across multiple carriers reveals which companies will offer better rates for your specific roof condition.

Safety features also qualify for discounts that reduce claim frequency: installing deadbolt locks, smoke detectors, and burglar alarms can lower your premium by 5% to 15%. These improvements cost far less than the savings they generate over time.

Adjust Your Deductible Strategy

Your deductible decision creates the largest single cost difference under your control. Increasing your standard deductible from $500 to $1,000 saves approximately $1,225 annually in Naples-roughly 37% off your premium-which means you trade $500 of additional out-of-pocket risk for $1,225 in annual savings. This math works only if you maintain an emergency fund to cover that deductible, but if you have $2,000 to $3,000 in liquid savings, the higher deductible becomes financially superior.

Hurricane deductibles operate differently and often function as a percentage of your home’s value rather than a flat amount, so increasing your standard deductible doesn’t reduce your hurricane deductible. This distinction matters significantly when you evaluate your total out-of-pocket exposure during a major storm event.

Review Coverage and Shop Regularly

Your coverage needs change as your home’s value shifts and your risk profile evolves. Contact your insurer after you make wind mitigation improvements, install a new roof, or upgrade security features to confirm you’re receiving applicable discounts-many homeowners miss savings simply because they don’t request rate reviews after property improvements. Shopping your policy across multiple carriers every two to three years uncovers rate changes in the competitive market; insurers in Naples vary from $604 annually for Security First to $6,281 for Citizens Insurance on identical coverage, proving that carrier selection matters far more than most people realize. This dramatic variation means your current insurer may no longer offer the best rate for your specific situation. Multiple quotes reveal where your home actually falls within these ranges and which carriers value your property’s characteristics most favorably.

Final Thoughts

Florida homeowners insurance costs far more than most Americans expect, but understanding the drivers behind those premiums puts you in control of your financial outcome. The average cost of homeowners insurance in Florida reflects genuine risks-hurricane exposure, litigation patterns, and rising construction costs-that justify higher premiums than inland states. Shopping around produces measurable savings because Naples carriers range from $604 to $6,281 annually for identical coverage, which means your current insurer may be charging you thousands more than competitors.

Your deductible choice and wind mitigation investments deliver the largest savings available to you without sacrificing protection. Increasing your deductible from $500 to $1,000 cuts roughly $1,200 off your annual premium, while roof replacement or hurricane shutters can reduce costs by 20% to 40%. Bundling your homeowners and auto policies saves another 30% on average, and these represent real money that stays in your pocket when you make informed choices.

We at Responsive Insurance, Inc. work with multiple A-rated insurance companies to help Naples residents compare coverage options and find policies that match both their needs and budgets. Contact us for quotes from multiple carriers, review your current coverage to confirm you’re receiving all applicable discounts, and make the deductible decision that fits your financial situation. The time you invest in this process typically returns hundreds or thousands of dollars in annual savings.

![Florida Home Insurance Quotes [2026 Guide]](https://responsiveinsurance.com/wp-content/uploads/emplibot/Florida-Home-Insurance-Quotes-_2026-Guide__1770848603-80x80.jpeg)